Fixed Income Update (September 2021) | ICICI Prudential Mutual Fund

•

0 gostou•156 visualizações

As highlighted in our earlier communication, we continue to believe in the gradual withdrawal of monetary stimulus and recommend following Accrual Strategy and Active Duration strategy.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Fixed Income Update (September 2021) | ICICI Prudential Mutual Fund

Semelhante a Fixed Income Update (September 2021) | ICICI Prudential Mutual Fund (20)

Mais de iciciprumf

Mais de iciciprumf (20)

Último

Último (20)

Fixed Income Update (September 2021) | ICICI Prudential Mutual Fund

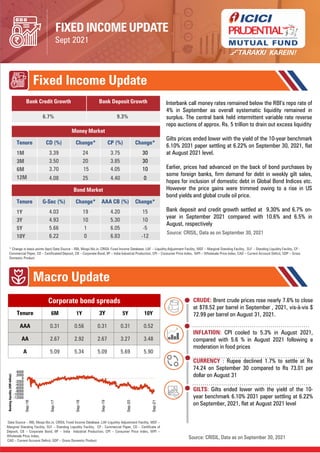

- 1. FIXED INCOME UPDATE Sept 2021 Fixed Income Update Macro Update * Change in basis points (bps) Data Source – RBI, Mospi.Nic.in, CRISIL Fixed Income Database, LAF – Liquidity Adjustment Facility, MSF – Marginal Standing Facility, SLF – Standing Liquidity Facility, CP - Commercial Paper, CD – Certificateof Deposit, CB – Corporate Bond, IIP – India Industrial Production, CPI – Consumer Price Index, WPI – Wholesale Price Index, CAD – Current Account Deficit, GDP – Gross Domestic Product Interbank call money rates remained below the RBI’s repo rate of 4% in September as overall systematic liquidity remained in surplus. The central bank held intermittent variable rate reverse repo auctions of approx. Rs. 5 trillion to drain out excess liquidity Gilts prices ended lower with the yield of the 10-year benchmark 6.10% 2031 paper settling at 6.22% on September 30, 2021, flat at August 2021 level. Earlier, prices had advanced on the back of bond purchases by some foreign banks, firm demand for debt in weekly gilt sales, hopes for inclusion of domestic debt in Global Bond Indices etc. However the price gains were trimmed owing to a rise in US bond yields and global crude oil price. Bank deposit and credit growth settled at 9.30% and 6.7% on- year in September 2021 compared with 10.6% and 6.5% in August, respectively Source: CRISIL, Data as on September 30, 2021 Bank Credit Growth Bank Deposit Growth 6.7% 9.3% Money Market Tenure CD (%) Change* CP (%) Change* 1M 3.39 24 3.75 30 3M 3.50 20 3.85 30 6M 3.70 15 4.05 10 12M 4.08 25 4.40 0 Bond Market Tenure G-Sec (%) Change* AAA CB (%) Change* 1Y 4.03 19 4.20 15 3Y 4.93 10 5.30 10 5Y 5.66 1 6.05 -5 10Y 6.22 0 6.83 -12 Data Source – RBI, Mospi.Nic.in, CRISIL Fixed Income Database ;LAF-Liquidity Adjustment Facility, MSF – Marginal Standing Facility, SLF – Standing Liquidity Facility, CP - Commercial Paper, CD – Certificate of Deposit, CB – Corporate Bond, IIP – India Industrial Production, CPI – Consumer Price Index, WPI – Wholesale Price Index, CAD – Current Account Deficit, GDP – Gross Domestic Product Source: CRISIL, Data as on September 30, 2021 CRUDE: Brent crude prices rose nearly 7.6% to close at $78.52 per barrel in September , 2021, vis-à-vis $ 72.99 per barrel on August 31, 2021. INFLATION: CPI cooled to 5.3% in August 2021, compared with 5.6 % in August 2021 following a moderation in food prices CURRENCY : Rupee declined 1.7% to settle at Rs 74.24 on September 30 compared to Rs 73.01 per dollar on August 31 GILTS: Gilts ended lower with the yield of the 10- year benchmark 6.10% 2031 paper settling at 6.22% on September, 2021, flat at August 2021 level Tenure 6M 1Y 3Y 5Y 10Y AAA 0.31 0.56 0.31 0.31 0.52 AA 2.67 2.92 2.67 3.27 3.48 A 5.09 5.34 5.09 5.69 5.90 Corporate bond spreads -12000 -10000 -8000 -6000 -4000 -2000 0 2000 4000 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21 Banking liquidity (INR billion)

- 2. Our Outlook Gilt prices ended flat, with the yield on the 10-year benchmark 6.10% 2031 paper remaining at 6.22% on September 30 (Source: CRISIL) As highlighted in our earlier communication, we continue to believe in the gradual withdrawal of monetary stimulus. The case for normalization of monetary conditions is starting to pick-up pace with number of COVID cases coming down, aggressive vaccine roll-out, economic activity leading to growth picking up, US Fed hinting for a taper soon, higher commodity prices etc. We believe, as the RBI gains comfort with growth picking-up, the possible glide-path for normalization of monetary conditions is expected to start with reduction in liquidity injection, post that measures to sterilize liquidity, following up with narrowing of the LAF corridor and after that change in stance. While RBI would continue to maintain adequate systemic liquidity, it has provided signals which points towards its intent to manage short-term liquidity more actively. For example, with the 7-day VRRR auction cut-off coming at 3.99% conducted on Sep 28, 2021, the market has already started raising questions, whether this is a signal that RBI has started giving shape to the policy normalization approach. To further bolster such steps, RBI may resort to slightly longer tenor VRRR and tapering of GSAP quantum. (Source: Deutsche Bank Research) Also, for the first time after many months, there has been a break in the unanimous decision of policy stance and the growing dissent among the MPC members point towards future policy decisions which would be characterized by giving due importance to inflation dynamics. Going forward, RBI may have to do a fine balancing act. On one hand, upside risk to COVID cases due to upcoming festive season, which may hamper growth recovery, which in normal conditions would have warranted for easing of monetary condition and on the other hand RBI would need to keep an eye on upside risk to inflation and global central banks initiating tapering. Hence, we believe the above evolving conditions points towards a more nimble and active duration management strategy, which may help in navigating higher interest rate sensitive period. Also, as communicated earlier, we believe that we are at the start of interest-rate rise cycle and the above mentioned strategy would provide better accrual (active strategy which may take advantage of higher term premium) and would help in mitigating mark-to-market impact (active strategy of having adequate short duration instruments). It may be an opportune time to invest in floating rate bond in this interest rate scenario with expected volatility. In the coming years, we recommend following strategies: Accrual Strategy and Active Duration strategy. Accrual strategy due to high spread premium which is still prevalent between the spread assets and AAA & MMI instruments, as going forward capital appreciation strategy may take a back seat due to limited rate cuts. Term premiums (spread between longer and shorter end of the yield curve) remains one of the highest seen historically, because of which active duration strategy is recommended to benefit from the high term premium. In our portfolios, we may follow barbell strategy i.e having high exposure to extreme short-end instruments with an aim to protect the portfolio from interest rate movements and high exposure to long-end instruments with an aim to benefit from higher carry OMO – Open Market Operations, MMI – Money Market instruments, VRRR – Variable Reverse Repo Rate, GSAP – G-sec acquisition programme, LAF – Liquidity Adjustment Facility Debt Valuation Index for Duration Risk Management Low Duration Data as on September 30, 2021. Debt Valuation Index considers WPI, CPI, Sensex returns, Gold returns and Real estate returns over G-Sec yield, Current Account Balance and Crude Oil Movement for calculation. Aggressive Highly Aggressive Very Cautious Cautious Moderate Aggressive Highly Aggressive Aggressive Highly Aggressive Moderate Cautious Very Cautious 1.78 0 1 2 3 4 5 6 7 8 9 10 Highly Aggressive Aggressive Moderate Cautious Very Cautious

- 3. Approach Scheme Name Call to Action Rationale Arbitrage ICICI Prudential Equity Arbitrage Fund Invest with 3 Months & above horizon Spreads at reasonable levels Measured Equity ICICI Prudential Equity Savings Fund Invest with 6 Months & above horizon Potential for upside and limiting downside Short Duration ICICI Prudential Savings Fund ICICI Prudential Ultra Short TermFund ICICI Prudential Floating InterestFund Invest for parking surplus funds Accrual + Moderate Volatility Accrual Schemes ICICI Prudential Credit Risk Fund ICICI Prudential Medium Term Bond Fund Core Portfolio with >1 Yr investment horizon Better Accrual DynamicDuration ICICI Prudential All Seasons BondFund Long Term Approach with >3 Yrs investment horizon Active Duration and Better Accrual Our Recommendation Riskometers ICICI Prudential Ultra Short Term Fund is suitable for investors who are seeking*:(An open ended ultra-short term debt scheme investing in instruments such that the Macaulay duration of the portfolio is between 3 months and 6 months) Moderate LOW HIGH Investors understand that their principal will be at Moderate risk • Short term regular income • An open ended ultra-short term debt scheme investing in a range of debt and money market instruments *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. ICICI Prudential Savings Fund is suitable for investors who are seeking*:(An open ended low duration debt scheme investing in instruments such that the Macaulay duration of the portfolio is between 6 months and 12 months.) Moderate • Short term savings • An open ended low duration debt scheme that aims to maximize income by investing in debt and money market instruments while maintaining optimum balance of yield,safety and liquidity LOW HIGH *Investorsshould consulttheirfinancial advisorsif indoubtaboutwhether theproduct issuitableforthem. None of the aforesaid recommendations are based on any assumptions. These are purely for reference and the investors are requested to consult their financial advisors before investing. Note: The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price. Please note that the Risk-o-meters specified above will be evaluated and updated on a monthly basis. Above riskometers are as on August 31, 2021.

- 4. Riskometers ICICI Prudential Medium Term Bond Fund is suitable for investors who are seeking*:(An open ended medium term debt scheme investing in instruments such that the Macaulay duration of the portfolio is between 3 Years and 4 Years. The Macaulay duration of the portfolio is 1 Year to 4 years under anticipated adverse situation) Moderate LOW HIGH Investors understand that their principal will be at Moderate risk • Medium term savings • A debt scheme that invests in debt and money market instruments with a view to maximize income while maintaining optimum balance of yield, safety and liquidity *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. ICICI Prudential All Seasons Bond Fund is suitable for investors who are seeking*:(An open ended dynamic debt scheme investing across duration) Moderate LOW HIGH Investors understand that their principal will be at Moderate risk • All duration savings • A debt scheme that invests in debt and money market instruments with a view to maximize income while maintaining optimum balance of yield, safety and liquidity *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. ICICI Prudential Credit Risk Fund is suitable for investors who are seeking*: (An open ended debt scheme predominantly investing in AA and below rated corporate bonds) Moderate LOW HIGH Investors understand that their principal will be at Moderate risk • Medium term savings • A debt scheme that aims to generate income through investing predominantly in AA and below rated corporate bonds while maintaining the optimum balance of yield, safetyand liquidity *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. ICICI Prudential Floating Interest Fund is suitable for investors who are seeking*:(An open ended debt scheme predominantly investing in floating rate instruments (including fixed rate instruments converted to floating rate exposures using swaps/derivatives) Moderate LOW HIGH Investors understand that their principal will be at Moderate risk • Short term savings • An open ended debt scheme predominantly investing in floating rate instruments *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. Please note that the Risk-o-meters specified above will be evaluated and updated on a monthly basis. Above riskometers are as on August 31, 2021. ICICI Prudential Equity Arbitrage Fund (Anopen ended scheme investing in arbitrage opportunities) is suitable for investors who are seeking* Moderate LOW HIGH • Short Term Income Generation • A hybrid scheme that aims to generate low volatility returns by using arbitrage and other derivative strategies in equity markets and investments in debt and money market instruments *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem. Investors should understand that their principal will be at low risk ICICI Prudential Equity Savings Fund (Anopen ended scheme investing inequity, arbitrage and debt) is suitable for investors who are seeking* Moderate LOW HIGH • Long term wealth creation • An open ended scheme that seeks to generate regular income through investments in fixed income securities, arbitrage and other derivative strategies and aim for long term capital appreciation by investing in equity and equity related instruments. *Investorsshouldconsulttheir financial advisorsif indoubt about whether theproduct issuitableforthem.

- 5. Benchmark Riskometer Sr No Scheme Name Benchmark Name Benchmark Riskometer 1 ICICI Prudential Equity Arbitrage Fund Nifty 50 Arbitrage Index 2 ICICI Prudential Savings Fund Nifty Low Duration Debt Index 3 ICICI Prudential Medium Term Bond Fund CRISIL Medium Term Debt Index 4 ICICI Prudential All Seasons Fund Nifty Composite Debt Index 5 ICICI Prudential Floating Interest Fund CRISIL Low Duration Debt Index 6 ICICI Prudential Equity Savings Fund Nifty Equity Savings TRI 7 ICICI Prudential Ultra Short Term Fund Nifty Ultra Short Duration Debt Index 8 ICICI Prudential Credit Risk Fund CRISIL Short Term Credit Risk Index Please note that the Risk-o-meters specified above will be evaluated and updated on a monthly basis. Above riskometers are as on August 31, 2021.

- 6. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. In preparation of the material contained in this document, ICICI Prudential Asset Management Company Limited (the AMC) has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the AMC and/or its affiliates and which may have been made available to the AMC and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The AMC, however, does not warrant the accuracy, reasonableness and / or completeness of any information. We have included statements / opinions / recommendations in this document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc. The AMC (including its affiliates), the Mutual Fund, the trust and any of its officers, directors, personnel and employees, shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/are liable for any decision taken on this material. All figures and other data given in this document are dated and the same may or may not be relevant in future. The information contained herein should not be construed as a forecast or promise nor should it be considered as an investment advice. Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the units of ICICI Prudential Mutual Fund. The sector(s)/stock(s) mentioned in this communication do not constitute any recommenda- tion of the same and ICICI Prudential Mutual Fund may or may not have any future position in these sector(s)/stock(s). Past performance may or may not be sustained in the future. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information document of the scheme. Please refer to the SID for more details. The information contained herein is only for the purpose of information and not for distribution and do not constitute an offer to buy or sell or solicitation of any offer to buy or sell any securities or financial instruments in the United States of America ("US") and/or Canada or for the benefit of US persons (being persons falling within the definition of the term "US Person" under the US Securities Act, 1933, as amended) or persons residing in Canada. Disclaimer