Charts from CBO's Budget and Economic Outlook: An Update

•

7 gostaram•28,872 visualizações

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Charts from CBO's Budget and Economic Outlook: An Update

Semelhante a Charts from CBO's Budget and Economic Outlook: An Update (20)

Mais de Congressional Budget Office

Mais de Congressional Budget Office (20)

Último

Último (20)

Charts from CBO's Budget and Economic Outlook: An Update

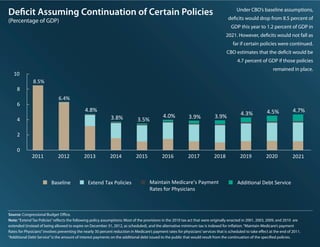

- 1. Deficit Assuming Continuation of Certain Policies Under CBO’s baseline assumptions, deficits would drop from 8.5 percent of (Percentage of GDP) GDP this year to 1.2 percent of GDP in 2021. However, deficits would not fall as far if certain policies were continued. CBO estimates that the deficit would be 4.7 percent of GDP if those policies remained in place. 10 8.5% 8 6.4% 6 4.8% 4.5% 4.7% 4.0% 3.9% 4.3% 4 3.8% 3.5% 3.9% 2 0 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Baseline Extend Tax Policies Maintain Medicare’s Payment Additional Debt Service Rates for Physicians Source: Congressional Budget Office. Note: “Extend Tax Policies” reflects the following policy assumptions: Most of the provisions in the 2010 tax act that were originally enacted in 2001, 2003, 2009, and 2010 are extended (instead of being allowed to expire on December 31, 2012, as scheduled), and the alternative minimum tax is indexed for inflation. “Maintain Medicare’s payment Rates for Physicians” involves preventing the nearly 30 percent reduction in Medicare’s payment rates for physicians’ services that is scheduled to take e ect at the end of 2011. “Additional Debt Service” is the amount of interest payments on the additional debt issued to the public that would result from the continuation of the specified policies.

- 2. Federal Debt Held by the Public With modest deficits projected for the latter part of the 2012–2021 period under CBO’s current-law baseline, debt held by (Percentage of GDP) the public recedes as a percentage of GDP. However, if certain provisions that are part of current law did not expire as scheduled, 120 debt held by the public would rise to 82 percent of GDP by the end of 2021, which would be the highest level since 1948. Actual Projected 100 Continuation of 80 Certain Policies 60 CBO’s Baseline 40 20 0 1940 1950 1960 1970 1980 1990 2000 2010 2020 Source: Congressional Budget Office. Note: The projected debt with the continuation of certain policies is based on several assumptions: rst, that most of the provisions of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 that originally were enacted in 2001, 2003, 2009, and 2010 do not expire on December 31, 2012, but instead continue; second, that the alternative minimum tax is indexed for inflation after 2011; and third, that Medicare’s payment rates for physicians are held constant at their 2011 level. Shaded bars indicate periods of recession.

- 3. Total Deficits or Surpluses If some of the changes specified in current law did not occur and certain (Percentage of GDP) current policies were continued instead, then annual deficits from 2012 through 2021 would be much higher—averaging 4.3 percent of GDP, compared with 1.8 percent in CBO’s baseline projections. 4 2.4% 2 2000 Actual Projected 0 CBO’s Baseline -2 -4 Continuation of -3.5% Certain Policies -4.2% 2004 1976 -4.7% -6 1992 -6.0% 1983 -8 -10 -10.0% 2009 -12 1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 Source: Congressional Budget Office. Note: The projected deficit with the continuation of certain policies is based on several assumptions: rst, that most of the provisions of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 that originally were enacted in 2001, 2003, 2009, and 2010 do not expire on December 31, 2012, but instead continue; second, that the alternative minimum tax is indexed for inflation after 2011; and third, that Medicare’s payment rates for physicians are held constant at their 2011 level.

- 4. Total Discretionary Budget If discretionary budget authority was allowed to grow at the rate of inflation, without the constraint on nonwar funding Authority Excluding War Funding imposed by the caps established in the Budget Control Act, (Percentage of GDP) that budget authority would be about 4 percent higher in 2012 and 8 percent higher in 2021. 12 Actual Projected 10 8 Funding for 2011 Adjusted for Inflationa 6 CBO’s Baselineb 4 2 0 1986 1991 1996 2001 2006 2011 2016 2021 Source: Congressional Budget Office. a Data reflect the assumption that discretionary funding related to federal personnel is inflated using the employment cost index for wages and salaries. All other discretionary funding is adjusted using the gross domestic product price index. b When constructing its baseline, CBO assumes that discretionary funding will adhere to the statutory caps recently enacted into law by the Budget Control Act of 2011.

- 5. Real Gross Domestic Product CBO expects that the economic recovery will (Trillions of 2005 dollars, logarithmic scale) continue but that real (inflation-adjusted) GDP will stay below the economy’s potential—a level that corresponds to a high rate of use of labor and capital—until 2017. 19 Actual Projected 18 17 Potential GDP 16 15 14 GDP 13 12 11 10 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2020 Sources: Congressional Budget Office; Department of Commerce, Bureau of Economic Analysis. Notes: Real gross domestic product is the output of the economy adjusted to remove the e ects of inflation. Potential GDP is CBO’s estimate of the output that the economy would produce with a high rate of use of its labor and capital resources. Data are quarterly. Actual data for GDP, which are plotted through the second quarter of 2011, incorporate the July 2011 revisions of the national income and product accounts. Projections of GDP, which are plotted through the fourth quarter of 2021, are based on data issued before the revisions. Shaded bars indicate periods of recession.

- 6. Ratio of GDP to Potential GDP CBO projects that GDP will grow considerably (Percent) faster than potential GDP between 2013 and 2016. That growth will bring the economy to a high rate of resource use—completely closing the gap between the economy’s actual and 4 potential output—by 2017. 2 Actual Projected 0 -2 -4 -6 -8 -10 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 Sources: Congressional Budget Office; Department of Commerce, Bureau of Economic Analysis. Notes: Real gross domestic product is the output of the economy adjusted to remove the e ects of inflation. Potential GDP is CBO’s estimate of the output that the economy would produce with a high rate of use of its labor and capital resources. Data are quarterly. Actual data for GDP, which are plotted through the second quarter of 2011, incorporate the July 2011 revisions of the national income and product accounts. Projections of GDP, which are plotted through the fourth quarter of 2021, are based on data issued before the revisions.

- 7. Unemployment Rate With the projection of modest growth in output, CBO expects (Percent) employment to expand slowly during the rest of this year and next year. The unemployment rate is projected to fall from an average of 9.1 percent in the second quarter of 2011 to 8.9 percent in the fourth quarter of 2011 and to 8.5 percent in the fourth quarter of 2012. 12 Actual Projected 10 8 6 4 2 0 1980 1985 1990 1995 2000 2005 2010 2015 2020 Sources: Congressional Budget Office; Department of Labor, Bureau of Labor Statistics. Notes: The unemployment rate is a measure of the number of jobless people who are available for work and are actively seeking jobs, expressed as a percentage of the labor force. Data are quarterly. Actual data are plotted through the second quarter of 2011; projections are plotted through the fourth quarter of 2021.

- 8. Interest Rates Consistent with its forecast of modest economic (Percent) growth through 2013 under current law, CBO projects that interest rates will remain very low for the next few years and then rise to more-normal levels as output approaches its potential in 2017. 16 Actual Projected 14 12 11.1% 10 8.6% 8 8.4% 6.0% 6 5.9% 5.3% 5.8% 10-Year Treasury Notes 4 5.8% 3.3% 3-Month Treasury Bills 4.0% 4.0% 3.0% 2 1.0% 0.1% 0 1983 1987 1993 2000 2003 2011 2017 Sources: Congressional Budget Office; Federal Reserve. Notes: Data are annual. Actual data are plotted through 2010; projections are plotted through 2021.

- 9. House Prices House prices are nearing the end of their decline, in (Index, 1991 = 100) CBO’s estimation. But they probably will not begin a sustained increase until the second half of 2012, when CBO expects there to be fewer foreclosures and distressed sales. CBO projects that by the end of 2013, house prices as measured by the S&P/Case-Shiller 300 index will be back to 2003 levels. 250 Actual Projected 200 150 100 50 0 1990 1995 2000 2005 2010 2015 2020 Sources: Congressional Budget Office; Standard & Poor’s (S&P) Financial Services. Notes: The S&P/Case-Shiller national home price index tracks the prices of home sales financed using mortgages purchased or securitized by Fannie Mae or Freddie Mac as well as sales financed with mortgages that do not conform to the size or credit criteria for purchase by Fannie Mae or Freddie Mac. Values shown are annual averages of quarterly data. Actual data are plotted through 2010; projections are plotted through 2021.

- 10. Vacant Housing Units The recovery of the housing market is likely to be slowed by the fact that an unusually large percentage of housing units are now vacant. That percentage, (Percentage of total units) which was already high before the 2007–2009 recession because of overbuilding during the housing boom, partly reflects the large number of foreclosures and continued slow pace of household formation since the end of the recession. 15 14.3% 14 13 12.7% 12 11.8% 11.6% 11.2% 11.2% 11.0% 11 10.4% 10.5% 10.0% 10 9 8 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 Sources: Congressional Budget Office; Department of Commerce, Census Bureau. Notes: Housing units comprise occupied units and vacant units, including units intended for year-round use and seasonal units. Values are annual averages of quarterly data.

- 11. Net Business Fixed Investment Investment by businesses declined sharply during the recession, and although it picked up a bit relative to GDP in (Percentage of GDP) 2010, it remained well below its long-run historical average. The growth in GDP that CBO has projected for the near term will encourage businesses to boost net fixed investment to 5 Actual meet increases in demand for their products. 4.6% 4.7% 4.4% 4.5% 4.1% 4 Projected 3.5% 3.4% 3.4% 3.0% 3.1% 3.1% 3 2.7% 2.3% 2.4% 2 1 1.0% 0 1980 1985 1955 1960 1965 1970 1975 1990 1995 2000 2005 2010 2015 2020 1950 Sources: Congressional Budget Office; Department of Commerce, Bureau of Economic Analysis. Notes: Business fixed investment consists of businesses’ spending on nonresidential structures, equipment, and software. It is shown here net of depreciation. Data are annual. Actual data incorporate the July 2011 revisions to the national income and product accounts; projections are based on data issued before the revisions.

- 12. Exchange Value of the U.S. Dollar The trade-weighted exchange value of the dollar declined for most of the past decade, as foreign (Index, March 1973 = 100) investors became less willing to keep adding to their increasingly large holdings of U.S. dollar assets. 130 CBO expects that decline to continue at a moderate pace, on average, over the next 10 years. 120 110 100 90 80 70 1980 1985 1990 1995 2000 2005 2010 Sources: Congressional Budget Office; Federal Reserve. Notes: This index is an average of the U.S. dollar’s exchange value against the currencies of a large group of major U.S. trading partners, adjusted for inflation and weighted by the amount of trade the United States conducts with each of those countries. The index weights change over time. Data are monthly and are plotted through July 2011. Tan lines represent a year’s worth of values; light blue bars represent the annual average.

- 13. Net Job Growth per Month Labor market conditions deteriorated (Thousands of jobs) dramatically during the recent recession, and despite a modest recovery in job growth beginning in early 2010, employment remains 400 well below its prerecession level. 200 0 -200 -400 -600 -800 -1,000 January July January July January July January July January July 2007 2007 2008 2008 2009 2009 2010 2010 2011 2011 Sources: Congressional Budget Office; Department of Labor, Bureau of Labor Statistics. Notes: Data are monthly and are plotted through July 2011. They exclude temporary jobs associated with the 2010 census.

- 14. Labor Force Participation Rate The labor force participation rate has fallen significantly in the past decade. Although economic (Percent) recovery will increase the demand for labor, CBO expects that rate to continue to decline as the aging of the baby boomers and tax increases scheduled under current law prompt more people to leave the labor force. 1970 60.4% 1980 63.8% 1990 66.5% 2000 67.1% 2010 64.7% 2020 63.0% 55% 60% 65% Sources: Congressional Budget Office; Department of Labor, Bureau of Labor Statistics. Notes: The labor force participation rate is the percentage of the civilian noninstitutionalized population age 16 or older that is either working or actively looking for work. Values are annual averages of quarterly data.

- 15. Unemployed Workers per Job Opening The number of unemployed workers per job opening averaged about 4½ in the first half of 2011—down (Number) from an average of more than 6 in 2009 but still much higher than before the recent recession. 8 7 6 5 4 3 2 1 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Sources: Congressional Budget Office; Department of Labor, Bureau of Labor Statistics. Notes: Data are monthly and are plotted through June 2011. Shaded bars indicate periods of recession.

- 16. Inflation Although inflation increased in the first half of 2011, CBO projects that it will recede somewhat (Percentage change in prices from previous year) in the second half and that prices will rise at a subdued pace over the next few years. 12 Actual Projected 10 8 6 Overall 4 Core 2 0 -2 1980 1985 1990 1995 2000 2005 2010 2015 2020 Sources: Congressional Budget Office; Department of Commerce, Bureau of Economic Analysis. Notes: The overall inflation rate is based on the price index for personal consumption expenditures; the core rate excludes prices for food and energy. Data are quarterly. Actual data, which are plotted through the second quarter of 2011, incorporate the July 2011 revisions of the national income and product accounts. Projections, which are plotted through the fourth quarter of 2021, are based on data issued before the revisions.

- 17. Crude Oil Prices A key reason for the increase in inflation earlier this year was a spike in the (Dollars per barrel) price of oil, which rose from an average of about $75 per barrel last summer to more than $110 in late April, partly because of political uncertainty and supply disruptions in the Middle East and North Africa. The benchmark price of crude oil fell back below $100 at the end of June and has declined further since then. 160 140 120 100 80 60 40 20 0 September September September September September September September August 2004 2005 2006 2007 2008 2009 2010 2011 Sources: Congressional Budget Office; Bloomberg. Notes: The price shown is the spot price of the West Texas Intermediate grade of crude oil delivered at Cushing, Oklahoma. Data are prices at the end of each week and are plotted through August 12, 2011.

- 18. Labor Income Labor income has fallen sharply as a share of gross domestic (Percentage of gross domestic income) income since 2009—well below its share during most of the past 30 years. In CBO’s projections, labor income grows faster than GDI over the next decade, bringing its share from about 60 percent of 65 GDI in early 2011 to about 61 percent by 2021. Actual Projected 64 63.2% 2001 Q1 63 62.9% 1992 Q3 62 61.3% 61 1984 Q4 60.6% 1997 Q3 60 60.0% 2006 Q3 59.4% 2010 Q1 59 1980 1985 1990 1995 2000 2005 2010 2015 2020 Sources: Congressional Budget Office; Department of Commerce, Bureau of Economic Analysis. Notes: Labor income is defined here as labor compensation plus 65 percent of proprietors’ income. Gross domestic income is the sum of all income earned in the production of gross domestic product. Data are quarterly. Actual data, which are plotted through the first quarter of 2011, incorporate the July 2011 revisions of the national income and product accounts. Projections, which are plotted through the fourth quarter of 2021, are based on data issued before the revisions.

- 19. Stock Prices Stock prices, as measured by the value of the (Index, 1941–1943 = 10) S&P 500 index, dropped by more than 15 percent between early July and mid-August 2011, returning to their level of late 2010. 1,600 1,400 1,200 1,000 800 600 400 200 0 January 2007 January 2008 January 2009 January 2010 January 2011 Sources: Congressional Budget Office; Bloomberg. Notes: The Standard & Poor’s (S&P) 500 index includes the prices of actively traded common stocks of 500 leading companies in key industries of the U.S. economy. Data are monthly; the value for August 2011 runs through August 19. The span of each line reflects the high and low index values for that month.