Russian Call Girls In Gurgaon ❤️8448577510 ⊹Best Escorts Service In 24/7 Delh...

MRV Initiation

1. MRV Engenharia (MRVE3)

Sector: Real Estate & Construction

Target Price: R$44.00 / US$23.61 (as of September 19th)

Current Price: R$28,99 / US$15.55 (as of September 19th)

Upside: 51.8% / 35.3%

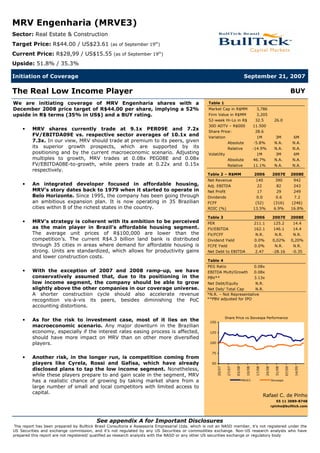

Initiation of Coverage September 21, 2007

The Real Low Income Player BUY

We are initiating coverage of MRV Engenharia shares with a Table 1

December 2008 price target of R$44.00 per share, implying a 52% Market Cap in R$MM 3,786

upside in R$ terms (35% in US$) and a BUY rating. Firm Value in R$MM 3,205

52-week Hi-Lo in R$ 32.5 26.0

30D ADTV – R$000 11.500

MRV shares currently trade at 9.1x PER09E and 7.2x

• Share Price: 28.6

FV/EBITDA09E vs. respective sector averages of 10.1x and Variation 1M 3M 6M

7.3x. In our view, MRV should trade at premium to its peers, given Absolute -5.8% N.A. N.A.

its superior growth prospects, which are supported by its Relative -14.9% N.A. N.A.

positioning and by the current macroeconomic scenario. Adjusting Volatility 1M 3M 6M

multiples to growth, MRV trades at 0.08x PEG08E and 0.08x Absolute 46.7% N.A. N.A.

FV/EBITDA08E-to-growth, while peers trade at 0.22x and 0.15x Relative 11.1% N.A. N.A.

respectively.

Table 2 – R$MM 2006 2007E 2008E

Net Revenue 140 390 942

An integrated developer focused in affordable housing,

• Adj. EBITDA 22 82 243

MRV’s story dates back to 1979 when it started to operate in Net Profit 17 29 249

Belo Horizonte. Since 1995, the company has been going through Dividends 0.0 0.6 7.2

an ambitious expansion plan. It is now operating in 35 Brazilian FCFF (52) (316) (246)

cities within 8 of the richest states in the country. ROIC (%) 13.5% 6.9% 16.8%

Table 3 2006 2007E 2008E

MRV’s strategy is coherent with its ambition to be perceived

• PER 211.1 125.2 14.4

as the main player in Brazil’s affordable housing segment. FV/EBITDA 162.1 146.1 14.4

The average unit prices of R$100,000 are lower than the FV/FCFF N.R. N.R. N.R.

competition’s. The current R$4.3 billion land bank is distributed Dividend Yield 0.0% 0,02% 0,20%

through 35 cities in areas where demand for affordable housing is FCFE Yield 0.0% N.R. N.R.

strong. Units are standardized, which allows for productivity gains Net Debt to EBITDA 2.47 -28.16 -0.35

and lower construction costs.

Table 4

PEG Ratio 0.08x

With the exception of 2007 and 2008 ramp-up, we have

• EBITDA Multi/Growth 0.08x

conservatively assumed that, due to its positioning in the PBV** 3.13x

low income segment, the company should be able to grow Net Debt/Equity N.R.

slightly above the other companies in our coverage universe. Net Deb/ Total Cap N.R.

A shorter construction cycle should also accelerate revenue *N.R. – Not Representative

**PBV adjusted for IPO

recognition vis-à-vis its peers, besides diminishing the PoC

accounting distortions.

Share Price vs Ibovespa Performance

As for the risk to investment case, most of it lies on the

• 150

macroeconomic scenario. Any major downturn in the Brazilian

economy, especially if the interest rates easing process is affected, 125

should have more impact on MRV than on other more diversified

players. 100

75

Another risk, in the longer run, is competition coming from

•

players like Cyrela, Rossi and Gafisa, which have already 50

20/07

27/07

03/08

10/08

17/08

24/08

31/08

07/09

14/09

disclosed plans to tap the low income segment. Nonetheless,

while these players prepare to and gain scale in the segment, MRV

has a realistic chance of growing by taking market share from a MRVE3 Ibovespa

large number of small and local competitors with limited access to

capital.

Rafael C. de Pinho

55 11 3089-8748

rpinho@bulltick.com

See appendix A for Important Disclosures

This report has been prepared by Bulltick Brasil Consultoria e Assessoria Empresarial Ltda. which is not an NASD member, it’s not registered under the

US Securities and exchange commission, and it’s not regulated by any US Securities or commodities exchange. Non-US research analysts who have

prepared this report are not registered/ qualified as research analysts with the NASD or any other US securities exchange or regulatory body

2. Investment Thesis: Three Reasons Why we Like MRV

1 – MRV is well positioned to profit from the Brazilian housing boom.

Among Brazil’s listed real estate companies, MRV is the only one who can claim full

Positioning: Fully exposed

exposure to lower income segments. Some of the major players in the sector recently

to lower income segments.

disclosed their strategies to tap lower income segments which will include: (i) shift land

banks from now on to more affordable housing projects; (ii) redesign products and

brands and (iii) launch a higher percentage of affordable segment projects as a

percentage of the launchings pipeline going forward.

However, 20% to 25% exposure to the segment in terms of future launchings does not

look enough. Investors willing to play the low income segment in Brazil have MRV as an

option that presents proven and sound track record and a solid brand, widely recognized

as being 100% focused in the affordable housing segment.

Below we present the recent evolution of launchings in terms of average price per unit

Recent launchings track

launched by some developers. It is important to note MRV is way ahead of competition in

record: consistent with

terms of product positioning in the lower income segments.

positioning.

Exhibit 1: Average price/unit launched – in R$ thousands

600

500

400

300

200

100

-

Company Cyrela Gafisa Klabin Rossi Tecnisa MRV Rodobens

Segall

2005 2006 1H07

Source: Companies and Bulltick

The first requisite to launch low income developments, as for any development, is to have

the land bank in the right place. We present below MRV’s land bank as of 2Q07.

Exhibit 2: MRV’s Land Bank and Average Unit Prices

State PSV (R$ MM) % Potential Units Avg Price (R$/Unit)

SP 2,619 60.4% 24,924 105,099

MG 779 18.0% 9,588 81,271

RJ 235 5.4% 2,960 79,364

DF 210 4.8% 1,542 136,267

ES 179 4.1% 1,912 93,778

GO 172 4.0% 1,734 99,250

PR 122 2.8% 1,324 91,993

SC 17 0.4% 181 95,647

4,334 100% 44,165 98,138

Source: MRV

It is interesting to note that not only past launchings show MRV consistent positioning in

Land bank’s average unit

the segment, but also does the profile of its R$4.3 billion PSV land bank going forward.

price: R$98,138.

Besides being diversified in 36 cities within 8 of the richest states in Brazil, unit sales

prices are on average R$98,138.

The cities where MRV’s land bank is located and the strategy behind their choice are also

MRV’s current competition

worth mentioning. MRV targets cities with at least 200,000 inhabitants, where it will

is formed by small players…

normally find enough demand for its developments. Besides having demand in place, this

kind of city presents an advantage: lack of competition. As the major players are

2

3. traditionally more active in state capitals, in most of the cases MRV ends up competing in

most of the cases against small local players, which lack the capital and structure to be

fierce opponents.

Exhibit 3: Geographic Positioning – MRV

GOIÁS

Brasília

MINAS GERAIS

Goiânia

BRAZIL

Belo Horizonte

Uberaba

Uberlândia

Contagem

Nova Lima

ESPÍRITO

SANTO

Serra

RIO DE JANEIRO

PARANÁ

Rio de Janeiro

Curitiba

Londrina

Maringá

SÃO PAULO

São Paulo Campinas

SANTA São Bernardo Sta. Bárbara do Oeste

S.J. Campos Piracicaba

CATARINA

Santo André Americana

Mauá Paulínia

Taubaté Marília

Joinville

Cotia Bauru

Sorocaba Araraquara

Mogi das Cruzes São Carlos

Jundiaí Ribeirão Preto

S.J. Rio Preto Franca

Source: MRV

Last but not least, we shall examine MRV’s product strategy. Building affordable housing

Key to profitability in low

is something that demands a change in the way traditional companies look at the

income housing:

standardization. development process. Instead of tailor-made projects, standardization comes in play as a

key to a successful and profitable operation. Exhibit 5 shows our view of different product

levels and the corresponding price sensitivity at each level.

Exhibit 4: Real Estate Product Levels

Source: Bulltick

MRV positioned itself as a leader in the low income segment by understanding clients’

Standardization: 3 basic

demand for monthly installments to fit their income. Standardization was the answer to

products replicated

decrease unit prices. The company designed 3 basic types of projects that are used

everywhere…

depending on the local demand.

3

4. On top of minimizing design costs other companies face on a per-project basis, the

… resulting in low design

costs and allowing for gains approval process tends to be faster as the standardized project becomes known of the

of scale. authorities. Additionally, raw material purchases can be concentrated on fewer suppliers

and executed by the company’s headquarters in a centralized manner, allowing for gains

of scale. Exhibit 6 depicts the three basic product types designed by MRV.

Exhibit 5: MRV’s Product Types

Village

100-220

Two parking spaces;

Two to four bedrooms

with suite.

Spazio

Unit Price (R$ thousands)

70-140

One parking space; Two to

three bedrooms, suite

option; Balcony.

Parque

One parking space; Two

77

to three bedrooms, no

suite option.

40-55 42-70 70-120

Apartment Area (m2)

Source: MRV and Bulltick

4

5. 2 – MRV is sticking to the right strategy

Besides being uniquely positioned, the company has a solid brand name in a segment

MRV has no reason to

where most of the big names either lack one or are still in the making. Additionally, the

change. On the contrary,

competition will have to capital investment made earlier this year by Autonomy Capital allowed the company to

change. accelerate its already fast-paced growth plans and expand its land bank. The latest boost

to the company’s growth plans came after the roughly R$1 billion in equity issued.

Growth way before the IPO. Differently from many real estate companies, MRV has been paving its growth long before

its IPO. Not only has the company been growing operationally, but also geographically.

MRV’s geographical expansion which started in 1995 and since then reached 35 cities,

followed a logical path, using regional offices as operational hubs from where it expanded

to surrounding cities. The results of such strategy can be seen on exhibit 7, a 61% and

43% CAGR in the PSV of launchings and in contracted sales, respectively, in the 2004-

2006 period.

Exhibit 6: Operational Highlights

2004 2005 2006 1H07 CAGR '04-'06

Launchings

Launching PSV - MRV Stake - (R$ MM) 130 184 337 433 61%

Average Price per Unit Launched - (R$) 80,477 104,166 112,935 96,910

2

Launched Usable Area (m ) 101,434 133,294 229,331 286,595

Number of developments launched 28 45 67 61

Number of units launched 1,618 1,769 2,987 4,463 36%

2

Average Price (R$/m ) 1,312 1,421 1,512 1,723

Sales

Contracted Sales - MRV Stake - (R$ MM) 100 110 206 276 43%

Average Price per Unit Sold - (R$) 66,611 81,038 99,201 103,869

2

Usable area sold (m ) 88,703 90,043 148,953 181,799

Number of units sold 1,506 1,361 2,079 2,658 17%

2

Average Price (R$/m ) 1,148 1,245 1,430 1,627

Source: MRV

Despite the accelerated expansion observed in recent years, MRV has ambitious growth

“MRV 40,000”: strategic

moves and debottlenecking plans for the coming years: recently it has disclosed the “MRV 40,000” initiative,

to boost production. consisting of a plan to enable the company to deliver 40,000 units a year. In order to do

that, MRV started by defining production objectives for each team in the company in

terms of production. In order to reach those objectives, the company’s processes and

production bottlenecks were mapped so that the teams could start working on solving

them.

Additionally, such an ambitious plan would not be possible without heavy technological

support. MRV has ERP software running to manage its different construction sites and is

taking steps to make its systems capable of handling the desired volumes.

Regarding measures of the plan already taken, the regional offices administrative

routines and all the purchasing structures are now centralized as much as possible in Belo

Horizonte, leaving the regional offices focus on operational and commercial issues

regarding the developments.

5

6. 3 - Macroeconomic scenario: winds are blowing in the right direction

The elements that allow for MRV to grow and exploit Brazil’s enormous housing deficit

apply to every other company in the sector: the country’s monetary easing process,

increased credit availability, economic stability and higher populations’ disposable

income. Nonetheless, MRV’s case is much more dependent on these fundamentals due to

its average client profile. Our view is that not only these conditions are sustainable, given

the current economic scenario, but are improving much faster than previously expected,

especially when credit availability is concerned.

As mortgages become increasingly affordable vis-à-vis other options such as paying rents

and the country’s economic stability is assimilated by the average Brazilian, the idea of

contracting mortgages, a long term commitment, is seriously considered.

Nonetheless, it was not long ago when as companies had to finance clients given banks

limited appetite for mortgages. In order to do that, construction had to be delayed as

much as possible so cash flows became smoother and working capital requirements

reduced.

The solution allowing MRV to meet client’s needs and desires became concrete as banks’

Private banks willingness to

willingness to lend money to homebuyers shifted from apathy to a frantic market share

lend money allowed for

fight. Banks came in to lend homebuyers money as soon as construction was finished, in

shorter construction cycles.

turn enabling the company to curtail the construction cycle, delivering products faster.

This way, besides solving marketing issues, the cash flows of a typical development were

improved as a project can be developed faster than previously, yielding better returns.

Mortgage conditions have improved much faster than previously expected by market

Mortgage conditions are

participants. As the recent offer of 90% of loan-to-value mortgages by Caixa Econômica

improving faster than

Federal reaches the overall market, in the near future, the biggest barrier to real estate

expected.

purchase decision, down payment, should be minimized. The down payment issue is

especially important when we put in perspective the fact that the Brazilian population is

not prone to savings. As a result, most of the low-income families cannot hold up for the

current 20% down payment standard.

On top of the favorable macro scenario, demographics in Brazil also show MRV has large

Demographics point to at

room to grow in the coming years. The most recent census in Brazil points out for the

least 21 target cities within

existence of at least 21 cities with around 200 thousand inhabitants, where the GDP per

MRV’s geographical reach.

capita indicates potential for MRV to prospect business. Our analysis included only cities

within MRV’s current geographic presence in the Southeast, South and Midwest regions of

Brazil.

Exhibit 7: Potential New Cities, GDP per capita vs. inhabitants

1,800

P o rt o A le gre

1,600

G ua rulho s

1,400

1,200

D uque de C a xia s

1,000

Osasco

800

C uia bá

N it e ró i

600 D ia de m a

C a xia s do S ul

F lo ria nó po lis

C a no a s

S uza no

400

P re s ide nt e P rude nt e

200

S ã o J o s é do s

A ra ç a t uba

Inda ia t uba P inha is

-

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

P e r C a pit a GD P ( R $ )

Source: IBGE, Bulltick

6

7. Exhibit 8: MRV’s Current Markets, GDP per capita vs. inhabitants

3,000

B e lo H o rizo nt e

B ra s í lia

2,500

2,000

C urit iba

1,500

C a m pina s

S ã o B e rna rdo do

C a m po

Sã o J o s é do s

1,000 C a m po s

Ube rlâ ndiaS a nt o A ndré

M a uá

Lo ndrina S o ro c a ba

P ira c ic a ba

B a uru S e rra

J o inv ille

500 M a ringá

T a uba t é J undia í

F ra nc a Ube ra ba

C o t ia

M a rí lia A m e ric a na

-

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

P e r C a pit a G D P ( R $ )

Source: IBGE, Bulltick

7

8. Valuation

We defined MRV shares price target using a DCF-based model and then compared its

We discount MRV’s cash

multiples with the peers in our coverage universe. In order to reach our DCF PT we

flows at the highest WACC

assumption among covered discounted cash flows to the firm (FCFF) at a WACC of 13.26% in R$ terms, the highest

companies. for companies in our coverage universe. We also applied a 4% nominal perpetuity growth

in R$ terms. Exhibit 11 depicts our discount rates, target capital structure, the resulting

WACC and valuation outcome.

Our total return target price for Dec. 2008 reaches R$44.00 for MRV shares, implying a

potential upside of 51.8% in R$ (or 35.3% in US$) and a BUY rating.

Exhibit 9: Discount and Growth Rates

US Risk Free Rate 4.5%

Brazil Country Risk 1.75%

Beta 1.30

Equity Risk Premium 6.0%

LT R$ Depreciation 2.0%

Ke (R$) 16.05%

Weight - Equity 70.00%

Cost of Debt, in R$, Before Taxes 10.3%

Effective Tax Rate 34.0%

Kd (R$) 6.77%

Weight - Debt 30.00%

WACC (R$) 13.26%

Forecasted Period 2007 – 2020

Perpetuity Growth 4.00%

Source: Bulltick

It is interesting to note MRV’s cash flows become positive sooner that those of other real

estate companies. The difference lies on its lower working capital needs, a direct result of

its business model. For more details please refer to the investment case section.

Exhibit 10: Cash Flows

2005 2006 2007E 2008E 2009E 2010E 2011E 2012E

EBITDA 25 22 21 243 446 629 760 844

Taxes (4) (4) (4) (40) (73) (102) (122) (136)

Change in Net Working Assets (20) (69) (330) (444) (434) (383) (222) (111)

CAPEX (0) (2) (3) (5) (3) (3) (3) (4)

FCFF 1 (52) (316) (246) (63) 142 412 594

Source: Bulltick

Main Valuation Assumptions and Sensitivity Analysis

Our DCF model main inputs are the potential sales value (PSV) of launchings and the

company’s typical sales velocity, client payments and construction schedule, from which

we derive cash flows. Except for gross margins, which we conservatively reduce at a 50

bps / year pace, we use the other inputs in line with the company’s current business

model. It is important to notice that so far the company has delivered results in line or

above these expectations.

We view MRV as well positioned to have sustainable and above-average launchings

growth. The company should deliver explosive 180% and 95% launchings growth in 2007

and 2008 respectively. Investors should bear in mind that the land bank to support this

growth is secured, as stated in 2Q07 results release. Additionally, we expect MRV to

deliver growth at ratios slightly above its peers in the long run. The normalized

launchings and growth assumptions in the 2008-2012 period for covered companies are

summarized in exhibit 13.

8

9. Exhibit 11: Launchings Growth 2008-2012

250

Growth: conservatively in

line with higher segment

225

companies under coverage.

Index (2007 = 100)

200

175

150

125

100

2008 2009 2010 2011 2012

MRV Company Cyrela Gafisa Klabin Segall Rossi Tecnisa

Source: Bulltick

The faster pace applied to construction by MRV results in faster revenue recognition when

compared to other players, as it can be seen on exhibit 13 below. Additionally, exhibit 12

shows our sales velocity and construction costs assumptions for typical MRV’s

developments.

Exhibit 12: Revenue Recognition Assumptions

6M 12M 18M 24M

Sales Velocity 60% 14% 14% 12%

Cost Incurred 17% 42% 42% 0%

Recognized Revenues 10% 33% 45% 12%

Source: Bulltick

Exhibit 13: Revenue Recognition Patterns

120%

Shorter construction cycle

100%

translates in faster revenue 100%

recognition.

80%

60%

43%

40%

20%

0%

Launching 1st Year 2nd Year 3rd Year

Cyrela Klabin Segall Rossi Gafisa

Company Tecnisa MRV

Source: Bulltick

9

11. Multiples Analysis

Besides valuing MRV through our DCF model, we also performed multiple comparisons in

order to better understand the potential upside of the case. Our preferred multiple to

follow is PER09E, as we view 2009 as a more normalized year, not only to MRV but also

for its peers, when most of the growth companies are undergoing will be already factored

in.

Based on PER09E we see MRV trading at 9.1x, slightly discounted to the average for the

companies we cover. In our opinion, though, given the company’s superior growth

prospects and positioning, we see room for multiple expansion going forward, as results

start to be delivered.

Exhibit 15: PER09E ratios

16.0x 15.2x

12.0x 11.3x

11.1x

10.1x

9.1x

8.0x

7.1x

6.5x

6.1x

4.0x

Klabin Company Tecnisa MRV Average Rossi Cyrela Gafisa

Source: Bulltick

Another multiple worth analyzing is PER adjusted to growth. Looking at the PER08E-to-

growth we separate more stabilized stories, with earlier capitalization in relation to MRV,

from those still in the upswing movement in terms of launchings and sales. Using this

multiple we view MRV discounted to most of its peers as shown on exhibit 18.

Exhibit 16: PEG08E ratios

0.60x

0.48x

0.50x

0.40x

0.31x

0.30x

0.22x

0.20x 0.16x

0.16x

0.14x

0.08x

0.10x

0.04x

0.00x

Klabin MRV Tecnisa Company Rossi Average Gafisa Cyrela

Source: Bulltick

11

12. Risks

As a real estate company, in our opinion, the major risk for MRV’s case lies on the

Risks: Brazilian

macroeconomic front. Although we classify this as improbable, if the Brazilian economy

macroeconomic scenario…

suffers any major downturn in the near future, it may impact interest rates and the

country stability, limiting growth for MRV and its peers.

Although in the short-term it is still far from being an issue to MRV given its geographic

… long run competition from

diversification, positioning and track record, we view the movements of big names like

the big three…

Gafisa, Rossi and Cyrela into MRV’s segment as a potential risk in the future. Increased

competition could impact margins and hurt the company’s profitability in the long run.

As a third risk impacting not only MRV but the whole sector, additional equity offerings

… and the real estate sector

expected to happen in the real estate sector could create short-term volatility for the

IPO pipeline.

shares as investors rebalance portfolios to participate in upcoming IPOs.

12

13. Brief Company Description

MRV story dates back to 1979 when it was founded in Belo Horizonte, Minas Gerais, by

Mr. Rubens Menin (current CEO). Over its long history in the real estate sector, MRV has

built a solid reputation among competition and especially with its clients.

Much before the Brazilian real estate sector boom, back in 1995, the company started

Geographically diversified

building the blocks to its current configuration by diversifying its operations

much before the current

Brazilian housing boom. geographically. Currently, MRV reaches 35 cities in 8 states. The expansion was backed

by a structure of regional offices, which help to coordinate efforts on a local basis, given

the considerable distance from some cities to the headquarters and the need for local

support during real estate developments.

Exhibit 17: MRV’s geographical expansion timeline

Nova Lima, St Barbara do

Oeste, Taubaté, Paulínia,

2007

Serra, Mauá and Cotia

Goiania

2006

2004 Mogi das Cruzes and Santo André

2003 Araraquara

Brasília, Rio de Janeiro and São Bernardo

2001

Maringá, Joinville, Marília, Jundiaí, Franca and

2000

São Paulo

Londrina and Curitiba

1999

1998 São José dos Campos and São Carlos

Piracicaba, Campinas, Sorocaba and Bauru

1997

São José, Rio Preto and Ribeirão Preto

1996

Uberaba, Urberlândia and Americana

1995

Contagem

1981

1979 Belo Horizonte

Source: MRV

The company is currently 100% focused in developing affordable housing, ranging from

100% focused in affordable

R$80,000 to R$200,000. It uses a highly standardized production process, based on 3

housing.

types of products: Parque, Spazio and Village. Alongside with its peers, the company

presented strong growth over the last couple of years given the improvements in the

Brazilian macroeconomic scenario.

Recently listed in BOVESPA’s Novo Mercado, MRV made a primary offering to prepare the

Listed in the Novo Mercado.

company to take advantage of the favorable winds and to profit from its unique

Primary-only offer prepared

positioning in the lower income segments. Exhibit 2 below summarizes the company’s

company to grow.

shareholding structure after the IPO conclusion.

Exhibit 18: MRV’s shareholders structure

Rubens Menin Autonomy Capital Unno Maio MA Cabaleiro

Free Float

Teixeira de Souza Two Sarl Participações Participações Participações

44,2%ON 11,6%ON 5,3%ON 2,5%ON 2,5%ON 33,9%ON

MRV

Source: MRV

13

17. APPENDIX A

IMPORTANT DISCLOSURES

Bulltick Brasil Consultoria e Assessoria Empresarial Ltda. is an affiliate of Bulltick LLC (The Firm). Bulltick LLC may do

business with the companies covered in this report, as a result, investors should be aware that the Firm may have a

conflict of interest that could affect the objectivity of this report. Investors should consider this report only as a single

factor in making their investment decision.

A. CONFLICTS OF INTEREST

From the companies covered in this report, Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, or its affiliates,

currently has, or has had within the past 12 months, Tecnisa and MRV as client and/or received compensation for products

and services provided to this company.

From the companies covered in this report, Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, or its affiliates,

managed or co-managed a public offering of securities for Tecnisa and MRV in the past 12 months, received

compensation for investment banking services from Tecnisa and MRV in the past 12 months.

Neither Bulltick Brasil Consultoria e Assessoria Empresarial Ltda nor any of its affiliates own equity securities of any of the

subject companies.

Analyst compensation is determined by Bulltick Brasil Consultoria e Assessoria Empresarial Ltda management and is not

linked to specific transactions or recommendations.

B. ANALYST CERTIFICATION

I, Rafael Pinho, author of this report, hereby certify that all of the views expressed in this report accurately reflect my

personal views about any and all of the subject issuer(s) or securities, no part of my compensation was, is , or will be

directly or indirectly related to the specific recommendation(s) or view(s) in this report. I have not received any

compensation from any of the subject companies in the past 12 months. I also certify that neither I nor any member of

my household serves as a director, officer, or advisory board member of any of the subject companies in this report.

C. INVESTMENT RATING

Investment ratings are determined by the ranges described below:

BUY: Total return of securities expected to be above 18% (in dollar terms) in the following 12 months

NEUTRAL: Total return of securities expected to be below 18% (in dollar terms) and above 8% (in dollar terms) in the

following 12 months.

SELL: Total return of securities expected to be below 8% (in dollar terms) in the following 12 months.

Price Target: The valuation method used to determine the price targets in this report were based on the discounted

cash flow methodology.

D. RISK RATINGS

Risks for the achievement of the target prices defined in this report include major change in our base case macro-

economic scenario, increase in interest rates and in the Brazil risk, reduction in the expectations for demand for real

estate in Brazil and impact on already listed stocks of new IPOs in Brazil´s real estate sector.

Based on last 6 months volatility of subject companies, and comparing them to the volatility of the Bovespa Index

(Ibovespa) in the same period, we define each subject company´s relative volatility in the following way: Company

High, Cyrela High, Gafisa High, Klabin Segall High, MRV High, Rossi Residencial High and Tecnisa High

17

18. OTHER DISCLOSURES

Bulltick Brasil Consultoria e Assessoria Empresarial Ltda and its subsidiaries, affiliates, shareholders, directors, officers,

employees, and licensors (“The Bulltick Parties”) will not be liable (individually, jointly, or severally) to you or any other

person as a result of your access, reception or use of the information contained in this document for indirect,

consequential, special, incidental, punitive, or exemplary damages, including, without limitation, lost profits, lost savings

and lost revenues (collectively, the “Excluded Damages”), whether or not characterized in negligence, tort, contract, or

other theory of liability.

The information contained in this document has been obtained from sources believed to be reliable, although its

accuracy and completeness cannot be guaranteed. All opinions, projections, and estimates constitute the judgment of

the author as of the date of the report and these, plus any other information contained in the report, are subject to

change without notice. Prices and availability of financial instruments also are subject to change without notice.

Bulltick Brasil Consultoria e Assessoria Empresarial Ltda and its affiliated companies have not taken any steps to insure

that the securities referred to in this report are suitable for any particular investor. The Report is for informational

purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. Securities mentioned

in the report are subject to investment risks, including the possible loss of the principal amount invested. Any decision

to purchase securities mentioned in the Report must take into account existing public information on such a security or

any registered prospectus.

The financial instruments mentioned in this document may not be eligible for sale in some countries. The Report is not

to be construed as providing investment services in any jurisdiction where the provision of such services would be

illegal.

Bulltick Brasil Consultoria e Assessoria Empresarial Ltda, its affiliated companies, and/or its officers, directors, or

shareholders, may from time to time have long or short positions in the financial instruments of the companies

mentioned in this document, engage in securities transactions in a manner inconsistent with this report, buy or sell from

customers on a principal basis, or serve in an advisory capacity.

Investing in non-US securities, including ADRs, may entail certain risks. The securities of non-US issuers may not be

registered with, and may not be subject to the reporting requirements of the US Securities and Exchange Commission.

There may be limited information available on foreign securities. Foreign companies are generally not subject to

uniform audit and reporting standards, practices and requirements comparable to those in the US Securities of some

foreign companies may be less liquid and their prices more volatile than securities of comparable US companies. In

addition, exchange rate movements may have an adverse effect on the value of an investment in a foreign stock and its

corresponding dividend payment for US investors.

The information contained in the report is privileged and confidential and intended solely for the recipients who have

been specifically authorized to receive it and it may not be further distributed. Bulltick Brasil Consultoria e Assessoria

Empresarial Ltda and its affiliates accept no liability whatsoever for the actions of third parties. Should you receive this

message by mistake you are hereby notified that any disclosure reproduction, distribution, or use of this message is

strictly prohibited.

The Report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the Report

refers to the website material of the Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates, the

Firm has not reviewed the linked site. Equally, except to the extent to which the Report refers to website material of

Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates, the Firm takes no responsibility for, and

makes no representation or warranties whatsoever as to, the data and information contained therein. Such address or

hyperlink (including addresses or hyperlinks to website material of Bulltick Brasil Consultoria e Assessoria Empresarial

Ltda or any of its affiliates) is provided solely for your convenience and information and the content of the linked site

does not in any way form part of this document. Accessing such website or following such link through the Report or

the website of Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates shall be at your own risk

and Bulltick Brasil Consultoria e Assessoria Empresarial Ltda or any of its affiliates shall have no liability arising out of,

or in connection with, and such referenced website.

18