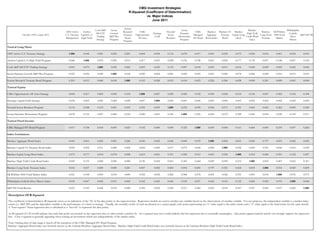

1. CMG Investment Strategies

R-Squared (Coefficient of Determination)

vs. Major Indices

June 2011

System

Cook S&P Scotia Scotia Barclays Philadelphia

AIFS Active Anchor Research CMG Howard CMG Barclays Barclays US Barclays Barclays DJ Wilshire

500 ETF Growth Heritage Dynamic High Yield Gold &

October 1993 to June 2011 U.S. Treasury Capital L/S Treasury Opportunistic Sector Managed Aggregate Treasury Equity Long Long-Term 5000 Total S&P 500 TR

Trading S&P Plus Gold Momentum Credit Bond Silver

Management High Yield Bond All Asset Rotation HY Bond Bond Index Bond Short Treasury Market

Strategy Program Program Index Miners

Program

Tactical Long/Short:

AIFS Active U.S. Treasury Strategy 1.000 0.044 0.001 0.023 0.201 0.004 0.054 0.116 0.078 0.017 0.041 0.055 0.073 0.000 0.016 0.061 0.018 0.051

Anchor Capital L/S High Yield Program 0.044 1.000 0.070 0.050 0.013 0.217 0.003 0.028 0.156 0.338 0.061 0.002 0.177 0.135 0.007 0.148 0.047 0.149

Cook S&P 500 ETF Trading Strategy 0.001 0.070 1.000 0.045 0.060 0.003 0.050 0.153 0.007 0.018 0.003 0.011 0.014 0.000 0.000 0.005 0.002 0.006

Scotia Partners Growth S&P Plus Program 0.023 0.050 0.045 1.000 0.018 0.030 0.064 0.001 0.000 0.003 0.001 0.000 0.074 0.006 0.000 0.014 0.013 0.019

System Research Treasury Bond Program 0.201 0.013 0.060 0.018 1.000 0.103 0.028 0.019 0.018 0.023 0.226 0.206 0.028 0.000 0.241 0.000 0.065 0.000

Tactical Equity:

CMG Opportunistic All Asset Strategy 0.004 0.217 0.003 0.030 0.103 1.000 0.007 0.295 0.429 0.192 0.030 0.002 0.619 0.136 0.007 0.452 0.162 0.394

Heritage Capital Gold Strategy 0.054 0.003 0.050 0.064 0.028 0.007 1.000 0.003 0.001 0.000 0.005 0.000 0.001 0.002 0.002 0.002 0.042 0.002

Howard Sector Rotation Program 0.116 0.028 0.153 0.001 0.019 0.295 0.003 1.000 0.236 0.090 0.024 0.071 0.351 0.063 0.065 0.262 0.045 0.249

Scotia Dynamic Momentum Program 0.078 0.156 0.007 0.000 0.018 0.429 0.001 0.236 1.000 0.325 0.000 0.072 0.529 0.343 0.054 0.548 0.102 0.511

Tactical Fixed Income:

CMG Managed HY Bond Program 0.017 0.338 0.018 0.003 0.023 0.192 0.000 0.090 0.325 1.000 0.039 0.000 0.161 0.444 0.005 0.278 0.037 0.260

Index Correlations:

Barclays Aggregate Bond Index 0.041 0.061 0.003 0.001 0.226 0.030 0.005 0.024 0.000 0.039 1.000 0.854 0.001 0.049 0.797 0.003 0.042 0.005

Barclays Capital US Treasury Bond Index 0.055 0.002 0.011 0.000 0.206 0.002 0.000 0.071 0.072 0.000 0.854 1.000 0.036 0.009 0.921 0.026 0.016 0.018

Barclays Equity Long Short Index 0.073 0.177 0.014 0.074 0.028 0.619 0.001 0.351 0.529 0.161 0.001 0.036 1.000 0.212 0.024 0.551 0.122 0.457

Barclays High Yield Credit Bond Index 0.000 0.135 0.000 0.006 0.000 0.136 0.002 0.063 0.343 0.444 0.049 0.009 0.212 1.000 0.003 0.401 0.062 0.367

Barclays Long-Term Treasury Index 0.016 0.007 0.000 0.000 0.241 0.007 0.002 0.065 0.054 0.005 0.797 0.921 0.024 0.003 1.000 0.014 0.020 0.009

DJ Wilshire 5000 Total Market Index 0.061 0.148 0.005 0.014 0.000 0.452 0.002 0.262 0.548 0.278 0.003 0.026 0.551 0.401 0.014 1.000 0.076 0.973

Philadelphia Gold & Silver Miners Index 0.018 0.047 0.002 0.013 0.065 0.162 0.042 0.045 0.102 0.037 0.042 0.016 0.122 0.062 0.020 0.076 1.000 0.060

S&P 500 Total Return 0.051 0.149 0.006 0.019 0.000 0.394 0.002 0.249 0.511 0.260 0.005 0.018 0.457 0.367 0.009 0.973 0.060 1.000

Description Of R-Squared

The coefficient of determination (R-Squared) serves as an indication of the “fit’ of the data points to the regression line. Regression models are used to predict one variable based on the observations of another variable. For our purposes, the independent variable is a market index

return (i.e. S&P 500) and the dependent variable is the performance of a fund or strategy. Visually, the monthly results of each are plotted on a scatter graph, each point representing an “x” value equal to the index return and a “y” value equal to the fund return for the same month.

A “least-squares” linear regression line is calculated as a “best-fit” to represent the data points.

An R-squared of 1.00 would indicate that each data point was located on the regression line; in other words, a perfect fit. An r-squared near zero would indicate that the regression line is essentially meaningless - date points appear random and do not strongly support the regression

line. A low r-squared is generally appealing when seeking an investment which acts independently of the market index.

Note: Starting date of data range is based off the inception of the CMG Managed HY Bond Program.

Barclays Aggregate Bond Index was formerly known as the Lehman Brothers Aggregate Bond Index. Barclays High Yield Credit Bond Index was formerly known as the Lehman Brothers High Yield Credit Bond Index

2. CMG Investment Strategies

Correlation Coefficient

vs. Major Indices

June 2011

System

Cook S&P Scotia Scotia Barclays

AIFS Active Anchor Research CMG Howard CMG Barclays Barclays US Barclays Barclays DJ Wilshire Philadelphia

500 ETF Growth Heritage Dynamic High Yield

October 1993 to June 2011 U.S. Treasury Capital L/S Treasury Opportunistic Sector Managed Aggregate Treasury Equity Long Long-Term 5000 Total Gold & Silver S&P 500 TR

Trading S&P Plus Gold Momentum Credit Bond

Management High Yield Bond All Asset Rotation HY Bond Bond Index Bond Short Treasury Market Miners

Strategy Program Program Index

Program

Tactical Long/Short:

AIFS Active U.S. Treasury Strategy 1.000 0.209 0.032 0.150 0.449 (0.064) (0.232) (0.340) (0.280) (0.130) 0.203 0.234 (0.270) (0.021) 0.125 (0.247) 0.135 (0.225)

Anchor Capital L/S High Yield Program 0.209 1.000 (0.265) (0.224) 0.113 0.466 (0.057) 0.166 0.395 0.581 0.246 0.042 0.421 0.368 0.082 0.385 0.217 0.385

Cook S&P 500 ETF Trading Strategy 0.032 (0.265) 1.000 0.213 0.245 (0.057) 0.224 (0.391) (0.082) (0.134) 0.058 0.104 (0.117) 0.001 0.017 0.074 (0.039) 0.078

Scotia Partners Growth S&P Plus Program 0.150 (0.224) 0.213 1.000 0.135 (0.174) 0.253 (0.023) (0.003) 0.051 (0.032) 0.015 (0.272) 0.076 (0.022) (0.120) (0.113) (0.137)

System Research Treasury Bond Program 0.449 0.113 0.245 0.135 1.000 0.322 (0.167) (0.138) (0.133) 0.151 0.475 0.454 (0.167) (0.014) 0.491 (0.006) 0.256 0.011

Tactical Equity:

CMG Opportunistic All Asset Strategy (0.064) 0.466 (0.057) (0.174) 0.322 1.000 0.085 0.543 0.655 0.438 0.173 0.042 0.787 0.369 0.085 0.673 0.403 0.627

Heritage Capital Gold Strategy (0.232) (0.057) 0.224 0.253 (0.167) 0.085 1.000 0.056 0.031 (0.011) (0.071) (0.021) (0.030) (0.040) (0.044) (0.040) 0.205 (0.044)

Howard Sector Rotation Program (0.340) 0.166 (0.391) (0.023) (0.138) 0.543 0.056 1.000 0.486 0.299 (0.156) (0.266) 0.592 0.251 (0.255) 0.512 0.213 0.499

Scotia Dynamic Momentum Program (0.280) 0.395 (0.082) (0.003) (0.133) 0.655 0.031 0.486 1.000 0.570 (0.019) (0.268) 0.727 0.586 (0.233) 0.741 0.320 0.715

Tactical Fixed Income:

CMG Managed HY Bond Program (0.130) 0.581 (0.134) 0.051 0.151 0.438 (0.011) 0.299 0.570 1.000 0.198 0.012 0.402 0.666 0.069 0.527 0.193 0.510

Index Correlations:

Barclays Aggregate Bond Index 0.203 0.246 0.058 (0.032) 0.475 0.173 (0.071) (0.156) (0.019) 0.198 1.000 0.924 (0.025) 0.221 0.893 0.052 0.206 0.073

Barclays Capital US Treasury Bond Index 0.234 0.042 0.104 0.015 0.454 0.042 (0.021) (0.266) (0.268) 0.012 0.924 1.000 (0.190) (0.097) 0.960 (0.160) 0.128 (0.135)

Barclays Equity Long Short Index (0.270) 0.421 (0.117) (0.272) (0.167) 0.787 (0.030) 0.592 0.727 0.402 (0.025) (0.190) 1.000 0.461 (0.154) 0.742 0.349 0.676

Barclays High Yield Credit Bond Index (0.021) 0.368 0.001 0.076 (0.014) 0.369 (0.040) 0.251 0.586 0.666 0.221 (0.097) 0.461 1.000 (0.055) 0.633 0.249 0.605

Barclays Long-Term Treasury Index 0.125 0.082 0.017 (0.022) 0.491 0.085 (0.044) (0.255) (0.233) 0.069 0.893 0.960 (0.154) (0.055) 1.000 (0.119) 0.142 (0.096)

DJ Wilshire 5000 Total Market Index (0.247) 0.385 0.074 (0.120) (0.006) 0.673 (0.040) 0.512 0.741 0.527 0.052 (0.160) 0.742 0.633 (0.119) 1.000 0.275 0.986

Philadelphia Gold & Silver Miners Index 0.135 0.217 (0.039) (0.113) 0.256 0.403 0.205 0.213 0.320 0.193 0.206 0.128 0.349 0.249 0.142 0.275 1.000 0.245

S&P 500 Total Return (0.225) 0.385 0.078 (0.137) 0.011 0.627 (0.044) 0.499 0.715 0.510 0.073 (0.135) 0.676 0.605 (0.096) 0.986 0.245 1.000

Description Of Correlation

Correlation, represented by the correlation coefficient (R), measures the extent of linear association of two variables, and ranges between -1 and +1. Perfect positive correlation (a correlation co-efficient of +1) implies that as one security moves, either up or down, the other security will

move in lockstep, in the same direction. Alternatively, perfect negative correlation (correlation co-efficient of -1) means that if one security moves in either direction the security that is perfectly negatively correlated will move by an equal amount in the opposite direction. If the

correlation is 0, the movements of the securities is said to have no correlation. It is completely random. For example, if one security moves up or down there is as good a chance that the other will move either up or down, but the way in which they move is totally random. A

correlation between -0.50 and 0.50 signifies a weak relationship between a strategy and either its peers or the general markets. We believe incorporating non-correlating strategies into a portfolio is essential for diversification.

Note: Starting date of data range is based off the inception of the CMG Managed HY Bond Program.

Barclays Aggregate Bond Index was formerly known as the Lehman Brothers Aggregate Bond Index. Barclays High Yield Credit Bond Index was formerly known as the Lehman Brothers High Yield Credit Bond Index.