Institutions in housing market and housing finance in india

•Transferir como PPTX, PDF•

8 gostaram•2,477 visualizações

there are many policies , organisations and institutions in india which are guarding housing market . check out the details about it.

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Institutions in housing market and housing finance in india

Semelhante a Institutions in housing market and housing finance in india (20)

Mais de padamatikona swapnika

Mais de padamatikona swapnika (20)

Último

Último (20)

Institutions in housing market and housing finance in india

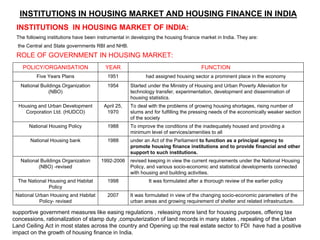

- 1. POLICY/ORGANISATION YEAR FUNCTION Five Years Plans 1951 had assigned housing sector a prominent place in the economy National Buildings Organization (NBO) 1954 Started under the Ministry of Housing and Urban Poverty Alleviation for technology transfer, experimentation, development and dissemination of housing statistics. Housing and Urban Development Corporation Ltd. (HUDCO) April 25, 1970 To deal with the problems of growing housing shortages, rising number of slums and for fulfilling the pressing needs of the economically weaker section of the society National Housing Policy 1988 To improve the conditions of the inadequately housed and providing a minimum level of services/amenities to all National Housing bank 1988 under an Act of the Parliament to function as a principal agency to promote housing finance institutions and to provide financial and other support to such institutions. National Buildings Organization (NBO) -revised 1992-2006 revised keeping in view the current requirements under the National Housing Policy, and various socio-economic and statistical developments connected with housing and building activities. The National Housing and Habitat Policy 1998 It was formulated after a thorough review of the earlier policy National Urban Housing and Habitat Policy- revised 2007 It was formulated in view of the changing socio-economic parameters of the urban areas and growing requirement of shelter and related infrastructure. supportive government measures like easing regulations , releasing more land for housing purposes, offering tax concessions, rationalization of stamp duty ,computerization of land records in many states , repealing of the Urban Land Ceiling Act in most states across the country and Opening up the real estate sector to FDI have had a positive impact on the growth of housing finance in India. INSTITUTIONS IN HOUSING MARKET OF INDIA: The following institutions have been instrumental in developing the housing finance market in India. They are: the Central and State governments RBI and NHB. ROLE OF GOVERNMENT IN HOUSING MARKET: INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA

- 2. INSTITUTIONS IN HOUSING MARKET OF INDIA: The following institutions have been instrumental in developing the housing finance market in India. They are: the Central and State governments RBI and NHB. RESERVE BANK OF INDIA : INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA BUSINESS STANDARD NEWSPAPER’S ARTICLE ABOUT RBI ROLE IN HOUSING SECTOR This will be a boost for the low-ticket housing segment (up to Rs 30 lakh) … increasing the loan-to-value will encourage builders to focus on this segment. With the interest rates coming down, they expect more sanctions and disbursement for banks NATIONAL HOUSING BANK: National housing bank helps to regulate and supervise the housing finance companies. a number of new players have entered the housing finance market with competitive offerings which have helped increase the demand for housing loans. INDIA MORTGAGE GUARANTEE CORPORATION India Mortgage Guarantee Corporation (IMGC) was founded in June 2012 with a vision to make early home ownership a real possibility through the provision of mortgage guarantees. SOURCE: NHB

- 3. LAND ADMINISTRATION INSTITUTIONS: THE BASIC STRUCTURE OF LAND ADMINISTRATION INVOLVES FOUR MAIN INSTITUTIONS. THEY ARE: 1. The Land Revenue Department maintains the database for land records 2. Department of Survey and Land Records is responsible for maintaining spatial data, mapping and demarcating boundaries. 3. The Office of Stamp and Registration is responsible for collecting stamp duties on these transactions. 4. Local bodies maintain property tax registers. INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA INSTITUTIONAL SCHEMES: • The Rural Housing Fund (RHF) was set up in 2008, to enable primary lending institutions to access funds for extending housing finance to targeted groups in rural areas at competitive rates. Disbursements under the Rural Housing Fund have helped in creation of dwelling units for women, marginal farmers, small artisans, members of scheduled castes and scheduled tribes and minority communities. • In May 2007, NHB conceptualized the Reverse Mortgage Loan (RML) and formulated the Operational Guidelines for RMLs • The Central Registry of Securitization Asset Reconstruction and Security Interest of India (CERSAI), a Government Company licensed under Section 25 of the Companies Act, 1956 has been incorporated for the purpose of operating and maintaining the Central Registry under the provisions of the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act). The objective of setting up the Central Registry is to prevent frauds in loan cases involving multiple lending from different banks on the same immovable property. • Indira Awaas Yojana (IAY) aims at providing dwelling units to houseless below poverty line (BPL) households identified by the gram sabhas and those living in dilapidated and kutcha houses, with a component for providing house sites to the landless poor as well. • Along with developing housing sector, welfare of construction workers also needs to be seen. As a part of Deen Dayal Upadhyaya Shramev Jayne Karyakaram, the Government has launched Portability through Universal Account Number of Employees Provident Fund benefitting around 10 lakhs construction workers and contract labourers.

- 4. INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA INSTITUTIONAL SCHEMES: the Government of India has launched few more following schemes to alleviate the shortage of affordable housing: i) Rajiv Awas Yojana (RAY): Government of India launched RAY in June 2011 .The Central support under the scheme is admissible to States/UTs and Central Government Agencies for providing housing including new houses, incremental houses, rental houses, transit housing and development/improvement of basic civic & social infrastructure under the scheme. 212 projects in 22 states approved with 1,53,326 houses at project cost of ` 8,139.78 crore with central share of Rs 4,470.41 crore. `1632.27 crore has been released so far. Construction of 1406 houses has been completed till date. • (ii) Jawaharlal Nehru National Urban Renewal Mission (JNNURM): For rehabilitation of slum dwellers Government launched the JNNURM on 3rd December, 2005 for assisting State Governments in providing housing and basic civic services like water, sanitation etc to urban poor/ slum dwellers in 65 select cities under the Sub Mission Basic Services to the Urban Poor (BSUP) and in other cities and towns, under the Integrated Housing and Slum Development Programme (IHSDP). One of the 3 pro-poor reforms under JNNURM is provision of basic services to urban poor including security of tenure improved housing, water supply, sanitation education health and social security. As on 16th Oct 2014, 1517 projects have been approved for construction of 14,38,275 houses at cost of ` 20,140.97 crore. Construction of 1406 houses has been completed till date. • (iii) Affordable Housing in Partnership (AHP): As an integral part of RAY, the competent authority has also approved continuation of implementation of Affordable Housing in Partnership (AHP) Scheme. The scheme has been amended to provide Rs 75,000 per EWS/LIG dwelling unit of 40 sqm size for housing and internal development components with an objective to encourage private sector participation in affordable housing. 18 projects are approved at project cost of ` 1192.25 crore with central share of ` 112.53 crore for construction of 20,472 houses. Construction of 4728 houses has been completed (iv) Rajiv Rinn Yojana (RRY): Government of India has implemented RRY with effect from 1st October 2013. Under this Scheme, an interest subsidy of 5% p.a for loans upto Rs 5.00 lakhs and for tenure of 15-20 years, will be provided to EWS/LIG housing loan borrowers in Urban Areas availing loans from Financial Institutions i.e Scheduled Commercial Banks & HFCs etc

- 5. INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA HOUSING FINANCE COMPANIES : Housing Finance Companies (HFCs) registered with NHB are the second largest players in the housing market. The outstanding amount of housing loans by 56 HFCs with 2,065 branches spread across the country increased from Rs. 33,250 crore as at end- March 2001 to Rs, 86,155 crore as at end-March 2006 to Rs. 2,90,427 crore as at end-March 2013. In 2012-2013, maximum loans by HFCs were distributed in Maharashtra and Tamil Nadu followed by UP and Karnataka. In the case of HFCs loans to Individuals, 72 per cent of housing loans were disbursed for the purpose of constructing or acquiring a new house while 25 percent was disbursed for purchase of an old or an existing house. Top housing finance companies in india (source: CNBC) OTHER HOUSING FINANCE COMPANIES: 1. Hometrust Ltd., a company by Gujarat Ambuja Group, 2. Global Housing finance Ltd., a syndicate of reputed builders, 3. Weizmann Homes Ltd., a company from Weizmann Finance Ltd., 4. Maharishi Housing Finance Corporation Ltd., a company from Maharishi Group, are also catering to housing finance sector. 5. SBI Home finance Ltd., a subsidiary of SBI, 6. PNB Housing Finance Ltd., a subsidiary of PNB is also doing very good business. SBI Home Finance Ltd. is doing little bit slow for the time being but PNB Housing Finance Ltd. has recently opened its new branch near Shoppers Stop, Andheri. 7. BOB Housing Finance Ltd., a subsidiary of Bank of Baroda also having very attractive housing finance schemes. 8. Can Fin Homes, very aggressive subsidiary of Canara Bank in Southern India , is also doing very good job in Western parts of the country.

- 6. INSTITUTIONS IN HOUSING MARKET AND HOUSING FINANCE IN INDIA HOUSING FINANCE SYSTEM IN INDIA: The following institutes are providing different Home Loan product to the different class of the people in the society and conduct the activity of financing and refinancing in the sector: 1. Scheduled Commercial Banks 2. Housing Finance Companies 3. Scheduled Cooperative Banks (Scheduled State Co-operative Banks, Scheduled District Cooperative Banks and Scheduled Urban Cooperative Banks) 4. Agriculture and Rural Development Banks 5. State Level Apex Co-operative Housing Finance Societies NHB Refinance Disbursements • NHB extends financial assistance to banks, HFCs, and cooperative sector institutions, towards their individual housing loans. • Refinance by NHB has increased substantially from Rs. 1,008 crore in 2000-01 to Rs.5, 632 crore in 2005-06 and to Rs.17, 542 crore in 2012-13. SCBs account for a major component of disbursement • Cumulative disbursement by NHB is Rs.86, 277 crore between 2006-07 and 2012-13 of which 52 percent is to SCBs and 46 percent to HFCs.