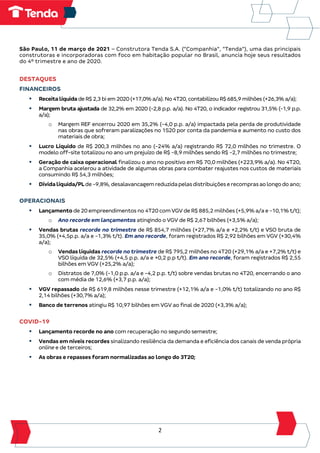

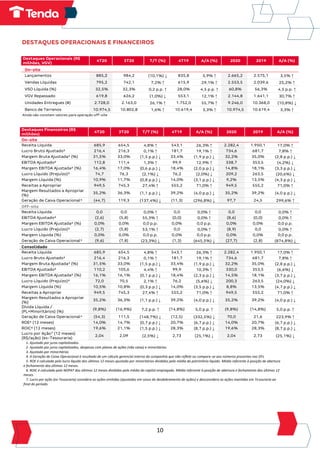

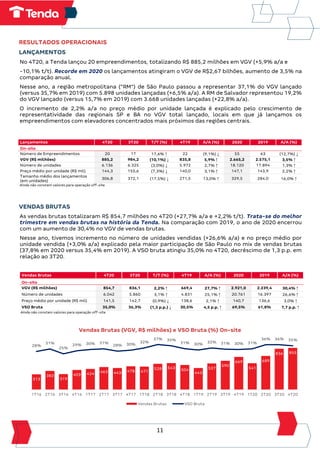

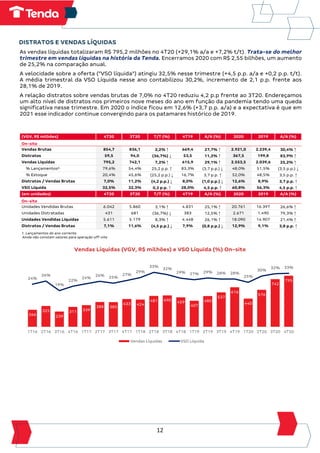

O documento relata os resultados financeiros e operacionais da construtora Tenda no quarto trimestre e ano de 2020. Destaca-se o crescimento da receita líquida em 17% no ano, mas queda do lucro líquido em 24%. As vendas e lançamentos bateram recordes, mas as margens bruta e de lucro foram impactadas negativamente pela pandemia.