Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Tax Remedies and Revision of Orders

Semelhante a Tax Remedies and Revision of Orders (20)

Último

Último (20)

Tax Remedies and Revision of Orders

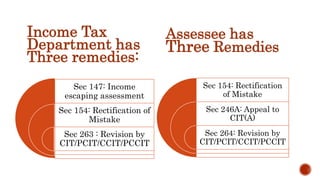

- 1. Income Tax Department has Three remedies: Sec 147: Income escaping assessment Sec 154: Rectification of Mistake Sec 263 : Revision by CIT/PCIT/CCIT/PCCIT Assessee has Three Remedies Sec 154: Rectification of Mistake Sec 246A: Appeal to CIT(A) Sec 264: Revision by CIT/PCIT/CCIT/PCCIT

- 4. Under this Section, CIT/PCIT/CCIT/PCCIT can call for and examine the “Records”of any proceeding in which Order has been passed by an A.O. which is : Erroneous Prejudicial to the interest of Revenue then CIT/PCIT/CCIT/PCCIT can pass any revisional order under this section as he deems fit. CIT/PCIT/CCIT/PCCIT can enhance, modify or cancel the assessment & direct for fresh assessment.

- 5. Order passed by A.O. shall be deemed to be erroneous in so far as it is prejudicial to the interest of the revenue, if in the opinion of the CIT/PCIT/CCIT/PCCIT : Order passed without making inquiries or verification which should have been made. The order is passed allowing any relief without inquiring into the claim. the order has not been made in accordance with any order, direction or instruction issued by the Board under section 119; the order has not been passed in accordance with any decision which is prejudicial to the assessee, rendered by the jurisdictional High Court or Supreme Court in the case of the assessee or any other person.

- 6. An Order can be said to be prejudicial to the revenue if: Income has been under assessed Losses have been over assessed Income has been assessed at a lower rate Excessive losses, deductions, allowances and reliefs have been allowed to assessee

- 7. The term Record means everything which is available on record at the time of examination of the file by CIT/PCIT/CCIT/PCCIT & not only those things which were available on record at the time of passing of the order by A.O. Example: A report of Valuation officer, which was not available earlier at the time of passing of the order of A.O. but is now available at time of the examination of the file by CIT/PCIT/CCIT/PCCIT.

- 8. An Opportunity of being heard must be given to assessee before any such revisional order. The time limit to pass any such order by CIT/PCIT/CCIT/PCCIT is 2 Years from the end of the Financial Year in which original order of A.O. was passed. Order passed under section 263 can be appealed against at ITAT level. CIT/PCIT/CCIT/PCCIT cannot revise matter involving appeal, means matter which are decided or considered in any appeal cannot be revised(Partial Merger),However CIT/PCIT/CCIT/PCCIT can revise other matters of same order.

- 12. CIT/PCIT/CCIT/PCCIT may either on his own motion or on an application made by assessee, call & examine the records of any proceeding ,in which an order other than referred u/s 263 has been passed by A.O. & CIT/PCIT/CCIT/PCCIT may pass such revisional order u/s 264 as he deems fit. The CIT/PCIT/CCIT/PCCIT can revise the order on his own motion within 1Year from date of passing of the order by A.O. If assessee applies for revision, then he can make an application within 1 Year from the date of receiving a copy of order by Assessee. If assessee has asked for revision the CIT/PCIT/CCIT/PCCIT has to pass an order within 1 Year from the end of F.Y. in which application was made by assessee. Order which is prejudicial to the interest of assessee cannot be passed under this section

- 13. • However once an appeal is preferred against an order of A.O., then such order cannot be revised by CIT/PCIT/CCIT/PCCIT u/s 264,even if appeal is on different grounds/matters.(Total Merger) • Appeal cannot be filed against order u/s 264. • Assessee can apply for revision u/s 264 only if : Time Limit to file CIT appeal has been expired(30 days) or, Assessee waived his right of appeal in writing.(where 30 days have not expired)

- 15. Appeal to CIT(A) Time limit for appeal shall be 30 days from the date of receipt of order sought to be appeal against. Appeal to ITAT is possible. Rs.250 to Rs.1000 One can go to highest authority in the entire appellate hierarchy i.e. Supreme Court. Application for revision u/s 264 Time limit to apply u/s 264 by assessee shall be 1 Year from the date of receipt of copy of orders sought to be revised. No further appeal possible Rs.500 irrespective of the amount of assessed income involved. One Man Show, no further appeal is possible.

- 16. An order can be revised any number of times, but within the time limit provided in section 263 and 264. What can be revised u/s 263 or 264 is only an Order. In other words, an Intimation u/s 143(1) cannot be revised under these sections. If the Order, which is sought to be appealed against, had been a subject matter of appeal, then such order can be revised by CIT/PCIT/CCIT/PCCIT u/s 263, but only to a limited extent.