Room To Run, But Value Vanishes

Be realistic, be selective. We believe this market rally has pushed valuations to the point where growth expectations have reached implausible levels. In fact, profits have just begun to turn down. We are not overly bearish – our Buy list is longer than our Sell list – but we caution that optimism over growth can disappear as quickly as it appeared. Domestic factors, particularly political developments, may be a positive catalyst. Profit recession has just begun. Industrial production peaked in January 2008, but profits only began a broad-based decline in 1Q09. Within our coverage, 63% of the companies that have released 1Q earnings reported lower sequential quarterly net profits. In seven sectors, our entire coverage list suffered profit contractions. This suggests the recession in profits has just begun. Market valuation implies an optimistic view of growth. The market currently trades at 15.2x 2009 earnings, up from 12x earlier this year. This is only 10% below the previous cycle’s mid-cycle value, but today, we face growth of -7.7% (2009) and +9.7% (2010), taking market earnings only 1% higher by the end of 2010 from its end-2008 level. Market growth expectations seem to be running ahead of reality. History tells us the bear market isn’t over. Two previous bear markets over 1981-86 and 1993-98 lasted 57 and 58 months respectively. It has now been 17 months from the January 2008 collapse. Those bear markets had 22-38 trend reversals of 5% or more; we have now seen 12 since January 2008. These comparisons suggest we are, at best, half way through this bear market. Bet on Prime Minister Najib, but Sell hope. Our top stock picks are in the construction sector. We expect PM Najib will deliver on the fiscal spending promises, reinvigorating the construction and building materials sectors. Our top Sells are stocks where high hopes and expectations have been built in; where current prices have run well ahead of both our and consensus target prices. Politics a positive wildcard. Beyond rapidly executed fiscal packages, the country’s new leadership could make further changes to longstanding policies to attract foreign investment and win back broader support from all Malaysians. These initiatives should be positive for equity market at least in the short-term.

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (18)

Destaque

Semelhante a Room To Run, But Value Vanishes

Semelhante a Room To Run, But Value Vanishes (20)

Mais de Boyboy cute

Mais de Boyboy cute (20)

Último

Último (20)

Room To Run, But Value Vanishes

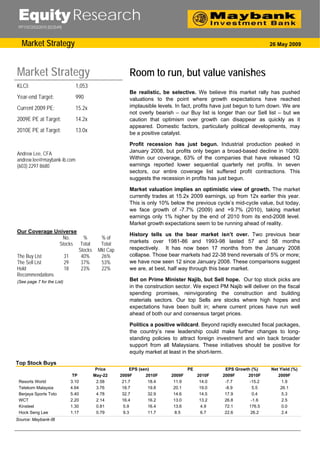

- 1. Equity Research PP11072/03/2010 (023549) Market Strategy 26 May 2009 Market Strategy Room to run, but value vanishes KLCI: 1,053 Be realistic, be selective. We believe this market rally has pushed Year-end Target: 990 valuations to the point where growth expectations have reached Current 2009 PE: 15.2x implausible levels. In fact, profits have just begun to turn down. We are not overly bearish – our Buy list is longer than our Sell list – but we 2009E PE at Target: 14.2x caution that optimism over growth can disappear as quickly as it appeared. Domestic factors, particularly political developments, may 2010E PE at Target: 13.0x be a positive catalyst. Profit recession has just begun. Industrial production peaked in Andrew Lee, CFA January 2008, but profits only began a broad-based decline in 1Q09. andrew.lee@maybank-ib.com Within our coverage, 63% of the companies that have released 1Q (603) 2297 8680 earnings reported lower sequential quarterly net profits. In seven sectors, our entire coverage list suffered profit contractions. This suggests the recession in profits has just begun. Market valuation implies an optimistic view of growth. The market currently trades at 15.2x 2009 earnings, up from 12x earlier this year. This is only 10% below the previous cycle’s mid-cycle value, but today, we face growth of -7.7% (2009) and +9.7% (2010), taking market earnings only 1% higher by the end of 2010 from its end-2008 level. Market growth expectations seem to be running ahead of reality. Our Coverage Universe History tells us the bear market isn’t over. Two previous bear No. % % of Stocks Total Total markets over 1981-86 and 1993-98 lasted 57 and 58 months Stocks Mkt Cap respectively. It has now been 17 months from the January 2008 The Buy List 31 40% 26% collapse. Those bear markets had 22-38 trend reversals of 5% or more; The Sell List 29 37% 53% we have now seen 12 since January 2008. These comparisons suggest Hold 18 23% 22% we are, at best, half way through this bear market. Recommendations (See page 7 for the List) Bet on Prime Minister Najib, but Sell hope. Our top stock picks are in the construction sector. We expect PM Najib will deliver on the fiscal spending promises, reinvigorating the construction and building materials sectors. Our top Sells are stocks where high hopes and expectations have been built in; where current prices have run well ahead of both our and consensus target prices. Politics a positive wildcard. Beyond rapidly executed fiscal packages, the country’s new leadership could make further changes to long- standing policies to attract foreign investment and win back broader support from all Malaysians. These initiatives should be positive for equity market at least in the short-term. Top Stock Buys Price EPS (sen) PE EPS Growth (%) Net Yield (%) TP May-22 2009F 2010F 2009F 2010F 2009F 2010F 2009F Resorts World 3.10 2.58 21.7 18.4 11.9 14.0 -7.7 -15.2 1.9 Telekom Malaysia 4.64 3.76 18.7 19.8 20.1 19.0 -8.9 5.5 26.1 Berjaya Sports Toto 5.40 4.78 32.7 32.9 14.6 14.5 17.9 0.4 5.3 WCT 2.20 2.14 16.4 16.2 13.0 13.2 26.8 -1.6 2.5 Kinsteel 1.30 0.81 5.9 16.4 13.6 4.9 72.1 176.5 0.0 Hock Seng Lee 1.17 0.79 9.3 11.7 8.5 6.7 22.6 26.2 2.4 Source: Maybank-IB

- 2. Market Strategy Are we there yet? Four months ago, the question “Are we there yet?“ could only refer to whether markets had reached the bottom; today it could equally refer to whether we have reached a top – that is the measure of how confused investors are. Global markets have been fuelled by liquidity and optimism: Liquidity created by central banks’ attempts to unfreeze credit and money markets and government investments in certain institutions; Optimism that the world has avoided a global depression, and Asia is likely to rebound sooner, due to China’s growth. We make two points in this section: (i) that corporate profits have just begun to fall, and (ii) Chinese growth will not save us. Malaysia felt the impact of the global financial crisis via a slump in exports after July 2008. The electronics companies whose revenues slumped were initially mostly wholly-owned subsidiaries of foreign owned firms, and are barely represented in the equity market. The broader impact on domestic consumption only began to bite from end- 4Q08 and we believe its severity has accelerated in 1Q. The recession in corporate profits has just begun. Combined net profits of our research universe Combined Earnings (RM b) 12.0 10.8 10.8 10.6 8.9 9.0 7.3 6.0 3.0 0.0 CY 4Q07 CY 1Q08 CY 2Q08 CY 3Q08 CY 4Q08 Source: Maybank-IB The combined recurring net profit of the 80 stocks we cover fell by 16% QoQ in 3Q and a further 18% in 4Q. The 3Q profit decline was not sector wide but due to specific companies – Tenaga, Air Asia and two banks. The 4Q profit decline was mostly due to the plantation sector and Axiata. Excluding these, total net profit was more stable. 26 May 2009 Page 2 of 12

- 3. Market Strategy Net Profits of coverage universe excluding plantations, Axiata 10 Total NP excl plantations, Axiata (RM b) 9 8.3 8.3 8.1 8 7 6.7 6.6 6 5 4 3 2 CY 4Q07 CY 1Q08 CY 2Q08 CY 3Q08 CY 4Q08 Source: Maybank-IB So far in the May 2009 reporting season, an overwhelming 63% of stocks in our coverage universe that have reported showed contractions in sequential quarterly net profits. Every stock under our coverage in seven sectors showed a quarterly net profit decline. The seven sectors are property, plantations, REITs, semi-conductors, construction, building materials and media. Net profits of the six banks in our universe fell 2.1% QoQ, and a sharper 13.1% YoY. Don’t count on China Malaysia’s monthly exports have fallen by RM37bn between July 2008 (when exports peaked) and March 2009. Of this amount, exports destined for the US (directly and indirectly via other Asian countries) accounts for an estimated RM6.3bn, or 16% of the total export decline. Conversely, exports destined for final China demand accounts for only about RM2.4bn, or 4% of the decline, after excluding the amounts re- exported to the US. The US consumption recovery therefore, is far more important to Malaysian exports than Chinese consumption demand. Malaysian exports catering to final Chinese demand comprises primarily palm oil products, which represents 21% of total exports to China, and wood-based products. Exports of building materials account for only 11% of Malaysian exports to China. Exports of consumption goods to China account for under 10% of total Malaysian exports to China. This means that neither Chinese fiscal stimulus nor consumers will return Malaysian exports to anything close to previous levels. Another way to view this is to examine the relative sizes of consumer spending. Based on last year’s spending, the US consumer is 2.3x the size of total Chinese GDP, and 6.3x the size of Chinese consumers. 26 May 2009 Page 3 of 12

- 4. Market Strategy US vs. Chinese economies and consumers (USD b, 2008 prices) 16,000 14,265 14,000 12,000 10,058 10,000 8,000 6,000 4,402 4,000 1,601 2,000 0 US GDP US consumers Chinese GDP Chinese consumers Source: Maybank-IB We expect only an anaemic recovery in US consumer spending. Rising unemployment, job insecurity and falling house prices have already resulted in a rebound in the savings rate as households rebuild their balance sheets. US households are unlikely to return to their free spending ways for years. 26 May 2009 Page 4 of 12

- 5. Market Strategy Market valuation – expensive for the growth Having fallen 33% from its peak, one would expect bargains in the Malaysian market. Not so. Earnings have collapsed too. The KLCI has bounced from a p/e of 12x 2009 earnings to 15.2x now. It is only 10% below the previous cycle’s mid-cycle valuation. While 12x p/e may not seem unduly high, it is expensive relative to the anaemic growth prospects and to the recovery phase of the cycle we are at. Most large caps are fairly valued or expensive. 2010 earnings will be only at 2008 levels. At 1,053 pts, the KLCI is trading at 15.2x 2009 earnings, with earnings projected to fall 7.7% in 2009, and recover 9.7% in 2010. This is not attractive given that it represents an earnings CAGR of just 0.6% p.a. from end-2008. It is difficult to justify equities trading at over 15x p/e if the prospective growth is less than 1% for each of the next 2 years. This valuation level is also not attractive on a regional basis. The KLCI traded at 15-16x p/e in 2005 despite close to zero earnings growth, but there was then the prospect of double digit growth in the subsequent two years. With prospective single digit corporate earnings growth in 2010 and low single digit GDP growth, we consider a range of 10-13x is fair. Market valuation: KLCI and its P/E valuation 1600 (x) 20 1400 18 16 1200 Mean 14 1000 12 800 10 600 KLCI (LHS) PER (RHS) 8 6 400 4 200 2 0 0 01 02 03 04 05 06 07 08 09 Source: Maybank-IB, Bloomberg YoY change in market earnings Year 2001 2002 2003 2004 2005 2006 2007 2008 2009F 2010F % chg -7.9 33.1 26.4 19.1 0.0 17.9 21.7 -5.4 -7.7 9.7 Source: Maybank-IB 26 May 2009 Page 5 of 12

- 6. Market Strategy Market valuation has moved too far, unsupported by growth. At under 12x, the Malaysian market did appear cheap in early 2009 relative to its 10-year historical average of 15.8x. The current 15.2x p/e though, is only 4% below the 10-year average and is 9% from the 16.7x mid-point of the previous cycle’s valuation. Corporate earnings growth, at negative to single digit in 2009-10, have barely shown real signs of a recovery, but market valuation, being near its mid-cycle value, is expecting, and pricing in, a V-shaped recovery in 2010. We see no evidence for this, and we believe markets have moved too far, too fast. Peak-to-trough P/E valuations through the cycle Peak Trough Mid point Bear mkt: 1981-86 29.8x 14.3x 22.1 Bull mkt: 1988-93 33.7x 18.1x 25.9 Bear mkt: 1993-98 33.7x 9.6x 21.7 Bull mkt: 2000-2007 19.6x 13.8x 16.7 Current mkt: 2008 - now 19.2x 11.2x 15.2 Source: Maybank-IB KLCI year-end target By end-2009, with a prospective growth of around 9.7% in 2010, we believe fair valuation for the KLCI would be 990 pts, which represents a p/e of 13.0x earnings. We recognize liquidity and a seismic shift in global portfolios towards greater risk and therefore equities could continue to keep the domestic market at lofty valuations. If the KLCI reaches 1,100 in the near-term, it would be at 15.8x 2009 earnings – clearly expensive for the prospective growth, and a point at which we would turn distinctly bearish. Some signs that this rally is showing its age include rotational play out of large caps by domestic institutions, but latecomers, including foreign portfolio investors, may continue to keep the index at current levels. 26 May 2009 Page 6 of 12

- 7. Market Strategy Our Buy/Sell Lists: Bearish by value, not by numbers 40% of our stock coverage universe are Buy recommendations, 37% Sells and 23% Holds. By market capitalization though, our Buy list represents only 26% of our coverage universe, with 53% of market capitalization in Sells and 22% in Hold. If all our Buys reach their target prices, the KLCI would be 0.6% higher at 1,060. If all our Sells also reach their target prices, the index would be 6.6% lower, at 984. THE BUY LIST THE SELL LIST Name Mkt Cap TP Name Mkt Cap TP AEON Credit 337.2 3.16 AirAsia 2,777.9 0.85 AEON Co 1,474.2 4.70 Asiatic 4,126.0 3.80 Alam Maritim 576.6 1.55 Axiata 20,606.2 2.18 Axis REIT 360.8 1.78 BCHB 31,487.1 6.80 Bintulu Port 2,440.0 6.70 Bursa 3,579.4 3.76 Berjaya Sports 6,349.8 5.40 Dreamgate 148.2 0.11 CB Ind Product 370.0 3.60 Digi.Com 17,493.8 19.60 Guinness 1,812.6 6.50 Dialog 1,554.5 1.20 Hartalega Hldgs 833.6 4.00 EON Capital 2,634.2 3.40 HSL 439.9 1.17 F&N Hldgs 3,137.1 6.70 IJM Corp 5,227.8 5.50 Genting 18,222.9 4.40 KFC 1,368.1 7.90 Hap Seng 1,562.9 2.05 KLCC Prop 2,989.0 3.60 IOI Corp 29,229.0 3.50 Kossan Rubber 575.5 4.00 KL Kepong 13,023.6 9.80 Kinsteel 741.6 1.30 Lafarge 3,959.6 4.20 Litrak 1,144.6 2.88 MISC 31,060.6 7.50 MAHB 3,718.0 4.00 MPI 1,059.9 4.20 Petra Perdana 764.8 3.00 Media Prima 1,033.1 1.00 PLUS 16,600.0 3.20 Public Bank 30,198.0 7.60 QL Resources 874.5 3.80 Proton 1,559.8 2.50 Quill Capita 327.7 1.10 Petronas Gas 18,798.0 8.80 RCE Capital 362.6 0.62 SapCrest 1,725.8 1.00 JTI 1,098.4 5.30 Shell 3,120.0 7.80 Resorts World 14,282.6 3.10 SP Setia 3,863.9 2.00 SunCity 1,189.0 2.10 Star 2,304.3 2.54 Sunrise 837.2 1.90 Tan Chong 1,088.6 1.05 Telekom 13,594.1 4.64 TH Plantations 804.6 1.38 Tanjong 5,645.6 17.60 Tj Offshore 305.9 1.00 Tenaga 32,076.4 7.00 Unisem 518.6 0.77 Top Glove 1,838.4 6.00 WCT 1,529.2 2.20 Total mkt cap 121,780 250,983 Source:Maybank-IB Our Buy List is weighted towards the construction and consumer sectors. The construction sector preference can be supported by the new PM staking his credibility on successful implementation of the fiscal packages and contracts, that have hitherto been flowing slowly. Earnings are likely to grow next year through this year’s contract awards and many of the construction stocks under our coverage are far from peak cycle valuations of the previous cycle. Buying the construction sector is placing confidence in PM Najib’s ability to deliver economic stabilization through fiscal spending. 26 May 2009 Page 7 of 12

- 8. Market Strategy Within the consumer sector, the non-gaming stocks such as KFC and JTI have strong brand franchises and defensive qualities and continue to see top line growth. Also, these companies are continuing to expand their number of outlets, reflecting positive views of their longer-term prospects. The gaming companies report there is little impact so far on their revenues, and for Resorts World, we consider valuations to be reasonable, as most of its cash is not reflected in the share price. Buys in our preferred sectors EPS Growth Gross DPS Price EPS (sen) PE (%) (sen) Net Yield (%) TP May-22 2008 2009F 2010F 2009F 2010F 2009F 2010F 2009F 2010F 2009F 2010F Construction / Building Mat HSL 1.17 0.79 7.6 9.3 11.7 8.5 6.7 22.6 26.2 2.5 2.5 2.4 2.4 Kinsteel 1.30 0.81 3.5 5.9 16.4 13.6 4.9 72.1 176.5 0.0 0.0 0.0 0.0 WCT 2.20 2.14 13.0 16.4 16.2 13.0 13.2 26.8 -1.6 7.0 7.0 2.5 2.5 Consumer AEON Co 4.70 4.22 34.4 37.8 41.7 11.2 10.1 10.1 10.1 13.0 14.0 2.3 2.5 Sports Toto 5.40 4.78 27.8 32.7 32.9 14.6 14.5 17.9 0.4 34.0 34.0 5.3 5.3 JTI 5.30 4.30 37.5 40.5 43.2 10.6 10.0 8.0 6.5 53.0 53.5 9.2 9.3 KFC 7.90 7.05 62.1 67.7 75.4 10.4 9.3 9.0 11.5 47.0 52.4 5.0 5.6 Resorts World 3.10 2.58 23.5 21.7 18.4 11.9 14.0 -7.7 -15.2 6.5 5.5 1.9 1.6 High Yield Telekom 4.64 3.76 20.5 18.7 19.8 20.1 19.0 -8.9 5.5 130.7 27.1 26.1 5.4 JTI 5.30 4.30 37.5 40.5 43.2 10.6 10.0 8.0 6.5 53.0 53.5 9.2 9.3 Axis REIT 1.78 1.42 15.2 16.9 16.9 8.4 8.4 11.1 -0.4 16.4 16.3 8.7 8.6 Litrak 2.88 2.27 21.4 20.5 18.2 11.1 12.5 -3.9 -11.3 25.0 18.0 8.3 5.9 Quill Capita 1.10 0.84 7.5 8.2 8.4 10.3 10.0 8.5 2.8 8.2 8.1 7.3 7.3 BAT (M) 44.75 42.25 284.3 294.2 304.3 14.4 13.9 3.5 3.4 380.5 393.6 6.8 7.0 Guinness 6.50 6.05 41.6 44.4 45.7 13.6 13.2 6.6 3.0 50.0 52.0 6.2 6.4 Source: Maybank-IB Sell Hope and high expectations Within our Sell List are a number of stocks whose share prices have exceeded consensus target prices by 15% or more. These, we believe are stocks which have built into their prices high degrees of hope and expectations of near-term earnings recovery. They are on our list of Top Sells. Share Price Current Consensus Target Exceeds consensus by Bursa Malaysia 7.10 5.20 37% MISC 8.50 7.26 17% SP Setia 3.82 2.80 36% Tan Chong 1.64 1.30 26% Source: Maybank-IB 26 May 2009 Page 8 of 12

- 9. Market Strategy Legends of the fall The historical lesson to be learnt from previous bear markets is that we are not out of the woods. Bursa Malaysia has experienced two bear markets since the 1980s, one in each decade – 1980s and 1990s. Measured against the perspective of these two bear markets, the Malaysian market appears to be no more than half way through its current bear market. Assessing the current bear market against previous ones from the perspective of time and trend reversals, we find the following: There are many bear market reversals. In the previous bear markets, the KLCI witnessed 23 trend reversals of 5% or more between 1981-5, and 38 trend reversals in 1994-8. In the current bear market, the KLCI has so far made 12 trend reversals of over 5%, suggesting we are only about half way through. Bear markets last six years: The 1981-5 bear market took 58 months to play out, while the 1994-8 market played out in a similar 57 months. We are currently in the 17th month of the present bear market, which began in January 2008. If history repeats itself, we are just 30% of the way through the current bear market. There could be one huge bear market rally. Each of the bear markets witnessed one major rally before continuing its downtrend. In the 1981-5 bear market, a rally retraced 64% of its drop before continuing the decline. In the mid-1990s, the bear market rally retraced 91% of its drop before continuing its downtrend. The present bear market rally has retraced 32% of its drop. We believe the KLCI is tracing out a similar bear market rally. Our strategy revolves around overweights in the construction and building materials sector, selected consumer stocks and some high yield stocks. While we recognize this rally may well have room to run, we believe it is beginning to look expensive relative to growth. KLCI Bear Markets: 1981-86 and 1994-98 Source: Maybank-IB, Bloomberg 26 May 2009 Page 9 of 12

- 10. Market Strategy Politics: The Empire Strikes Back New prime minister Najib Tun Razak has pinned his credibility on swift implementation of the fiscal stimuli announced so far – RM7bn in Nov 2008 and RM60bn in Mar 2009. However, successful economic management may not translate to ballot box success – the Barisan Nasional’s poor electoral performance in 2008 was despite GDP growth rates which were among the fastest in the decade at 5.3% to 6.3%. A measure of the task ahead for the new leadership can be seen from the results of the five by-elections since the March 2008 general elections. In 4 out of 5 of these elections, the opposition increased its majority. By-Election Winning Majority Date Constituency Winning party Latest by- Mar 08 GE election 26 Aug 08 Permatang Pauh PKR 15,671 13,388 17-Jan-09 Kuala Terengganu PAS 2,631 628 07-Apr-09 Bukit Gantang PAS 2,789 1,566 07-Apr-09 Bukit Selambau PKR 2,403 2,362 07-Apr-09 Batang Ai BN 1,854 806 Source: Maybank-IB Against this worsening electoral sentiment post 2008 elections, the new leadership must feel it has its back to the wall and must deliver economic recovery through the stimulus, in under 3 years. Yet, as of 12th May, only RM0.8bn of the 1st stimulus package has been spent. This is positive for the future, because the new leadership has every reason to spend it way out of this malaise. It has already raised RM40bn YTD vs only RM19.5bn this time last year and is poised to accelerate the pace of construction awards massively in the next two to three quarters. We expect the government to raise a gross amount of RM100bn this year, including amounts needed for refinancing. We believe PM Najib recognizes the non-economic grouses too such as perceptions, allegations and incidences of corruption, favoritism, and inefficiency and discontent over educational and religious issues. The perception of having addressed these issues will be important. Within a month of taking office, Najib has gone on the offensive. Foreign investors were wooed with a relaxation of Bumiputera equity requirements in 27 business services, and the financial sector was further liberalised. We believe Najib will continue to chip away at such sacred cows, and these steps will have a positive effect on the market at least in the short-term. It would be unsurprising, therefore, if the new leadership implements additional initiatives to create a more inclusive and efficient government. Such moves would mimic the Badawi administration’s GLC reforms spearheaded by Khazanah and issuance of foreign brokerage licenses. 26 May 2009 Page 10 of 12

- 11. Market Strategy H1N1 virus – the replacement killer? Financial markets have shrugged off the possibility that the H1N1 virus could be substantially more lethal than the current prognosis, because markets probably over-reacted to the SARS pandemic in 2003. Markets have looked to the SARS episode and concluded that any impact on the economy will be temporary, so the effect on financial markets should be even more transient. SARS, after all, had a mortality rate of ‘only’ 9.6%, and its impact on the economies of China and Hong Kong, the epicenter of the pandemic, was less than 7 months. Markets are more optimistic the H1N1 flu virus will have a smaller impact because:- Authorities are more prepared, implementing measures that have evolved during SARS; The mortality rate appears much lower (under 1%) than for the SARS virus; The epicenter of the outbreak is not Asia; Ultimately, the impact of SARS on economies was temporary, and financial markets are willing to look beyond a temporary effect. Although the infection rate for H1N1 is now greater than for SARS in the same period, the mortality is so much lower it has not created the sort of panic and consumer behavior that SARS did. One of the dangers of such viruses is their ability to mutate, and take a nastier turn, although at present this possibility appears to be remote. This is a negative wildcard worth watching, but not yet worth reacting to. Confirmed Cases: SARS versus H1N1 Death Tolls: SARS versus H1N1 12,000 900 Cumulative Total Cumulative Total 800 10,000 700 8,000 600 500 6,000 400 4,000 300 2,000 200 100 0 0 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 SARS Confirmed Cases Days since official report started H1N1 Confirmed Cases SARS Deaths Days since official reports started H1N1 Deaths Source: Maybank-IB Source: Maybank-IB 26 May 2009 Page 11 of 12

- 12. Market Strategy Definition of Ratings Maybank Investment Bank Research uses the following rating system: BUY Total return is expected to be above 10% in the next 12 months HOLD Total return is expected to be between above -5% to 10% in the next 12 months SELL Total return is expected to be below -5% in the next 12 months Applicability of Ratings The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not carry investment ratings as we do not actively follow developments in these companies. Some common terms abbreviated in this report (where they appear): Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings BV = Book Value FV = Fair Value PEG = PE Ratio To Growth CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On Equity DPS = Dividend Per Share NTA = Net Tangible Asset ROSF = Return On Shareholders’ Funds EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date EV = Enterprise Value PBT = Profit Before Tax Disclaimer This report is for information purposes only and under no circumstances is it to be considered or intended as an offer to sell or a solicitation of an offer to buy the securities referred to herein. Investors should note that income from such securities, if any, may fluctuate and that each security’s price or value may rise or fall. Opinions or recommendations contained herein are in form of technical ratings and fundamental ratings. Technical ratings may differ from fundamental ratings as technical valuations apply different methodologies and are purely based on price and volume-related information extracted from Bursa Malaysia Securities Berhad in the equity analysis. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. This report is not intended to provide personal investment advice and does not take into account the specific investment objectives, the financial situation and the particular needs of persons who may receive or read this report. Investors should therefore seek financial, legal and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report. The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently verified by Maybank Investment Bank Bhd and consequently no representation is made as to the accuracy or completeness of this report by Maybank Investment Bank Bhd and it should not be relied upon as such. Accordingly, no liability can be accepted for any direct, indirect or consequential losses or damages that may arise from the use or reliance of this report. Maybank Investment Bank Bhd, its affiliates and related companies and their officers, directors, associates, connected parties and/or employees may from time to time have positions or be materially interested in the securities referred to herein and may further act as market maker or may have assumed an underwriting commitment or deal with such securities and may also perform or seek to perform investment banking services, advisory and other services for or relating to those companies. Any information, opinions or recommendations contained herein are subject to change at any time, without prior notice. This report may contain forward looking statements which are often but not always identified by the use of words such as “anticipate”, “believe”, “estimate”, “intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”, “should”, “could” or “might” occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions made and information currently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on these forward- looking statements. Maybank Investment Bank Bhd expressly disclaims any obligation to update or revise any such forward looking statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events. This report is prepared for the use of Maybank Investment Bank Bhd's clients and may not be reproduced, altered in any way, transmitted to, copied or distributed to any other party in whole or in part in any form or manner without the prior express written consent of Maybank Investment Bank Bhd and Maybank Investment Bank Bhd accepts no liability whatsoever for the actions of third parties in this respect. This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. Published / Printed by Maybank Investment Bank Berhad (15938-H) (Formerly known as Aseambankers Malaysia Berhad) (A Participating Organisation of Bursa Malaysia Securities Berhad) 33rd Floor, Menara Maybank, 100 Jalan Tun Perak, 50050 Kuala Lumpur Tel: (603) 2059 1888; Fax: (603) 2078 4194 Stockbroking Business: Level 8, MaybanLife Tower, Dataran Maybank, No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888; Fax: (603) 2282 5136 http://www.maybank-ib.com 26 May 2009 Page 12 of 12