Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (10)

Semelhante a CMD2012 - Mats Granryd - Tele2's strategy

Semelhante a CMD2012 - Mats Granryd - Tele2's strategy (20)

Mais de Tele2

Mais de Tele2 (20)

Último

Último (20)

CMD2012 - Mats Granryd - Tele2's strategy

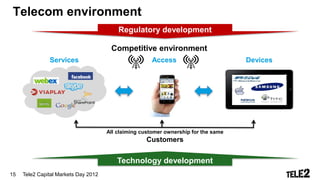

- 1. Telecom environment Regulatory development Competitive environment Services Access Devices All claiming customer ownership for the same Customers Technology development 15 Tele2 Capital Markets Day 2012

- 2. Tele2 House Vision We will be champions of customer value in everything we do Mission We are challengers, fast-movers and will always offer our customers what they need, for less Wanted Position Customers Employees Shareholders We shall be the We shall be considered a great We shall have the best TSR operator of choice place to work within our peer group Focus Areas Cost Business People Growth Differentiation Quality Leadership Model Tele2 Way 16 Tele2 Capital Markets Day 2012

- 3. Cost Business People Growth Differentiation Quality Leadership Model People Tools Tele2 Russia Leadership Performance and and Talent the Tele2 Way Tele2 Norway • Extremely low unemployment rate of 3%* Learning and Reward and • Manage the merger with low attrition Development Recognition Tele2 Sweden 17 Tele2 Capital Markets Day 2012 * Source: Statistics Norway, September 2012

- 4. Cost Business People Growth Differentiation Quality Leadership Model Engaged employees 6,633 employees* Best-in-class employee engagement Yearly survey ”MyVoice” shows 50% record high engagement levels 40% and employee satisfaction 30% 20% Tele2 10% Global Benchmark 0% 18 Tele2 Capital Markets Day 2012 * 2011, consultants, people on sick leave, newly employed etc. not included

- 5. Cost Business People Growth Differentiation Quality Leadership Model Growth Household spending on telecom in Sweden Group revenue breakdown SEK/year/ 100% household 67% growth 50,000 90% 02’-11’ 45,000 80% 31% growth 70% 40,000 02’-06’ 60% 35,000 50% 30,000 40% 25,000 30% 20,000 2007 2008 2009 2010 2011 Q3 12* 15,000 Mobile Other 10,000 5,000 Tele2 will continue to be a growth 0 company, focusing on mobile business and a good mix of mature and high Communication; fixed, mobile and Internet growth markets Source: SCB National accounts; School of Economics at Gothenburg University 19 Tele2 Capital Markets Day 2012 * Operating revenue; rolling 12 months

- 6. Cost Business People Growth Differentiation Quality Leadership Model Mobile Market Revenue Drivers FOCUS AREAS VAS by VOICE PARTNERSHIPS DATA Subscriber growth MOU APPM Infrastructure Data Device Consumption SMS/MMS/ M-Commerce Maturity Penetration Trends RBT/Games 20 Tele2 Capital Markets Day 2012

- 7. Cost Business People Growth Differentiation Quality Leadership Model From Discounter to Value Champion DISCOUNTER VALUE CHAMPION Reasons to evolve from discounter to value champion: • Less involvement in price wars to defend price position, with risk of margin erosion • Get return on quality investments • Secure customer relationships 21 Tele2 Capital Markets Day 2012

- 8. Cost Business People Growth Differentiation Quality Leadership Model From Discounter to Value Champion DISCOUNTER VALUE CHAMPION Outperform Challenger Low price in customer VALUE CHAMPION = + experience + Culture 22 Tele2 Capital Markets Day 2012

- 9. Cost Business People Growth Differentiation Quality Leadership Model Several market sector brands have moved from Purchase value to User value Price + Design Price + Choice and convenience Price + Style Price + Ease Price + Service Price + Customer experience Price + Speed and quality Designed to cater for customers who actively seek added value that builds on low price 23 Tele2 Capital Markets Day 2012

- 10. Cost Business People Growth Differentiation Quality Leadership Model From Discounter to Value Champion Discounter Best Deal Value Champion 24 Tele2 Capital Markets Day 2012

- 11. Cost Business People Growth Differentiation Quality Leadership Model Focus on customer value in all touch points Join Pay Pay 25 Tele2 Capital Markets Day 2012

- 12. Cost Business People Growth Differentiation Quality Leadership Model World Class Customer Service Average customer satisfaction with Tele2’s call centers Customer service role models 82% 80% = world class standard * 80% 78% 76% 74% 72% 70% Source: Tele2 26 Tele2 Capital Markets Day 2012 * COPC benchmarking standards

- 13. Cost Business People Growth Differentiation Quality Leadership Model Cost Leadership 33.1% 30.8% 28.0% -0.9% 27.1% 25.8% 25.6% 23.2% 23.1% 22.3% 21.7% T2 2010 T2 2011 • Tele2 continues to reduce the cost gap but is still second best • Gap to best operator group also continues to decrease • Tele2 shall become ”best in class” 27 Tele2 Capital Markets Day 2012 Source: AT&Kearney

- 14. Cost Business People Growth Differentiation Quality Leadership Model Quality Call cent. End user sat. Invoice drop accuracy First contact res. Rate Coverage perception Cat. 1 syst. Available Invoice correctness Product innovation Quality perception Mystery shopping Data completion Projects on time Call completion Cell availability Consideration Refill setup NPS Latest rep. 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 1209 period 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 SE NO RU EE LV LT HR KZ NL AT DE Rep. freq. Q Q Q M/Q Q M M M Q M M M M M M M LT resp. AO AO AO AO AO AO JH JH AO JH JH JH JH JH AO AO 28 Tele2 Capital Markets Day 2012

- 15. Cost Business People Growth Differentiation Quality Leadership Model Business model – Voice to Data WESTERN EUROPE MOBILE DATA FORECAST Monthly usage per subscriber – Sweden postpaid * Data as % of total revenue 463 60% 206 206 227 169 178 172 50% 131 21 40% MoU # of SMS Data (MB) 2010 30% 2011 ASPU Sweden postpaid 2012 20% 202 197 198 10% 0% 2008 2009 2010 2011 2012 2013 2014 2015 2016 Postpaid ASPU (SEK) Source: Analysis Mason, includes data, content and messaging revenues 29 Tele2 Capital Markets Day 2012 * Postpaid residential; MoU, nr of SMS and MB per sub per month

- 16. Cost Business People Growth Differentiation Quality Leadership Model Business model – Volume to Value Mobile handset penetration Russia Tele2 Group churn value dynamic Q1 & Q2 2012 160% 35% 140% 30% ↓ 2 p.p 120% 25% 100% 20% 80% 15% 60% 10% 40% ↓ 8 p.p 20% 5% 0% 0% 2004 2005 2006 2007 2008 2009 2010 2011 2012 Jan Feb Mar Apr Maj June Postpaid Prepaid As markets mature it becomes more important to focus on the value of each • Reduce churn of most valuable customers customer rather than the volume of • Increase value of existing customer base customers Source (LHS): Analysys Mason February 2012, Source (RHS): Tele2 30 Tele2 Capital Markets Day 2012

- 17. Cost Business People Growth Differentiation Quality Leadership Model Business model – B2B Market share residential, upside B2B and share of total turnover * ∆ Residential market share vs. B2B market share ∆ 520% 500% Sweden 400% Attractive B2B market Norway with expected growth 300% Croatia ∆ 296% Latvia 200% Lithuania ∆ 108% Russia ∆ 104% ∆ 98% 100% Estonia ∆ 73% ∆ 58% 0% 0% 10% 20% 30% 40% 50% Residential market share * The size of the circles represent share of total revenue, X axis is market share residential and 31 Tele2 Capital Markets Day 2012 Y axis is the difference between market share residential and market share B2B. Source: Tele2

- 18. Cost Business People Growth Differentiation Quality Leadership Model Business model – Distribution Customer contribution* by sales channel Group online intake (thousands of customers) 124 113 466 Index 100 69% 63 275 Branded Shops Online Other 20112011 Sept. YTD 2012 2012 Sept. YTD Focus on online and branded shops, creating the best customer lifetime revenue * Calculated as lifetime revenue subtracted by acquisition costs 32 Tele2 Capital Markets Day 2012 Source: Tele2

- 19. Tele2 House Vision We will be champions of customer value in everything we do Mission We are challengers, fast-movers and will always offer our customers what they need, for less Wanted Position Customers Employees Shareholders We shall be the We shall be considered a great We shall have the best TSR operator of choice place to work within our peer group Focus Areas Cost Business People Growth Differentiation Quality Leadership Model Tele2 Way 33 Tele2 Capital Markets Day 2012

- 20. Summary • We are the challenger of our industry • Our strategy is focused on excelling in customer relations and access capabilities • As a result, we will be able to continue growing in a shrinking European telecom market 34 Tele2 Capital Markets Day 2012 * Group figures; YTD Q3 2012