Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Tesoro.Buy.Sell_10.27.2016_Sensitive Sector

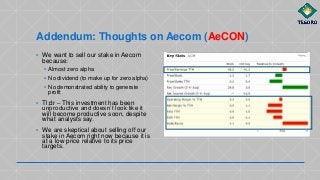

- 1. Addendum: Thoughts on Aecom (AeCON) ▪ We want to sell our stake in Aecom because: ▪ Almost zero alpha ▪ No dividend (to make up for zero alpha) ▪ No demonstrated ability to generate profit ▪ Tl;dr – This investment has been unproductive and doesn’t look like it will become productive soon, despite what analysts say. ▪ We are skeptical about selling off our stake in Aecom right now because it is at a low price relative to its price targets.

- 2. Addendum: Thoughts on Aecom We got in

- 3. Addendum: Thoughts on Aecom ▪ Analyst price targets are above its current price, which has dropped recently ▪ Analysts rate it as a buy because of its low current price, revenue growth, etc. ▪ Problem: Analysts have been pretty bullish on it forever, and it seems to always underperform

- 4. Addendum: Thoughts on Aecom ▪ To consider (not up for vote) ▪ Put in a limit order for around $30-$31 to sell it ▪ Monitor price expectations after putting in limit order ▪ Reanalyze the industrials sector at that time, as it is already under-allocated and would be even more under-allocated upon selling Aecom.

- 6. Sensitive Sector – Russell Romney, Justin Marino, Josh Rudolph – October 27, 2016

- 7. Investment Thesis Tesoro is an established company with solid assets, outstanding operating measures, and an excellent financial position. It is investing in sustainably expanding its competitive advantage by increasing its access to lower-price crude oil. The company is also well-poised to handle future uncertainty. We believe that Tesoro is undervalued considering its operating, financial, and growth position relative to its own results and to that of its peers in the oil refining and marketing sector, and that its high growth potential makes it a great investment.

- 8. Company Profile ▪ Fortune 100 company ▪ Independent refiner and marketer of petroleum products ▪ Strategically concentrated presence in the western U.S. ▪ Holds a 36% interest in Tesoro Logistics Partners, including the general partner interest ▪ “Moving ahead, we are committed to continuing to meet and exceed the standards of safe, reliable operations, while focusing on improving profitability and increasing shareholder value” (Company History | TSOCORP). Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 9. Snapshot Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 10. Products/Services ▪ Three revenue streams: ▪ Refining ▪ Marketing ▪ Tesoro Logistics ▪ Tesoro "operates seven refineries with a total crude oil capacity of 850,000 barrels per day after the acquisition of BP's 266 mb/d Carson refinery and the shutdown of its Hawaii refinery" Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 11. • Products/Services ▪ Operates retail fuel outlets in the Western and midcontinental United States ▪ "Tesoro’s retail-marketing system includes over 2,400 retail stations under the ARCO®, Shell®, Exxon®, Mobil®, USA Gasoline™, Rebel™ and Tesoro® brands" (Company Profile | TSOCORP)

- 12. Products/Services ▪ Total operating income is derived approximately from ▪ 65% from refining, ▪ 20% from marketing (retail fuel outlets), and ▪ 15% from Tesoro Logistics (36% equity interest)

- 13. Upcoming Events Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 14. Locations Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary ▪ Tesoro’s operations are concentrated on the West coast of the US, with some activity in the Bakken shale fields.

- 15. Industry Overview ▪ The Oil & Gas Refining & Marketing industry consists of companies engaged in the operation of oil and gas refineries for the production of heating, lubricating and fuel oils, as well as gasoline, diesel, jet fuel, propane, kerosene and other liquefied petroleum gas (LPG) products. The industry also includes marketing operations, such as bulk gasoline and crude oil terminals, and truck and automobile service stations with or without convenience stores. The industry excludes refining and marketing operations with substantial exploration and development operations, classified in Integrated Oil & Gas. Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 16. Industry – Fair Value Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary Oil & Gas Oil & Gas Integrated Oil & Gas Midstream Oil & Gas Refining & Marketing

- 17. ▪ Energy Sector (as a whole) is overvalued right now. ▪ Oil & Gas Refining & Marketing subsector is undervalued right now. Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary Neither are short-term trends; it’s been like this for several months. Industry – Fair Value (longer term)

- 18. Industry Moat ▪ The Oil & Gas Refining and Marketing industry is difficult to earn an economic moat in ▪ Economic moats in refining are earned through ▪ Proximity to crude production or access to stranded crude that results in the refiner capturing a discount to international benchmarks or ▪ Investing in being able to process lower-quality crude oil at a similar cost (easier, but less successful) ▪ Refining is a highly competitive business with no product differentiation, and refiners are price takers, with little control over input or output costs. ▪ Questions surround the sustainability of crude discounts prevent refiners from earning wide economic moats Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 19. Industry Indicators • The Brent/WTI price spread has decreased rapidly as US midstream companies have invested in better transport. • US refiners have had an input cost advantage when the spread is higher as they refine cheaper oil and sell refined output in a higher-price Brent-crude- dominated market. That advantage has disappeared as the spread has declined. • It has become more important to gain access to cost-advantaged (a.k.a. stranded) oil production. • Tl;dr – When the Brent/WTI spread is wider, midcontinent-focused US refiners have a profitability advantage, but this advantage is declining Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 20. Industry Indicators - Commodity Prices Tesoro (TSO) vs United States Oil (USO) 5 years - Despite drop in oil prices starting in 2014 and continuing, Tesoro has shown strong share price increase - As a refiner and marketer with relatively stable margins, oil prices don’t [perfectly] correlate to success of company like it would with a driller Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 21. Industry Indicators – Input Costs ▪ Input costs are expected to rise in 2017 from lows in 2016. Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 22. Economic Moat: Narrow Moat Trend: Stable ▪ From Morningstar: ▪ Midcontinent oil refineries get price discounts compared to coastal refineries because oil production is stranded . ▪ Tesoro has the only refinery in the Bakken region, and has invested in expanding its two midcontinent refineries to take greater advantage of those price discounts. ▪ Those price discounts are disappearing with the Brent/WTI spread convergence, so Tesoro’s west-coast focus makes less of a difference ▪ Tesoro has also: ▪ Undertaken one of the largest crude-by-rail project in the US to bring over 350,000 bpd from the Bakken region to a new facility in Vancouver, Washington, which will increase its yield and margins (compared to paying coastal rates for crude) and decrease its reliance on higher-cost imports from abroad and from declining Alaska/California. production ▪ This will also increase access to marine traffic ▪ Acquired BP’s Carson refinery in 2013; the company will continue to integrate that with its adjacent Wilmington refinery and realize cost and margin benefits from its added scale. (both refineries are next to each other in Los Angeles, California) ▪ Closed its high-cost Hawaii refinery that was not very profitable Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 23. Economic Moat: Narrow Moat Trend: Stable ▪ Tesoro has the highest Refining Margin Per Barrel of any of its immediate competitors (Valero, Marathon, Phillips 66) ▪ In the refining business, everything pretty much relies on refining margins; because Tesoro's are higher, it will be better able to withstand increases in the price of oil. Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 24. Economic Moat Summary ▪ Tesoro’s investment in access to stranded production will give them feedstock (crude input) discounts to maintain their refining margin advantage. ▪ Tesoro will continue to realize cost efficiencies from combining its refinery with BP’s refinery and from investment in its midcontinent refineries.

- 25. Tesoro vs. Competitors (price history) Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary • Tesoro has consistently demonstrated its ability to beat its closest competitors in price returns. • Morningstar analysts rate the beginning of CEO Goff’s tenure as successful; overall stewardship is Standard.

- 26. Key Financial Ratios Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary R/E to total assets • Tesoro does better than its immediate competitors in almost any financial metric. • Higher recent and average gross margin, operating margin, and profit margin. • Dupont: ROE and ROA are higher than competitors, both recently and on average. • ROIC is high, and the higher RE/TA shows a moderately mixed investment financing strategy.

- 27. EBITDA growth Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 28. Revenue Breakdown: Increasing importance of TLLP (Tesoro Logistics LP, a TSO Master Limited Partner subsidiary) Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary • Marketing’s effect on income is equal to [Marketing – Intersegment Sales] • Tesoro’s MLP TLLP has played an increasingly important role in Tesoro’s revenue. TLLP has a three-star rating in Morningstar right now and a market cap of $4.8B.

- 29. Debt breakdown Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary - As Tesoro has invested in increasing their competitive advantage, they have also marginally increased their debt to equity and leverage. However, these have stabilized both after a large spike in 2014; they are and will continue to realize the gains on those investments in the next several years.

- 30. Weighted Average Cost of Capital Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary Trend (added) • Tesoro’s WACC has decreased over time even as the company has continued to invest in growth. • lower-risk

- 31. Debt breakdown: ability to pay Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary Because of its strong capital structure and comfortable cash position, Tesoro will have no problem honoring its liabilities.

- 32. Cash Position Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 33. Cash Position - Sustainable Growth Rate ▪ A measure of the firm’s ability to grow using only current cash and funds from operations ▪ Tesoro’s cash flow position has increased relative to its competitors and it has a larger ability to grow Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 34. Fair Value and Price Ratios Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 35. Analyst Opinions ▪ Morningstar Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 36. Bullish & Bearish Perspectives Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 37. Beta 0 0.5 1 1.5 2 2.5 alon pbf phillips 66 ppg hollyfrontier western average valero delek tesoro marathon Beta by firm, Refining & Marketing ▪ Tesoro’s Beta is 2.03, which is high, but it is not too much higher than its industry average ▪ Our portfolio target Beta is 1.25we need growth, and Tesoro’s higher beta will help us toward that. Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 38. SWOT Analysis ▪ Strengths: ▪ Tesoro maintains good credit metrics with gross leverage of 1.5 times and net leverage of 1.4 times at June. ▪ Excellent liquidity with $1.1 billion of cash and equivalents, full availability on the $2.1 billion borrowing base of the Tesoro Corp. revolving credit facility and $1.4 billion available on Tesoro Logistics’ combined $1.6 billion credit facilities. ▪ Refining Margin/Barrel is higher than three nearest competitors ▪ Weaknesses ▪ Geographical Concentration, particularly in California ▪ Cost of production strongly affects margins ▪ As cost of production rises, margins will drop Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 39. SWOT Analysis ▪ Opportunities ▪ The priority to grow Tesoro Logistics should increase Tesoro’s own value through greater distributions and further diversification of earnings and cash flow from more volatile refining. ▪ Development of a crude by rail and marine facility in Washington ▪ "The increased throughput of discount crude, along with the integration of Carson, could ultimately deliver upward of $615 million in annual EBITDA improvement by 2017" ▪ Threats ▪ Advances in the electric vehicle industry ▪ Legislation to reduce carbon emissions, paricularly in California ▪ Any extended turnaround or shutdown because of an accident Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 40. Other risks ▪ High current inventory levels could lower refining output for near future ▪ Interest rate liftoff could hurt plans for continued capital investment Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 41. Compared to Traditional Davis Guidelines Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary Beta % Institutional Investors Market Capitalization Number of Analysts Davis Guideline 1.25 <65% > $500 million <10 Tesoro (TSO) 2.03 Unreported, competitors around 80% $9.73 billion 16

- 42. Davis Portfolio Sector Allocations Name Current value Percent of Portfolio Target allocationDifference Domestic equity $369,506 75.3% 70% 5.3% International equity $28,844 5.9% 10% -4.1% Fixed income $37,060 7.6% 10% -2.4% Cash $55,367 11.3% 10% 1.3% Consumer Discretionary $49,226 9.7% 6.00% 3.7% Energy $39,736 7.8% 11.00% -3.2% Financials $42,656 8.4% 7.00% 1.4% Healthcare $57,493 11.3% 10.00% 1.3% Technology $34,094 6.7% 10.00% -3.3% Industrials $26,492 5.2% 7.00% -1.8% Consumer Staples $61,831 12.1% 9.00% 3.1% Utilities $29,743 5.8% 4.00% 1.8% Telecommunications $11,721 2.3% 2.00% 0.3% Basic Materials $16,515 3.2% 4.00% -0.8% ▪ Target sector allocations are not extremely important, but we are under Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

- 43. Proposal Buy 200 shares of TSO at $84.38 per share for a total of $16,876. Effect on portfolio: Cash allocation from 11.3% to 7.9% (target 10%) Energy allocation from 7.8% to 11.1% (target 11%) Company Overview Industry Analysis Competitive Position Financial Analysis Valuation Risks Summary

Notas do Editor

- Analyst ratings and price target ranges from NASDAQ

- Russell

- Josh "Company History | TSOCORP." N.p., 2016. Web. 24 Oct. 2016.http://tsocorp.com/about-tesoro/company-history/

- "Company Profile | TSOCORP." N.p., 2016. Web. 24 Oct. 2016.http://tsocorp.com/about-tesoro/company-profile/

- Justin

- From Morningstar analyst report

- Refiner input cost is expected to rise in 2017 as compared to 2015 and 2016.

- Russell

- Their p/e ration is very good, and their price/ebitda ratio is just as good.,

- Justin

- Josh

- Quote from MorningStar

- Russell

- Justin