Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a 31 March Daily market report

Semelhante a 31 March Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

31 March Daily market report

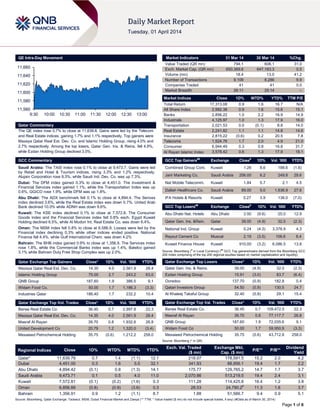

- 1. Page 1 of 6 QE Intra-Day Movement Qatar Commentary The QE index rose 0.7% to close at 11,639.8. Gains were led by the Telecom and Real Estate indices, gaining 1.7% and 1.1% respectively. Top gainers were Mazaya Qatar Real Est. Dev. Co. and Islamic Holding Group, rising 4.0% and 2.7% respectively. Among the top losers, Qatar Gen. Ins. & Reins. fell 4.9%, while Ezdan Holding Group declined 3.0%. GCC Commentary Saudi Arabia: The TASI index rose 0.1% to close at 9,473.7. Gains were led by Retail and Hotel & Tourism indices, rising 3.3% and 1.2% respectively. Alujain Corporation rose 9.3%, while Saudi Ind. Dev. Co. was up 7.3%. Dubai: The DFM index gained 0.3% to close at 4,451.0. The Investment & Financial Services index gained 1.1%, while the Transportation Index was up 0.6%. GGICO rose 1.9%, while DFM was up 1.8%. Abu Dhabi: The ADX benchmark fell 0.1% to close at 4,894.4. The Serives index declined 3.6%, while the Real Estate index was down 0.7%. United Arab Bank declined 10.0% while ADNH was down 9.6%. Kuwait: The KSE index declined 0.1% to close at 7,572.8. The Consumer Goods index and the Financial Services index fell 0.8% each. Egypt Kuwait Holding declined 6.5%, while Al Mudon Int. Real Estate Co. was down 6.4%. Oman: The MSM index fell 0.8% to close at 6,586.9. Losses were led by the Financial index declining 0.3% while other indices ended positive. National Finance fell 4.4%, while Gulf International Chem. was down 4.2% Bahrain: The BHB index gained 0.9% to close at 1,356.9. The Services index rose 1.8%, while the Commercial Banks index was up 1.4%. Batelco gained 3.1% while Bahrain Duty Free Shop Complex was up 2.0%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Est. Dev. Co. 14.35 4.0 2,561.9 28.4 Islamic Holding Group 75.00 2.7 243.2 63.0 QNB Group 187.60 1.9 386.5 9.1 Widam Food Co. 50.00 1.7 1,186.3 (3.3) Industries Qatar 186.40 1.7 232.2 10.4 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Barwa Real Estate Co 36.45 0.7 2,997.8 22.3 Mazaya Qatar Real Est. Dev. Co. 14.35 4.0 2,561.9 28.4 Masraf Al Rayan 39.70 0.8 1,932.6 26.8 United Development Co 20.79 1.2 1,320.0 (3.4) Mesaieed Petrochemical Holding 35.75 (0.6) 1,212.2 258.0 Market Indicators 31 Mar 14 30 Mar 14 %Chg. Value Traded (QR mn) 794.1 606.1 31.0 Exch. Market Cap. (QR mn) 650,369.6 647,183.3 0.5 Volume (mn) 18.4 13.0 41.2 Number of Transactions 9,109 8,286 9.9 Companies Traded 41 41 0.0 Market Breadth 26:11 25:14 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 17,313.08 0.9 1.6 16.7 N/A All Share Index 2,992.38 0.9 1.6 15.6 15.1 Banks 2,856.22 1.0 2.2 16.9 14.9 Industrials 4,125.97 1.0 1.3 17.9 16.0 Transportation 2,021.53 0.0 (0.1) 8.8 14.0 Real Estate 2,241.82 1.1 1.1 14.8 14.6 Insurance 2,815.22 (0.6) 0.2 20.5 7.8 Telecoms 1,524.76 1.7 2.0 4.9 21.0 Consumer 6,944.49 0.3 0.8 16.8 31.7 Al Rayan Islamic Index 3,578.42 0.6 1.3 17.9 18.1 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Combined Group Cont. Kuwait 1.26 8.6 188.6 (1.6) Jarir Marketing Co. Saudi Arabia 206.00 6.2 249.8 29.6 Nat Mobile Telecomm. Kuwait 1.84 5.7 2.1 4.5 Dallah Healthcare Co. Saudi Arabia 89.00 5.0 1,636.9 27.6 IFA Hotels & Resorts Kuwait 0.27 3.9 136.0 (7.0) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Abu Dhabi Nat. Hotels Abu Dhabi 3.50 (9.6) 25.0 12.9 Qatar Gen. Ins. &Rein. Qatar 39.00 (4.9) 32.0 (2.3) National Ind. Group Kuwait 0.24 (4.3) 3,378.9 4.3 Raysut Cement Co Muscat 2.19 (3.5) 106.6 8.4 Kuwait Finance House Kuwait 910.00 (3.2) 6,086.5 13.8 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Gen. Ins. & Reins. 39.00 (4.9) 32.0 (2.3) Ezdan Holding Group 15.91 (3.0) 83.7 (6.4) Ooredoo 137.70 (0.9) 182.8 0.4 Qatari Investors Group 54.50 (0.9) 130.5 24.7 Al Khaleej Takaful Group 32.40 (0.8) 29.1 15.4 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Barwa Real Estate Co. 36.45 0.7 109,472.5 22.3 Masraf Al Rayan 39.70 0.8 77,117.7 26.8 QNB Group 187.60 1.9 72,035.6 9.1 Widam Food Co 50.00 1.7 59,950.9 (3.3) Mesaieed Petrochemical Holding 35.75 (0.6) 43,712.8 258.0 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 11,639.79 0.7 1.4 (1.1) 12.1 218.07 178,591.5 15.2 2.0 4.2 Dubai 4,451.00 0.3 1.6 5.5 32.1 341.93 88,956.1 19.4 1.7 2.2 Abu Dhabi 4,894.42 (0.1) 0.8 (1.3) 14.1 175.77 129,765.2 14.7 1.7 3.7 Saudi Arabia 9,473.71 0.1 0.5 4.0 11.0 2,070.86 513,219.5 19.4 2.4 3.1 Kuwait 7,572.81 (0.1) (0.2) (1.6) 0.3 111.28 114,425.8 16.4 1.2 3.8 Oman 6,856.89 (0.8) (0.9) (3.6) 0.3 28.53 24,790.2# 11.3 1.6 3.7 Bahrain 1,356.91 0.9 1.2 (1.1) 8.7 1.88 51,566.7 9.4 0.9 5.1 Source: Bloomberg, Qatar Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) (#Data as of March 30, 2014) 11,560 11,580 11,600 11,620 11,640 11,660 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QE index rose 0.7% to close at 11,639.8. The Telecom and Real Estate indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders. Mazaya Qatar Real Est. Dev. Co. and Islamic Holding Group were the top gainers, rising 4.0% and 2.7% respectively. Among the top losers, Qatar Gen. Ins. & Reins. fell 4.9%, while Ezdan Holding Group declined 3.0%. Volume of shares traded on Monday rose by 41.2% to 18.4mn from 13.0mn on Sunday. Further, as compared to the 30-day moving average of 16.2mn, volume for the day was 13.7% higher. Barwa Real Estate Co. and Mazaya Qatar Real Est. Dev. Co. were the most active stocks, contributing 16.3% and 13.9% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Ooredoo (ORDS) Fitch Qatar LT IDR A+ A+ – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency) Earnings Releases Company Market Currency Revenue (mn) FY2013 % Change YoY Operating Profit (mn) FY2013 % Change YoY Net Profit (mn) FY2013 % Change YoY Dubai Holding Commercial Operations Group (DHCOG) Dubai AED 11,645.2 27.0% 3,301.7 121.3% 3,299.0 176.6% Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 03/31 US NAPM - Milwaukee ISM Milwaukee March 56.0 51.0 48.6 03/31 EU Eurostat CPI Estimate YoY March 0.50% 0.60% 0.70% 03/31 EU Eurostat CPI Core YoY March 0.80% 0.80% 1.00% 03/31 France INSEE GDP YoY 4Q2013 0.80% 0.80% 0.80% 03/31 France INSEE GDP QoQ 4Q2013 0.30% 0.30% 0.30% 03/31 Germany Destatis Retail Sales YoY February 2.00% 0.80% 0.90% 03/31 Germany Destatis Retail Sales MoM February 1.30% -0.50% 1.70% 03/31 UK Hometrack Hometrack Housing Survey MoM March 0.60% – 0.70% 03/31 UK Hometrack Hometrack Housing Survey YoY March 5.70% – 5.40% 03/31 UK Bank of England Net Consumer Credit February 0.6B 0.7B 0.6B 03/31 UK Bank of England Mortgage Approvals February 70.3K 75.3K 76.8K 03/31 Spain Ministerio de Hacienda Spain Budget Balance YTD February -12.40B – -6.09B 03/31 Italy ISTAT CPI NIC incl. tobacco MoM March 0.10% 0.10% -0.10% 03/31 Italy ISTAT CPI NIC incl. tobacco YoY March 0.40% 0.40% 0.50% 03/31 Italy ISTAT CPI EU Harmonized MoM March 2.10% 2.30% -0.30% 03/31 Italy ISTAT CPI EU Harmonized YoY March 0.30% 0.40% 0.40% 03/31 Japan Markit Markit/JMMA Japan Manufacturing PMI March 53.9 – 55.5 03/31 Japan JAMA Industrial Production MoM February -2.30% 0.30% 3.80% 03/31 Japan JAMA Industrial Production YoY February 6.90% 9.90% 10.30% 03/31 Japan JAMA Vehicle Production YoY February 7.10% – 14.50% 03/31 Japan Ministry of Land, Infra. Housing Starts YoY February 1.00% 4.80% 12.30% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar GISS to acquire JDC’s 30% share in GDI at net book value – Gulf International Services (GISS) has signed a share purchase agreement (SPA) with Japan Drilling Company (JDC) to acquire all of JDC’s 30% share in Gulf Drilling International (GDI). GISS shall own all of JDC’s shares in GDI starting May 1, 2014, making GDI a wholly owned subsidiary of GISS. Further, GDI and JDC also signed a letter of intent for the exchange of technical cooperation between the two companies and the promotion of mutually beneficial business opportunities. Now established as a world-class drilling contractor, GDI is in the process of doubling the size of its total fleet (offshore, onshore, Overall Activity Buy %* Sell %* Net (QR) Qatari 59.99% 65.45% (43,316,118.62) Non-Qatari 40.01% 34.55% 43,316,118.62

- 3. Page 3 of 6 lift boats, barges, etc), from 9 to 18, over 2012-2014. With its share of GDI’s results increasing from 70% to 100%, GISS will enjoy substantially higher earnings from GDI in the future by having a larger share of a bigger operation. GISS Chief Coordinator, Mr. Ebrahim Al Mannai advised that consolidated revenue for the GISS group is projected to reach QR3.5bn in 2014 due to the GDI acquisition. Mr. Al Mannai added that the fundamentals of the GISS investment to increase its stake in GDI were favorable. The price of JDC’s 30% stake will be valued at 30% of GDI’s net book value as of 30 April 2014, pursuant to the joint venture agreement between GISS and JDC, while the fair market value of GDI’s assets, with the majority of its rigs on multiyear contracts and utilization at 100%, is well above that value. The net book value and acquisition cost is approximately $160mn, subject to change due the final account settlements on the acquisition date. Meanwhile, the fair market value is estimated to be QR1.2bn. Moreover, expected additional revenue in 2014 from the acquisition is expected to reach QR445mn with additional net profit of QR150mn. (QE, GISS Press Release) Qatar Rail, QMIC sign deal to adopt Masarak platform – Qatar Railways Company (Qatar Rail) and Qatar Mobility Innovations Centre (QMIC) have inked an agreement that will allow Qatar Rail to use QMIC’s Masarak platform and services for traffic monitoring, logistics management and road safety. The partnership will enable Qatar Rail to deploy the Masarak platform and its integrated set of transport and logistics services and applications. As part of this agreement, QMIC will design, build, operate and maintain a Logistics Transport Coordination Centre (LTCC) on Qatar Rail’s premises to monitor various operations round the clock. The Masarak-enabled LTCC will be staffed with traffic experts to deliver key services and intelligence for minimizing the impact of logistics operations on traffic flow in Doha. (Gulf-Base.com) MDPS releases socio-economic statistics for February – According to the monthly statistics released by the Ministry of Development Planning & Statistics (MDPS), Qatar’s population stood at 2.1mn in February 2014, of whom males constituted around 1.5mn. The 15-64 age group was estimated at 1.7mn of the total population. Further, MDPS data showed that the total number of vehicles registered with the traffic department in February amounted to 8,123 vehicles, of which 5,250 are private. Meanwhile, the Consumer Price Index attained 116.5 points last month. There were 748 real estate transactions that were valued at around QR2.8bn. The total electricity generated stood at 1.865mn kilowatts and water production exceeded 29.430mn cubic meters. (MDPS) QIMD, Takamul sign MoU to cooperate on projects – Takamul Investment Company and the Qatar Industrial Manufacturing Company (QIMD) signed a MoU that enables both entities to cooperate on jointly developing future industrial projects in Oman and Qatar. QIMD’s CEO Abdul Rahman Al- Ansari said that the MoU enables them to find some real mutual benefits and QIMD’s team will be keen to explore areas for collaboration and sharing of best practices. (QE) NDSQ signs 2 MoUs worth QR3.1bn to build 7 naval vessels – Nakilat Damen Shipyards Qatar (NDSQ) has signed two MoUs worth QR3.1bn to build seven vessels for the Qatar Armed Forces. The MoUs pertain to some six 50m-long axe-bow high- speed patrol vessels and one 52m-long diving support vessel for the Qatar Armed Forces. These state-of-the-art naval ships will be constructed in Qatar at NDSQ’s shipbuilding facility at Erhama Bin Jaber Al Jalahma Shipyard in Ras Laffan. Further, a large integrated logistic support package is also mentioned in the MoUs. NDSQ is a JV between Nakilat and Dutch shipbuilder Damen, which is based at Ras Laffan Port. (Gulf-Times.com) DHBK to announce 1Q2014 results on April 20 – Doha Bank (DHBK) stated that it will publish its 1Q2014 financial results on April 20, 2014. (QE) QFLS to announce 1Q2014 results on April 21 – Qatar Fuel Company (QFLS) will disclose its first quarter financial results for the year 2014 on April 21, 2014 (QE) QIIK to disclose 1Q2014 results on April 23 – Qatar International Islamic Bank (QIIK) will disclose its first quarter financial results for the year 2014 on April 23, 2014. (QE) ORDS to disclose 1Q2014 results on April 30 – Ooredoo (ORDS) has announced its intent to disclose its 1Q2014 financial results on April 30, 2014. (QE) Sidra appoints acting COO – The Sidra Medical & Research Center has appointed Abdulrazaq al-Kuwari as the Acting Chief Operating Officer (COO). Al-Kuwari will be reporting to CEO William Owen, and will be responsible for planning, implementing, evaluating, and improving the operational functions in Sidra, which is set to open in 1Q2015. (Gulf- Times.com) International China’s HSBC manufacturing PMI hits eight-month low in March – China's manufacturing engine contracted in the first quarter of 2014, a private survey showed, adding to market expectations for government stimulus to arrest the loss of momentum in the world's second-largest economy. The final Markit/HSBC Purchasing Managers' Index (PMI) fell to an eight- month low of 48.0 in March from February's final reading of 48.5. The outcome was in line with last week's preliminary PMI reading of 48.1. The index has been below the 50 level since January, indicating a contraction in the sector. HSBC China’s Chief Economist Hongbin Qu said the final PMI reading in March confirmed the weakness of domestic demand conditions. This implies that first quarter GDP growth is likely to have fallen below the annual target of 7.5%. However, the National Bureau of Statistics' official PMI rose to 50.3 in March from February's 50.2, in line with forecasts. Hence, Asian shares hit four-month high after the news, as the PMI survey showed manufacturing managed to continue expanding in March. Above 50 indicates expansion, below 50 signifies contraction.(Reuters) Japan corporate sentiment gains seen short-lived as tax rises – Sentiment among large Japanese manufacturers rose to the highest level since 2007, a gain that may be short-lived as sales-tax increase on April 1 weighs on consumption and confidence. The Tankan index stood at 17 in March, climbing from 16 in December, a Bank of Japan report showed. The index is forecast to drop to 8 in June, worse than Bloomberg economists’ forecast of 13. The survey showed big companies plan to boost investment 0.1% in the year starting today, less than an estimated increase of 3.9% in the previous fiscal year. The lack of support from private-sector demand could add to pressure on the central bank to boost unprecedented easing to support Japan. (Bloomberg) BoE signs Yuan clearing deal with China’s PBoC – The Bank of England (BoE) signed an agreement with the People’s Bank of China (PBoC) to enable the clearing and settlement of Chinese Yuan transactions in London as the UK vies to become a hub for trading the currency in Europe. The BOE said the deal will facilitate the use of the Yuan by banks and other companies conducting international transactions. A clearing bank will be designated in London in due course. The accord comes three

- 4. Page 4 of 6 days after Germany’s Bundesbank signed a similar agreement. Paris and Luxembourg are also seeking to capture a slice of the growing market for Yuan trading as China opens up its capital market and promotes the use of the currency in international trade and financing. (Bloomberg) Regional OPEC crude output down 117,000 bpd to 30.293mn – According to the Bloomberg survey, crude oil production from the 12-member OPEC group declined 117,000 bpd in March from February. (Bloomberg) Saudi Arabia’s AHAB calls banks for Dubai meeting on $5.9bn default – Ahmad Hamad Algosaibi & Brothers Company (AHAB) invited creditors including BNP Paribas and Standard Chartered to discuss claims on $5.9bn of debt as it seeks to recover from the Middle East’s biggest default. The Saudi Arabian company, with interests ranging from construction to finance, will outline proposals aimed at achieving a comprehensive settlement with more than 70 creditors at a May 7 meeting in Dubai. Banks rejected an original debt restructuring proposal from AHAB four years ago. AHAB and billionaire Maan al-Sanea’s Saad Group defaulted on at least $15.7bn in 2009 as the global economic crisis froze credit markets and asset prices slumped. (Bloomberg) Bahri receives a dry bulk vessel Bahri Trader – The National Shipping Company of Saudi Arabia (Bahri) announced that its subsidiary Bahri Dry Bulk (BDB) (owned 60% by Bahri and 40% by Arasco) in Japan received a dry bulk vessel named Bahri Trader. This is the fifth and final vessel delivered from the five vessels that were contracted in 2012. The financial impact of the delivered vessel will materialize during the 2Q2014. Bahri had announced that Bahri Dry Bulk signed contract to build 5 dry bulk ships with one of the leading ship yards in Japan. These vessels have a capacity of 82,000 dwt and length of 229 meters, consumes less fuel and ecofriendly. The Company started its operation through chartering 5 vessels and chartering them out to Arasco which will be replaced by the delivered vessels. (Tadawul) Dubai World sees more early debt payments, can meet 2015 maturity – Dubai World, the conglomerate at the centre of the emirate's debt crisis, has the means to make its first big repayment on time next year and expects to pay off more of its debt ahead of schedule, a top executive said. Mohammed al- Shaibani, chief executive of sovereign wealth fund Investment Corp of Dubai and a key figure in negotiating the emirate's debt restructurings in recent years, said Dubai World would be able to meet a $4.4bn loan maturity in May 2015 and to make some other repayments early. (Gulf-Times.com) Waha Capital secures $750mn credit facility – Abu Dhabi investment company Waha Capital had secured a new five-year $750mn credit facility. The facility, comprising a term loan for $375mn and a revolving loan for the same amount, replaces the previous $505mn facility secured in 2011. The deal was coordinated by HSBC and First Gulf Bank, with Emirates NBD Capital Limited, First Gulf Bank and HSBC acting as book- runners and mandated lead arrangers. (Reuters, ADX) AHB considers capital hike to fuel growth – Abu Dhabi government-owned Al Hilal Bank’s (AHB) CEO Mohamed Jamil Berro said that AHB is considering a capital increase in 2014 to support growth of its operations. The Islamic lender, owned by the Abu Dhabi Investment Council, an investment arm of the Abu Dhabi government, plans to expand its retail and wholesale banking business locally and internationally over the next five years. Unlisted Al Hilal has paid-up capital of AED4bn, of which AED3.09bn have been drawn. The bank's capital adequacy ratio is around 13%, below the average of roughly 20% for banks in the UAE. The UAE central bank stipulates a minimum 12% ratio for banks. (Reuters) Noor Bank AED255mn net profit for 2013 – Noor Bank reported a record net profit of AED255mn for 2013, up from AED76mn for the year ended 2012. Noor Bank's total assets also saw strong growth, rising 29%, to AED23.2bn as compared with AED18bn, at the start of the year. Total customer financing increased by 32% to AED14.3bn. Customer deposits were increased by 33% in 2013, reaching AED18.6bn as compared with AED14.0bn at the year-end 2012. This was driven by a 24% increase in the bank's customer base. (Bloomberg) FY2013/14 budget surplus expected at KD11bn – Kuwaiti public finance figures for the first 11 months of FY2013/14 showed that the government spending climbed to KD11.3bn in February, up 7% YoY on the back of higher transfers. The latter has driven growth in current expenditures, while capital spending has remained weak. As usual, recorded spending should register a big jump in the final month of the fiscal year (i.e. March), partly due to reporting issues. Nevertheless, overall spending growth is projected to end up at a modest 4% in FY2013/14, well below last year. Inter-governmental transfers continue to drive growth in current expenditures, which have more than offset large declines in the goods & services component. Current spending rose 7% YoY to KD10.4bn in February, driven largely by a KD1.3bn rise in transfer payments to the social security fund (PIFSS). The latter has more than offset a 24% YoY decline in spending on goods and services. This is mostly related to a drop in the cost of purchasing fuel from government refineries, as a result of lower oil prices. Government revenues reached KD28.9bn in February, down 2% YoY as a result of lower oil revenues. The latter has declined on the back of a 3% YoY fall in Kuwait crude export prices over the same period. (Gulf-Base.com) KIPCO says OSN’s IPO to start within weeks – Kuwait Projects Company (KIPCO) said the IPO of its pay-TV company OSN, will start within weeks. KIPKO’s Vice Chairman, Faisal Al Ayyar said KIPCO will go ahead with the IPO as a shareholder. Al Ayyar said the market conditions are now right as equity valuations have improved in the Middle East. KIPKO will be starting the process within a few weeks and is hoping to complete it in 3Q or 4Q2014. KIPKO, which owns 60.5% of OSN, said in June 2013, it had hired Rothschild to examine options for a potential IPO. (Bloomberg) Burgan Bank to raise capital to comply with Basel III – Kuwait-based Burgan Bank wants to raise more capital in 2014 to comply with the Basel III regulations, while any acquisitions were unlikely to come soon. The bank’s CEO Eduardo Eguren said the capital increase, which may happen in 3Q2014, could be pure capital or perpetual bonds or both. (Bloomberg) Burgan Bank distributes dividends of 7 fils per share – The Burgan Bank Group AGM approved to distribute cash dividends amounting to KD0.007 (7 fils) and 7% bonus shares among shareholders. (Bloomberg) Omantel’s public offer opens at OMR1.35 per share – The Omani government began the second phase of its share sale in Oman Telecommunications Company (Omantel) on March 31. The IPO is open for Omani citizens at a fixed price of OMR1.35 per share and will close on April 13. After the first two phases are completed, government ownership in Omantel will drop from 70% to 51%. Meanwhile, Omantel announced a speed upgrade of its home broadband plans. (Bloomberg)

- 5. Page 5 of 6 6 Omani projects win MEED Quality Awards – MEED has announced the names of the various projects in Oman that have won the national round in The MEED Quality Awards for Projects 2014, which are given in association with Mashreq. After a rigorous judging process, MEED revealed that Oman’s Projects Of The Year are: Duqm Development Company’s Duqm Frontier Town project, United Real Estate Company’s Salalah Gardens Mall and Residences, Technical Trading Co. and APR Energy’s Oman 32MW Peak Shaving Power project, Oman Educational Service’s German University of Technology in Oman and finally, Petroleum Development Oman’s Saih Nihayda Depletion Compression Phase-1 project and Solar EOR Project. (Gulf-Base.com) Oman’s exports and re-exports hit OMR3bn in 2013 – The Minister of Commerce & Industry Ali bin Masoud Al Sunaidy said that the total value of products exported and re-exported from Oman to other GCC countries showed an increase in 2013 and reached about OMR3bn. Out of this, Al Sunaidy said Omani products accounted for around OMR1.5bn. In 2012, OMR1bn worth of Omani products were exported to other GCC countries and the total amount of exported and re-exported goods to the GCC stood at OMR2bn. He said that plastic-related industries in Iran would be looking for materials from GCC. He added that there would also be a demand from Iran for materials that can be used in intermediary industries as well as automotive and spare parts industries. (Gulf-Base.com) Moody's changes outlook on Bahraini banks to stable – Moody's Investors Service has changed the outlook on Bahrain's retail banking system to Stable from Negative. Moody's said this reflects the solid funding base and capital buffers, as well as an economic recovery driven by increased government spending and construction activity. While economic growth will buoy banks' credit fundamentals and their profitability, Moody's noted that increased government spending also puts pressure on Bahrain's fiscal position, which could affect the government capacity to provide support for financial institutions over the outlook horizon. Moody's also noted that real non-oil GDP will strengthen to 3.8% in 2014 from 3.0% in 2013. Given that most bank lending in Bahrain remains directed toward the non-oil economy, Moody's forecasts domestic credit growth of around 7-8% over the next 12-18 months. (Bloomberg) Batelco, AmEx Mid-east sign partnership deal – Bahrain’s leading telecommunications provider Batelco and American Express Middle East (AmEx Mid-east) have signed an agreement that will see the operator providing advanced technology services to the international payments firm. The partnership will support AmEx Mid-east’s commitment to deliver innovative solutions and better customer service in the MENA region. (Gulf-Base.com) NASS approves 15% dividend – Nass Corporation’s (NASS) AGM has approved the distribution of 15% cash dividend from the paid-up capital amounting to 15 fils per share. Accordingly, NASS’ shares will be traded ex-dividend starting from April 1, 2014. (Bahrain Bourse) TAKAFUL approves 5% dividend – Takaful International Company’s (TAKAFUL) AGM approved the distribution of 5% cash dividend from the paid-up capital amounting to 5 fils per share. (Bahrain Bourse) AHLIA approves 5% dividend – Al Ahlia Insurance Company (AHLIA) AGM approved the distribution of 5% cash dividends from the paid-up capital amounting to 0.005 fils per share. Accordingly, AHLIA’s shares shall trade ex-dividend starting from April 1, 2014. (Bahrain Bourse)

- 6. Contacts Saugata Sarkar Keith Whitney Sahbi Kasraoui Head of Research Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg (*Market Closed on March 31, 2014) Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC 0.1% 0.7% (0.1%) 0.9% (0.8%) (0.1%) 0.3% (1.2%) (0.8%) (0.4%) 0.0% 0.4% 0.8% 1.2% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,284.01 (0.9) (0.9) 6.5 DJ Industrial 16,457.66 0.8 0.8 (0.7) Silver/Ounce 19.77 (0.3) (0.3) 1.6 S&P 500 1,872.34 0.8 0.8 1.3 Crude Oil (Brent)/Barrel (FM Future) 107.76 (0.3) (0.3) (2.7) NASDAQ 100 4,198.99 1.0 1.0 0.5 Natural Gas (Henry Hub)/MMBtu 4.47 (0.3) (0.3) 2.9 STOXX 600 334.31 0.2 0.2 1.8 LPG Propane (Arab Gulf)/Ton* 106.25 0.0 0.0 (16.0) DAX 9,555.91 (0.3) (0.3) 0.0 LPG Butane (Arab Gulf)/Ton 121.00 (0.2) (0.2) (10.9) FTSE 100 6,598.37 (0.3) (0.3) (2.2) Euro 1.38 0.1 0.1 0.2 CAC 40 4,391.50 (0.4) (0.4) 2.2 Yen 103.23 0.4 0.4 (2.0) Nikkei 14,827.83 0.9 0.9 (9.0) GBP 1.67 0.1 0.1 0.6 MSCI EM 994.65 1.0 1.0 (0.8) CHF 1.13 0.3 0.3 0.9 SHANGHAI SE Composite 2,033.31 (0.4) (0.4) (3.9) AUD 0.93 0.2 0.2 3.9 HANG SENG 22,151.06 0.4 0.4 (5.0) USD Index 80.10 (0.1) (0.1) 0.1 BSE SENSEX 22,386.27 0.2 0.2 5.7 RUB 35.17 (1.6) (1.6) 7.0 Bovespa 50,414.92 1.3 1.3 (2.1) BRL 0.44 (0.4) (0.4) 4.1 RTS 1,226.10 3.4 3.4 (15.0) 167.3 148.6 134.9