1. 1

CASE STUDIES

(1) IAS 1: Presentation of financial statements

FLOUR MILLS NIGERIA PLC

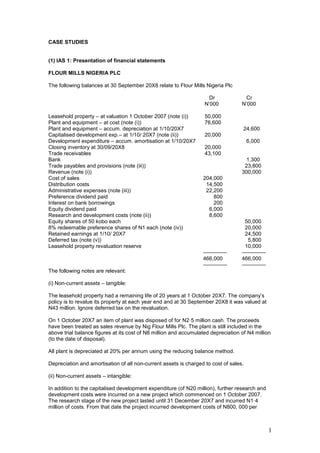

The following balances at 30 September 20X8 relate to Flour Mills Nigeria Plc

Dr Cr

N’000 N’000

Leasehold property – at valuation 1 October 2007 (note (i)) 50,000

Plant and equipment – at cost (note (i)) 76,600

Plant and equipment – accum. depreciation at 1/10/20X7 24,600

Capitalised development exp.– at 1/10/ 20X7 (note (ii)) 20,000

Development expenditure – accum. amortisation at 1/10/20X7 6,000

Closing inventory at 30/09/20X8 20,000

Trade receivables 43,100

Bank 1,300

Trade payables and provisions (note (iii)) 23,800

Revenue (note (i)) 300,000

Cost of sales 204,000

Distribution costs 14,500

Administrative expenses (note (iii)) 22,200

Preference dividend paid 800

Interest on bank borrowings 200

Equity dividend paid 6,000

Research and development costs (note (ii)) 8,600

Equity shares of 50 kobo each 50,000

8% redeemable preference shares of N1 each (note (iv)) 20,000

Retained earnings at 1/10/ 20X7 24,500

Deferred tax (note (v)) 5,800

Leasehold property revaluation reserve 10,000

–––––––– ––––––––

466,000 466,000

–––––––– ––––––––

The following notes are relevant:

(i) Non-current assets – tangible:

The leasehold property had a remaining life of 20 years at 1 October 20X7. The company’s

policy is to revalue its property at each year end and at 30 September 20X8 it was valued at

N43 million. Ignore deferred tax on the revaluation.

On 1 October 20X7 an item of plant was disposed of for N2·5 million cash. The proceeds

have been treated as sales revenue by Nig Flour Mills Plc. The plant is still included in the

above trial balance figures at its cost of N8 million and accumulated depreciation of N4 million

(to the date of disposal).

All plant is depreciated at 20% per annum using the reducing balance method.

Depreciation and amortisation of all non-current assets is charged to cost of sales.

(ii) Non-current assets – intangible:

In addition to the capitalised development expenditure (of N20 million), further research and

development costs were incurred on a new project which commenced on 1 October 2007.

The research stage of the new project lasted until 31 December 20X7 and incurred N1·4

million of costs. From that date the project incurred development costs of N800, 000 per

2. 2

month. On 1 April 2008 the directors became confident that the project would be successful

and yield a profit well in excess of its costs. The project is still in development at 30

September 20X8.

Capitalised development expenditure is amortised at 20% per annum using the straight-line

method. All expensed research and development is charged to cost of sales.

(iii) Nigeria Flour Mills Plc is being sued by a customer for N2 million for breach of contract

over a cancelled order. Nigeria Flour Mills has obtained legal opinion that there is a 20%

chance that it will lose the case. Accordingly Nigeria Flower Mill has provided N400, 000 (N2

million x 20%) included in administrative expenses in respect of the claim. The unrecoverable

legal costs of defending the action are estimated at N100, 000. These have not been provided

for as the legal action will not go to court until next year.

(iv) The preference shares were issued on 1 April 20X8 at par. They are redeemable at a

large premium which gives them an effective finance cost of 12% per annum.

(v) The directors have estimated the provision for income tax for the year ended 30

September 20X8 at N11·4 million. The required deferred tax provision at 30 September 20X8

is N6 million.

Required:

In accordance with IAS 1, Presentation of Financial Statement, prepare

(a) The statement of comprehensive income for the year ended 30 September 20X8.

(b) The statement of changes in equity for the year ended 30 September 20X8.

(c) The statement of financial position as at 30 September 20X8.

Note: notes to the financial statements are not required.

(ACCA F7 Dec 2008 Adapted)

(2) IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

(a) IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors contains

guidance on the use of accounting policies and accounting estimates.

Required:

Explain the basis on which the management of an entity must select its accounting

policies and distinguish, with an example, between changes in accounting policies and

changes in accounting estimates.

(b) The directors of Consolidated Breweries are disappointed by the draft profit for the year

ended 30 September 2010. The company’s assistant accountant has suggested two areas

where she believes the reported profit may be improved:

(i) A major item of plant that cost N20 million to purchase and install on 1 October 2007 is

being depreciated on a straight-line basis over a five-year period (assuming no residual

value). The plant is wearing well and at the beginning of the current year (1 October 2009) the

production manager believed that the plant was likely to last eight years in total (i.e. from the

date of its purchase). The assistant accountant has calculated that, based on an eight-year

life (and no residual value) the accumulated depreciation of the plant at 30 September 2010

would be N7·5 million (N20 million/8 years x 3). In the financial statements for the year ended

3. 3

30 September 2009, the accumulated depreciation was N8 million (N20 million/5 years x 2).

Therefore, by adopting an eight-year life, Consolidated Breweries can avoid a depreciation

charge in the current year and instead credit N0·5 million (N8 million – N7·5 million) to the

income statement in the current year to improve the reported profit.

(ii) Most of Consolidated Breweries’ competitors value their inventory using the average cost

(AVCO) basis, whereas Consolidated Breweries uses the first in first out (FIFO) basis. The

value of Consolidated Breweries’ inventory at 30 September 2010 (on the FIFO basis) is N20

million; however on the AVCO basis it would be valued at N18 million. By adopting the same

method (AVCO) as its competitors, the assistant accountant says the company would

improve its profit for the year ended 30 September 2010 by N2 million. Consolidated

Breweries’ inventory at 30 September 2009 was reported as N15 million, however on the

AVCO basis it would have been reported as N13·4 million.

Required:

Comment on the acceptability of the assistant accountant’s suggestions and quantify

how they would affect the financial statements if they were implemented under IFRS.

Ignore taxation.

(ACCA F7 Dec 2010)

(3) IAS 7 Statement of Cash Flow

Pinto is a publicly listed company. The following financial statements of Pinto are available:

Statement of comprehensive income for the year ended 31 March 2008

N’000

Revenue 5,740

Cost of sales (4,840)

––––––

Gross profit 900

Income from and gains on investment property 60

Distribution costs (120)

Administrative expenses (note (ii)) (350)

Finance costs (50)

––––––

Profit before tax 440

Income tax expense (160)

––––––

Profit for the year 280

––––––

Other comprehensive income

Gains on property revaluation 100

––––––

Total comprehensive income 380

––––––

Statements of financial position as at 31 March 2008 31 March 2007

N’000 N’000 N’000 N’000

Assets

Non-current assets (note (i))

Property, plant and equipment 2,880 1,860

4. 4

Investment property 420 400

–––––– ––––––

3,300 2,260

Current assets

Inventory 1,210 810

Trade receivables 480 540

Income tax asset nil 50

Bank 10 1,700 nil 1,400

––––– –––––– –––––– ––––––

Total assets 5,000 3,660

–––––– ––––––

Equity and liabilities

Equity shares of 20 kobo each (note (iii)) 1,000 600

Share premium 600 nil

Revaluation reserve 150 50

Retained earnings 1,440 2,190 1,310 1,360

––––– –––––– –––––– ––––––

3,190 1,960

Non-current liabilities

6% loan notes (note (ii)) nil 400

Deferred tax 50 50 30 430

––––– ––––––

Current liabilities

Trade payables 1,410 1,050

Bank overdraft nil 120

Warranty provision (note (iv)) 200 100

Current tax payable 150 1,760 nil 1,270

––––– –––––– –––––– ––––––

Total equity and liabilities 5,000 3,660

–––––– ––––––

The following supporting information is available:

(i) An item of plant with a carrying amount of N240, 000 was sold at a loss of N90, 000 during

the year. Depreciation of N280, 000 was charged (to cost of sales) for property, plant and

equipment in the year ended 31 March 2008.

Pinto uses the fair value model in IAS 40 Investment Property. There were no purchases or

sales of investment property during the year.

(ii) The 6% loan notes were redeemed early incurring a penalty payment of N20, 000 which

has been charged as an administrative expense in the income statement.

(iii) There was an issue of shares for cash on 1 October 2007. There were no bonus issues of

shares during the year.

(iv) Pinto gives a 12 month warranty on some of the products it sells. The amounts shown in

current liabilities as warranty provision are an accurate assessment, based on past

experience, of the amount of claims likely to be made in respect of warranties outstanding at

each year end. Warranty costs are included in cost of sales.

(v) A dividend of 3 kobo per share was paid on 1 January 2008.

Required:

Prepare a statement of cash flows for Pinto for the year to 31 March 2008 in

accordance with IAS 7 Statement of cash flows.

(ACCA F7 Jun 2008)