Baixar para ler offline

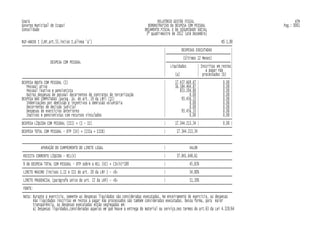

Este relatório apresenta informações sobre as despesas com pessoal, dívida consolidada líquida e garantias concedidas pelo município de Icapuí-CE no 3o quadrimestre de 2012. Mostra que as despesas com pessoal representaram 45,83% da receita corrente líquida, abaixo do limite máximo de 54%. A dívida consolidada líquida foi de R$6.486.945,89, correspondendo a 17,14% da RCL, também abaixo do limite de 120%. Nenhuma garantia foi concedida no per