1. Lesson 16 Crisis Related Liquidity Provisions

The History of a Powerful Paragraph

http://www.minneapolisfed.org/publications_papers/pub_display.cfm

Federal Reserve Liquidity Provision During the Financial Crisis

of 2007-2009, Michael Fleming, FRBNY Staff Reports # 563,

July 2012.

http://www.newyorkfed.org/research/staff_reports/sr563.html

Interest on Reserves and Monetary Policy, Marvin Goodfriend ,

FRBNY Economic Policy Review 2002

http://www.newyorkfed.org/research/epr/02v08n1/0205good.pdf

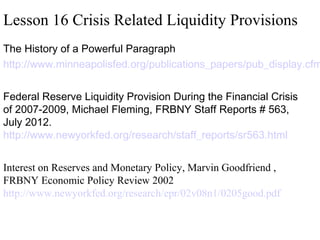

2. When Banks Borrow From The Discount Window

Bank Reserves Increase

Federal Reserve

assets

+Discount Loans

Banking System

liabiliies

+Reserves

assets

+Reserves

liabiliies

+Due to Fed

3. Eligible Collateral for Discount Window Advances

Marg ins for S ec urities

(as percentage of

C ollateral C ateg ory

2

U.S . Treas uries & F ully G uaranteed A gencies

B ill/Notes /B onds /Inflation Indexed

Zero C oupon, S TR IP s

B ills /Notes /B onds - U.S . D ollar D enominated

Zero C oupon - U.S . D ollar D enominated

G overnment S pons ored E nterpris es

B ills /Notes /B onds

C orporate B onds

A A A rated - U.S . D ollar D enominated

B B B -A A rated - U.S . D ollar D enominated

Municipal B onds

U.S . D ollar D enominated

A s s et B acked S ecurities

A A A rated

B B B -A A rated

C ollateralized D ebt Obligations - A A A rated

C ommercial Mortgage B acked S ecurities - A A A rated

A gency B acked Mortgages

P as s Throughs

C MO s

C ommercial L oans & L eas es

Minimal R is k R ated

7

8

Normal R is k R ated

C ommercial R eal E s tate L oans

Minimal R is k R ated

7

8

Normal R is k R ated

C ons umer L oans - Uns ecured

C ons umer L oans & L eas es (auto, boat, etc.)

C ons umer L oans - C redit C ard R eceivables

C ons umer L oans - S ubprime C redit C ard R eceivables

S tudent L oans

3

es timated fair market value)

D uration B uc kets

0-5

>5-10

>10

99%

98%

98%

97%

97%

96%

96%

95%

96%

95%

93%

96%

95%

86%

91%

93%

96%

96%

L oans

83%

82%

90%

92%

98%

98%

G roup D epos ited

95%

98%

89%

92%

97%

4, 5

94%

92%

98%

L oans

95%

97%

95%

Indiv idually D epos ited

96%

92%

95%

91%

98%

Marg ins for L oans

(as percentage of es timated fair market value)

95%

90%

87% to 96%

87%

63% to 95%

63%

78% to 96%

78%

57% to 95%

60% to 96%

76% to 96%

57%

60%

76%

59%

54%

83%

4

5. Prior to 2003

• Discount Rate was set below Fed Funds rate

• The Discount rate served as anchor on the Funds rate

• Banks were forced to borrowed from the discount window,

because the provision of nonborrowed reserves was below

the demand for combined demand for required and excess

reserves

• There were implicit costs of borrowing from the Fed, and

banks were generally reluctant to do so, unless the Fed

funds rate was elevated relative to the discount rate

• The larger the volume of forced discount window

borrowing the great the spread between the discount rate

and the Funds rate

7. Discount Rate Policy Prior to 2003

• During times of financial market stress, such as the

failure of Continental Illinois in 1984 the implicit costs

of borrowing from the Fed became more pronounced.

• The higher the implicit costs the larger the spread

between the Funds rate and the discount rate for a given

level of borrowing.

• The FOMC would establish “Borrowing Objectives”,

instructing the Open Market Desk to provide

nonborrowed reserves in such volumes as to force a

particular volume of discount window borrowings

• In effect the FOMC was attempting to foster a

particular spread between the funds rate and the

discount rate

8. The higher the level of Net Borrowed Reserves

(borrowed reserves – excess reserves), the higher the

Funds Rate trades above the Discount Rate

9. Beginning January 2003 The Discount

rate became a penalty rate

• The discount rate was set initially 1 percent above

the prevailing Fed funds target

• By having a penalty rate the Fed attempted to

remove any implicit costs of borrowing.

• Banks were no longer discouraged from

borrowing at the discount window

• This new approach to discount window policy was

thought of as putting a ceiling on the Fed funds

rate

10. In 2003 the Fed change the way the discount window operates. Henceforth, the

discount rate was set as a spread above the FF target…On August 17, 2007 that

spread was reduced from 1% to only ½%, and on March 16, 2008 the spread was

reduced to only ¼%.

11. Cutting the discount rate usually doesn’t impact on

the funds rate, only if banks are already borrowing

heavily from the window

12. Onset of Current Crisis: Term Funding Rates (1-mo

Euro$) exceeded the discount rate early in the crisis

13. Crisis Related Adjustments to

Discount Window Policies

• The Fed’s first crisis related action was to reduce the spread

between the funds rate target and the discount rate from 1% to .

50%. This resulted in a drop in the discount rate from 6-1/4% to

5-3/4%.

• Later following the the unwinding of Bear Stearns in March 2008

the discount rate spread was reduced to only .25%.

• Initially the Fed also extended the term of borrowings from

overnight to up to 30-days, after Bear Stearns this was increased

to 90-days.

• The intent was to encourage borrowings so that stress in the interbank funding markets would ease

• Banks still would not go to window because of a perceived

stigma

14. Why a Stigma in borrowing at the

discount window?

• Banks were concerned that if it became known

that they were accessing the discount window they

would be perceived as suffering liquidity

problems

• Banks feared depositors might withdraw deposits

• Banks feared that other creditors, such as banks

lending Fed funds, would pull back credit

• Banks also feared that speculators would “short”

their stock, causing a rumor related plunge in their

stock price.

15. Why was the Fed concerned about the

lack of borrowing?

• The Fed was hoping that the stress in the term

interbank funding market would encourage

discount window advances, recall the purpose of

setting the discount rate above the funds rate was

to provide a ceiling on the funds rate, and related

interbank financing costs. If banks borrowed

from the window the stress in the markets would

be relieved.

16. What Did the Fed Do to Increase

Liquidity of Financial Institutions?

• Eased Terms at Discount Window – Lower

Discount/FFR Target Spread, Longer Borrowing Terms

• Term Auction Facility (TAF)—Instead of banks coming

to the window, the Fed auctioned credit. Banks bidding

successfully in the auction won credit at costs below

market term funding rates

• Fed opened the Primary Dealer Credit Facility (PDCF)

to ensure liquidity to dealers with appropriate collateral

• Fed activated Currency Swap Lines providing dollar

related credit to foreign central banks to enable a relending of these dollars to banks outside the US

18. Under Section 13(3) of the Federal Reserve Act the

Fed provided credit to systemically important

institutions such as AIG

19. The Various Liquidity Programs Enacted During the

2008/2009 Period Caused Bank Reserves to Rise

20. The Rise in Bank Reserves Associated with these

Liquidity Provisions would have resulted in a Fed

funds rate plunge to zero, if not for payment of

interest on reserves

21. By paying Interest on Reserves (IOR) the Fed could expand its

balance sheet without having the funds rate fall to zero. The thinking

was that IOR would put a floor on the funds rate, even when there

was an abundance of excess reserves in the banking system.

22. Fed Pays 0.25% Interest on Reserve Balances, lifts

floor on funds from zero to 0.25%

23. Why Does the Funds Rate Trade Below the Floor? Answer: Not all

deposits at Fed pay interest. GSEs don’t earn interest on deposits and

therefore have incentive to sell these deposits (reserves).

24. Fed will move towards managing the Fed funds rate within

a “corridor” sometime in the years ahead

The demand curve has a downward-sloping portion because banks want to

hold more reserves when the federal funds rate is lower

25. The Supply Curve for Bank Reserves: Discount Rate

serves as a theoretical ceiling on the funds rate

The supply of reserves is vertical when ffr is less than the

primary discount rate and horizontal when they are equal

26. The IOER serves as a theoretical floor on the funds rate

When ffr exceeds the Fed’s target, the Fed engages in purchases in the amount

of ∆R and equilibrium ffr will equal the target

27. Together the IOER and the Discount Rate define a

“corridor” for the Fed Funds Rate

When ffr exceeds the Fed’s target, the Fed engages in purchases in the amount

of ∆R and equilibrium ffr will equal the target

28. A Shift in the demand for reserves does not

cause the funds rate to trade above ceiling

If demand for reserves is D2 instead of D1, ffr will rise to equal the

discount rate

Notas do Editor

There was a stigma by the Fed. Instead of borrowers coming to the Fed to borrow, the fed instead went to them and said you can bid for the money. This way they didn’t have to bid in the Eurodollar market which cause the Libor rate to come down

Under this special section the Fed can lend money to people like us. Maiden Lane was the bad balance sheet that Bear Stearns collapsed under and the Fed used this section and lended money to this T account. Jp Morgan also lended money.

The supply curve before the liehmann brothers collapsed. Then the fed starts doing stuff and then shifted to S2 and the funds rate becomes 0. The fed didn’t really want to do this as to having the feds fund rate 0.

By giving interest on the reserves the feds funds rate increased as it can be seen by the black demand line. Also the amount of excess reserve you may want to hold will increase because the fed is now paying you interest for keeping a reserve.