1. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 1 of 8

What is the rationale behind contingent capital and other hybrid debt instruments?

Can you explain the main trade-offs at play behind their most important design

features?

In this report, I will begin by defining hybrid securities and contingent capital notes, then

discuss the design features (language and structure) of the two securities. I will also look

at recent hybrid issues, their structures and how they have evolved. Then, I will look at

reasons why corporates and financial institutions issue such securities. Given, that tax

regimes differ by region and a uniform treatment is still pending, analyses on tax will be

limited. This report will focus on issuers, regulation facing CCNs, rating agencies and

investors.

Hybrid Corporate Debt: What is it?

Hybrid debt is essentially a fixed-coupon paying note with no set maturity (perpetual) that

is junior or sub-ordinated to other debt in the capital structure. Figure 1 illustrates the

seniority of claims. In bankruptcy or liquidation scenario, the debt ranks junior to all other

debt and is only paid once all other obligations or claims are satisfied, implying a lower

recovery.

For pricing and recovery analysis, sub-debt carries a recovery rate of 20% versus 40% for

senior debt. The investors are paid a premium for the additional risk they take and the

spread is subject to the credit profile of each issuer.

Typical Corporate Balance Sheet Typical Capital Structure

Current Assets

Senior Secured Debt

Senior Unsecured Debt

+ Subordinated Debt

Fixed Assets

Hybrid

Equity

Figure 1: Example of a corporate balance sheet and capital structure.

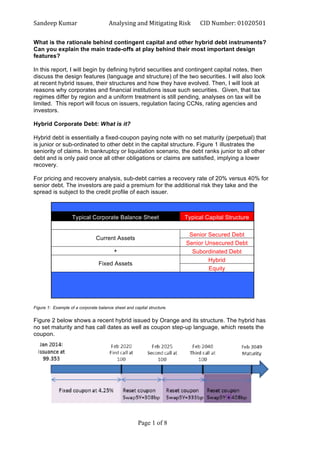

Figure 2 below shows a recent hybrid issued by Orange and its structure. The hybrid has

no set maturity and has call dates as well as coupon step-up language, which resets the

coupon.

2. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 2 of 8

Figure 2

Source: Natixis, Ideas – Fixed Income, June 2014.

Contingent Capital Notes (CCNs)- What are they?

Contingent Capital Notes are hybrid securities issued by financial institutions (FI). These

come in various forms; Enhanced Capital Notes (ECNS), Alternative Tier 1 (AT1),

Contingent Convertible Securities (Cocos), and T2 Cocos but essentially they are all junior

ranking or second lien debt that carry a loss absorbing mechanism. They provide leverage

and an “equity buffer” for the issuer. At times of crisis, these automatically covert into

equity i.e. when the banks capital ratio falls below a set trigger level.

Furthermore, they provide a tax efficient way of raising capital and are complimentary to

the issuers CET (common equity) ratios, which is a focus for all banks following Basel III

requirements. The focus for banks is to issue the right debt; one that meets the required

percentage for risk weighted assets (RWA) in T1 capital and meets the leverage ratio

requirement i.e.T1/Exposure measure, which in laymen terms is total assets plus off

balance sheet items.

CCN’s were introduced in late 2009 following an asset liability management exercise by

Lloyds Treasury to replace existing legacy Lower Tier 2 (LT2), Upper Tier 2 (UT2) and Tier

1 (T1) debt. The new instruments carried a predefined trigger option that allowed the

issuer (in this case, Lloyds) to convert their debt into equity, which essentially allowed that

bank to increase its core capital without the needed to tap equity capital markets. The

investors were paid an attractive coupon to compensate for this risk. Attractive proposition

at the time given over 40% of equity was still owned by the government.

Language and Features:

The common features and their impact for hybrids are shown in figure 3.

The corporates main aim is to get the highest equity treatment from rating agencies at the

lowest cost possible. The obvious cost is paying investors the risk premium i.e. a high

coupon.

Features Impact

Cash Cumulative

Interest Deferral

Issuers right to defer coupon payment but the interest is

cumulative and compounded.

Dividend Pusher

Either forces coupon payment on the hybrid or limit any

coupon or dividend payment on instruments ranking pari

passu or subordinated to the hybrid debt in the event of

coupon cancellation on this debt.

Replacement

Capital Covenant

(RCC)

The obligation or intent to replace the hybrid debt with capital

of similar or better quality.

Mandatory Interest

Deferral

Covenants, if breached, require coupon to be deferred.

Proffered by ratings agencies.

Coupon Step-up

Call options accompanied by a coupon step-up associated

with the call dates.

Change of Control

(Coca)

Protects investors in the event of takeover of the parent

company, with a 500bps coupon step-up in most cases.

Alternative Coupon

Satisfaction

Mechanism (ACSM)

Option offering compensation (most often in shares) for

investors at the time of coupon cancellation.

Figure 3

3. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 3 of 8

Source: www.hughyieldbonds.com/covenants

Issuance: The re-emergence

The issuance of subordinated bonds by corporates re-emerged in mid 2010 where utilities

and telecoms dominated this space. The rationale was simple for the two sectors: high

capital expenditure and stretched balance sheets. The corporate hybrids allow issuers to

issue debt and earn partial equity treatment by the credit rating agencies (please note: the

treatment language by credit agencies has changed hence the partial equity treatment).

Furthermore, tax breaks also provide an incentive to issue hybrid as one can treat interest

as an expense and still get favorable equity treatment. However, I believe a combination of

low interests rates, central bank action (namely QE) and inflow of money made hybrids

and cocos compelling for investor that lead to record hybrid issuance (figure 4b) – in 2014,

we saw 46bnEur Corporate Hybrid (figure 4) and 50bnEur Cocos (Bloomberg, 2015).

Figure 4 a Figure 4 b

Source: Dealogic and FT Source: Markit, BNP Paribas, Bloomberg

Credit Rating Agencies: Rating a Hybrid and Cocos

i) Corporate Hybrids

Ratings agencies rate the hybrid debt a few notches below the senior debt but this differs

from issuer to issuer and by methodologies. One can assume, as a rule of thumb, that

hybrids are rated two to three notches below senior debt. The lower the rating, the higher

the risk and the closer it is to equity treatment.

Key features analyzed by agencies for a corporate hybrid are: subordination, coupon

deferral language and maturity. A summary of these (required by the top three ratings

agencies) is shown in figure 5. So, naturally issuers’ structure their hybrid to their issue

qualifies for the 50% equity treatment.

4. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 4 of 8

Figure 5

Source: Western Asset Management Monthly Report, 2013

Figure 6 shows a RNS issued by Moody’s following their assessment of Telefonica’s

hybrid issue from 2013. Moody provides its credit rationale and rating.

Figure 6

Source: www.telefonica.com/investors

5. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 5 of 8

ii) CCN’s

The approach by agencies on Contingent Capital Notes differs to that of corporate hybrids.

Historically, the key elements for T1 Perps (legacy CCNS) were the following:

a) "Going concern"?

b) "Gone-concern"?

c) Is the loss-absorbing hybrid there when needed?

The considerations above are self-explanatory. However, as the regulatory framework

evolved under Basel III, issuers and their treasury departments were innovative (funkier) in

their structures to satisfy: a) the regulators, b) rating agencies but more importantly, c) the

investor base.

The funkier structures and regulatory developments have led to agencies scrutinising the

CCNS further and looking at them on a case-to-case basis to fully understand the special

features.

The most interesting one (for me) is the recent Societe General 8.75% 49 AT1 that, in

addition to being a “going concern”, carries write down and write up language. So, at times

of distress the issue is written down as a “going concern” but as the bank recovers, the

investors have write-up language the kicks in – increasing the likely hood of getting their

principle investment back. The issue also has multiple triggers including regulatory calls to

protect the issuer from the evolving regulatory framework i.e. if it ceases to qualify the

issue as AT1.

Figure 7 (below) shows a summary of recent CCNs issued and their structures and

features.

Figure 7 (also see appendix)

Source: BNP Research: Cocos – European Credit Strategy Sep 2013.

The above table shows the complexity of the recent CCNs and how they have evolved

over the last decade. Banks are essentially looking at innovative ways to comply with the

regulators while reducing their cost of capital and engaging the investors. The rational for

the bank is clear: to get favourable treatment for CET calculation from the CCN.

6. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 6 of 8

Assessing Hybrids

For investors, the most important features when assessing hybrids are: ratings, language

in the offering memorandum, reputational risk of the issuer, rationale for issuance i.e. use

of proceeds and LBO risk. These are explained further in figure 8.

Figure 8

Source: Western Asset Management, Publication June 2013.

Conclusion

In summary, for corporates the incentive to issue hybrids is to diversify funding, tax breaks

and equity credit from rating agencies. For banks, it is to boost investor confidence and

have an equity cushion in case of a credit crisis.

In the current climate, hybrid issuance via CCNs and corporate hybrid is led by purely by

technicals. Investors are chasing yield and hybrids provide an attractive coupon but the

risks (in my view) are not fully compensated for (figure x).

Investors are attracted by the lower trigger levels on CCNs (in some cases as low as 5%)

and there is widespread belief that the sovereigns or the ECB will step-in at times of crisis

but they should remember that this is second tier debt that, like that case of Irish Banks,

can have haircuts. More importantly, most securities are a “going concern” that

automatically converts into equity before any form of government intervention comes into

play.

In my view, investors should avoid issuance with covenant lights features and should focus

their efforts into national champions (for corporates) and banks with a higher parent rating

that provide a hold-co guarantee. Issuers’ rationale for these is compelling in the current

climate but they need to keep in mind that these instruments can become costly if

regulation or methodologies change. Furthermore, there could be a contagion effect if

investor confidence fades away.

Word Count Inc. Headings and Subheadings: 1189.

Ratings:

This

is

more

important

for

investors.

One

should

pay

close

attention

to

the

full

capital

structure

of

the

issuer

and

where

the

debt

fits.

While

holding

company

(HoldCo)

ratings

are

important,

one

should

pay

attention

to

where

the

debt

lies

in

case

of

default,

leverage

buy-‐outs

and

how

interest

and

principal

payment

are

treated

following

ratings

action

(HoldCo

vs.

Opco).

Document

Language:

Terms

and

structures

vary

from

issuer

to

issuer

and

industry

to

industry

and

one

should

pay

close

attention

of

the

offering

memorandum/circular

to

fully

understand

what

happens

in

case

of

default

and

what

is

the

interest

deferral

language

i.e.

non-‐dividend

payment,

must-‐pay

or

deferred/cumulative

interest

payments.

Reputational

Risk:

One

should

assess

the

size

of

hybrid

relative

to

the

issuers

total

enterprise

value

and

the

coupon

vs.

the

dividend.

Issuers

are

concerned

about

their

reputation

and

more

importantly,

their

ability

to

raise

debt

via

debt

capital

markets

so

the

smaller

the

hybrid

issue

the

better

as

deferring

and

non-‐payment

of

coupons

can

dent

investor

confidence.

Rationale

for

issuance:

Historically,

hybrids

have

been

an

expensive

method

to

raise

funding

but

in

the

current

low

rates

environment

we

are

in

these

provide

an

incentive

for

issuers

to

raise

funding

at

a

lower

cost

of

capital.

LBO:

The

option

to

defer

interest

could

raise

serious

issues

for

investors.

In

case

of

a

LBO,

the

hybrid

can

essentially

turn

in

a

zero

coupon

perp

bond.

7. Sandeep

Kumar

Analysing

and

Mitigating

Risk

CID

Number:

01020501

Page 7 of 8

REFERENCE LIST

• BNP Paribas: European Credit Research: Valuing the Coco collection, September

2013.

• Natixis Asset Management: Ideas Fixed Income, June 2014.

• Moody’s Investor Services: Ratings Action, September 2013. Deutsche Bank

• Financial Times (2014), Telefonica SA. [Online] Available from:

http://markets.ft.com/research/Markets/Tearsheets/Summary?s=TEF:MCE

[Accessed: April 3rd

2015]

• Practical Law: Hybrid Securities: an Overview. Available from:

www.gobal.practicallaw.com/1-517-1581

[Accessed: April 3rd

2015]

• Western Asset Management, Corporate Hybrids, May 2013.