Cairn india ltd q3 fy12 result update

•

0 gostou•438 visualizações

Cairn India reported a 12.5% rise in net profit for the third quarter driven by higher crude oil realizations and forex gains. Production is expected to increase with the ramp-up of new fields. While the stock has outperformed recently, the company is forecast to benefit from its low-cost assets as oil prices remain favorable. Analysts maintain a buy rating and price target of Rs. 415 based on Cairn's ability to increase production and realize higher prices in the current macroeconomic environment.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (17)

Destaque

Destaque (14)

Semelhante a Cairn india ltd q3 fy12 result update

Semelhante a Cairn india ltd q3 fy12 result update (20)

Mais de Vinit Bolinjkar LION bolinjkar.vinit@gmail.com

Mais de Vinit Bolinjkar LION bolinjkar.vinit@gmail.com (20)

Último

Último (20)

Cairn india ltd q3 fy12 result update

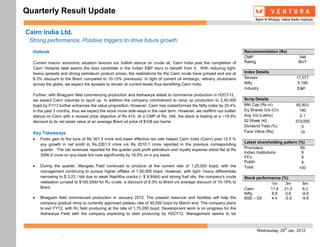

- 1. Quarterly Result Update Cairn India Ltd. Strong performance, Positive triggers to drive future growth Outlook Recommendation (Rs) CMP 346 Current macro- economic situation favours our bullish stance on crude oil, Cairn India post the completion of Rating BUY Cairn Vedanta deal seems the best candidate in the Indian E&P story to benefit from it. With reducing light- heavy spreads and strong petroleum product prices, the realizations for the Cairn crude have jumped and are at Index Details 8.3% discount to the Brent compared to 10-15% previously. In light of current oil embargo, refinery shutdowns Sensex 17,077 across the globe, we expect the spreads to remain at current levels thus benefiting Cairn India. Nifty 5,158 Industry E&P Further, with Bhagyam field commencing production and Aishwarya slated to commence production in H2CY12 , we expect Cairn volumes to spurt up. In addition the company commitment to ramp up production to 2,40,000 Scrip Details bopd by FY13 further enhances the value proposition. However, Cairn has outperformed the Nifty index by 20.4% Mkt Cap (Rs cr) 65,803 in the past 3 months, thus we expect the stock move side-ways in the near term. However, we reaffirm our bullish Eq Shares O/s (Cr) 190 stance on Cairn with a revised price objective of Rs 415. At a CMP of Rs. 346, the stock is trading at a ~19.9% Avg Vol (Lakhs) 2.1 discount to its net asset value at an average Brent oil price of $108 per barrel. 52 Week H/L 372/250 Dividend Yield (%) 0 Key Takeaways Face Value (Rs) 10 Forex gain to the tune of Rs 301.5 crore and lower effective tax rate helped Cairn India (Cairn) post 12.5 % Latest shareholding pattern (%) yoy growth in net profit to Rs.2261.9 crore v/s Rs 2010.1 crore reported in the previous corresponding quarter. The net revenues reported for the quarter post profit petroleum and royalty expense stood flat at Rs Promoters 59 Indian Institutions 6 3096.8 crore on qoq basis but rose significantly by 16.8% on a yoy basis. FII’s 6 Public 8 During the quarter, Mangala Field continued to produce at the current rate of 1,25,000 bopd, with the Total 100 management continuing to pursue higher offtake of 1,50,000 bopd. However, with light- heavy differentials narrowing to $ 3.23 / bbl due to weak Naphtha cracks (- $ 9.9/bbl) and strong fuel oils, the company’s crude Stock performance (%) realisation jumped to $100.3/bbl for RJ crude, a discount of 8.3% to Brent v/s average discount of 10-15% to 1m 3m 6m Brent. Cairn 11.4 21.0 8.3 Nifty 8.8 0.6 -8.9 Bhagyam field commenced production in January 2012. The present reservoir and facilities will help the BSE – Oil 4.4 -5.9 -9.9 company gradual ramp to currently approved plateau rate of 40,000 bopd by March end. The company plans to exit FY12, with RJ field producing at the rate of 1,75,000 bopd. Development work is on progress for the Aishwarya Field with the company expecting to start producing by H2CY12. Management seems to be th Wednesday, 25 Jan, 2012 .

- 2. Quarterly Result Update committed to ramp the production from the MBA fields to 2,40,000 bopd by 2013. EOR activities at the MBA field continues to progress at an expected rate with encouraging results. However, with the current pipeline capacity of 175,000 bopd, the company would require further investments or would have to rationalize production. Exploration charge for the quarter was at Rs 176.3 crore, much higher than Rs 38.9 crore reported in previous quarter majorly on account of plugged and abandoned well in Sri Lanka. Resultantly, EBITDA (Excl. OI) for the quarter stood at Rs 2369.2 crore v/s Rs 2541.8 crore, down by 6.8% yoy. However, other income of Rs 112.4 crore and foreign exchange gain on account of depreciating rupee (Rs 53.21) at Rs 301.5 crore helped the company post better profits. Lower interest and effective tax rate further helped uplift profit numbers. Cairn has guided for $1.0 - $1.25 billion for FY13 which would cover majority of investments including investments pertaining to ramp up of production in the MBA field, pipeline capacity expansion, investments in Barmer field, other satellite fields in RJ Block, EOR as well as exploratory activities in other blocks. Cairn India has commenced exploratory activities in 3 blocks in KG D6 Basin. Cairn Lanka has completed the first phase of the exploration campaign in Sri Lanka and are planning to enter the second phase. Net Cash at the end of the quarter stood at Rs 6460.2 crore, slightly lower on the back payment of debentures and other liabilities. th Wednesday, 25 Jan, 2012

- 3. Quarterly Result Update Description Q3FY12 Q3FY11 % Chg. Q3FY12 Q2FY12 % Chg. 9M201112 9M201012 % Chg. Net Sales 3096.8 3096.4 0.0 3096.8 2652.2 16.8 9461.6 6623.5 42.9 Other operational Income 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Total Oper. Income(TOI) 3096.8 3096.4 0.0 3096.8 2652.2 16.8 9461.6 6623.5 42.9 Raw Materials Cons.- - 0.0 - - - - - 0.0 - % to TOI - 0.0 - - - - - 0.0 - Stock adj. (-)Inc / (+)Dec- -11.4 4.9 - -11.4 - -207.8 -9.5 -35.2 -73.1 % to TOI -0.4 0.2 - -0.4 -0.1 -0.1 -0.5 - Net Raw Mat adj. for stock -11.4 4.9 - -11.4 -3.7 -207.8 -9.5 -35.2 -73.1 % to TOI -0.4 0.2 - -0.4 -0.1 -0.1 -0.5 - Other expenses 711.7 518.2 37.3 711.7 567.3 25.4 1810.9 1289.5 40.4 % to TOI 23.0 16.7 - 23.0 21.4 19.2 20.5 - Contribution Net_Sales 2396.5 2573.3 -6.9 2396.5 2088.6 14.7 7659.5 5304.4 44.4 Personnel 27.3 31.5 -13.5 27.3 23.5 16.2 69.8 80.4 -13.1 % to TOI 0.9 1.0 - 0.9 0.9 0.7 1.2 - Total expenditure 727.5 554.6 31.2 727.5 587.1 23.9 1871.2 1334.7 40.2 Operating Profit 2369.2 2541.8 -6.8 2369.2 2065.1 14.7 7590.4 5288.8 43.5 % to TOI 76.5 82.1 - 76.5 77.9 80.2 78.9 - Non-Operating Income 413.8 34.2 1111.4 413.8 593.0 -30.2 1059.6 90.4 1071.8 Interest 24.0 74.2 -67.7 24.0 122.8 -80.5 191.4 251.6 -23.9 Exceptional Items 0.0 0.0 0.0 0.0 -1355.2 100.0 -1354.4 64.8 - Gross Profit 2759.1 2501.8 10.3 2759.1 3890.5 -29.1 9813.0 5062.8 93.8 Depreciation 378.7 287.1 31.9 378.7 314.2 20.5 1039.0 728.6 42.6 PBT before Extra-ord 2380.3 2214.7 7.5 2380.3 865.9 174.9 6063.7 4334.2 39.9 % to TOI 76.9 71.5 - 76.9 32.7 - 64.1 65.4 - Extraordinary Items 0.0 - - - - 0.0 - PBT 2380.3 2214.7 7.5 2380.3 865.9 174.9 6063.7 4334.2 39.9 Tax Rate 5.0 9.2 -46.2 5.0 11.9 -58.2 5.2 10.6 -51.2 Prov. for Tax 118.4 204.6 -42.1 118.4 102.9 15.1 312.2 457.6 -31.8 % to TOI 3.8 6.6 - 3.8 3.9 - 3.3 6.9 - Profit after Tax 2261.9 2010.1 12.5 2261.9 763.0 196.4 5751.5 3876.6 48.4 % to TOI 73.0 64.9 - 73.0 28.8 - 60.8 58.5 - Minority Interest - - - - - - - 0.0 - PAT (adj. For MI) 2261.9 2010.1 12.5 2261.9 763.0 196.4 5751.5 3876.6 48.4 Face Value 10.0 10.0 - 10.0 10.0 - 10.0 10.0 - Equity Share capital 1903.0 1900.7 - 1903.0 1902.6 - 1903.0 1900.7 - EPS (Rs.) 11.9 10.6 12.4 11.9 4.0 196.5 30.2 20.4 48.2 CEPS (Rs.) 13.9 12.1 14.8 13.9 5.7 145.2 35.7 24.2 47.3 th Wednesday, 25 Jan, 2012

- 4. Quarterly Result Update P/E Bands P/B Bands EV/EBITDA Bands 450 700 120000 400 600 100000 350 300 500 80000 250 400 60000 200 150 300 40000 100 200 20000 50 100 0 0 -50 0 Jan-07 -20000 Jan-09 Jan-11 Jan-13 Jan-07 Jan-09 Jan-11 Jan-07 Jan-09 Jan-11 Jan-13 CMP 7X 8X 9X 10X 11X CMP 1X 1.25X 1.5X 1.75X 2X EV 3X 4.5X 6X 7.5X 9X NIFTY Comparison BSE- OIL Comparison Rating Chart 120.0 120.0 24 EXPECTED 2YR EPS CAGR% 110.0 110.0 20 100.0 100.0 90.0 90.0 16 CAIRN 80.0 80.0 12 ONGC 70.0 70.0 60.0 60.0 8 RIL 50.0 50.0 4 40.0 40.0 0 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 0 1 2 3 4 5 6 Cairn Nifty Cairn BSE Oil RATING SCORE th Wednesday, 25 Jan, 2012

- 5. Quarterly Result Update Price Realization & Gas Production Production Profile of Rajasthan Block 200 Q1 FY12 180 Q2 FY12 160 Q3 FY12 140 Q4 FY12 120 Q1 FY13 Q2 FY13 (bdp) 100 80 Q3 FY13 60 Q4 FY13 Q1 FY14 40 Q2 FY14 20 Q3 FY14 0 Q2 FY11 Q3 FY11 Q4 FY11 Q1 FY12 Q2 FY12 Q3 FY12 0 50000 100000 150000 200000 250000 Price Realization (USD/boe) Gas Production (Kbopd) Production Profile of Rajasthan Block Rajasthan (Block RJ-ON-90/1) Particulars Q3 FY 12 Q3 FY11 Y-o-Y (%) Q2 FY 12 Q-o-Q (%) Average daily gross operated Production (bopd) 125,122 124,861 0.2 125,251 -0.1 Average daily working Interest (bopd) 87,585 87,403 0.2 87676 -0.1 Eastern India (Block PKGM-I- PKGM- Ravva Filed) – Krishna Godavari Block Basin Particulars Q3 FY 12 Q3 FY11 Y-o-Y (%) Q2 FY 12 Q-o-Q (%) Average daily gross operated Production (boepd) 36,567 39,434 -7 36,185 1 Average daily oil production (bopd) 26,254 29,667 -12 26,965 -3 Average daily Gas production (mmscfd) 62 59 5 55 12 Average daily working Interest Production (boepd) 8,228 8,873 -7 8,142 1 th Wednesday, 25 Jan, 2012

- 6. Quarterly Result Update Western (Block CB/OS-2) – Cambay Basin Particulars Q3 FY 12 Q3 FY11 Y-o-Y (%) Q2 FY 12 Q-o-Q (%) Average daily gross operated Production (boepd) 7,890 9,988 -21 8,508 -7 Average daily oil production (bopd) 4,795 6,279 -24 5,390 -11 Average daily Gas production (mmscfd) 19 22 -17 19 - Average daily working Interest Production (boepd) 3,156 3,995 -21 3,403 -7 Sensitivity Analysis Crude Oil ($/bbl) TP (Rs) 80 90 100 108 120 130 140 150 43 265 299 333 360 401 435 470 504 44 272 307 342 369 411 446 481 516 45 279 314 350 379 422 457 493 529 Exchange Rate 46 286 322 359 388 432 468 505 541 47 293 330 367 397 442 479 516 554 48 300 338 376 406 452 490 528 566 49 306 345 384 415 462 501 540 579 50 313 353 393 425 472 512 551 591 51 320 361 401 434 482 523 563 604 52 327 369 410 443 492 534 575 616 53 334 376 418 452 503 545 587 629 th Wednesday, 25 Jan, 2012

- 7. Quarterly Result Update Financials & Projections Y/E March, Fig in Rs. Cr FY 2010 FY 2011 FY 2012e FY 2013e Y/E March, Fig in Rs. Cr FY 2010 FY 2011 FY 2012e FY 2013e Profit & Loss Statement Per Share Data (Rs) Net Sales 1623.0 10277.9 13466.8 17860.9 EPS 5.5 33.3 57.5 60.3 % Chg. 533.3 31.0 32.6 Cash EPS 5.6 36.5 50.8 70.1 Total Expenditure 988.7 2614.5 2928.5 3843.3 DPS 0.0 0.0 0.0 0.0 % Chg. 164.4 12.0 31.2 Book Value 178.1 211.9 269.4 329.7 EBDITA 634.3 7663.4 10538.3 14017.6 Capital, Liquidity, Returns Ratio EBDITA Margin % 39.1 74.6 78.3 78.5 Debt / Equity (x) 0.1 0.1 0.0 0.0 Other Income 407.7 128.8 1255.5 353.0 Current Ratio (x) 1.5 2.7 4.8 5.8 PBDIT 1042.0 7792.2 11793.8 14370.5 ROE (%) 3.1 15.7 16.1 18.3 Depreciation 10.9 611.3 1431.6 1856.5 ROCE (%) 2.8 17.9 22.1 22.2 Interest 14.8 290.9 208.3 313.2 Dividend Yield (%) 0.0 0.0 0.0 0.0 Exceptional Items -1355.2 Valuation Ratio (x) PBT 1016.3 6890.0 8798.7 12200.8 P/E 62.6 10.4 6.0 5.7 Tax Provisions -34.8 555.6 575.5 732.0 P/BV 1.9 1.6 1.3 1.0 Reported PAT 1051.1 6334.4 8223.3 11468.8 EV/Sales 39.4 6.2 4.8 3.6 PAT Margin (%) 64.8 61.6 61.1 64.2 EV/EBIDTA 100.9 8.4 6.1 4.6 Efficiency Ratio (x) Operational Exp. / Sales (%) 26.2 14.8 15.7 15.7 Inventory (days) 65.4 11.6 10.6 9.3 Manpower cost / Sales (%) 6.8 1.1 0.8 0.7 Debtors (days) 69.0 52.7 55.0 55.0 Tax Rate (%) -3.4 8.1 6.5 6.0 Creditors (days) 194.6 37.3 40.6 40.6 Balance Sheet Cash Flow statement Share Capital 1943.4 1957.4 1962.5 1962.5 Profit After Tax 1051.1 6334.4 10933.6 11468.8 Reserves & Surplus 31925.0 38335.8 49269.5 60738.2 Depreciation 10.9 611.3 1431.6 1856.5 Minority Interest & Others 0.0 0.0 0.0 0.0 Working Capital Changes -660.5 -761.4 -1935.9 -747.2 Total Loans 3400.7 2678.2 1670.0 1562.4 Others -264.5 305.7 92.4 0.0 Deferred Tax Liability 445.3 561.2 568.3 568.3 Operating Cash Flow 137.0 6490.0 10521.8 12578.0 Total Liabilities 37714.4 43532.6 53470.2 64831.4 Capital Expenditure -3238.1 -2835.1 -2015.4 -3128.3 Goodwill 25319.3 25319.3 25319.3 25319.3 Change in Investment -1541.1 618.0 -109.4 -120.4 Gross Block 222.8 6653.9 7319.3 8197.7 Cash Flow from Investing -4779.3 -2217.1 -2124.8 -3248.7 Less: Acc. Depreciation 95.8 730.4 2162.0 4018.5 Proceeds from equity issue 0.3 4.9 5.1 0.0 Net Block 127.0 5923.6 5157.3 4179.2 Inc/ Dec in Debt -955.7 -722.5 -1008.2 -107.7 Capital Work in Progress 9662.9 6066.8 7416.8 9666.8 Dividend and DDT 0.0 0.0 0.0 0.0 Investments 1712.4 1094.4 1203.9 1324.3 Cash Flow from Financing -955.4 -717.6 -1003.1 -107.7 Net Current Assets 717.6 5034.3 14371.0 24340.0 Net Change in Cash -5597.6 3555.3 7393.8 9221.7 Misc Expenses 175.2 94.3 1.9 1.9 Opening Cash Balance 6527.1 929.4 4484.7 11885.7 Total Assets 37714.4 43532.6 53470.2 64831.4 Closing Cash Balance 929.4 4484.7 11878.5 21107.3 th Wednesday, 25 Jan, 2012

- 8. Quarterly Result Update Ventura Securities Limited Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079 This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be reliable, but no responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in the securities mentioned in their articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the above information/articles. Reproduction in whole or in part without written permission is prohibited. This report is for private circulation. th Wednesday, 25 Jan, 2012