Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (17)

Destaque

Destaque (14)

Semelhante a WDR Initiation

Semelhante a WDR Initiation (20)

WDR Initiation

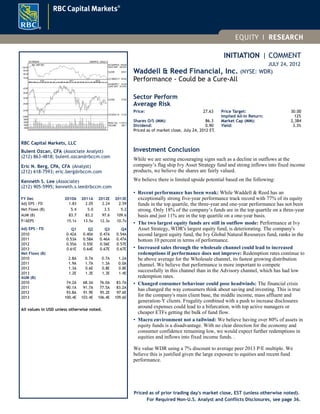

- 1. INITIATION | COMMENT JULY 24, 2012 Waddell & Reed Financial, Inc. (NYSE: WDR) Performance - Could be a Cure-All Sector Perform Average Risk Price: 27.63 Shares O/S (MM): 86.3 Dividend: 0.90 Price Target: 30.00 Implied All-In Return: 12% Market Cap (MM): 2,384 Yield: 3.3% Priced as of market close, July 24, 2012 ET. Investment Conclusion While we are seeing encouraging signs such as a decline in outflows at the company’s flag ship Ivy Asset Strategy fund and strong inflows into fixed income products, we believe the shares are fairly valued. We believe there is limited upside potential based on the following: • Recent performance has been weak: While Waddell & Reed has an exceptionally strong five-year performance track record with 77% of its equity funds in the top quartile, the three-year and one-year performance has not been strong. Only 18% of the company’s funds are in the top quartile on a three-year basis and just 11% are in the top quartile on a one-year basis. • The two largest equity funds are still in outflow mode: Performance at Ivy Asset Strategy, WDR's largest equity fund, is deteriorating. The company's second largest equity fund, the Ivy Global Natural Resources fund, ranks in the bottom 10 percent in terms of performance. • Increased sales through the wholesale channel could lead to increased redemptions if performance does not improve: Redemption rates continue to be above average for the Wholesale channel, its fastest growing distribution channel. We believe that performance is more important to compete successfully in this channel than in the Advisory channel, which has had low redemption rates. • Changed consumer behaviour could pose headwinds: The financial crisis has changed the way consumers think about saving and investing. This is true for the company's main client base, the middle income, mass affluent and generation-Y clients. Frugality combined with a push to increase disclosures around expenses could lead to a bifurcation, with top active managers or cheaper ETFs getting the bulk of fund flow. • Macro environment not a tailwind: We believe having over 80% of assets in equity funds is a disadvantage. With no clear direction for the economy and consumer confidence remaining low, we would expect further redemptions in equities and inflows into fixed income funds. . We value WDR using a 7% discount to average peer 2013 P/E multiple. We believe this is justified given the large exposure to equities and recent fund performance. Priced as of prior trading day's market close, EST (unless otherwise noted). 125 WEEKS 12MAR10 - 23JUL12 24.00 28.00 32.00 36.00 40.00 M A M J J A S O N 2010 D J F M A M J J A S O N 2011 D J F M A M J J 2012 HI-08APR11 42.49 LO/HI DIFF 97.44% CLOSE 27.84 LO-02JUL10 21.52 2000 4000 6000 8000 10000 PEAK VOL. 11107.8 VOLUME 393.1 70.00 80.00 90.00 100.00 Rel. S&P 500 HI-23APR10 106.58 HI/LO DIFF -38.22% CLOSE 68.91 LO-30DEC11 65.84 RBC Capital Markets, LLC Bulent Ozcan, CFA (Associate Analyst) (212) 863-4818; bulent.ozcan@rbccm.com Eric N. Berg, CPA, CFA (Analyst) (212) 618-7593; eric.berg@rbccm.com Kenneth S. Lee (Associate) (212) 905-5995; kenneth.s.lee@rbccm.com FY Dec 2010A 2011A 2012E 2013E Adj EPS - FD 1.83 2.05 2.24 2.59 Net Flows (B) 5.4 5.0 3.5 5.2 AUM (B) 83.7 83.2 97.6 109.6 P/AEPS 15.1x 13.5x 12.3x 10.7x Adj EPS - FD Q1 Q2 Q3 Q4 2010 0.42A 0.40A 0.47A 0.54A 2011 0.53A 0.58A 0.46A 0.47A 2012 0.55A 0.55E 0.56E 0.57E 2013 0.61E 0.64E 0.67E 0.67E Net Flows (B) 2010 2.8A 0.7A 0.7A 1.2A 2011 1.9A 1.7A 1.3A 0.0A 2012 1.3A 0.6E 0.8E 0.8E 2013 1.2E 1.3E 1.3E 1.4E AUM (B) 2010 74.2A 68.3A 76.0A 83.7A 2011 90.1A 91.7A 77.5A 83.2A 2012 93.8A 91.9E 95.2E 97.6E 2013 100.4E 103.4E 106.4E 109.6E All values in USD unless otherwise noted. For Required Non-U.S. Analyst and Conflicts Disclosures, see page 36.

- 2. 2 Investment Summary We are initiating coverage of Waddell & Reed with a Sector Perform, Average Risk rating and a $30 price target. We view the following favourably: Equity fund outflows have declined significantly over the previous quarter. Waddell & Reed reported outflows of $1 billion from its equity funds in the December quarter. As of March 31, 2012, outflows had declined to $71 million. Outflows were only a fraction of what the industry experience had been (as a percentage of beginning account values). We project positive flows for the second quarter of 2012. Waddell & Reed has generated very strong organic growth in its fixed income franchise. Fixed income funds are just a small part of its business. However, we like the fact that the company seems to be able to appeal to fixed income investors, offsetting equities outflows experienced over the past two quarters. Waddell & Reed has very strong long-term fund performance as measured over a five-year period. Based on Lipper, 77% of its equity funds have ranked in the top quartile of their respective peer groups and 88% have ranked in the top half. These are impressive results. There are initiatives underway which could help Waddell & Reed attract additional assets. It is deepening its relationships with independent distributors and regional broker/dealers such as LPL and Edward Jones. Management stated that WDR is in a nascent state with some of the largest distributors. It is using hybrid wholesalers to increase market share. There is potential to grow assets. However, there are challenges the company faces which lead us to believe that the shares are fully priced at current levels: Short term performance has been weak. While Waddell & Reed has an exceptionally strong five-year performance track record, the three-year and one-year performance have not been strong. Only 18% of the company’s equity funds are in the top quartile on a three-year basis and just 11% are in the top quartile on a one-year basis. WDR’s two largest equity funds are still in outflow mode. Performance at Ivy Asset Strategy is deteriorating, based on the latest Morningstar data. WDR’s second largest equity fund, the Ivy Global Natural Resources fund continues to generate inadequate performance, with 90% of its peers outperforming the fund. Redemption rates continue to be above average for the Wholesale channel, WDR’s fastest growing distribution channel. We believe that performance is becoming increasingly important to retaining and growing assets in this channel. The company’s “captive” sales force (Advisory channel) has had low redemption rates, in comparison. We think there is little loyalty in the Wholesale channel as advisors chase performance. We believe that a change in consumer behaviour could pose headwinds for the company on two fronts. The financial crisis has impacted its core customer base, the middle income and mass affluent, more than that of its competitors. Having seen their wealth dissipate, we believe these customers have become more cost conscious and are in need of strong performance. ETFs are a cheaper option if performance lags. The company’s upcoming customer base, generation Y, has fewer resources than previous generations and is more technologically savvy. They might rely less on brokers and advisors and choose instead to buy directly. One way WDR could differentiate itself would be to through strong performance. Given the state of the economy and investor sentiment, having over 80% of assets tied to equity funds could be a disadvantage. With consumer confidence remaining low, economic growth declining globally and Europe working very slowly through its issues, equity funds could see an increase in redemption requests. Waddell & Reed Financial, Inc.July 24, 2012

- 3. 3 Company Overview Waddell & Reed, Inc., founded in 1937, is one of the oldest mutual fund companies in the United States, having introduced the Waddell & Reed Advisors Group of Mutual Funds in 1940. Waddell & Reed Financial, Inc. provides investment advisory, distribution and administrative services. It operates its business through three distinct distribution channels: Advisors channel, Wholesale channel and Institutional channel. The Advisors channel focuses on financial planning, serving primarily middle class and mass affluent clients. The Wholesale channel's activities include retail fund distribution through broker/dealers, registered investment advisors and retirement and insurance platforms. The Institutional channel manages assets in a variety of investment styles for a variety of types of institutions. Exhibit 1: Waddell & Reed Snapshot Waddell & Reed Headquarters Overland Park, KS Total AUM $93.8 bn Major Brands Ivy Funds, Waddell & Reed % retail funds AUM rated 4-5 stars by Morningstar 13% Signature Active investment manager with captive sales force Source: Company filings; RBC Capital Markets Valuation The asset managers are currently trading at 12.3x calendar-year 2013 estimated earnings. Over the past 10 years, Waddell & Reed has been trading at a 7% discount to peers. We believe that the discount is still justified given the company’s large exposure to equity funds and the weak performance of its two largest funds. We arrive at our price target using a price-to-earnings multiple of 11.4x, which represents a 7% discount to the company’s peers and our 2013 calendar year earnings estimate of $2.59 per share. Our price target is $30. Exhibit 2: WDR’s Forward Looking P/E Relative to RBC Asset Managers Index 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x 1.0x 1.1x 1.2x 1.3x Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Note: RBC Asset Managers Index includes BLK, EV, IVZ, LM, TROW, WDR, BEN, JNS, AB, ART, AMG, CNS, CLMS, GBL, PZN Source: Bloomberg; RBC Capital Markets Waddell & Reed Financial, Inc.July 24, 2012

- 4. 4 Ownership Exhibit 3: Top 10 Holders Position Mkt Val Ultimate Holder ('000) (MM) % OS FMR LLC 7,073 208 8.2 BlackRock, Inc. 4,330 127 5.0 The Vanguard Group, Inc. 4,120 121 4.8 Wellington Management Co. LLP 3,536 104 4.1 Atlanta Life Financial Group 3,041 89 3.5 Kornitzer Capital Management, Inc. 3,016 89 3.5 Affiliated Managers Group, Inc. 2,760 81 3.2 Fisher Asset Management LLC 2,611 77 3.0 Legg Mason, Inc. 2,347 69 2.7 State Street Corp. 2,000 59 2.3 Source: FactSet Exhibit 4: Ownership by Region Position Mkt Val Global Region ('000) (MM) % OS North America 73,243 2,155 84.8 Europe 2,734 80 3.2 Pacific 47 1 0.1 Asia 4 0 0.0 Middle East 4 0 0.0 Source: FactSet Waddell & Reed Financial, Inc.July 24, 2012

- 5. 5 Investment Thesis & Analysis We are initiating coverage on Waddell & Reed with a Sector Perform, Average risk rating. We believe that strong past performance and a dedicated “captive” sales force helped the company navigate through the financial crisis – despite the company’s large exposure to equity funds and the recent performance of its funds. Yet, we see limited upside potential for the shares as we believe there are obstacle the company need to overcome, with the largest being fund performance. At the same time, one cannot be overly pessimistic about Waddell & Reed’s prospects. For the purpose of this initiation note, we have focused on areas for improvement instead of weighing the positive against the negatives. We believe the Investment Summary provides a balanced overview in a succinct way. Assuming that investors are familiar with the Waddell & Reed story, we instead focus on variables we use to measure the company. These could influence our thinking about the company in the future. We discuss our concerns in detail below: Recent Performance Lags Peers In our opinion, the biggest issue the company faces is performance. Recent performance has not been strong and absent an improvement, assets under management could decrease due to outflows. We would like to acknowledge that Waddell & Reed funds have had an immensely strong track record. Consider this: About 77% of its equity funds are ranked by Lipper in the top quartile for a five-year period. Furthermore, the company’s funds have held top spots in Barron’s “Best Mutual Fund Families” rankings, with Ivy Funds being the top performer for two years in a row. This is encouraging to us. Exhibit 5: Barron’s Five-year Performance Rankings Year Ended Waddell & Reed Ivy Funds 2011 (53 firms) 2 1 2010 (54 firms) 2 1 2009 (54 firms) 1 2 2008 (53 firms) 1 3 Source: Company Web site, Barron’s However, the saying goes that past performance is not a guarantee of future results; and we think Waddell & Reed is no exception to this rule. Our concern is that recent weak recent performance, coupled with a change in the behaviour of its client base, could ultimately lead to a structural break. Waddell & Read has enjoyed the benefits of low redemption rates due to the fact that its client base preferred to purchase funds through the captive Advisor channel. These advisors preferred to sell WDR funds and keep the assets with the company. This was not problematic in the past because fund performance had been good. We believe that it might not be appropriate to operate on the assumption that retention levels will always remain strong. We may be moving into a period where Waddell & Reed’s organic AUM growth rate could converge with the industry’s. Exhibit 6 depicts this trend. It shows that over the past three years, the organic (annualized) growth rate of WDR’s equity fund franchise has started to converge with the industry growth rate. Waddell & Reed Financial, Inc.July 24, 2012

- 6. 6 Exhibit 6: Recent Annualized Organic Growth Resembles that of the Industry (10%) (5%) 0% 5% 10% 15% 20% 25% 30% 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 US Domiciled Funds Waddell & Reed Source: Company reports, Morningstar, RBC Capital Markets We will discuss in greater detail as to why this might have happened in the section titles “Wholesale Channel Generates Sales, but Retaining Assets could be a Problem”. We believe that weak fund performance over the past 3 years is one of the biggest contributors to this trend. More recent results have trailed its peers. We assessed performance at Waddell & Reed, focusing on the company’s top 10 funds. Our reasoning is that the largest funds and their respective performance should have the largest impact on organic growth and on earnings. Our findings based on our analysis: Performance has been not only mediocre for the most part, but the company has seen increased performance volatility. Although the fixed income funds seem to be gaining traction, we don’t see the same progress for the equities offering. This is how we got there: Using Morningstar Direct, we downloaded data for all funds offered and split the universe into two categories: equity funds and fixed income funds. We then eliminated ETFs, indexed funds, alternative funds, commodities funds, money market, and funds which invest in properties only. We eliminated funds which are part of an insurance product offering, as the asset management company has little control over the ultimate cost structure of the variable annuity or the variable life product being offered. We then weighted the rankings of the funds versus their peers using the individual rankings of the underlying share classes offered within the top 10 funds by their net asset value. That is, we weighted the rankings by the size of the share class within the subgroup of 10 funds. The exhibits below plot the ranking for the one-, three- and five-year periods. Understanding that investors and consultants/advisors are focused on three- and five-year performance, we felt it was important to look at the one-year performance, as it can serve as an indication of where the three- and five-year performance may head. While the five-year performance was good – as we would have expected based on the awards the company has received for its Ivy and Waddell & Reed funds – we are concerned about recent performance. Specifically, the top 10 equity funds underperformed on a one- and three-year basis. This is a concern since Waddell & Reed is known for its equity funds, with over 80% of assets under management in this asset class. Waddell & Reed Financial, Inc.July 24, 2012

- 7. 7 Exhibit 7: One-year Performance of the top 10 Funds 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% M ay-03 M ay-04 M ay-05 M ay-06 M ay-07 M ay-08 M ay-09 M ay-10 M ay-11 Equities Fixed Income 50 Percentile Source: Morningstar, RBC Capital Markets Although Waddell & Reed’s funds were performing well at the onset of the financial crisis, beating the majority of their peers, performance deteriorated relatively quickly in mid-2009. At one point, over 80% of their peers were outperforming WDR’s top 10 equity funds, on average. The main culprits were the Asset Strategy and Global Natural Resources funds, which we cover in more detail later in this note. Despite a promising early 2011, later results were weak – and the most recent trend is not encouraging either. While there has been an improvement in the performance of fixed income funds, equity funds continue to be mediocre. Exhibit 8: Three-year Performance of the top 10 Funds 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11 Equities Fixed Income 50 Percentile Source: Morningstar, RBC Capital Markets Our concern is that the three-year performance could remain below its peers unless the one-year performance improves. Given the volatility in performance on a one-year basis, it is difficult to get a sense of where performance on a three-year basis is heading. What we know is that on an asset-weighted basis, April 2012 figures show that, on average, the top 10 equity funds underperformed more than 70% of their peers. Both fixed income and equity funds are lagging the majority of their peers. If performance does not improve, we would expect this trend to impact the five-year numbers as better performance numbers roll off. Good Bad Good Bad Waddell & Reed Financial, Inc.July 24, 2012

- 8. 8 Exhibit 9: Five-year Performance of the top 10 Funds 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11 Equities Fixed Income 50 Percentile Source: Morningstar, RBC Capital Markets On a five-year basis, Waddell & Reed benefits from the strength of previous years. Equity funds are outperforming 80% of their peers while fixed income funds are easily outperforming three-quarters of their peers. However, it is just a question of time until more recent three-year numbers roll into the five-year figures, diluting previous accomplishments. This could impact future sales and flows, unless we see meaningful progress. Could we have arrived at a different conclusion if we looked at a larger subset instead of the top 10 funds? We don’t believe so. Exhibit 10 shows the percentage of retail funds with a four- or five-star rating based on Morningstar data. The subset is composed of retail open-end funds excluding ETFs and index funds. The results appear consistent with our previous analysis. Exhibit 10: Percentage of Retail Funds with Four- or Five-Star Morningstar Ratings 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Source: Morningstar, RBC Capital Markets We believe that improved performance in the company’s fixed income funds is of lesser importance as they comprise less than 20% of total assets under management. Fixed income funds simply don’t have the same impact on earnings as equity funds. Good Bad Waddell & Reed Financial, Inc.July 24, 2012

- 9. 9 Waddell & Reed’s Largest Equity Funds are Still in Outflow Mode Positive flows into smaller, more successful funds could be more than offset by the outflows from Waddell & Reed’s two largest equity funds. Absent a market rally, growing equity fund AUM could be a challenge. We believe we could see continued outflows from Waddell & Reed’s largest equity funds, based on the one-year performance numbers we obtained using Morningstar. Once again, performance at Ivy Asset Strategy, Waddell & Reed’s largest equity fund with $33 billion in combined AUM, has deteriorated. This is important as the fund comprises about 35% of total assets under management. Performance had been improving in early 2012, with Ivy Asset Strategy and Waddell & Reed Asset Strategy in the top 50% percentile of Morningstar’s one-year ranking in the March quarter. However, recent results show that management could not hang on to the performance. As of May 2012, the fund was ranking in the bottom 30%. Exhibit 11: Outflows at Ivy Asset Strategy Accelerating Once Again ($1,000m) ($500m) $0 $500m $1,000m $1,500m $2,000m $2,500m Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Source: Morningstar, RBC Capital Markets The deteriorating trend continued into June with the fund ranking in the bottom 20% of its peers, according to Morningstar. A comment analysts hear frequently is that underperformance is based on certain styles doing better during certain economic cycles. We have looked at the one-year performance of the Asset Strategy fund and compared it against the S&P 500 to see if there was a trend we could identify in macro events which could explain the fund’s performance. Waddell & Reed Financial, Inc.July 24, 2012

- 10. 10 Exhibit 12: Ranking of Ivy Asset Strategy Fund and Level of S&P 500 0 10 20 30 40 50 60 70 80 90 100 May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11 MorningstarRanking 0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 S&P500 Ivy Asset Strategy Ranking (LHS) S&P 500 (RHS) Source: Morningstar, RBC Capital Markets We could not identify a correlation between the two, which in our view points to the fund’s performance being primarily driven by stock selection and not by economic cycles. This makes sense to us. The Asset Strategy fund can invest in various asset classes, short stocks and use derivatives. Managers can use hedges to protect against downturns. Therefore, we believe performance is dependent on the portfolio manager’s ability to choose winners. As for the Ivy Global Natural Resources fund, Waddell & Reed’s second largest equity fund with almost $4 billion in AUM, performance remains in the bottom 10%. The company announced during the most recent earnings call that the Global Natural Resources fund had been removed from a model portfolio at a broker- dealer, with performance being cited as the reason. We think this could lead to further outflows. We compared the trend in ranking of the Ivy Global Natural Resources fund based on one-year performance and the trend in the S&P 500 and came to a similar conclusion. There seems to be little correlation between the ranking of the fund and the broader market. The culprit in the underperformance appears to us to be stock selection, again. Exhibit 13: Ranking of Ivy Global Natural Resources Fund and Level of S&P 500 0 10 20 30 40 50 60 70 80 90 100 May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11 MorningstarRanking 0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 S&P500 Ivy Global Natural Resources (LHS) S&P 500 (RHS) Source: Morningstar, RBC Capital Markets Good Bad Good Bad Waddell & Reed Financial, Inc.July 24, 2012

- 11. 11 Exhibit 14 indicates the outflows of the Ivy Global Natural Resources fund. We believe that unless performance improves, we would not expect any major improvements in flows. Exhibit 14: Outflows at Ivy Global Natural Resources Fund Remains High ($400m) ($300m) ($200m) ($100m) $0 $100m $200m $300m $400m Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Source: Morningstar, RBC Capital Markets Thus, we would expect continued outflows out of the company’s largest equity funds as we do not see an improvement in performance. This, in turn, will hold back growth of assets under management and earnings. Wholesale Channel Generates Sales, but Retaining Assets could be a Problem With the Wholesale channel sales more prominently impacting total assets under management, we believe that redemption rates could increase. Furthermore, strong fund performance should become imperative in retaining assets. We believe that performance could become even more important in the future, as more sales are being generated by the Wholesale channel. As management has indicated, redemption rates continue to be above industry average for the Wholesale channel, Waddell & Reed’s fastest growing distribution channel. The Wholesale channel serves clients through all the major wire houses, regional and independent broker/dealers. It distributes its retail funds through registered broker/dealers, investment advisors and retirement and insurance platforms in the Wholesale channel. These distributors could be less loyal to certain fund families and more focused on selling the hottest and best performing funds. With the advent of no load retail funds, the cost of switching funds has been minimized for investors as well as advisors This is in stark contrast to the Advisor channel, which comprises Waddell & Reed’s “independent financial advisors”. It enjoys one of the lowest redemption rates in the industry, according to the company. The Advisor channel provides financial planning services to middle income and mass affluent clients. While there is an open-architecture environment, advisors sell predominantly Waddell & Reed products and join the company right out of college or are career changers who have a vested interest in Waddell & Reed doing well (equity compensation is a part of the company’s strategy to retain the most productive agents). The wash rate is high with only 30% of applicants becoming careers advisors. However, if applicants “make the cut”, they are offered extensive support, which builds loyalty. Advisors are managed by eight regional vice presidents, about 100 managing principals and more than 100 district managers. Thus, while remaining independent, advisors are still influenced by corporate headquarters. Management said that assets remain much longer on their books than for competitors who do not have a network of financial advisors selling their product. We believe the company’s asset retention could be two to three times longer than competitors’. Waddell & Reed Financial, Inc.July 24, 2012

- 12. 12 The importance of the Wholesale channel has increased in recent years. While about 37% of assets under management were attributed to the Wholesale channel as of the beginning of 2009, about 50% of assets were raised by the Wholesale channel as of the first quarter of 2012. Exhibit 15: Wholesale Channel Dominates Sales 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 Wholesale Channel Advisory Channel Institutional Channel Source: Company reports, RBC Capital Markets In 2003, Waddell & Reed had six wholesalers. Today, it has more than 50 wholesalers and it wants to expand. As management put it, it has been late to the Wholesale channel, with other tier 1 firms having sold through the Wholesale channel for much longer. We believe that there are advantages to being late to this channel as demonstrated by the high redemption rates. We believe that performance could be even more important to compete in the Wholesale channel compared to the Advisor channel. Exhibit 16 compares redemption rates across various distribution channels. Exhibit 16: Redemption Rates by Distribution Channel 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 Advisors Wholesale Institutional Source: Company reports, RBC Capital Markets Waddell & Reed Financial, Inc.July 24, 2012

- 13. 13 While Waddell & Reed is broadening its distribution, in a sense, we think it is also reducing the quality of the assets it is attracting. We believe that a decline in asset retention rates could be a direct result of increased sales through the Wholesale channel. We believe that the spikes in redemptions seen over the past three quarter in the Wholesale channel could be the result of weak fund performance. Changing Demographics and Consumer Behaviour Could Present Headwinds With the core customer base (the middle income and mass affluent) becoming more cost conscious and the upcoming customer base (generation Y) relying less on guidance by advisors, benefits of having a captive sales force could evaporate. Outflows could increase. Waddell & Reed prides itself on providing financial planning to the middle income and mass affluent market. We believe that the financial crisis has impacted Americans as they have seen a decline in real and perceived wealth. In a sense, individuals who would have considered themselves “mass affluent” just five years ago are now most likely considering themselves middle income. We believe that recent changes in consumer behavior coupled with changes in demographics could lead to higher redemption rates at Waddell & Reed. The financial crisis has changed the way investors think about saving and investing. Risk aversion has increased, especially in the middle income market, which comprises over 80% of Waddell & Reeds assets under management. Financial concerns have risen as perceived wealth declined among the middle income and mass affluent clients. The 2012 Merrill Edge Report, which investigates the financial priorities and concerns of the mass affluent market, identifies rising health care costs and not outliving retirement assets as the top two financial concerns of the mass affluent. Exhibit 17: Greatest Financial Concerns of Mass Affluent 73% 72% 74% 70% 52% 89% 83% 80% 80% 61% 45% 83% N/A 46% 45% 75% 49% 49% 0% 20% 40% 60% 80% 100% Rising health care costs Outliving retirement assets Affording the lifestyle I want in retirement Impact of the economy Impact of tax reform Financially supporting my family, including my parents or adult children Current amount of personal debt Caring for an aging parent and/or adult children Rising cost of college Nov. 11 Apr. 12 Source: April 2012 Merrill Edge Report Asking the same set of questions of the subgroup generation Y (defined as people between the ages of 18 and 34 in the Merrill Edge Report), Waddell & Reed’s upcoming client base, outliving retirement assets is an even bigger concern than for the overall mass affluent group. Waddell & Reed Financial, Inc.July 24, 2012

- 14. 14 Exhibit 18: Greatest Financial Concerns of Generation Y 70% 66% 69% 93% 92% 92% 89% N/A 61% 84% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100 % Outliving retirement assets Financially supporting my family, including my parents or adult children Rising health care costs Affording the lifestyle I want in retirement Impact of economy to meet financial goals Nov. 11 Apr. 12 Source: April 2012 Merrill Edge Report These exhibits indicate that saving for retirement has become more important that it was even just six months ago and that the younger generation is even more concerned about retirement and more focused on achieving financial stability than previous generations. An article published by Bloomberg Businessweek titled “Young Consumers Pinch Their Pennies” (March 22, 2012) shows that in 2009, households led by someone below 35 had 68% less inflation-adjusted wealth than households led by those younger than 35 in 1984. Consequently, we believe there is a new frugality and value consciousness. Consider this: The same article says that 45% of generation Y-ers have reduced their driving versus 24% of those 55 years and older. Having lived through a severe economic recession, their behavior is different from that of generation X (35 to 50 years of age) and the baby boomers (51 years of age and above). We believe that paying off debt has become more important to Generation Y than buying a new car or a second home. According to Richard Mason, president of corporate markets for ING US Retirement, ING’s research shows that generation Y has entered the work force with more college debt than its parents. We believe that a forced frugality combined with an increase in tech savvy could change the way investment decisions are made. Traditional investors, especially in the middle income class, typically preferred to deal with their financial advisor when making financial planning or investment decisions. Generation Y, which we believe to be financially smart, having lived through the crisis and expecting more given their limited resources, could be inclined to cut the middle man. We believe this generation could be selective when allocating assets and that asset managers who do not deliver strong results might simply not appeal to them. It appears to us that Generation Y does not often trust the market and frequently questions the status quo, which is why it is sometimes called Generation “Why”. We think this too should not come as a surprise. The following exhibit shows that active management has not been an effective way to protect assets from the financial crisis: Waddell & Reed Financial, Inc.July 24, 2012

- 15. 15 Exhibit 19: Years Majority of Actively Managed Funds Beat Benchmarks 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Number of funds with positive excess returns 1,559 1,653 1,517 1,687 2,196 1,481 2,232 1,995 3,169 2,491 1,742 Number of funds with data 3,153 3,333 3,503 3,700 3,921 4,232 4,600 4,946 5,275 5,513 5,748 % of funds beating benchmark 49.4% 49.6% 43.3% 45.6% 56.0% 35.0% 48.5% 40.3% 60.1% 45.2% 30.3% Note: Excess returns are calculated as fund return in excess of the benchmark return. Benchmark used is the primary prospectus benchmark for each fund. Actively managed US mutual funds, excluding index funds. Fund returns exclude sales charges, but include management, administrative, and 12b-1 fees. Source: Morningstar, RBC Capital Markets We used Morningstar data to determine if actively managed funds add value. Our finding is that only in 2005 and 2009 did a majority of actively managed funds beat their benchmark over the past 10 years. This is not encouraging given that clients are paying fees for the professional management of funds. We think that the table above explains the increasing popularity of exchange-traded funds – why pay more, if you can’t beat the market? Exhibit 20: Passively Managed Funds have been Gaining Market Share 12% 13% 15% 15% 17% 18% 19% 21% 24% 24% 26% 27% 88% 87% 85% 85% 83% 82% 81% 79% 76% 76% 74% 73% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Passively Managed Actively Managed Note: Percent of net assets of equity open-end mutual funds and ETFs. Funds as categorized by Morningstar. Source: Morningstar, RBC Capital Markets This brings us back to the discussion of performance. Actively managed funds need to perform well to attract assets. The pressure to do so could likely increase as investors evaluate the cost of paying high active management fees versus the benefits of professional management. We believe Waddell & Reed needs to improve performance to grow assets. It is known for being an active manager and we think the new generation of investors could be even more demanding and financially savvy than the previous ones. Younger generations are expected to rely less on advisors, which should make the assets less “sticky” and could increase redemption rates if performance cannot justify the additional costs. Waddell & Reed Financial, Inc.July 24, 2012

- 16. 16 Significant Exposure to Equity Markets could Lead to Slow AUM Growth With over 80% of assets in equity funds, Waddell & Reed has a significant exposure to the equity market. Given the uncertainty about an economic recovery, we believe that Waddell & Reed would not reap the benefit of a market rally in the near term. While margins could expand at Waddell & Reed if equity markets rally, driving assets under management higher, we assign a low probability to this scenario. With uncertainty about Europe, a decelerating of growth in emerging markets, a lack of consumer confidence and the US recovery not gaining traction, being heavily exposed to equity markets could cause some headwinds. We would expect further redemptions in equities and inflows into fixed income funds, if conditions do not improve. RBC’s Chief Investment Strategist Myles Zyblock (RBC Dominion Securities Inc.) recommends that investors remain underweight equities. Dawn Desjardins, Assistant Chief Economist for Royal Bank of Canada, has said that world growth is expected to fall short of the long-term trend rate by about one-quarter of a percentage point in 2012. The near-term outlook for Europe remains grim. And while Greece seems to be willing to remain in the Eurozone, it is likely that austerity measures demanded by the troika could be watered down. There could be the risk of falling into a deeper recession again, unless the economy starts gaining steam in Europe. This would impact not only Europe, but the world economy. According to Tom Porcelli, RBC’s Chief US Economist, GDP growth in the US was driven by exports, which accounted for 45% of the GDP growth. The majority of US exports go into countries such as Brazil, Mexico and China. These countries, in turn, finance their acquisitions by borrowing from European banks. A tightening of lending standards could slow down growth globally. The consequence would be a deceleration in the rate of expansion in emerging market economies and potentially a decline in exports for the US. Another point of contagion is the exposure the US financial system has to Europe. According to the Bank of International Settlement (BIS), US banks held $656 billion of euro-area debt in the fourth quarter of 2011. The BIS is also worried that central bank money printing and support for the financial sector is reaching its limits. At the end of 2011, the world’s central bank balance sheets stood at $18 trillion, double the pre-crisis level and about 30% of global GDP. The BIS wrote in its annual report published in June 2012, that the persistence of loose monetary policy is largely the result of insufficient action by governments in addressing structural problems. According to the BIS, the positive effect and impact of central bank intervention is shrinking while the negative side effects of loose monetary policy are growing. Put differently, low interest rates and almost unconditional liquidity provided by central banks de-incentivize the private sector to de-lever and repair its balance sheet. We believe that investors should not own Waddell & Reed in hopes of a fast recovery in equity markets, as we don’t believe that structural deficiencies in the economy can be fixed quickly. While being levered to equity markets can be beneficial in a recovery, the opposite could also be true for a further deterioration in the economy. Sure, the company is a conundrum in that it defies some of our conventional beliefs. For instance, it has above industry average growth rates despite its below-peer performance in equities. The below chart demonstrates this. Waddell & Reed Financial, Inc.July 24, 2012

- 17. 17 Exhibit 21: Equity Funds’ Organic Growth – Waddell & Reed versus Industry (US-domiciled Funds) 1.7% 1.2% 0.6% (0.5%) (1.2%) (0.5%) 2.2% (0.1%) (1.6%)(1.5%) (2.0%) (1.5%) (1.0%) (0.5%) 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 1Q11 2Q11 3Q11 4Q11 1Q12 WDR Industry Source: Company reports, Morningstar, RBC Capital Markets Waddell & Reed was also able to achieve above industry-average organic growth rates in its fixed income funds in recent quarters, despite being known as an “equities shop” focused on active management. Exhibit 22: Fixed Income Funds’ Organic Growth – Waddell & Reed versus Industry (US-domiciled Funds) 3.0% 1.8% 2.2% 6.9% 9.0% 3.6% 1.0% 2.0% 0.0% 2.1% 3.9% 1.8% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E WDR Industry Source: Company reports, Morningstar, RBC Capital Markets Conventional wisdom would suggest that equity outflows should have been larger than for the industry based on weak fund performance over the past few years. This would be based on one-year and three-year measurement periods. Likewise, one could have expected that organic growth in its fixed income funds would have been low based on the fact that the company’s expertise is in actively managed equity funds. Waddell & Reed Financial, Inc.July 24, 2012

- 18. 18 However, Waddell & Reed seems to defy conventional wisdom in that it generates relatively strong flows despite weak equity fund performance and has strong flows into fixed income funds despite being known as a provider of equity funds. One explanation could be that the Waddell & Reed has a very loyal customer base and is less likely to suffer outflows to the same degree as its competitors. This is supported by management’s assertion that it has one of the best retention rates on assets sold through its captive sales force. We are impressed by this, as well. Nonetheless, despite all these desirable qualities, we are not certain how sustainable they are. Eventually, even the most loyal customers could reach the pain point and start withdrawing cash unless performance improves from here on. Until then, we would recommend investors remain on the sidelines. Waddell & Reed Financial, Inc.July 24, 2012

- 19. 19 Financial Analysis Recent Results Waddell & Reed had a strong March quarter, with earnings of $0.55 per share exceeding consensus estimates of $0.46. While the company’s heavy exposure to equities had been creating headwinds for some time, it seems to have reaped the benefits of its equity bias in the current quarter as assets under management grew 13% sequentially to $94 billion. Market performance was not the only factor leading to sequential growth of 5.4% in revenues. Waddell & Reed’s strategy to diversify sales and to offer new products seems to be paying off. The company generated 6.3% organic growth in AUM, reporting net flows of $1.3 billion in the quarter. In comparison, based on ICI data, organic growth for the industry was close to zero for the same time period. If one were to exclude money market funds, which had outflows of about $109 billion in the quarter, organic growth for the industry would have been still lower at 3.8%. Organic growth for the company in the March quarter was the lowest in recent history. However, we believe that the decision to diversify the product mix, reducing exposure to equities and moving into fixed income offerings should pay off. Net inflows of $1.5 billion into fixed income funds were the strongest additions into this asset class – ever. There were other encouraging signs in the quarter. While still in outflow mode, redemptions have been declining in the company’s flagship Ivy Asset Strategy fund. With a heavy equities exposure of 80%, this fund has been experiencing outflows for some time now. Having a large cap growth strategy, the fund has fallen out of favor with investors in the current market environment. However, should the move towards increasing risk exposure persist, we could see the funds flow number turning positive. This is important given the size of the fund, which represents about 28% of total assets under management as of the end of 2011. Nonetheless, equities as an asset class continued to suffer from outflows for a second consecutive quarter – albeit at a lower rate. The company reported redemptions of $156 million versus inflows of $1.6 billion a year earlier. The redemption rate continues to be above industry average for the Wholesale channel. In the current quarter, the company reported a redemptions rate of 30.7%, down from 35.7% in the previous quarter. As a comparison, average redemption rates in the Wholesale channel for the industry were 27.0% for 2011 and 26.3% in 2010. Waddell & Reed had 29.5% and 29.3% for the years ended December 31, 2011 and 2010, respectively. The current quarter’s redemption rate is still a concern despite the sequential decline in this ratio. Assets overall are less sticky compared to other distribution channels, especially the advisory channel, which had redemption rates of about 10% over the past few quarters. Thus, performance becomes an even more important part of the Waddell & Reed story as third-party distribution is by now the biggest contributor of organic growth. The most recent performance data show that while performance has been good over five years and has been improving more recently, the three-year performance has been subpar. This is true for equity assets as well as for fixed income assets. Waddell & Reed Financial, Inc.July 24, 2012

- 20. 20 Exhibit 23: Rating by Number of Funds as of 1Q12 Fund Rating By Rank 1 Year 3 Years 5 Years Lipper Equity Funds Top Quartile 24% 29% 52% Top Half 43% 39% 79% Fixed Income Funds Top Quartile 47% 19% 53% Top Half 58% 44% 73% All Funds Top Quartile 30% 26% 52% Top Half 47% 40% 78% Morningstar Equity Funds 4 & 5 Star 47% 12% 57% All Funds 4 & 5 Star 42% 9% 53% Source: Company reports; Lipper; Morningstar Looking at ratings weighted by assets leads to the same conclusion. The three-year performance could be an issue in the future as performance is rolled forward. Exhibit 24: Rating by Assets as of 1Q12 Fund Rating By Rank 1 Year 3 Years 5 Years Lipper Equity Funds Top Quartile 11% 18% 77% Top Half 67% 21% 88% Fixed Income Funds Top Quartile 62% 10% 62% Top Half 68% 46% 79% All Funds Top Quartile 21% 16% 74% Top Half 67% 26% 86% Morningstar Equity Funds 4 & 5 Star 29% 8% 72% All Funds 4 & 5 Star 31% 6% 70% Source: Company reports; Lipper; Morningstar While we are impressed with the flows in the current quarter, we are not convinced yet that fundamentals could improve. The reason for our scepticism is the trend in the one-year performance. We have created exhibits which show the volatility in the one-year performance from one quarter to the next. Our verdict: performance has been anything but steady. If fund performance does not improve, we believe the one-year performance could turn into a three-year performance and the three-year performance could blend with the five-year performance. This could lead to outflows in the future unless company-wide performance starts improving. Waddell & Reed Financial, Inc.July 24, 2012

- 21. 21 Exhibit 25: One-year Performance by Number of Funds (Equally Weighted) 1 Year Performance - Number of Funds 0% 10% 20% 30% 40% 50% 60% 70% 80% 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 Equity Funds - Lipper Top Quartile Equity Funds - Lipper Top Half Morningstar 4 & 5 Star Ratings Source: Company reports; Lipper; Morningstar Exhibit 26: One-year Performance Weighted by Assets 1 Year Performance - Weighted by Assets 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 Equity Funds - Lipper Top Quartile Equity Funds - Lipper Top Half Morningstar 4 & 5 Star Ratings Source: Company reports; Lipper; Morningstar It seems that Waddell & Reed’s funds were actually starting to perform well in late 2010 and early 2011, but the trend reversed as the year progressed. Specifically, we saw a decline in the Lipper rankings from the top quartile to the top half, which should make it more difficult for the company to differentiate itself from other fund providers. Performance was probably one of the reasons why another flagship Waddell & Reed fund, Global Natural Resources, was removed from a model portfolio, which resulted in outflows in the March quarter. This fund is the company’s second-largest fund, with over $4.4 billion in assets under management. The fund, which is subadvised by Mackenzie Financial, had a very difficult year in 2008, losing 61.4% due to its significant exposure to emerging markets. On a cumulative basis, the fund has been underperforming its category average by 12.6%, meaning that it has underperformed its investment peer group over the past three years. While outflows out of funds sub-advised by other managers is not as big an issue as outflows of funds managed directly by the company (as there should be some offset on the expense side to the lost revenue), we would still prefer inflows as the asset management business is a scale business. Good Bad Good Bad Waddell & Reed Financial, Inc.July 24, 2012

- 22. 22 We believe performance has to improve at Waddell & Reed to attract more assets. In the meantime, the company has new initiatives to increase organic growth. It is planning to deepen relationships with some of the largest distributors which, according to management, are in a nascent stage. It is developing two new products, the Ivy International Balanced Fund and the Ivy Global Income Allocation Fund, to gather assets. However, we believe that sales should follow performance and as such, asset growth could be somewhat slower than for its peers. Exhibit 27: Recent Net Flows have been Soft in Equities ($ in Billion) $1.56 $1.18 $0.46 ($0.16) $0.55 $0.53 $0.70 $1.32 $1.54 ($1.26) ($1.500) ($1.000) ($0.500) $0.000 $0.500 $1.000 $1.500 $2.000 1Q11 2Q11 3Q11 4Q11 1Q12 Equity Funds Fixed Income Funds Source: Company reports, RBC Capital Markets Financial Projections We expect Waddell & Reed to grow its total AUM at year-end from $83.2 billion in 2011 to $97.6 billion in 2012 and $109.6 billion in 2013, mainly driven by growth in the equity asset class. Exhibit 28: AUM Roll Forward Assets under management ($ in billion) 2009A 2010A 2011A 2012E 2013E Consolidated Total AuM Beginning assets $47.0 $69.8 $83.7 $83.2 $97.6 Sales (net of commissions) 19.7 21.7 23.8 25.6 29.1 Redemptions (10.9) (17.0) (19.5) (22.2) (24.0) Net sales $8.7 $4.7 $4.3 $3.3 $5.2 Net exchanges (0.0) 0.0 (0.0) (0.0) - Reinvested dividends & capital gains 0.6 0.7 0.7 0.2 - Market action 13.5 8.5 (5.5) 10.9 6.8 Ending assets $69.8 $83.7 $83.2 $97.6 $109.6 - - - - - Net flows $9.3 $5.4 $5.0 $3.5 $5.2 Source: RBC Capital Markets Estimate We expect equity funds AUM to increase from $67.6 billion in 2011 to $78.2 billion in 2012 and $88.0 billion in 2013. Our projections incorporate net flows of $273 million in 2012 and $3.3 billion in 2013. The increase in flows in 2013 is a result of a shift in customer demand towards equity funds. Waddell & Reed Financial, Inc.July 24, 2012

- 23. 23 We expect client interest in the fixed income asset class to continue, with fixed income funds’ AUM increasing from $14.0 billion in 2011 to $18.1 billion in 2012 and $20.3 billion in 2013. We are projecting net flows of $3.3 billion in 2012 and $2.0 billion in 2013. Our expectation is that investors could move from fixed income funds to equity funds in 2013, resulting in lower net additions than in 2012. Given our expectations for increasing AUM in the next few years, we are forecasting net revenues to increase, going from $929.5 million in 2011 to $1.0 billion in 2012 and $1.1 billion in 2013, mainly due to increasing investment management fees revenues. However, we believe net operating margins could decline from the 31.4% seen in 2011 to 29.8% in 2012 and expand to 31.2% in 2013, as equity funds are projected to receive inflows. We expect Waddell & Reed to generate $298.1 million in operating income in 2012 and $344.0 million in 2013, compared to operating income of $292.0 million in 2011. Our diluted EPS estimates for 2012 and 2013 are $2.24 per share and $2.59 per share, respectively. This compares to diluted EPS of $2.05 in 2011. Waddell & Reed Financial, Inc.July 24, 2012

- 24. 24 Valuation Each of the three exhibits below show how Waddell & Reed has traded: On an absolute P/E basis, on a basis of Waddell & Reed’s P/E relative to that of the S&P 500, and on a basis which looks at Waddell & Reed’s P/E relative to that of a broad valuation index we’ve constructed for asset managers in general. On an absolute P/E basis, Waddell & Reed’s shares have traded at a discount to historical levels over the past five and a half years. Exhibit 29: WDR’s Forward Looking P/E Multiples 0x 5x 10x 15x 20x 25x 30x Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Source: Bloomberg; RBC Capital Markets On a relative basis, Waddell & Reed has been trading at a premium to the S&P 500. However, the shares have recently started to trade in line with the S&P Exhibit 30: WDR’s Forward Looking P/E Relative to S&P 500 Index 0.4x 0.6x 0.8x 1.0x 1.2x 1.4x 1.6x 1.8x Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Source: Bloomberg; RBC Capital Markets Waddell & Reed has been trading at a discount to peers on average over the past five and half years. Waddell & Reed Financial, Inc.July 24, 2012

- 25. 25 Exhibit 31: WDR’s Forward Looking P/E Relative to RBC Asset Managers Index 0.3x 0.4x 0.5x 0.6x 0.7x 0.8x 0.9x 1.0x 1.1x 1.2x 1.3x Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Note: RBC Asset Managers Index includes BLK, EV, IVZ, LM, TROW, WDR, BEN, JNS, AB, ART, AMG, CNS, CLMS, GBL, PZN Source: Bloomberg; RBC Capital Markets The asset managers are currently trading at 12.3x calendar year 2013 estimated earnings. Over the past 10 years Waddell & Reed has been trading at a 7% discount to peers. We believe that the discount is still justified given the company’s significant exposure to equity funds and the weak performance of its two largest funds. We arrive at our price target using a price-to-earnings multiple of 11.4x, which represents a 7% discount to the company’s peers, and our 2013 calendar year earnings estimate of $2.59 per share. Our price target is $30. Market Sensitivity Analysis Our EPS sensitivity analysis to equity market movements starts with our published estimates as the base case. Our base case assumes uniform market appreciation, with equity markets appreciating 2% sequentially and fixed income markets appreciating 1% sequentially, starting in calendar fourth quarter of 2012. For simplification, we assume the alternative asset classes appreciate at the same rate as the equity markets and thus assign an appreciation rate of 2% sequentially. We believe these assumptions are in line with long-term historical average returns. For the bull case scenario, we assume equity markets and alternative asset classes appreciate 4% sequentially, with fixed income appreciation unchanged from the base case scenario. For the bear case, we assume zero appreciation within the equity markets and alternative asset classes. We apply these assumed appreciation rates uniformly starting in the calendar December quarter (4Q12) and throughout calendar 2013. Exhibit 32: EPS Sensitivity to Equity Market Movements Scenario 2013 P/E 2013 Peer P/E (Discount)/ Premium 2013 EPS PT Base Case 11.4x 12.3x -7% $2.59 $30 Bear Case 11.4x 12.3x -7% $2.36 $27 Bull Case 11.4x 12.3x -7% $2.83 $32 Source: RBC Capital Markets estimate Waddell & Reed Financial, Inc.July 24, 2012

- 26. 26 Exhibit 33: Valuation Matrix Market Current 52-week Div. Enterprise YTD YTD Company Ticker Cap ($m) Price High Low Yield Value ($m) 2012E 2013E 2012E 2013E 2011A 2012E 2013E EV/AuM P/AuM Price Perf. Total Return Traditional Asset Managers BlackRock BLK $24,213 $173.31 $209.37 $137.00 3.46% $33,397.86 $13.08 $14.59 13.2x 11.9x 9.2x 9.1x 8.2x 0.009x 0.007x (2.8%) (1.1%) T.Rowe Price TROW 15,681 61.47 $66.00 $44.68 2.21% $15,111.57 3.27 3.76 18.8x 16.3x 11.6x 10.4x 9.2x 0.027x 0.028x 7.9% 9.1% INVESCO IVZ 9,655 21.54 $26.94 $14.52 3.20% $10,680.89 1.82 2.10 11.9x 10.2x 9.2x 9.0x 8.0x 0.016x 0.014x 7.2% 8.6% Legg Mason LM 3,616 25.61 $32.58 $22.36 1.72% $3,499.53 1.67 2.27 15.4x 11.3x 7.3x 6.7x 6.1x 0.005x 0.006x 6.5% 7.2% Franklin Resources BEN 23,746 110.35 $135.21 $87.71 0.98% $19,075.69 8.92 9.74 12.4x 11.3x 6.7x 6.7x 6.2x 0.026x 0.033x 14.9% 15.4% Waddell & Reed WDR 2,457 28.46 $38.73 $22.85 3.51% $2,023.61 2.21 2.44 12.9x 11.6x 6.5x 6.2x 5.6x 0.022x 0.026x 14.9% 16.8% Janus Capital Group Inc. JNS 1,361 7.22 $9.70 $5.36 3.32% $1,401.99 0.57 0.68 12.7x 10.6x 4.0x 5.0x 4.6x 0.009x 0.008x 14.4% 16.1% Eaton Vance Corp. EV 3,054 26.43 $29.64 $20.07 2.88% $3,642.09 1.83 2.04 14.4x 13.0x 8.0x 8.7x 8.3x 0.018x 0.015x 11.8% 13.4% Federated Investors, Inc. FII 2,158 20.71 $23.89 $14.36 4.64% $2,115.35 1.64 1.76 12.6x 11.8x 7.7x 7.1x 6.7x 0.006x 0.006x 36.7% 40.0% AllianceBernstein AB 1,260 11.98 $18.76 $11.55 8.68% $1,220.60 1.04 1.17 11.5x 10.3x 2.5x 2.6x 2.5x 0.003x 0.003x (8.4%) (5.9%) Artio Global Investors ART 187 3.14 $11.22 $2.83 2.55% $164.13 0.16 0.04 19.8x n/m 1.2x 10.0x n/m 0.006x 0.007x (35.7%) (34.4%) Affiliated Manager Group AMG 5,528 107.63 $115.66 $70.27 0.00% $7,276.03 7.28 8.58 14.8x 12.5x 14.9x 13.3x 11.3x 0.020x 0.015x 12.2% 12.2% Cohen & Steers CNS 1,377 31.91 $40.93 $23.79 2.26% $1,242.58 1.63 1.93 19.5x 16.5x 15.3x 10.9x 9.5x 0.028x 0.031x 10.4% 11.7% Calamos CLMS 221 10.85 $14.66 $9.40 3.50% $113.22 0.92 0.89 11.9x 12.3x 0.7x 0.9x 0.8x 0.003x 0.006x (13.3%) (11.9%) GAMCO GBL 1,214 45.57 $52.98 $35.81 0.35% $1,169.06 3.13 3.30 14.6x 13.8x 9.2x 8.4x 7.8x 0.032x 0.033x 4.8% 5.6% Pzena Investment Mgmt PZN 266 4.11 $7.39 $3.18 2.92% $268.93 0.33 0.39 12.3x 10.5x 6.2x 6.8x 6.5x 0.018x 0.018x (5.1%) (1.3%) Mean 2.89% 14.3x 12.3x 7.5x 7.6x 6.7x 0.016x 0.016x 4.8% 6.3% Median 2.90% 13.1x 11.8x 7.5x 7.8x 6.7x 0.017x 0.015x 7.6% 8.9% Min 0.00% 11.5x 10.2x 0.7x 0.9x 0.8x 0.003x 0.003x (35.7%) (34.4%) Max 8.68% 19.8x 16.5x 15.3x 13.3x 11.3x 0.032x 0.033x 36.7% 40.0% Alternative Asset Managers Och-Ziff OZM $2,920 $7.05 $13.23 $6.56 5.67% $2,493.47 $0.48 $1.15 6.2x 5.4x 8.9x 3.6x 3.3x 0.083x 0.097x (16.2%) (14.8%) Apollo Global Manager APO 1,696 13.41 $17.94 $8.85 7.46% $7,415.10 (0.86) 2.22 6.0x 4.6x -24.3x 7.8x 6.1x 0.086x 0.020x 8.1% 14.9% Blackstone BX 6,727 13.15 $17.78 $10.51 3.04% $23,469.76 (0.57) 1.47 9.0x 6.4x 46.7x 38.3x 28.3x 0.123x 0.035x (6.1%) (4.0%) KKR KKR 3,253 14.00 $16.10 $8.95 4.29% $43,312.58 0.73 2.06 6.8x 6.4x 73.7x 156.8x 102.3x 0.695x 0.052x 9.1% 12.7% Fortress Investment Group FIG 1,950 3.79 $4.79 $2.67 5.28% $2,518.22 0.46 0.41 9.2x 6.9x 11.0x 10.4x 7.6x 0.054x 0.042x 12.1% 15.3% Mean 5.15% 7.4x 5.9x 23.2x 43.4x 29.5x 0.208x 0.049x 1.4% 4.8% Median 5.28% 6.8x 6.4x 11.0x 10.4x 7.6x 0.086x 0.042x 8.1% 12.7% Min 3.04% 6.0x 4.6x -24.3x 3.6x 3.3x 0.054x 0.020x (16.2%) (14.8%) Max 7.46% 9.2x 6.9x 73.7x 156.8x 102.3x 0.695x 0.097x 12.1% 15.3% S&P 500 SP50 $12,316,922 $1,362.66 $1,422.38 $1,074.77 2.21% $96.42 $104.26 14.1x 13.1x 8.4% 8.4% S&P 500 / Asset Mgmt & Custody Banks SPT30 134,632 120 138.27 94.63 2.53% 9.84 10.32 12.7x 12.1x 5.3% 5.3% S&P Comp. 1500 / Asset Mgmt & Custody Banks SPT29 154,759 131 149.00 102.23 2.59% 10.56 11.04 12.8x 12.3x 6.3% 6.3% S&P Mid Cap 400 / Asset Mgmt & Custody Banks SPT31 16,977 225 245.14 168.41 2.50% 16.40 16.85 14.0x 13.6x 14.7% 14.7% S&P 500 / Financials SP621 1,737,330 $193.42 215.37 151.85 2.07% 14.57 17.63 13.5x 11.2x 10.4% 10.4% CurrentP/EConsensus CY EPS EV/EBITDA Consensus Asset Management Research Source: FactSet (Priced as of market close July 20, 2012 ET); RBC Capital Markets Waddell & Reed Financial, Inc.July 24, 2012

- 27. 27 Company Description Founded in 1937, Waddell & Reed, Inc. (NYSE:WDR) is one of the oldest mutual fund companies in the United States. The company provides investment management, investment product underwriting and distribution, and shareholder services administration to mutual funds and institutional and separately managed accounts. It offers four different fund families – Waddell & Reed Advisory Funds (mutual funds), Ivy Funds (mutual funds), Ivy Funds Variable Insurance Portfolios (variable annuities) and InvestEd Portfolios (529 college savings plans). The company operates through three distinct distribution channels: Through the Advisory channel, Waddell & Reed serves primarily the middle class, the mass affluent market, families and businesses. It uses its own network of financial advisors to provide personal financial planning services in the United States. The advisors provide personal financial plans and investment strategies for retirement, education, insurance and estate planning needs. The Waddell & Reed Advisors funds are offered through Waddell & Reed advisors, the company’s network of personal financial planners. Through the Wholesale channel, the company distributes its retail funds (the Ivy Funds, Ivy Fund Variable Insurance Portfolios and InvestEd Portfolios) through broker/dealers, independent registered investment advisors, and retirement and insurance platforms. Ivy Funds are offered through the company’s Wholesale channel. Through the Institutional channel, the company manages assets for institutional clients. Waddell & Reed’s largest client base is funds which utilize it as sub-advisors. These clients either lack the scale and/or track record to manage funds internally or choose to market multi-manager styles. It offers its investment strategies to defined benefit plans, pension plans (defined benefit and defined contribution) and endowments. As of December 2011, the company had $83.2 billion in assets under management. While it offers a broad range of products, it is still focused mostly on domestic equities. The majority of its assets, more than 80%, are invested in equities, of which 73% were domestic and 27% were international equities. Waddell & Reed employed a total of 1,616 individuals full-time at the end of 2011, of which 1,235 were home office and Legend employees, and the remaining 381 employees were in charge of administration and field supervision. Legend is Waddell & Reed’s mutual fund distribution and retirement planning subsidiary which serves employees of school districts and other not-for-profit organizations. The company’s sales force, totaling 1,816 financial advisors, operated out of 163 offices across the United States, and 256 individual advisor offices. The company claims to have one of the largest sales forces in the United States selling primarily mutual funds, serving more than 502,000 mutual fund customers in the advisors channel. Waddell & Reed Financial, Inc.July 24, 2012

- 28. 28 Milestones: 1937 Waddell & Reed was founded by Chauncey Waddell and Cameron Reed, two World War I pilots 1940 Waddell & Reed introduced one of the first mutual funds in the United States to be registered under the Investment Company Act of 1940 1950 Waddell & Reed became a top five mutual fund sales organization in the United States 1958 Waddell & Reed became the first company to open a mutual fund sales outlet in a department store – in Buffalo, New York. The company was also the first one to hire part- time agents 1963 Dudley F. Cates resigned as president and was succeeded by Cameron Reed, the founder and former president. 1965 Cameron Reed resigned and sold his stockholdings to the du Pont group, giving it 24% of the voting stock 1969 Continental Investment Corporation of Boston bought Waddell & Reed after the company’s performance in its funds deteriorated around the bear market in 1966 1981 Liberty National Insurance Holding Company, the predecessor of Torchmark Corporation, acquired Waddell & Reed 1998 Torchmark Corporation spun off Waddell & Reed in an initial public offering and distributed WDR common shares to Torchmark shareholders 2000 The United Group of Mutual Funds was renamed Waddell & Reed Advisors Funds, Inc. 2003 Waddell & Reed launched the new Ivy Funds and officially entered wholesale distribution 2007 Waddell & Reed reached $50 billion in assets under management on its 70th anniversary Source: Company Web site; RBC Capital Markets Waddell & Reed Financial, Inc.July 24, 2012

- 29. 29 Organizational Structure Waddell & Reed operates through its various subsidiary companies: Its investment advisory business operates primarily through Waddell & Reed Investment Management Company (WRIMCO), a registered investment advisor; Ivy Investment Management Company (IICO), the registered investment advisor for Ivy Funds; and Legend Advisory Corporation, the registered investment advisor to Legend. The investment advisory business generated about 44% of total revenues in 2011. The underwriting and distribution business operates through three broker/dealers: Waddell & Reed, Inc. (W&R), national distributor and underwriter of shares of the Advisors Funds, other mutual funds and of insurance products; Ivy Funds Distributor, Inc. (IFDI), distributor and underwriter for the Ivy Funds); and Legend Equities Corporation (LEC), a mutual fund distributor and retirement planning subsidiary serving not-for profit organizations. The underwriting and distribution business generated about 45% of total revenues in 2011. Waddell & Reed Services Company (WRSCO) provides accounting and transfer-agency services to the Advisory Funds, Ivy Funds, Ivy Funds VIP and InvestEd. Shareholder services generated about 11% of total revenues in 2011. Exhibit 34: Organization Structure Source: Company reports Products & Services Investment management products The company offers mutual fund products in various investment styles and options. As of December 31, 2011, WDR offered 80 registered open-ended mutual fund options. The main funds offered by the company are: Advisor Funds: Variable products (variable annuity funds) offered through multiple channels. Ivy Funds: Offered through both the Advisors channel and Wholesale channel. These mutual funds offer exposure to a range of asset classes, investment styles and sectors. Ivy Funds VIP (Variable Insurance Portfolios): Offered through the company’s financial advisors and Legend advisors and occasionally through the Wholesale channel. Ivy Funds VIP serves as the underlying investment for a number of insurance products, including variable annuities and variable life insurance policies. Waddell & Reed Financial, Inc.July 24, 2012

- 30. 30 InvestEd: Similar to Ivy Funds VIP, the product is offered through Waddell & Reed’s financial advisors and Legend advisors and sometimes through the Wholesale channel. The Ivy Fund InvestEd 529 plan offers various options to save for college. Other Products Waddell & Reed offers other products in addition to the mutual fund products mentioned above. Annuity: The company distributes its business partners’ annuity products through its Advisor channel. The annuity products offer Ivy Funds VIP as the investment vehicle. Retirement and Life Insurance: Waddell & Reed offers retirement and life insurance products to its customers through the Advisor channel. The products are underwritten by the company’s business partners. The company also offers life insurance and disability products underwritten by multiple carriers through its insurance agency subsidiary, Waddell & Reed financial advisors. Asset allocation and investment advisory: Waddell & Reed offers fee-based asset allocation and investment advisory products to its Advisor channel’s customers under the following brand names: Managed Allocation Portfolio (MAP) MaPPlus Strategic Portfolio Allocation (SPA) Together, MAP, MaPPlus and SPA products had US$6.0 billion in assets under management as of December 31, 2011. Distribution Channels The company operates its business through three different distribution channels: Exhibit 35: AUM by Channel (December 31, 2011) Advisors channel 38% Wholesale channel 49% Institutional channel 13% Source: Company reports Waddell & Reed Financial, Inc.July 24, 2012

- 31. 31 Exhibit 36: AUM Breakdown by Investor Type (December 31, 2011) Institutional 12% Retail / HNW 88% Source: Company reports Advisor Channel This channel comprises independent financial advisors responsible for the sale of the company’s retail products. The advisors’ target groups are middle class and mass affluent clients, and businesses. The typical financial planning products sold in this channel are retirement planning, estate planning, education funding, and other products designed to address various financial needs of clients. As of December 31, 2011, the total assets under management in this channel were $31.7 billion. The company prides itself on having one of the lowest redemption rates in the industry for this channel. The number of financial advisors associated with the company has been declining over the years due to the company’s push to improve productivity. Gross revenue per advisor was $156,000 for FY2011 compared to $119,000 for the year ended December 31, 2010. The company is trying to recruit experienced advisors to further improve productivity. As of year-end 2011, the sales force headcount stood at 1,816 financial advisors serving 502,000 mutual fund customers. Wholesale Channel Retail mutual funds are distributed through broker/dealers, registered investment advisors, including Legend Group of subsidiaries (Legend), and many retirement platforms utilizing a team of internal/external and hybrid wholesalers. Hybrid wholesaling is a new approach to selling that relies on technology (electronic marketing and communication via email / telephone) and face-to-face meetings in order to cover large territories. The primary focus is to distribute Ivy Funds through the Wholesale channel. The company restructured its wholesaler territories in 2010 into smaller territories to build relationships with additional distribution partners in these territories. As such, Waddell & Reed has been building its wholesaler force which stood at 51 wholesalers at year-end 2011. As of December 31, 2011, this channel had total AUM of $41.0 billion, and it is also the company’s fastest growing channel, with annual sales growth rate of 36% since 2007. The channel growth has been fuelled by good performance of the Ivy Funds family. The Ivy Asset Strategy fund is the best-selling fund and comprised 47% of total sales through this channel. Based on management, the company is encouraging wholesalers to sell other WDR funds in order to reduce concentration risk as the Asset Ivy Strategy fund comprises over 30% of total assets under management companywide. Institutional Channel The company manages various investment styles for institutional clients. The largest client type served through this channel is funds which hire Waddell & Reed to act as a sub-advisor for their branded funds. The funds either lack the scale or track record to compete or use Waddell & Reed as part of their multi- manager strategy. Other clients include corporations, foundations, endowments, Taft-Hartley plans and public plans such as defined benefit and defined contribution plans. At the end of FY2011, the total AUM for this channel was $10.5 billion, of which 60% was attributable to sub-advisory relationships. Waddell & Reed Financial, Inc.July 24, 2012

- 32. 32 AUM by Client and Asset Class WDR had AUM of US$83.2 billion at the end of 2011. The company’s assets under management are invested in equity, fixed income and money market instruments, with the majority of these assets being allocated to equities. Exhibit 37: AUM by Asset Class (December 31, 2011) Cash 2% Equities 84% Fixed Income 14% Note: Cash includes money market funds. Source: Company reports, RBC Capital Markets The Ivy Asset Strategy fund and Ivy Global Natural Resources fund comprised a third of total assets under management as of December 31, 2011. The company is trying to address this concentration risk by changing its compensation structure to entice wholesalers to sell more of its other products. Waddell & Reed’s top five mutual funds make up about 43% of total assets under management. Exhibit 38: Five Largest Mutual Funds by AUM (December 31, 2011) Ivy High Income 4% Ivy Global Natural Resources 5% Advisors Asset Strategy 3% Advisors Core Investment 3% Ivy Asset Strategy 28% Other 57% Source: Company reports Waddell & Reed Financial, Inc.July 24, 2012

- 33. 33 Management Team The table below summarizes the management team’s experience. Name Title Background Henry John Herrmann Chairman & Chief Executive Officer Mr. Herrmann has served as chairman of the board since January 2010. He was named chief executive officer in 2005, and named president in 1998 prior to Waddell & Reed's initial public offering. Mr. Herrmann managed the Waddell & Reed Advisors New Concepts Fund from its inception in June 1983 to February 1989. From 1976 to 1987, he was portfolio manager of the Waddell & Reed Advisors Vanguard Fund. Mr. Herrmann began his career with Waddell & Reed in 1971. Prior to joining Waddell & Reed, he was an investment analyst specializing in high technology stocks for a major New York City bank and two Wall Street brokerage firms. Michael L. Avery President Mr. Avery has been president of the company since January 2010. Prior to that, he served as chief investment officer from June 2005 to February 2011 and as senior vice president from June 2005 until January 2010. He has had various leadership roles at Waddell & Reed’s subsidiary companies. Mr. Avery joined the company in June 1981 and has served as a mutual fund portfolio manager since 1994. Daniel Paul Connealy Senior VP & Chief Financial Officer Mr. Connealy has been senior vice president and CFO since joining the company in June 2004. Prior to joining WDR, Mr. Connealy served as a director of Gold Banc Corporation, Inc., a director of the Russell Investment Company mutual funds, CFO of Stilwell Financial, Inc., and as a partner at PricewaterhouseCoopers LLP. Philip Sanders Senior VP & Chief Investment Officer Mr. Sanders serves as the CIO of Waddell & Reed Investment Management Company and Ivy Investment Management Company. He has 22 years of industry experience and has been with Waddell & Reed for 12 years. Previous experience includes: portfolio manager of several Waddell & Reed Advisors Funds and Ivy Funds and Portfolio Manager for Banc of America Capital Management, the investment management division of Bank of America. Michael D. Strohm Senior VP & Chief Operating Officer Mr. Strohm has been senior vice president of the company since January 1999 and chief operations officer since March 2001. In addition, he has served as president of Waddell & Reed Services Company, a transfer agent subsidiary of the company, since June 1999, as chief executive officer of WRI since December 2001 and as chief operating officer since March 2005. Mr. Strohm joined the company in June 1972. John E. Sundeen Senior VP & Chief Administrative Officer Mr. Sundeen has been senior vice president since July 1999 and chief administrative officer – Investments since January 2006. Previously, he served as chief financial officer from July 1999 to June 2004 and as treasurer from July 1999 to January 2006. Mr. Sundeen joined the company in June 1983. Source: SNL Financial; Morningstar Waddell & Reed Financial, Inc.July 24, 2012

- 34. 34 Investment Risks and Price Target Impediments Decline in security markets could impact Waddell & Reed’s earnings. Growth of assets under management is driven by inflows and market performance. A decline in security markets would result in lower assets under management, potentially offsetting any new money into the various funds. The value of investments can be driven by macro economic events over which the company has no control. A reduction in asset levels could lead to lower earnings as management fees would be applied to lower assets under management. Our price target would likely have to be revised downward if AUM were to decrease A reduction in risk appetite could lead to lower earnings A potential adverse effect of a decline in financial markets or further deterioration of the economy could be an increase in risk aversion. A political, economic or business crisis could lead to an increase in redemptions and lower assets under management as investors would convert their assets into cash. We do not model out a scenario like this as it is difficult to determine extreme events. As such, we would have to revise our earnings forecast and reduce our price target if such an event were to occur. Weak fund performance could lead to outflows and lower earnings Waddell & Reed’s ability to attract assets and grow earnings is dependent on the performance it generates. Weak performance, especially in its equity fund offerings could increase redemptions and lower inflows of new money. This could negatively impact our revenue and earnings forecast as higher investment advisory fees are earned with equity products. Our price target would have to be revised downward if performance deteriorated further. Regulatory changes could adversely impact Waddell & Reed’s business. Changes in regulations (legal, regulatory, accounting, tax, compliance) can negatively impact operations, revenues and earnings by increasing expenses and/or reducing investor interest in investment products. We would have to revise our forecasts based on the regulatory changes, which could negatively impact our price target. Impairment of intangibles could lead to lower earnings. Waddell & Reed has substantial intangibles. About 20% of total assets, or over $220 million consist of goodwill and identifiable intangibles assets. Any material deviation from key assumptions about the business and its prospect due to changes in market conditions or other external factors could lead to impairment charges. We would likely have to lower our earnings estimate in the quarter the charges occur. This could have a negative impact on the price target. Competition could pressure margins The asset management business is very competitive. There is a trend toward lower fees in some segments of the investment management business. New rules adopted by the SEC to improve mutual fund corporate governance could put further downward pressure on fees. Margins could decline as a result. This could negatively impact our price target. Likewise, Waddell & Reed competes with stock brokers, mutual funds, investment banking firms, insurance companies, banks and other financial institutions. These competitors could have larger resources than Waddell & Reed, broader product offering or provide services at lower rates. Consequently, the company could lose clients to competitors. If asset under management should decline, we would have to revise our earnings estimate and our price target. Waddell & Reed Financial, Inc.July 24, 2012