QNBFS Daily Market Report May 02, 2018

•

1 gostou•157 visualizações

The QSE Index declined 1.1% to close at 9,014.3. Losses were led by the Real Estate and Telecoms indices, falling 4.8% and 1.9%, respectively.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a QNBFS Daily Market Report May 02, 2018

Semelhante a QNBFS Daily Market Report May 02, 2018 (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

QNBFS Daily Market Report May 02, 2018

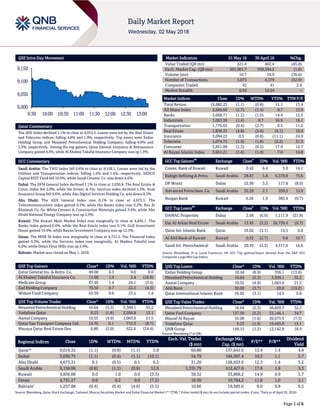

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 1.1% to close at 9,014.3. Losses were led by the Real Estate and Telecoms indices, falling 4.8% and 1.9%, respectively. Top losers were Ezdan Holding Group and Mesaieed Petrochemical Holding Company, falling 6.9% and 5.3%, respectively. Among the top gainers, Qatar General Insurance & Reinsurance Company gained 4.3%, while Al Khaleej Takaful Insurance Company was up 1.9%. GCC Commentary Saudi Arabia: The TASI Index fell 0.6% to close at 8,158.1. Losses were led by the Utilities and Transportation indices, falling 1.6% and 1.4%, respectively. SEDCO Capital REIT Fund fell 10.0%, while Saudi Ceramic Co. was down 4.6%. Dubai: The DFM General Index declined 1.1% to close at 3,030.8. The Real Estate & Const. index fell 2.0%, while the Invest. & Fin. Services index declined 1.5%. Arab Insurance Group fell 9.6%, while Aan Digital Services Holding Co. was down 8.3%. Abu Dhabi: The ADX General Index rose 0.1% to close at 4,673.3. The Telecommunications index gained 0.3%, while the Banks index rose 0.2%. Ras Al Khaimah Co. for White Cement & Construction Materials gained 3.4%, while Abu Dhabi National Energy Company was up 2.9%. Kuwait: The Kuwait Main Market Index rose marginally to close at 4,836.1. The Banks index gained 0.4%, while the Real Estate index rose 0.1%. Gulf Investment House gained 19.4%, while Bayan Investment Company was up 12.5%. Oman: The MSM 30 Index rose marginally to close at 4,731.3. The Financial index gained 0.3%, while the Services index rose marginally. Al Madina Takaful rose 6.0%, while Oman Flour Mills was up 3.9%. Bahrain: Market was closed on May 1, 2018. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. & Reins. Co. 49.00 4.3 0.0 0.0 Al Khaleej Takaful Insurance Co. 11.00 1.9 2.4 (16.9) Medicare Group 67.49 1.4 24.1 (3.4) Zad Holding Company 70.50 0.7 22.2 (4.3) Widam Food Company 63.39 0.6 23.5 1.4 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochemical Holding 16.64 (5.3) 3,309.1 32.2 Vodafone Qatar 9.23 (1.8) 2,056.8 15.1 Aamal Company 10.55 (4.9) 1,063.0 21.5 Qatar Gas Transport Company Ltd. 14.70 0.1 715.3 (8.7) Mazaya Qatar Real Estate Dev. 6.80 (2.0) 622.6 (24.4) Market Indicators 01 May 18 30 April 18 %Chg. Value Traded (QR mn) 221.4 402.4 (45.0) Exch. Market Cap. (QR mn) 501,061.7 509,394.2 (1.6) Volume (mn) 10.7 16.9 (36.6) Number of Transactions 3,073 4,579 (32.9) Companies Traded 42 41 2.4 Market Breadth 6:34 12:24 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 15,882.23 (1.1) (0.8) 11.1 13.4 All Share Index 2,666.66 (1.7) (1.4) 8.7 13.9 Banks 3,068.71 (1.2) (1.0) 14.4 12.5 Industrials 3,063.36 (1.4) 0.7 16.9 16.1 Transportation 1,776.65 (0.4) (2.7) 0.5 11.2 Real Estate 1,836.35 (4.8) (5.4) (4.1) 16.0 Insurance 3,094.22 0.5 (0.8) (11.1) 24.9 Telecoms 1,074.73 (1.9) (1.8) (2.2) 31.5 Consumer 5,851.00 (1.3) (0.5) 17.9 12.7 Al Rayan Islamic Index 3,661.21 (1.4) (1.4) 7.0 14.8 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Comm. Bank of Kuwait Kuwait 0.42 6.4 5.0 14.1 Rabigh Refining & Petro. Saudi Arabia 28.87 5.8 6,378.8 75.6 DP World Dubai 22.99 3.3 117.8 (8.0) Advanced Petrochem. Co. Saudi Arabia 52.29 2.1 359.5 13.9 Burgan Bank Kuwait 0.26 1.9 385.4 (9.7) GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% DAMAC Properties Dubai 2.58 (6.9) 1,111.9 (21.8) Dar Al Arkan Real Estate Saudi Arabia 13.43 (3.2) 26,739.4 (6.7) Qatar Int. Islamic Bank Qatar 55.02 (3.1) 14.5 0.8 Al Ahli Bank of Kuwait Kuwait 0.32 (2.7) 9.8 10.7 Saudi Int. Petrochemical Saudi Arabia 20.35 (2.3) 4,517.0 16.6 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 10.44 (6.9) 356.1 (13.6) Mesaieed Petrochemical Holding 16.64 (5.3) 3,309.1 32.2 Aamal Company 10.55 (4.9) 1,063.0 21.5 Ahli Bank 30.00 (3.7) 20.0 (19.2) Qatar International Islamic Bank 55.02 (3.1) 14.5 0.8 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Mesaieed Petrochemical Holding 16.64 (5.3) 56,829.3 32.2 Qatar Fuel Company 137.50 (2.2) 22,146.1 34.7 Masraf Al Rayan 35.00 (1.6) 20,675.9 (7.3) Vodafone Qatar 9.23 (1.8) 19,443.8 15.1 QNB Group 149.15 (1.2) 12,142.8 18.4 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,014.32 (1.1) (0.8) (1.1) 5.8 60.80 137,641.6 13.4 1.4 4.9 Dubai 3,030.75 (1.1) (0.4) (1.1) (10.1) 54.79 104,307.4 10.3 1.1 5.7 Abu Dhabi 4,673.31 0.1 (0.5) 0.1 6.2 31.20 128,923.6 12.3 1.4 5.2 Saudi Arabia 8,158.06 (0.6) (1.1) (0.6) 12.9 1,335.79 512,427.0 17.8 1.8 3.3 Kuwait 4,836.08 0.0 1.0 0.0 (3.3) 38.32 33,868.2 14.9 0.9 3.7 Oman 4,731.27 0.0 0.2 0.0 (7.2) 10.50 19,784.2 11.8 1.0 5.1 Bahrain# 1,257.88 (0.4) (0.4) (4.6) (5.5) 10.66 19,585.0 8.0 0.8 6.5 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any; # Data as of April 30, 2018) 9,000 9,050 9,100 9,150 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QSE Index declined 1.1% to close at 9,014.3. The Real Estate and Telecoms indices led the losses. The index fell on the back of selling pressure from Qatari and non-Qatari shareholders despite buying support from GCC shareholders. Ezdan Holding Group and Mesaieed Petrochemical Holding Company were the top losers, falling 6.9% and 5.3%, respectively. Among the top gainers, Qatar General Insurance & Reinsurance Company gained 4.3%, while Al Khaleej Takaful Insurance Company was up 1.9%. Volume of shares traded on Tuesday fell by 36.6% to 10.7mn from 16.9mn on Monday. Further, as compared to the 30-day moving average of 10.7mn, volume for the day was 0.5% lower. Mesaieed Petrochemical Holding Company and Vodafone Qatar were the most active stocks, contributing 30.7% and 19.2% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases Company Market Currency Revenue (mn) 1Q2018 % Change YoY Operating Profit (mn) 1Q2018 % Change YoY Net Profit (mn) 1Q2018 % Change YoY Dar Alarkan Real Estate Development Co. Saudi Arabia SR – – 436.5 349.0% 331.1 2,629.8% United Electronics Company Saudi Arabia SR – – 25.1 79.3% 21.6 66.2% Marka Dubai AED 20.4 -38.8% -2.6 N/A -8.0 N/A Emirates Driving Company Abu Dhabi AED 55.2 -5.7% – – 34.0 34.4% Arkan Building Materials Co. Abu Dhabi AED 251.0 10.0% – – 11.7 10.4% Abu Dhabi National Insurance Co. Abu Dhabi AED 1,219.2 12.8% – – 95.2 28.6% Sharjah Group Company Abu Dhabi AED 3.8 -1.4% – – 1.3 -34.6% Sharjah Cement and Industrial Development Co. Abu Dhabi AED 172.7 4.4% – – 12.2 4.6% Source: Company data, DFM, ADX, MSM, TASI, BHB. News Qatar Robust earnings expansion helps Qatar-listed companies enhance net profitability in the first quarter – Robust earnings expansion, especially in the industrials, consumer goods, banking and transport sectors, helped Qatar-listed companies better net profitability YoY in 1Q2018. Qatar’s listed companies have reported a cumulative net profit of QR10.96bn in 1Q2018 with banking and industrials together contributing more than 76% of the total net earnings. The cumulative net profitability is up 2.95% YoY in 1Q2018 compared to about 1% growth in the corresponding period of 2017, according to the Qatar Stock Exchange data. The bourse’s main 20-stock Qatar Share Index was up 0.59% during January-March this year against 0.44% decline in the comparable period of 2017. The industrials, consumer goods, banking and transport scripts were seen outperforming the main index. The industrials sector, which has nine listed constituents, witnessed 28.01% rise in net profitability to QR2.38bn compared to 7.66% increase in the year-ago period. The sector, which contributed 21.72% to the overall net profitability, was the best performer in the bourse as its index vaulted 10.18% in 1Q2018 against 0.19% fall in 2017 period. The banks and financial services sector reported 12.24% rise in cumulative net profit to QR5.95bn compared to a 4.34% growth in the comparable period of 2017. The sector, whose share was 54.29% in the overall net profitability, witnessed its index gain 4.27% in 1Q2018 against 3.4% in the year-ago period. (Gulf-Times.com) Umm Al Houl plant due to open in October – Qatar’s mega Umm Al Houl Power Plant is expected to be operational in October 2018. After completing 99% of the project works, the Qatar Electricity & Water Company (QEWS) is now involved in the final preparations before the launch of the project, according to QEWS’ General Manager and Managing Director, Fahad Bin Hamad Al Mohannadi. When the plant is completed, this project shall provide 25% of the electricity and 30% of the water needs in Qatar. Al Mohannadi also said the first phase of QEWS’ Solar project will be completed by the end of 2020. The investment in the project would range in between $500mn to $700mn. (Peninsula Qatar) QDB signs deal with five global VC firms for QR100mn SME fund – Qatar Development Bank (QDB) signed agreements with five international venture capital firms that would provide more than QR100mn worth of funding for Qatari small and medium-sized enterprises (SMEs). QDB’s CEO, Abdulaziz Bin Nasser Al Khalifa signed agreements with Iris Capital partner Alexander Wiedmer; Entrepreneurs Roundtable Accelerator (ERA) managing partner Murat Aktihanoglu; 212 Fund managing partner Numan Numan; IDG Capital partner Vineet Kapur, and AfricInvest founding partner Aziz Mebarek during the ‘QDB Investment Forum’. Al Khalifa said the total value of Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 56.07% 55.23% 1,842,837.71 Qatari Institutions 19.19% 20.15% (2,122,476.61) Qatari 75.26% 75.38% (279,638.90) GCC Individuals 1.20% 1.09% 259,799.71 GCC Institutions 3.72% 3.39% 726,572.64 GCC 4.92% 4.48% 986,372.35 Non-Qatari Individuals 10.38% 10.13% 545,941.78 Non-Qatari Institutions 9.45% 10.02% (1,252,675.23) Non-Qatari 19.83% 20.15% (706,733.45)

- 3. Page 3 of 6 the agreements exceeds QR100mn and is the first tranche of the bank’s $100mn ‘Fund of Fund’ initiative launched more than a year ago. He said FoF is the process of yellow service investing into VC funds to get exposure to major international companies, bring them potentially to Qatar, set up their offices here, ensure that they actively contribute to the entrepreneurial ecosystem, and ensure sufficient liquidity and help Qatar startups scale up globally. (Gulf-Times.com) Qatar Central Bank sells QR1.5bn of Treasury bills – Qatar Central Bank sold QR1.5bn of Treasury bills. It sold QR900mn of three-month bills at a yield of 2.49%, QR400mn of six-month bills with 2.69% yield, and QR200mn of nine-month bills at 2.84%. Last month, the central bank sold QR550mn of three- month bills at a yield of 2.65%, QR300mn of six-month bills with 2.8% yield, and QR150mn of nine-month bills at 3%. Qatar Central Bank’s international reserves and foreign currency liquidity edged up in March, official data showed. The reserves and liquidity, a measure of the central bank’s ability to support the Riyal currency, rose to $37.8bn last month from $37.6bn in February. (Zawya, Reuters) MDPS: Qatar’s nominal GDP rises 9.4% to QR160.88bn in 4Q2017 – Qatar’s gross domestic product (GDP) at current prices, or nominal GDP, increased 9.4% to QR160.88bn in 4Q2017 compared with QR147.04bn in the same quarter a year ago, according to the 23rd issue of the quarterly publication, ‘Window on Economic Statistics of Qatar’, by released by Ministry of Development Planning and Statistics (MDPS). When compared to previous quarter’s revised estimate of QR152.21bn, the report stated, the nominal GDP saw an increase of 5.7%. The quarterly GDP at constant (2013) prices, or real GDP, in the fourth quarter of 2017 stood at QR204.22bn, a growth of 1.8% compared with the estimated QR200.69bn in the same quarter in the previous year. However, the report stated, compared with the previous quarter’s revised estimate of QR209.0bn, real GDP in 4Q2017, registered a decrease of 2.3%. According to MDPS, the consumer price index (CPI) for the fourth quarter of 2017, showed an increase of 0.3% when compared to the previous quarter, and 0.3% decrease when compared to the corresponding quarter of 2016. (Qatar Tribune) Qatar PMI points to economic resilience – Qatar Financial Centre is set to officially release the first Qatar PMI on May 3, 2018. The newly launched report, compiled by IHS Markit, will provide an important source of timely information on the health of Qatar’s economy. Indeed, the Qatar PMI data collected since April 2017 reveals the resilience of the non-oil private sector over the past year, which is in line with the statistics released by the Ministry of Development Planning and Statistics (MDPS). The economy regained growth momentum at a remarkable pace following the deterioration in business conditions. The Qatari economy has weathered the challenges with strength and resilience, due to swift government responses. The deterioration in business conditions due to the embargo remained as transitory and new trade routes were quickly established. The situation has acted as a catalyst for enhancing domestic food production and reducing reliance on a small group of countries, as pointed by the IMF in the recent Article IV mission statement. (Peninsula Qatar) Italian chambers in Asian markets eye Qatari investments – Italian chambers of commerce based in Asia, South Africa and the Gulf region are encouraging the Qatari private sector to explore investment opportunities in various markets in Asia, particularly in the construction and food industry. The President of the Italian Chamber of Commerce in Qatar, Sheikh Mohamed Bin Faisal Bin Qassim Al Thani, said Asia is a vibrant market that could provide Qatar with new sources investments and partnerships. Further, Bilateral trade between Qatar and Italy grew almost 9% to €2.35bn in 2017 compared with the volume of bilateral trade between the two countries in the previous year, according to Carlotta Colli, Deputy Head of Mission at the Embassy of Italy in Qatar. Addressing the Qatar Asia Business Insight networking event, Colli said the growing trade volume despite the ongoing economic blockade of Qatar by some of its neighboring countries shows the mutual trust between the two countries. (Gulf-Times.com, Qatar Tribune) International US factory activity slows in April – US factory activity slowed for a second straight month in April, with manufacturers complaining about rising commodity prices in the wake of the Trump administration’s tariffs on steel and aluminum imports. The ISM said its index of national factory activity dropped to a reading of 57.3 last month from 59.3 in March. A reading above 50 in the ISM index indicates growth in manufacturing, which accounts for about 12% of the US economy. (Reuters) UK’s factory growth sinks to 17-month low in April – British manufacturing growth slid to a 17-month low in April, sending sterling sinking and further reducing the chances of an interest rate hike by the Bank of England next week. Markit/CIPS UK Manufacturing Purchasing Managers’ Index (PMI) dropped a full point to 53.9 in March, below the average forecast of 54.8 in a Reuters poll of economists. IHS Markit satted weakness centered especially on producers of consumer goods who have been hit by the reduced spending power among households caused by last year’s rise in inflation. (Reuters) PMI: Japan’s April services activity grows fastest in six months – Activity in Japan’s services sector expanded at the fastest pace in six months in April as new orders picked up, a private survey showed, suggesting the economy got off to a strong start in the second quarter. However, the survey also showed a dip in business confidence as companies struggle to hire workers amid a labor shortage. The Markit/Nikkei Japan Services Purchasing Managers Index (PMI) rose to 52.5 in April on a seasonally adjusted basis from 50.9 in March. (Reuters) India’s infrastructure output growth slows to three-year low in 2017-18 – India’s infrastructure growth slowed to a three-year low of 4.2% in the fiscal year ending in March, indicating Prime Minister Narendra Modi faces a tough challenge to boost investment ahead of general elections due early next year. Annual output growth was 4.2% during the 2017-18 fiscal year that ended in March, lower than 4.8% in the previous year, and dragged down by slower growth in the production of coal, steel and electricity, according to data released by the Ministry of Commerce and Industry. (Reuters) Regional IMF: Need for MENAP to integrate – The International Monetary Fund (IMF) said that there is a strong need for the

- 4. Page 4 of 6 countries across the MENAP (Middle East, North Africa, Afghanistan, and Pakistan) to integrate further into the global economy and diversify their products and services. This will require greater access to finance for the private sector, especially small and medium-sized enterprises and upgrading workforce skills. The IMF’s Regional Outlook released noted uncertainty surrounding oil prices, rising trade tensions, and the effects of ongoing conflicts and their spillovers have further constrained the region’s growth and remain risks going forward. “To take full advantage of the growing global economy, the region should accelerate key economic reforms. The focus should be on improving the investment climate, boosting productivity, and strengthening governance,” said Jihad Azour, Director of the IMF’s Middle East and Central Asia Department. High or rapidly increasing debt levels have forced countries to take significant measures to reduce deficits, by limiting government spending or mobilizing revenue. (Peninsula Qatar) Citigroup sees MENA syndicated loans at more than $70bn – The resurgence in syndicated loans in the Middle East and North Africa (MENA) seems set for a slowdown as the deal pipeline dries up, according to Citigroup Inc. Loans in the region have rose 85% in 2018 to $33.4bn, helped by a jumbo $16bn issue from Saudi Arabia, according to Bloomberg. Overall volume will probably climb to more than $70bn, according to Zain Zaidi, a Director for loans and acquisition finance at Citigroup, the region’s biggest loan arranger. Syndicated loans in MENA had fell 30% in 2017 to $82.9bn. (GulfBase.com) RJHI posts 7.3% YoY rise in net profit to SR2,383mn in 1Q2018 – Al Rajhi Bank (RJHI) recorded net profit of SR2,383mn in 1Q2018, an increase of 7.3% YoY. Total operating income rose 7.5% YoY to SR4,142mn in 1Q2018. Total assets stood at SR349.24bn at the end of March 31, 2018 as compared to SR337.23bn at the end of March 31, 2017. Loans and advances stood at SR229.04bn (-0.2% YoY), while customer deposits stood at SR283.94bn (4.7% YoY) at the end of March 31, 2018. EPS came in at SR1.47 in 1Q2018 as compared to SR1.37 in 1Q2017. (Tadawul) Saudi Arabia’s ICT spend to reach $40bn this year – Saudi Arabia’s digital transformation continues to burgeon with reports showing that the Kingdom’s ICT spend grew 6% in 2017 to over $36bn and is predicted to expand further this year to reach the value of $40bn. With the pace of KSA’s digitization continuing in rapid acceleration, Trend Micro, a global leader in cyber security solutions, emphasized the need for a modernized, integrated and secured system, noting the serious privacy and security challenges that come with a vast web of interconnected technologies. (GulfBase.com) UAE’s FDI outflow hits $16bn in 2016 – The total foreign direct investment (FDI) outflow from the UAE reached $16bn in 2016, ranking it 23 in the world in terms of FDI outflow and the first in the Middle East, making it a net capital exporting country in the world, said a top official. Jamal Al-Jarwan, Secretary- General of the UAE International Investors Council (UAEIIC) added that the UAEIIC is playing an instrumental role in bridging the gap between public and private sector as well as spearheading UAE’s investment in other countries. FDI flow in to the UAE reaches $10.3bn in 2017, up from $9.6bn in 2016, according to the UAE Competitiveness and Statistics Authority. (GulfBase.com) Non-oil trade between Japan, UAE touches $15bn in 2017 – Non-oil trade between the UAE and Japan has grown by 8.4% in 2017 and the two countries are focusing on strengthening ties in various sectors, UAE Economy Minister Sultan Bin Saeed Al Mansouri said. The non-oil trade between Japan and UAE touched $15bn in 2017 with a growth of 8.4% over 2016 and the average growth of non-oil trade between the two countries during the past five years reached about 2.5%. “The rates are excellent, but in my opinion does not proceed in parallel with the strength of the two countries, not keep pace with the strength of trade and investment ties between them. That means there are a lot of opportunities and possibilities to develop our economic cooperation that we did not benefit from earlier,” said Al Mansouri. (GulfBase.com) London judge orders Dana Gas to hold dividends in English bank account – A London judge ordered Dana Gas to pay any dividends into an English bank account where the funds must be held until a dispute over its $700mn Islamic bond is resolved, sources said. Friday’s ruling is the latest twist in a complex legal battle taking place in courts in London and the UAE, which began last year when the UAE energy producer halted payments on $700mn of Islamic bonds it said, had become unlawful because of changes in Islamic finance. Holders of the Sukuk contest its position and are demanding to be paid by Dana Gas, which declined to comment on the ruling. (Gulf- Times.com) Warba Bank’s net profit rises to KD2.92mn in 1Q2018 – Warba Bank recorded net profit of KD2.92mn in 1Q2018 as compared to KD1.36mn in 1Q2017. Net operating profit came in at KD6.86mn as compared to KD3.80mn in 1Q2017. Total assets stood at KD1.84bn at the end of March 31, 2018 as compared to KD1.32bn at the end of March 31, 2017. EPS came in at KD0.00048 in 1Q2018 as compared to KD0.00136 in 1Q2017. (Reuters) Commercial Bank of Kuwait’s net profit sharply rises to KD10.07mn in 1Q2018 – Commercial Bank of Kuwait’s recorded net profit of KD10.07mn in 1Q2018 as compared to KD0.80mn in 1Q2017. Net operating profit came in at KD26.66mn as compared to KD28.95mn in 1Q2017. Total assets stood at KD4.29bn at the end of March 31, 2018 as compared to KD4.27bn at the end of March 31, 2017. EPS came in at KD0.0062 in 1Q2018 as compared to KD0.0005 in 1Q2017. (Reuters) Oman, Kuwait to start work on $7bn refinery – Oman Oil Company and Kuwait Petroleum Corporation jointly laid the foundation stone for the $7bn Duqm Refinery project in Oman. Duqm Refinery will bolster the production of diesel, jet fuel, naphtha, Liquid Petroleum Gas (LPG), sulfur and pet coke as its primary products. It also seeks advanced technology to manufacture clean, high-quality products in compliance with global standards for safety and the highest operational standards. (GulfBase.com) Omran explores setting up REIT in Oman – Oman Tourism Development Company (Omran) is weighing plans to set up a Real Estate Investment Trust (REIT) designed to enable local and international investors to invest in its expanding portfolio

- 5. Page 5 of 6 of hospitality assets. Omran’s CEO, Peter Walichnowski said, “We are exploring funds management at the moment, which is how to take (Omran’s) hotel assets and securitize them and put them into an investment vehicle to allow the public and investors to participate in the hospitality portfolio.” (GulfBase.com) Alba closes $247mn export credit financing deal – Aluminium Bahrain (Alba) successfully closed the first part of the second tranche of $247.01mn Export Credit Agency (ECA) covered financing facilities. It will finance the green anode plant, gas treatment centers, pot tending machines and anode bake furnace as well as related equipment for Alba’s Line 6 Expansion Project, said a statement. Alba’s Chairman of board of directors, Shaikh Daij Bin Salman Bin Daij Al Khalifa said, “We are extremely pleased with the support received from our banking partners in the ECA-covered facilities. Their commitment is a vote of confidence in Bahrain, Alba and its landmark project – Line 6 Expansion Project. We also look forward to secure the final part of second ECA-tranche as we progress with the construction of Line 6 Expansion Project.” (GulfBase.com) Goldman Sachs: Qatar, Saudi Arabia, Abu Dhabi, Oman valuations are attractive – Sovereign bonds of countries such as Qatar, Saudi Arabia, Abu Dhabi and Oman have relatively steep curves and attractive valuations, while underperformance of those in oil-exporting Middle East may have been driven by increased issuance this year amid escalating geopolitical risk, according to Goldman Sachs. Several emerging-market sovereign bonds are inexpensive based on company’s model, partly reflecting market developments since February and IMF forecast revisions, this is especially the case for Middle East that has underperformed other regions in recent risk-off period and where IMF expects macro risk will decline next year following higher oil prices. Oman in particular stands to benefit from higher oil prices, predicted by IMF, although the risk of downgrade to sub-investment grade remains. (Bloomberg)

- 6. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mohamed Abo Daff QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mohd.abodaff@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg ( # Data as of April 30, 2018) Source: Bloomberg ( # Market closed on May 1, 2018) Source: Bloomberg (*$ adjusted returns; # Market closed on May 1, 2018) 60.0 80.0 100.0 120.0 140.0 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18 QSE Index S&P Pan Arab S&P GCC (0.6%) (1.1%) 0.0% (0.4%) 0.0% 0.1% (1.1%)(1.5%) (1.0%) (0.5%) 0.0% 0.5% SaudiArabia Qatar Kuwait Bahrain# Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,303.91 (0.9) (1.5) 0.1 MSCI World Index 2,083.77 (0.1) (0.6) (0.9) Silver/Ounce 16.17 (1.0) (2.1) (4.6) DJ Industrial 24,099.05 (0.3) (0.9) (2.5) Crude Oil (Brent)/Barrel (FM Future) 73.13 (2.7) (2.0) 9.4 S&P 500 2,654.80 0.3 (0.6) (0.7) Crude Oil (WTI)/Barrel (FM Future) 67.25 (1.9) (1.2) 11.3 NASDAQ 100 7,130.70 0.9 0.2 3.3 Natural Gas (Henry Hub)/MMBtu 2.77 0.7 (1.8) (21.7) STOXX 600 385.03 (0.8) (0.7) (1.1) LPG Propane (Arab Gulf)/Ton 90.75 (6.0) 3.7 (8.3) DAX# 12,612.11 0.0 0.2 (1.7) LPG Butane (Arab Gulf)/Ton 88.50 2.6 2.3 (18.4) FTSE 100 7,520.36 (0.9) (0.8) (1.4) Euro 1.20 (0.7) (1.1) (0.1) CAC 40# 5,520.50 0.0 0.6 4.6 Yen 109.86 0.5 0.7 (2.5) Nikkei 22,508.03 (0.3) (0.3) 1.6 GBP 1.36 (1.1) (1.2) 0.7 MSCI EM 1,162.48 (0.2) 0.5 0.3 CHF 1.00 (0.6) (0.9) (2.2) SHANGHAI SE Composite# 3,082.23 0.0 0.0 (4.3) AUD 0.75 (0.5) (1.2) (4.1) HANG SENG# 30,808.45 0.0 1.7 2.5 USD Index 92.45 0.7 1.0 0.4 BSE SENSEX# 35,160.36 0.0 0.5 (1.1) RUB# 62.97 0.0 1.3 9.3 Bovespa# 86,115.50 0.0 (0.9) 6.9 BRL 0.29 (0.0) (1.4) (5.6) RTS# 1,153.96 0.0 (1.1) (0.0) 83.9 83.6 75.7