Houston Retail Market Vacancy Rate Drops Below 7.0

•

1 gostou•192 visualizações

Houston's retail market saw positive net absorption of 560,000 square feet in Q2 2013, bringing the year-to-date total to 960,000 square feet absorbed. The citywide vacancy rate decreased from 7.0% to 6.8% between quarters. Notable tenants that opened new locations or expanded in Q2 include HEB, LA Fitness, Michael's, and Monkey Joe's. The average quoted rental rate increased slightly to $14.75 per square foot between quarters. With continued job and economic growth, Houston's retail market is expected to remain healthy.

Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Semelhante a Houston Retail Market Vacancy Rate Drops Below 7.0

Semelhante a Houston Retail Market Vacancy Rate Drops Below 7.0 (20)

Mais de Colliers International | Houston

Mais de Colliers International | Houston (20)

Último

Último (20)

Houston Retail Market Vacancy Rate Drops Below 7.0

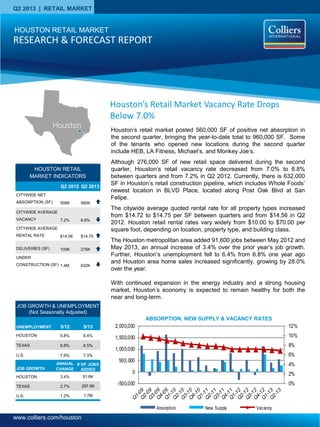

- 1. www.colliers.com/houston Q2 2013 | RETAIL MARKET HOUSTON RETAIL MARKET INDICATORS Q2 2012 Q2 2013 CITYWIDE NET ABSORPTION (SF) 508K 560K CITYWIDE AVERAGE VACANCY 7.2% 6.8% CITYWIDE AVERAGE RENTAL RATE $14.56 $14.75 DELIVERIES (SF) 105K 276K UNDER CONSTRUCTION (SF) 1.4M 632K Houston’s retail market posted 560,000 SF of positive net absorption in the second quarter, bringing the year-to-date total to 960,000 SF. Some of the tenants who opened new locations during the second quarter include HEB, LA Fitness, Michael’s, and Monkey Joe’s. Although 276,000 SF of new retail space delivered during the second quarter, Houston’s retail vacancy rate decreased from 7.0% to 6.8% between quarters and from 7.2% in Q2 2012. Currently, there is 632,000 SF in Houston’s retail construction pipeline, which includes Whole Foods’ newest location in BLVD Place, located along Post Oak Blvd at San Felipe. The citywide average quoted rental rate for all property types increased from $14.72 to $14.75 per SF between quarters and from $14.56 in Q2 2012. Houston retail rental rates vary widely from $10.00 to $70.00 per square foot, depending on location, property type, and building class. The Houston metropolitan area added 91,600 jobs between May 2012 and May 2013, an annual increase of 3.4% over the prior year’s job growth. Further, Houston’s unemployment fell to 6.4% from 6.8% one year ago and Houston area home sales increased significantly, growing by 28.0% over the year. With continued expansion in the energy industry and a strong housing market, Houston’s economy is expected to remain healthy for both the near and long-term. ABSORPTION, NEW SUPPLY & VACANCY RATES 0% 2% 4% 6% 8% 10% 12% -500,000 0 500,000 1,000,000 1,500,000 2,000,000 Absorption New Supply Vacancy Houston’s Retail Market Vacancy Rate Drops Below 7.0% UNEMPLOYMENT 5/12 5/13 HOUSTON 6.8% 6.4% TEXAS 6.8% 6.5% U.S. 7.9% 7.3% JOB GROWTH ANNUAL CHANGE # OF JOBS ADDED HOUSTON 3.4% 91.6K TEXAS 2.7% 297.9K U.S. 1.2% 1.7M JOB GROWTH & UNEMPLOYMENT (Not Seasonally Adjusted) HOUSTON RETAIL MARKET RESEARCH & FORECAST REPORT Houston

- 2. RESEARCH & FORECAST REPORT | Q2 2013 | HOUSTON RETAIL MARKET SALES ACTIVITY Houston retail investment sales activity increased between quarters with 205 sales transactions recorded in the second quarter compared to 180 in the first quarter. Total sales transaction volume totaled $1.1B and the average price per SF was $180. The average cap rate was 8.0%. Several of the more significant transactions that closed during the second quarter include: World Class Capital Group purchased the 10-building, 450,000- SF North Oaks Shopping Center from AEW Capital Management in June for $46.2M. The retail power center, located in the Northwest submarket, was 92% leased at the time of sale and was purchased as an investment. TJ Maxx, Ross Dress for Less, Hobby Lobby, Big Lots, and Staples are tenants in the center. Capcor Partners LLC purchased the 3-building, 102,837-SF Sheldon Forest Shopping Center from Weingarten Realty Investors in June for $8.5M. The neighborhood shopping center, located in the East submarket, was 98% leased at the time of sale. The center is anchored by Gerland’s Food Fair and other tenants include Burkes Outlet, A Sound Discount Warehouse, Family Dollar, and Boost Mobile. BNL Group Properties, Inc. purchased the 20,580-SF Shops at Fairfield from Satya, Inc. in April for $5.8M. The center is located along the perimeter of the Houston Premium Outlet Mall, located in the Northwest submarket. The strip center was 94% leased at the time of sale. Tenants include Verizon Wireless, Paris Salon, All Floors & More, Tomiko Restaurant, and Sergio’s Mexican Grill. LEASING ACTIVITY Houston retail leasing activity in the second quarter reached 939,600 SF, bringing the year-to-date total to 2M SF. Overall, transactions under 10,000 SF comprised the largest group of retail leases, with the market recording seventeen leases over 10,000 SF and only five over 20,000 SF in the second quarter. A partial list of the leases signed during the second quarter are listed in the table below. RETAIL SALE TRANSACTIONS North Oaks Shopping Center FM 1960 and Veterans Memorial Dr. Northwest Ret Submarket RBA: 450,000 SF Built: 1978/2004 Buyer: World Class Capital Group Seller: AEW Capital Management Sale Date: June 12, 2013 Sales Price: $46.2M Sales Price PSF: $103 COLLIERS INTERNATIONAL | P. 2 Shops at Fairfield 29110 Highway 290, Cypress, TX Northwest Ret Submarket RBA: 20,580 SF Built: 2010 Buyer: BNL Group Properties, Inc. Seller: Satya, Inc. Sale Date: April 10, 2013 Sales Price: $5.8M Sales Price PSF: $282 1 Renewal 2 Expansion 3 Sublease Building Name/Address Submarket SF Tenant Lease Date Northchase Plaza North 23,946 Goodwill1,2 May-13 Eastwood Shopping Center Liberty Co 23,806 Tractor Supply Jun-13 Copperfield Crossing Northwest 21,130 Monkey Joe's Apr-13 Kingwood Commons North 10,846 PETCO May-13 Alvin Towne Plaza Southeast Outlier 9,700 NAPA Auto Parts Apr-13 Country Club Plaza Southeast 8,100 Chinese Buffet3 Apr-13 West Pearland Plaza Far South 7,390 CrossFit Propel Jun-13 Sagemont Center Southeast 5,140 Gulf Coast Community Health Services1 May-13 Vintage Park Northwest 4,925 Mo's Irish Grill Apr-13 Champions Village Northwest 4,888 Don Ramon's Mexican Restaurant Apr-13 3939 Montrose Blvd Inner Loop 4,136 Canopy Restaurant May-13 Q2 2013 Retail Leases

- 3. RESEARCH & FORECAST REPORT | Q2 2013 | HOUSTON RETAIL MARKET RENTAL RATES The citywide average quoted rental rate increased to $14.75 from $14.72 per SF NNN between quarters and increased from $14.56 per SF NNN in Q2 2012. Class A in-line retail rental rates vary widely due to location and center type. Recent quoted rates for neighborhood centers, power centers and unanchored strip centers, range from $20.00 - $35.00 per SF (Class B and below can rent for $12.00 to $20.00 per SF) while theme/entertainment centers range from $25.00 - $35.00 per SF. Lifestyle centers and newly constructed strip centers in Class A locations such as High Street, Uptown Park and The Vintage range from $40.00 - $70.00 per SF. VACANCY & AVAILABILITY Houston’s retail vacancy decreased from 7.0% to 6.8% in the second quarter. By product type on a quarterly basis, lifestyle centers, theme/entertainment centers, and single tenant properties all posted a decrease in vacancy rate of 30 basis points followed by strip centers, power centers, and malls decreasing vacancy by 20 basis points. Outlet center vacancy rates saw the largest increase between quarters, 40 basis points. Houston’s retail construction pipeline contains 632,000 SF and second quarter deliveries totaled 276,000 SF. ABSORPTION & DEMAND Houston’s retail market posted 560,000 SF of positive net absorption in the second quarter, bringing the year-to-date positive net absorption to 960,000 SF. The opening of the new HEB Market in Conroe and LA Fitness in the Northwest submarket, contributed over 163,000 SF to the second quarter’s positive net absorption. Other notable tenants that moved into their space during the first quarter include: Kelsey-Seybold Clinic, Main Event, Michaels, Monkey Joe’s, and PETCO as seen in the table to the right. HOUSTON RETAIL MARKET STATISTICAL SUMMARY Q2 2013 ABSORPTION Tenant/ Submarket SF Occupied HEB Montgomery Co Ret 83,889 LA Fitness Near Northwest Ret 80,000 Kelsey-Seybold Clinic Southwest Ret 72,000 Main Event Southwest Ret 57,063 Michaels West Ret 23,000 Monkey Joe’s Northwest 21,130 PETCO North Ret 10,846 Chinese Buffet Southeast Ret 8,100 Don Ramon’s Northwest Ret 4,888 COLLIERS INTERNATIONAL | P. 3 Rentable Area Direct Vacant SF Direct Vacancy Rate Sublet Vacant SF Sublet Vacancy Rate Total Vacant SF Total Vacancy Rate Q2 2013 Net Absorption YTD 2013 Net Absorption Class A Rental Rates (in-line)* Strip Centers (unanchored) 32,048,543 3,252,065 10.1% 18,803 0.1% 3,270,868 10.2% 90,769 108,682 $20.00-$35.00 Neighborhood Centers (one anchor) 68,674,242 7,078,334 10.3% 151,134 0.2% 7,229,468 10.5% 83,836 307,799 $20.00-$35.00 Community Centers (two anchors) 41,618,907 2,541,191 6.1% 112,696 0.3% 2,653,887 6.4% 1,577 113,083 $18.00-$30.00 Power Centers (3 or more anchors) 19,715,839 1,031,423 5.2% 43,624 0.2% 1,075,047 5.5% 44,390 47,047 $20.00-$35.00 Lifestyle Centers 4,180,721 255,393 6.1% - 0.0% 255,393 6.1% 12,459 3,560 $40.00-$70.00 Outlet Centers 1,593,814 132,724 8.3% - 0.0% 132,724 8.3% (7,418) (6,418) N/A Theme/Entertainment 676,840 228,813 33.8% - 0.0% 228,813 33.8% - - $25.00-$35.00 Single-Tenant 64,422,260 1,331,106 2.1% 21,816 0.0% 1,352,922 2.1% 253,292 292,816 N/A Malls 30,199,471 1,675,871 5.5% 58,539 0.2% 1,734,410 5.7% 80,979 93,080 N/A Greater Houston 263,130,637 17,526,920 6.7% 406,612 0.2% 17,933,532 6.8% 559,884 959,649

- 4. RESEARCH & FORECAST REPORT | Q2 2013 | HOUSTON RETAIL MARKET Accelerating success. COLLIERS INTERNATIONAL 1223 W. Loop South Suite 900 Houston, Texas 77027 Main +1 713 222 2111 LISA R. BRIDGES Director of Market Research | Houston Direct +1 713 830 2125 Fax +1 713 830 2118 lisa.bridges@colliers.com The Colliers Advantage Enterprising Culture Colliers International is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. When you choose to work with Colliers, you choose to work with the best. In addition to being highly skilled experts in their field, our people are passionate about what they do. And they know we are invested in their success just as much as we are in our clients’ success. This is evident throughout our platform—from Colliers University, our proprietary education and professional development platform, to our client engagement strategy that encourages cross-functional service integration, to our culture of caring. We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry. That’s why we attract top recruits and have one of the highest retention rates in the industry. Colliers International has also been recognized as one of the “best places to work” by top business organizations in many of our markets across the globe. Colliers International offers a comprehensive portfolio of real estate services to occupiers, owners and investors on a local, regional, national and international basis. COLLIERS INTERNATIONAL | P. 4