Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Key terms finance

Semelhante a Key terms finance (20)

Mais de Georg Coakley

Mais de Georg Coakley (20)

Último

Último (20)

Key terms finance

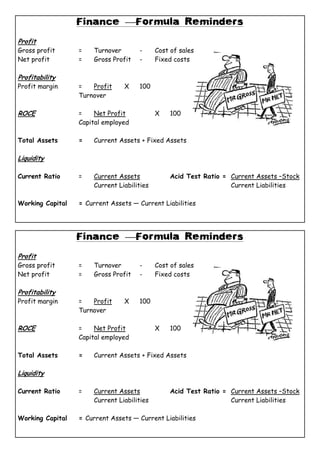

- 1. Finance —Formula Reminders Profit Gross profit = Turnover - Cost of sales Net profit = Gross Profit - Fixed costs Profitability Profit margin = Profit X 100 Turnover ROCE = Net Profit X 100 Capital employed Total Assets = Current Assets + Fixed Assets Liquidity Current Ratio = Current Assets Acid Test Ratio = Current Assets –Stock Current Liabilities Current Liabilities Working Capital = Current Assets — Current Liabilities Finance —Formula Reminders Profit Gross profit = Turnover - Cost of sales Net profit = Gross Profit - Fixed costs Profitability Profit margin = Profit X 100 Turnover ROCE = Net Profit X 100 Capital employed Total Assets = Current Assets + Fixed Assets Liquidity Current Ratio = Current Assets Acid Test Ratio = Current Assets –Stock Current Liabilities Current Liabilities Working Capital = Current Assets — Current Liabilities

- 2. Finance —Key Terms • Turnover – The Total value of money received from sales within a trading period. Also known as sales reve- nue • Cost of Sales – How much it costs the business to produce the goods they sell. Also known as costs of goods sold. • Costs – The amounts that a business has to pay in order to keep trading. Fixed & Variable Costs. • Current Assets – Something owned by a business that it does not expect to keep for more than 12 months and can be turned in to cash quickly. E.g stock, cash in the bank • Fixed Assets – Possessions which are owned by a business which are difficult to turn into cash. E.g build- ings • Total Assets — The total current and fixed assets. Everything a business owns or is owed. • Current Liabilities – A debt that a business has not yet paid, but expect to pay within the next 12 months • Capital Employed – A measure of a business’ assets which it can use to help it raise revenues. = Total As- sets – Current Liabilities • Working Capital – This is the day-to-day finance required for running a business. = Current Assets – Cur- rent Liabilities. • Gross Profit – What is left after the cost of sales has been subtracted from turnover. Overheads, inter- est and tax have not been taken into account. • Net profit – The profit made by a business AFTER all the trading expenses have been paid. • Operating Profit – The profit made by a business in it’s ordinary trading activities. All the administrative and selling expenses are subtracted from the Gross Profit. • Current Ratio — This demonstrates how many assets there is to pay off liabilities. 1:1 is safe. • Return on Capital Employed — (ROCE) Measures if money invested into a business has been used effec- tively. A high % ROCE means that the money invested is being used effectively and profitably. Finance —Key Terms • Turnover – The Total value of money received from sales within a trading period. Also known as sales reve- nue • Cost of Sales – How much it costs the business to produce the goods they sell. Also known as costs of goods sold. • Costs – The amounts that a business has to pay in order to keep trading. Fixed & Variable Costs. • Current Assets – Something owned by a business that it does not expect to keep for more than 12 months and can be turned in to cash quickly. E.g stock, cash in the bank • Fixed Assets – Possessions which are owned by a business which are difficult to turn into cash. E.g build- ings • Total Assets — The total current and fixed assets. Everything a business owns or is owed. • Current Liabilities – A debt that a business has not yet paid, but expect to pay within the next 12 months • Capital Employed – A measure of a business’ assets which it can use to help it raise revenues. = Total As- sets – Current Liabilities • Working Capital – This is the day-to-day finance required for running a business. = Current Assets – Cur- rent Liabilities. • Gross Profit – What is left after the cost of sales has been subtracted from turnover. Overheads, inter- est and tax have not been taken into account. • Net profit – The profit made by a business AFTER all the trading expenses have been paid. • Operating Profit – The profit made by a business in it’s ordinary trading activities. All the administrative and selling expenses are subtracted from the Gross Profit. • Current Ratio — This demonstrates how many assets there is to pay off liabilities. 1:1 is safe. • Return on Capital Employed — (ROCE) Measures if money invested into a business has been used effec- tively. A high % ROCE means that the money invested is being used effectively and profitably.