QNBFS Daily Market Report July 05, 2018

•

0 gostou•154 visualizações

The QSE Index rose 0.5% to close at 9,230.6

Recomendados

Recomendados

Mais conteúdo relacionado

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

QNBFS Daily Market Report July 05, 2018

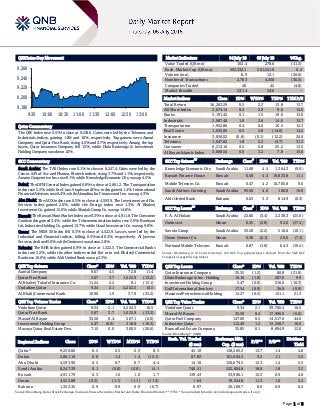

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.5% to close at 9,230.6. Gains were led by the Telecoms and Industrials indices, gaining 1.8% and 1.0%, respectively. Top gainers were Aamal Company and Qatar First Bank, rising 4.5% and 3.7%, respectively. Among the top losers, Qatar Insurance Company fell 1.2%, while Dlala Brokerage & Investment Holding Company was down 1.0%. GCC Commentary Saudi Arabia: The TASI Index rose 0.1% to close at 8,247.4. Gains were led by the Comm. & Prof. Svc and Pharma, Biotech indices, rising 3.7% and 1.1%, respectively. Amana Cooperative Ins. rose 9.1%, while Knowledge Economic City was up 4.5%. Dubai: The DFM General Index gained 0.8% to close at 2,861.2. The Transportation index rose 2.2%, while the Cons. Staples and Disc. index gained 1.4%. International Financial Advisors rose 6.4%, while Almadina for Finance and Inv. was up 4.3%. Abu Dhabi: The ADX index rose 0.5% to close at 4,593.9. The Investment and Fin. Services index gained 2.6%, while the Energy index rose 1.3%. Al Khaleej Investment Co. gained 15.0%, while Sharjah Group Co. was up 14.8%. Kuwait: The Kuwait Main Market Index rose 0.3% to close at 4,911.8. The Consumer Goods index gained 3.4%, while the Telecommunication index rose 2.9%. Boubyan Int. Industries Holding Co. gained 13.7%, while Osoul Investment Co. was up 9.8%. Oman: The MSM 30 Index fell 0.3% to close at 4,522.9. Losses were led by the Industrial and Financial indices, falling 0.5% and 0.4%, respectively. Al Jazeera Services declined 5.0%, while Ominvest was down 2.8%. Bahrain: The BHB Index gained 0.9% to close at 1,322.5. The Commercial Banks index rose 2.2%, while the other indices ended flat or in red. Khaleeji Commercial Bank rose 10.0%, while Ahli United Bank was up 3.3%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Aamal Company 9.67 4.5 72.8 11.4 Qatar First Bank 5.67 3.7 1,025.9 (13.2) Al Khaleej Takaful Insurance Co. 11.24 2.2 8.1 (15.1) Vodafone Qatar 9.34 2.1 4,252.3 16.5 Al Khalij Commercial Bank 10.90 1.9 37.9 (23.2) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 9.34 2.1 4,252.3 16.5 Qatar First Bank 5.67 3.7 1,025.9 (13.2) Masraf Al Rayan 35.50 0.4 507.1 (6.0) Investment Holding Group 5.47 (0.9) 316.0 (10.3) Mazaya Qatar Real Estate Dev. 7.15 0.0 300.5 (20.6) Market Indicators 04 July 18 03 July 18 %Chg. Value Traded (QR mn) 163.4 278.6 (41.3) Exch. Market Cap. (QR mn) 503,332.1 501,541.0 0.4 Volume (mn) 8.9 12.1 (26.6) Number of Transactions 2,763 4,350 (36.5) Companies Traded 40 42 (4.8) Market Breadth 23:14 34:6 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 16,263.29 0.5 2.3 13.8 13.7 All Share Index 2,674.14 0.4 2.0 9.0 14.0 Banks 3,191.43 0.1 1.5 19.0 13.0 Industrials 2,987.48 1.0 3.6 14.0 15.7 Transportation 1,952.86 0.4 0.6 10.5 12.3 Real Estate 1,635.06 0.5 2.8 (14.6) 14.2 Insurance 3,056.02 (0.8) (0.1) (12.2) 26.0 Telecoms 1,047.02 1.8 3.2 (4.7) 31.3 Consumer 6,213.16 0.5 0.8 25.2 13.5 Al Rayan Islamic Index 3,688.54 0.8 3.2 7.8 15.0 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Knowledge Economic City Saudi Arabia 11.68 4.5 1,364.3 (9.0) Kuwait Finance House Kuwait 0.58 4.3 19,833.8 11.1 Mobile Telecom. Co. Kuwait 0.47 4.2 10,785.8 9.0 Saudi Airlines Catering Saudi Arabia 95.50 4.0 100.8 19.0 Ahli United Bank Bahrain 0.63 3.3 814.9 (6.3) GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% F. A. Al Hokair Saudi Arabia 22.80 (3.4) 2,238.3 (25.0) Ominvest Oman 0.35 (2.8) 92.0 (17.4) Savola Group Saudi Arabia 35.50 (2.2) 516.6 (10.1) Oman Cement Co. Oman 0.38 (2.1) 20.0 (7.3) National Mobile Telecom. Kuwait 0.87 (1.8) 64.3 (19.4) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Insurance Company 35.35 (1.2) 80.8 (21.8) Dlala Brokerage & Inv. Holding 16.16 (1.0) 267.0 9.9 Investment Holding Group 5.47 (0.9) 316.0 (10.3) Gulf International Services 17.54 (0.9) 36.9 (0.9) Mesaieed Petrochemical Holding 15.27 (0.5) 151.1 21.3 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Vodafone Qatar 9.34 2.1 39,766.4 16.5 Masraf Al Rayan 35.50 0.4 17,996.9 (6.0) Qatar Fuel Company 147.00 0.5 14,517.6 44.0 Industries Qatar 112.49 1.2 13,296.7 16.0 Barwa Real Estate Company 35.85 0.1 8,894.9 12.0 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,230.60 0.5 2.3 2.3 8.3 45.10 138,265.3 13.7 1.4 4.8 Dubai 2,861.16 0.8 1.4 1.4 (15.1) 67.82 101,884.2 9.2 1.1 5.9 Abu Dhabi 4,593.90 0.5 0.7 0.7 4.4 14.16 126,674.5 12.3 1.4 5.2 Saudi Arabia 8,247.39 0.1 (0.8) (0.8) 14.1 746.51 522,804.8 18.6 1.8 3.3 Kuwait 4,911.79 0.3 1.0 1.0 1.7 139.43 33,986.1 15.3 0.9 4.0 Oman 4,522.88 (0.3) (1.1) (1.1) (11.3) 1.64 19,044.8 11.3 1.0 5.4 Bahrain 1,322.45 0.9 0.9 0.9 (0.7) 6.97 20,189.7 8.6 0.9 6.2 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,180 9,200 9,220 9,240 9,260 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QSE Index rose 0.5% to close at 9,230.6. The Telecoms and Industrials indices led the gains. The index rose on the back of buying support from Qatari and non-Qatari shareholders despite selling pressure from GCC shareholders. Aamal Company and Qatar First Bank were the top gainers, rising 4.5% and 3.7%, respectively. Among the top losers, Qatar Insurance Company fell 1.2%, while Dlala Brokerage & Investment Holding Company was down 1.0%. Volume of shares traded on Wednesday fell by 26.6% to 8.9mn from 12.1mn on Tuesday. Further, as compared to the 30-day moving average of 11.5mn, volume for the day was 22.6% lower. Vodafone Qatar and Qatar First Bank were the most active stocks, contributing 47.9% and 11.6% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Global Economic Data and Earnings Calendar Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 07/04 US Mortgage Bankers Association MBA Mortgage Applications 29-June -0.5% – -4.9% 07/04 EU Markit Markit Eurozone Services PMI June 55.2 55.0 55.0 07/04 EU Markit Markit Eurozone Composite PMI June 54.9 54.8 54.8 07/04 Germany Markit Markit Germany Services PMI June 54.5 53.9 53.9 07/04 France Markit Markit France Services PMI June 55.9 56.4 56.4 07/04 France Markit Markit France Composite PMI June 55.0 55.6 55.6 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 2Q2018 results No. of days remaining Status QNBK QNB Group 11-Jul-18 6 Due QGTS Qatar Gas Transport Company Limited (Nakilat) 11-Jul-18 6 Due QIBK Qatar Islamic Bank 15-Jul-18 10 Due MARK Masraf Al Rayan 16-Jul-18 11 Due WDAM Widam Food Company 17-Jul-18 12 Due ERES Ezdan Holding Group 17-Jul-18 12 Due QEWS Qatar Electricity & Water Company 18-Jul-18 13 Due UDCD United Development Company 18-Jul-18 13 Due CBQK The Commercial Bank 18-Jul-18 13 Due GWCS Gulf Warehousing Company 19-Jul-18 14 Due QIIK Qatar International Islamic Bank 19-Jul-18 14 Due IHGS Islamic Holding Group 19-Jul-18 14 Due KCBK Al Khalij Commercial Bank 19-Jul-18 14 Due ABQK Ahli Bank 19-Jul-18 14 Due DHBK Doha Bank 19-Jul-18 14 Due QNCD Qatar National Cement Company 23-Jul-18 18 Due DBIS Dlala Brokerage & Investment Holding Company 25-Jul-18 20 Due QIMD Qatar Industrial Manufacturing Company 26-Jul-18 21 Due NLCS Alijarah Holding 26-Jul-18 21 Due ORDS Ooredoo 29-Jul-18 24 Due DOHI Doha Insurance Group 31-Jul-18 26 Due AKHI Al Khaleej Takaful Insurance Company 3-Aug-18 29 Due Source: QSE Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 50.29% 56.40% (9,988,010.92) Qatari Institutions 25.87% 17.37% 13,903,277.91 Qatari 76.16% 73.77% 3,915,266.99 GCC Individuals 0.67% 2.53% (3,043,180.23) GCC Institutions 1.19% 3.63% (3,987,894.88) GCC 1.86% 6.16% (7,031,075.11) Non-Qatari Individuals 10.90% 11.82% (1,501,916.40) Non-Qatari Institutions 11.08% 8.25% 4,617,724.52 Non-Qatari 21.98% 20.07% 3,115,808.12

- 3. Page 3 of 6 News Qatar Qatar’s central bank sold QR800mn of Treasury bills – Qatar’s central bank sold QR800mn of Treasury bills in its monthly auction, with yields dropping from the previous sale, the bank stated. It sold QR400mn of three-month bills at 2.26%, QR200mn of six-month at 2.56% and QR200mn of nine-month at 2.79%. (Zawya) QIMD to disclose its semi-annual financials on July 26 – Qatar Industrial Manufacturing Company (QIMD) announced that it will disclose its semi-annual financial reports for the period ending June 30, 2018 on July 26, 2018. (QSE) GWCS to disclose its semi-annual financials on July 19 – Gulf Warehousing Company (GWCS) announced that it will disclose its semi-annual financial reports for the period ending June 30, 2018 on July 19, 2018. (QSE) QISI to disclose its semi-annual financials on July 30 – Qatar Islamic Insurance Company (QISI) announced that it will disclose its semi-annual financial reports for the period ending June 30, 2018 on July 30, 2018. (QSE) Ahli Bank files legal suit against Investment Holding Group – Investment Holding Group announced that, Ahli Bank Qatar has filed a legal case amount of QR178,529,133.61 against Investment Holding Group and a group of defendants, all being guarantors of bank facilities for Doha Convention Center project, executed by the Joint Venture of Debbas Contracting Qatar and ETA Star Engineering and Contracting, being the ‘Sub-Contractor’; where Investment Holding Group share is 25.5%. (QSE) Doha Insurance Group opens a representative office in Beirut, Lebanon – Doha Insurance Group announced that it obtained final approval from Qatar Central Bank to establish a representative office in Beirut, Lebanon under the name of ‘Mena Re Life’ to extend the Group’s reinsurance reach in the international arena. It is part of the Doha Insurance Group’s strategy of geographic expansion to open new markets and build on its strong credit and financial rating. (QSE) QFC: Private sector output, jobs creation boost non- hydrocarbons sector – Solid output growth in the private sector and job creation as well as falling average cost burden helped Qatar report improvement in business conditions within the non-hydrocarbons sector, according to the Qatar Financial Center (QFC). Price discounting and promotional activity continued to stimulate client demand, which in turn led to higher output requirements across the non-hydrocarbon sector. Furthermore, job creation was the “joint-fastest amid strong business confidence”, stated the QFC’s Qatar PMI (Purchasing Managers’ Index). The survey, compiled for QFC by IHS Markit, has been conducted since April 2017 and provides an early indication of the operating conditions in Qatar. The headline seasonally adjusted QFC PMI, a composite gauge designed to give a single-figure snapshot of operating conditions in the non- oil and gas private sector, softened to 51.8 in June compared to 52.4 in May. (Gulf-Times.com) QCB sees rapid increase in QDB’s high-quality capital – The total assets of Qatar Development Bank (QDB) increased to QR10.2bn in 2017, from QR9bn recorded a year ago. As in the previous year, the increase in total assets during 2017 was largely due to growth in credit facilities and increase in placements of its funds with the banks, according to Qatar Central Bank (QCB). Fully owned by the government, QDB is not profit oriented. It aims to make Qatari SMEs globally competitive through financing, developing skills and capabilities; and promoting exports. Commenting on QDB’s 2017 performance, QCB noted in its latest ‘Financial Stability Review’ that QDB continued to contribute to the diversification of the Qatar economy, through facilitation of development of SMEs during the year. With renewed thrust on diversification of the economy and growth of SMEs, the balance sheet of QDB has been recording rapid expansion in the past few years. The momentum of expansion was maintained during 2017. (Peninsula Qatar) IBQ’s net profit jumps 12% to QR313mn in 1H2018 – International Bank of Qatar (IBQ) posted QR313mn net profit in 1H2018, or 12% growth compared to the same period last year. Delivering a strong overall performance, IBQ stated that net operating income jumped by 8% to reach QR464mn, while total assets increased by 14% or QR33.6bn compared to the same period in 2017. Similarly, customer loans and advances grew by 3% to QR22bn, and customers’ deposits were up 11% at QR21.5bn, while cost income ratio improved to 32.6% from 34.9%, and total expenses only grew to 1%. (Gulf-Times.com) Real estate trading volume in Qatar exceeds QR470mn in a week – The trading volume of registered real estate’s between June 24 to June 28 at the Ministry of Justice’s real estate registration department stood at QR470,480,147. The department’s weekly report noted that the trading included empty lands, residential units, multipurpose buildings, empty multipurpose lands, residential complex and building. Most of the trading took place in Doha, Umm Salal, Al Rayyan, Al Daayen, Al Shamal, Al Khor, Al Thakhira and Al Shahaniya. (Gulf-Times.com) Qatari Venture wins approval for almost 1,000 London homes – Qatari Diar Real Estate Investment Co. venture won approval to build almost 1,000 homes in the UK capital’s Elephant and Castle district. Southwark Council approved the revised plans to replace a shopping mall with apartment towers, a new college campus and stores. Investor Delancey, Dutch pension fund APG Asset Management NV and the Qatari sovereign- wealth fund’s property development unit will develop the project using their firm ‘Get Living’. (Bloomberg) International UK’s economy picks up speed, raising chance of rate rise – Britain’s large services industry grew last month at its fastest rate since October, a survey showed, and prompting investors to increase bets that Bank of England will raise interest rates next month. After a weak first four months of 2018, the IHS Markit/CIPS services Purchasing Managers’ Index (PMI) rose to 55.1 in June, easily beating economists’ average forecasts in a Reuters poll of 54.0, unchanged from May’s reading. June surveys this week for the smaller manufacturing and construction sectors also beat expectations. Taken together, the three PMIs point to overall economic growth of 0.4% in the second quarter, double the pace of the first, IHS Markit stated. Sterling rallied and British government bond yields rose as

- 4. Page 4 of 6 financial markets priced in a greater chance that the Bank of England will raise interest rates to 0.75% from the 0.5% they have stood at for most of the past decade. (Reuters) Eurozone business activity picked up in June but doubts linger – Eurozone business growth accelerated in June, offering encouragement to European Central Bank to tighten policy, but optimism among purchasing managers was at its lowest ebb since late 2016, a survey found. Faster growth across the currency union, alongside rising price pressures, will reassure ECB policymakers who last month said the bank would shut its hallmark bond purchase scheme by the end of the year. But in a balanced announcement reflecting uncertainties hanging over the economy, the ECB signaled on June 14 that any interest rate hike was still distant. Britain provided a similar story of stronger growth. Its large services industry grew last month at its fastest rate since October, suggesting the economy might be strong enough for the Bank of England to raise rates in August, as expected. (Reuters) German services sector growth rebounds in June – Growth in Germany’s services sector accelerated to the highest level in four months in June, a survey showed, adding to signs that consumption is fuelling an upswing in Europe’s largest economy as exports weaken. Markit’s final services Purchasing Managers’ Index (PMI) rose to 54.5 from 52.1 in May, which was a 20-month low. The figure was higher than a flash reading of 53.9 but still below a near-seven-year high in January. Markit put the rebound down to stronger new orders underpinned by higher domestic demand. To meet the higher demand, service providers hired new workers at the highest rate since January. Markit’s PMI for manufacturing, which accounts for about a fifth of the German economy, fell to 55.9 from 56.9 in May, data showed. The fall was attributed to manufacturing export sales and new orders growing at their slowest pace in more than two years. This signaled the sector was cooling as fears of a full- blown global trade war cloud the economic outlook. The rebound in services more than compensated for the slower growth in manufacturing. (Reuters) French business growth picks up after slowest quarter since 2016 – French private sector activity picked up in June, helped by a rebound in the services sector that more than offset a further slowdown in manufacturing, a survey showed. Data compiler IHS Markit stated its Purchasing Managers’ Index (PMI) for services rose in June to 55.9 from 54.3 in May, lower than a preliminary reading of 56.4. The index rose further above the 50-point threshold dividing an expansion in activity from a contraction. IHS Markit’s overall PMI index, which includes the services and manufacturing sectors, rose to 55.0 from 54.2 in May, again slightly below the 55.6 originally reported. (Reuters) Regional IATA: Middle Eastern carriers’ freight volumes grow 2.4% YoY in May – Middle Eastern carriers’ freight volumes grew 2.4% YoY in May, International Air Transport Association (IATA) stated in a report. This was a significant deceleration in demand of over 6.9% the previous month. The decrease mainly reflects developments from a year ago rather than a substantive change in the current freight trend, IATA stated. Seasonally-adjusted freight volumes continue to trend upwards at a comparatively modest pace by the region’s standards. This is consistent with signs of a broader moderation in global trade. (Gulf-Times.com) Saudi Arabia’s PIF takes 15.2% direct stake in ACWA Power – Saudi Arabia’s sovereign wealth fund, Public Investment Fund (PIF), has taken a 15.2% direct stake in ACWA Power, a developer and operator of power and water plants. The PIF already owns a 9.8% stake in ACWA through a subsidiary, Sanabil Direct Investments Company, bringing its total shareholding in the company to 25%. “The investment will be in the form of a capital increase and proceeds will be used to support ACWA Power’s growth strategy and investment plan,” PIF stated. (Reuters) Saudi Arabia’s cement sector to see revenue drop in 2Q2018 – Saudi Arabia’s cement sector is expected to witness a drop in revenue in 2Q2018, according to a report by Al Rajhi Capital. The companies under Al Rajhi’s coverage are expected to report a ~6% YoY decline in revenue, whereas earnings are likely to fall by ~10% YoY. The cement sector’s sales volume declined 16.7% YoY in the first two months of 2Q2018, which is due to restructuring in the industry and the seasonality effect (summer, Ramadan month and holidays). (GulfBase.com) UAE, Saudi Arabia’s non-oil growth accelerates to six-month high – The health of the non-oil private sectors of both the UAE and Saudi Arabia improved at the fastest pace in 2018 during June, buoyed by strong inflows of new business and output growth, stated Emirates NBD in its PMI survey. In the UAE, promotional activity helped to stimulate client demand, reflected by new order books expanding at the fastest pace since December last year. Despite firms ramping up output, backlogs of work built up at a record pace. Meanwhile, input price inflation further softened from the peak seen in January. However, in Saudi Arabia, an upturn in output and new order growth were the key components behind the latest expansion. Furthermore, many panel respondents noted sharper capacity pressures, which led to the fastest build-up in backlogs of work in 11 months. In terms of inflation, both input and output price pressures remained subdued in the context of historical data. (GulfBase.com) Top-end UAE’s industrial-zone rents resist real estate downturn – Rents in the UAE’s most well-known industrial zones such as Jebel Ali Freezone (Jafza) or Khalifa Industrial Zone Abu Dhabi (Kizad) remained resilient in the face of a wider market downturn, according to a report. While rents in lower- end stock have seen a significant fall over the 12 months to the first quarter of this year, the cost of renting stock in the higher- end market has risen. The decline in lower-end stock rents range from 5.4% to 13.7% in 1Q2018 compared to the same time period last year, according to analysts. (GulfBase.com) ICAEW: Growth seen at 2.4% in Kuwait – According to Institute of Chartered Accountants in England and Wales’ (ICAEW) report, Kuwait economy is on track to recover from a difficult year in 2017, when growth contracted by 2.7%. Overall, Kuwait’s GDP growth is expected to rebound to 2.4% in 2018 and stabilize around 3% in 2020-2021. However, ICAEW is concerned about the negative effects of the ongoing dispute between government and parliament. (GulfBase.com) Oman’s economy to grow faster this year and next as energy exports rise – Oman’s economy is expected to grow faster this

- 5. Page 5 of 6 year and the next as rising oil and gas production boosts exports while the government increases investments in the non-oil sector to diversify hydrocarbons-revenue. GDP, adjusted for inflation is set to accelerate to 2.8% in 2018 and 3.5% next year, from 0.4% in 2017, according to a report by BMI. “The rising price of oil will offer upsides to fiscal revenues, boosting government consumption. Economic diversification efforts will continue apace and generate considerable investment in manufacturing, logistics and tourism,” the report stated. (GulfBase.com) CBO issues treasury bills worth OMR45mn – Central Bank of Oman (CBO) raised OMR45mn by way of allotting treasury bills. The treasury bills are for a maturity period of 91 days, from July 4, 2018 to October 3, 2018. The average accepted price reached 99.565 for every OMR100, and the minimum accepted price arrived at 99.420 per OMR100. Whereas the average discount rate and the average yield reached 1.744% and 1.752%, respectively. The interest rate on the Repo operations with CBO is 2.6% for the period from July 3, 2018 to July 9, 2018 while the discount rate on Treasury Bills Discounting Facility with CBO is 3.35% for the same period. (GulfBase.com) Bahrain-origin exports hit BHD181mn in May – The value of Bahrain-origin exports reached BHD181mn during May versus BHD189mn for the same month of the previous year, marking a 4% decrease, stated the Information & eGovernment Authority (iGA) in its foreign trade report. The top ten countries account for 86% of the exported national origin value and 14% for other countries. The value of imports decreased by 3% as it reached BHD489mn during May versus BHD506mn for the same month of the previous year, while the top 10 countries account for 66% of the imports value and 34% for other countries. (GulfBase.com)

- 6. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg ( # Market closed on July 4, 2018) Source: Bloomberg (*$ adjusted returns; # Market closed on July 4, 2018) 40.0 60.0 80.0 100.0 120.0 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 QSE Index S&P Pan Arab S&P GCC 0.1% 0.5% 0.3% 0.9% (0.3%) 0.5% 0.8% (0.5%) 0.0% 0.5% 1.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,254.66 0.2 0.1 (3.7) MSCI World Index 2,082.17 0.0 (0.3) (1.0) Silver/Ounce 16.09 0.4 (0.2) (5.0) DJ Industrial# 24,174.82 0.0 (0.4) (2.2) Crude Oil (Brent)/Barrel (FM Future) 78.24 0.6 (1.5) 17.0 S&P 500# 2,713.22 0.0 (0.2) 1.5 Crude Oil (WTI)/Barrel (FM Future)# 74.14 0.0 (0.0) 22.7 NASDAQ 100# 7,502.67 0.0 (0.1) 8.7 Natural Gas (Henry Hub)/MMBtu# 2.87 0.0 (3.5) (19.0) STOXX 600 380.05 0.2 (0.1) (5.2) LPG Propane (Arab Gulf)/Ton# 95.00 0.0 1.3 (2.8) DAX 12,317.61 (0.1) 0.0 (7.5) LPG Butane (Arab Gulf)/Ton# 105.00 0.0 1.0 (0.6) FTSE 100 7,573.09 0.2 (0.6) (3.7) Euro 1.17 (0.0) (0.2) (2.9) CAC 40 5,320.50 0.2 (0.1) (2.8) Yen 110.49 (0.1) (0.2) (2.0) Nikkei 21,717.04 (0.3) (2.4) (2.8) GBP 1.32 0.3 0.2 (2.1) MSCI EM 1,056.07 (0.2) (1.3) (8.8) CHF 1.01 (0.0) (0.2) (1.9) SHANGHAI SE Composite 2,759.13 (1.1) (3.3) (18.2) AUD# 0.74 0.0 (0.3) (5.4) HANG SENG 28,241.67 (1.0) (2.4) (6.0) USD Index 94.53 (0.1) 0.1 2.6 BSE SENSEX 35,645.40 0.2 (0.1) (3.1) RUB 63.23 0.2 0.8 9.7 Bovespa 74,743.11 1.1 1.5 (17.3) BRL 0.26 (0.4) (0.9) (15.4) RTS 1,147.53 0.0 (0.6) (0.6) 82.0 80.1 67.4