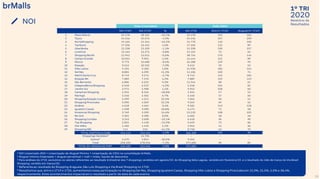

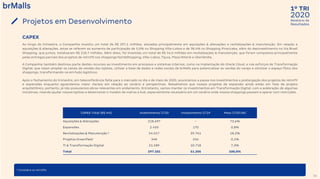

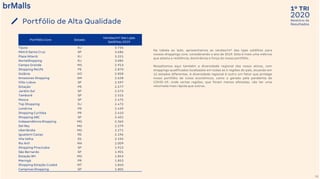

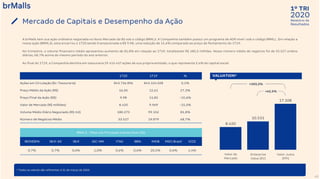

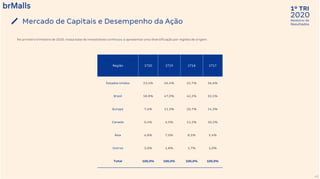

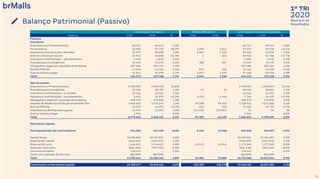

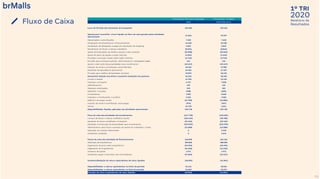

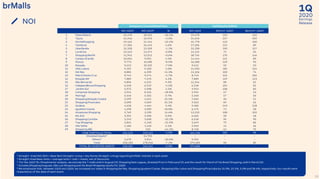

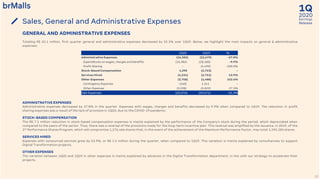

O relatório apresenta os resultados financeiros e operacionais da brMalls no primeiro trimestre de 2020. Detalha as medidas tomadas pela empresa em resposta à pandemia de COVID-19, como reduções de aluguéis e apoio a lojistas, e fornece atualizações sobre a reabertura gradual dos shoppings. Apresenta também iniciativas de responsabilidade social da brMalls para apoiar famílias afetadas pela crise.