The History of Banking in One Chart

•Transferir como PPTX, PDF•

229 gostaram•71,951 visualizações

This presentation provides an original, but brief, new way to view the history of banking in America.

Mais conteúdo relacionado

Destaque

Destaque (19)

Último

Último (20)

The History of Banking in One Chart

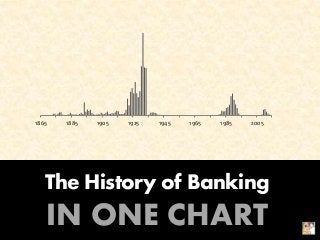

- 1. The History of Banking IN ONE CHART 1865 1885 1905 1925 1945 1965 1985 2005

- 2. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year A Chart About Bank Failures There is no more powerful force in the U.S. bank industry than the credit cycle – the undulating pattern of booms and busts that gave us the Roaring Twenties and the Great Depression; the housing bubble and the Financial Crisis. Nothing better captures the credit cycle’s savagery than the failures left in its wake. More than 17,000 banks have gone under since 1865, equating to an annual average of 115.

- 3. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The National Banking Acts of 1863 & 1864 The starting point for any conversation about bank history is the Civil War, or, to be more precise, the National Banking Acts of 1863 and 1864. These created the bank system we know today by (1) monopolizing the printing of bank notes (i.e., issuing money) by the federal government, and (2) providing a mechanism through which banks could acquire national, as opposed to state, charters.

- 4. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The Gilded Age: The Civil War to the Panic of 1907 The Gilded Age, a term coined by Mark Twain, was a particularly volatile episode in bank history. Thanks to rapid economic expansion fueled by the American industrial revolution as well as lax regulatory oversight, bank failures became a common occurrence. Two crises in particular, the Panics of 1873 and 1893, ignited full-blown economic depressions.

- 5. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year 1913: Creation of the Federal Reserve The Federal Reserve was created in 1913 in an effort to reduce, if not stop, the frequent occurrence of banking panics. To this end, it was empowered to lend hard currency to banks besieged by depositors withdrawing their money en masse. The theory was that, by providing access to all the currency sound banks needed to meet withdrawal requests, it would remove depositors’ incentive to run on banks in the first place.

- 6. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year Agricultural Depression of the 1920s After World War I ended, the demand for American agricultural products plunged throughout Europe. Farmers on the continent were again free to produce crops and the warring parties no longer needed the profusion of supplies to feed their armies. Prices for corn, tobacco, and other crops plummeted in the U.S., taking thousands of small rural banks down too, as farmers could no longer afford to service their loans.

- 7. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The Great Depression of the 1930s Following a decade of excess throughout urban America, the stock market crashed in 1929. In an effort to calm global markets and maintain the international gold standard, the Federal Reserve unwittingly aggravated the situation by raising interest rates and cutting the money supply. The Great Depression followed, leaving more than 5,000 failed banks in its wake.

- 8. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The Great Moderation: 1945-1975 Bank historians call the unusually quiet period from the end of World War II to the mid- 1970s the Great Moderation. Few banks failed over this stretch thanks to (1) increased regulatory oversight under FDR’s New Deal legislation, (2) heightened conservatism among bankers with firsthand experience of the Great Depression, (3) rapid economic expansion following the war, and (4) the introduction of national deposit insurance.

- 9. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The OPEC Oil Embargos of 1973 & 1979 OPEC’s twin oil embargoes in the 1970s, a response to America’s support for Israel in the 1973 Yom Kippur War, set off a series of events that changed banking forever. Most importantly, high oil prices accelerated inflation, which then caused the Federal Reserve to raise short-term interest rates to nearly 20%. This triggered a deep recession in 1974 and caused banks to hemorrhage net interest income.

- 10. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The 1980s: A Most Volatile Decade The 1970s turmoil culminated in 3 distinct financial crises a decade later. (1) An energy crisis fueled by high gas prices led to the first too-big-to-fail bank, Continental Illinois, which was nationalized by the FDIC in 1984. (2) High funding costs from the Fed’s assault on inflation yielded the S&L Crisis. (3) And the recycling of petrodollars from oil producers into loans to Latin American governments caused the Less Developed Country Crisis.

- 11. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year 1990s: The “Mergers of Equals” In an effort to make the bank industry more resilient to regional economic downturns and the stiflingly high short-term interest rates of the 1980s, Congress deregulated the industry by, among other things, allowing banks to operate across interstate lines on a national basis for the first time in history. This sparked a wave of bank mergers – the “mergers of equals” – that gave us the nationwide branch networks we know today.

- 12. 0 500 1,000 1,500 2,000 1865 1885 1905 1925 1945 1965 1985 2005 AnnualBankFailures Year The Financial Crisis of 2008-09 On its own, the financial crisis of 2008-09 seems to pale in comparison to the severity of the combined crises of the 1980s – to say nothing of the Great Depression. But because it came on the heels of the 1990s merger wave, the banks that did fail were almost unrecognizably massive compared to earlier periods. Thanks to imprudent bets on subprime mortgages, more than 500 lenders have since ceased operations.

- 13. Looking for more information like this? The Motley Fool’s mission is to help the world invest better. We’ve done this over the past 20 years by thinking long term and outside the box – even if that means turning Wall Street on its head. To learn more about what The Motley Fool thinks about current investment trends, and receive a special free report about what might be the next big industry to come out of Silicon Valley, simply click here now. 1865 1885 1905 1925 1945 1965 1985 2005 Created by John J. Maxfield, The Motley Fool