Transferir como PDF, PPTX

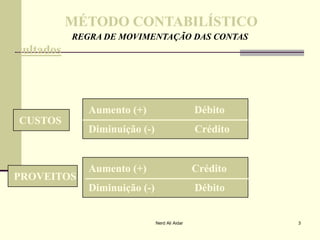

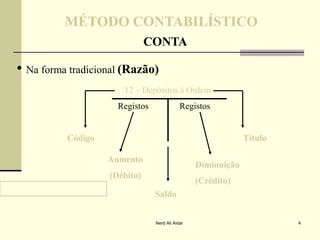

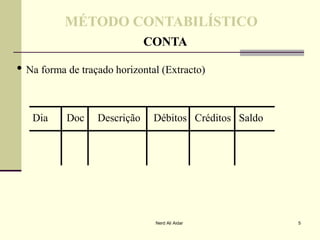

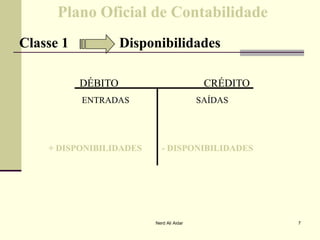

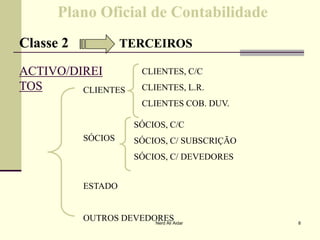

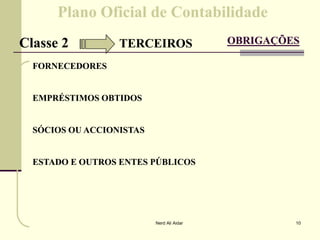

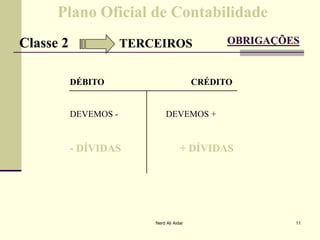

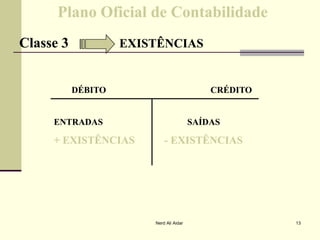

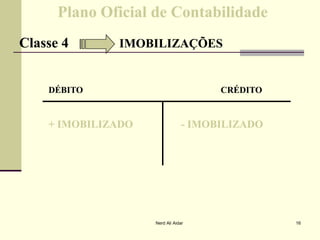

This document discusses accounting methods and the double-entry system. It explains that assets increase through debits and decrease through credits, while liabilities increase through credits and decrease through debits. It also outlines the different classes of accounts in the chart of accounts and their normal debit and credit entries.