Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a 3 August Daily market report

Semelhante a 3 August Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

3 August Daily market report

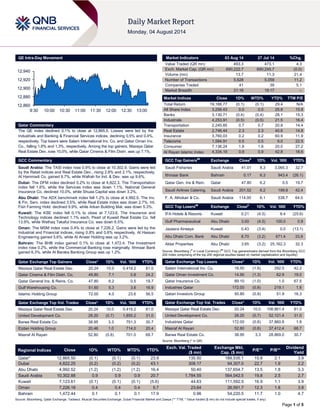

- 1. Page 1 of 5 QE Intra-Day Movement Qatar Commentary The QE index declined 0.1% to close at 12,865.5. Losses were led by the Industrials and Banking & Financial Services indices, declining 0.5% and 0.4%, respectively. Top losers were Salam International Inv. Co. and Qatar Oman Inv. Co., falling 1.6% and 1.3%, respectively. Among the top gainers, Mazaya Qatar Real Estate Dev. rose 10.0%, while Qatar Cinema & Film Distri. was up 7.1%. GCC Commentary Saudi Arabia: The TASI index rose 0.9% to close at 10,302.9. Gains were led by the Retail indices and Real Estate Dev., rising 2.8% and 2.1%, respectively. Al Hammadi Co. gained 9.7%, while Wafrah for Ind. & Dev. was up 9.6%. Dubai: The DFM index declined 0.2% to close at 4,822.3. The Transportation index fell 1.6%, while the Services index was down 1.1%. National General Insurance Co. declined 10.0%, while Shuaa Capital was down 3.2%. Abu Dhabi: The ADX benchmark index fell 1.2% to close at 4,992.5. The Inv. & Fin. Serv. index declined 3.5%, while Real Estate index was down 2.7%. Int. Fish Farming Hold. declined 9.9%, while Arkan Building Mat. was down 5.3%. Kuwait: The KSE index fell 0.1% to close at 7,123.6. The Insurance and Technology indices declined 1.1% each. Pearl of Kuwait Real Estate Co. fell 13.9%, while Wethaq Takaful Insurance Co. was down 6.5%. Oman: The MSM index rose 0.4% to close at 7,226.2. Gains were led by the Industrial and Financial indices, rising 0.8% and 0.6% respectively. Al Hassan Engineering gained 5.6%, while Al Anwar Holding was up 3.2%. Bahrain: The BHB index gained 0.1% to close at 1,472.4. The Investment index rose 0.2%, while the Commercial Banking rose marginally. Ithmaar Bank gained 6.3%, while Al Baraka Banking Group was up 1.2%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 20.24 10.0 5,419.2 81.0 Qatar Cinema & Film Distri. Co. 49.80 7.1 0.8 24.2 Qatar General Ins. & Reins. Co. 47.80 6.2 0.5 19.7 Gulf Warehousing Co. 51.60 5.3 3.6 16.9 Islamic Holding Group 72.00 4.0 23.6 56.5 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 20.24 10.0 5,419.2 81.0 United Development Co. 28.20 (0.7) 1,855.2 31.0 Barwa Real Estate Co. 38.95 3.3 751.3 30.7 Ezdan Holding Group 20.46 1.0 714.0 20.4 Masraf Al Rayan 52.80 (0.8) 701.0 68.7 Market Indicators 03 Aug 14 27 Jul 14 %Chg. Value Traded (QR mn) 493.3 473.1 4.3 Exch. Market Cap. (QR mn) 690,222.7 690,245.7 (0.0) Volume (mn) 13.7 11.3 21.4 Number of Transactions 5,628 5,059 11.2 Companies Traded 41 39 5.1 Market Breadth 21:16 19:17 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 19,188.77 (0.1) (0.1) 29.4 N/A All Share Index 3,256.43 0.0 0.0 25.8 15.8 Banks 3,130.71 (0.4) (0.4) 28.1 15.3 Industrials 4,253.91 (0.5) (0.5) 21.5 16.4 Transportation 2,245.85 0.7 0.7 20.8 14.4 Real Estate 2,746.44 2.3 2.3 40.6 14.8 Insurance 3,760.03 0.2 0.2 60.9 11.9 Telecoms 1,584.91 0.5 0.5 9.0 22.5 Consumer 7,136.24 1.8 1.8 20.0 27.2 Al Rayan Islamic Index 4,334.19 0.9 0.9 42.8 18.6 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Fisheries Saudi Arabia 41.01 8.3 3,065.3 32.7 Ithmaar Bank Bahrain 0.17 6.3 943.4 (26.1) Qatar Gen. Ins & Rein. Qatar 47.80 6.2 0.5 19.7 Saudi Airlines Catering. Saudi Arabia 201.52 6.2 199.8 42.4 F. A. Alhokair & Co. Saudi Arabia 114.00 6.1 538.7 64.0 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% IFA Hotels & Resorts Kuwait 0.21 (4.5) 8.4 (25.6) Gulf Pharmaceutical Abu Dhabi 3.00 (4.5) 100.0 0.9 Jazeera Airways Kuwait 0.43 (3.4) 0.0 (13.1) Abu Dhabi Com. Bank Abu Dhabi 8.70 (3.2) 671.4 33.9 Aldar Properties Abu Dhabi 3.65 (3.2) 25,162.3 32.3 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Salam International Inv. Co. 18.50 (1.6) 292.5 42.2 Qatar Oman Investment Co. 14.90 (1.3) 62.9 19.0 Qatar Insurance Co. 89.10 (1.0) 1.0 67.5 Industries Qatar 172.00 (0.8) 219.1 1.8 Qatari Investors Group 50.80 (0.8) 51.9 16.3 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Mazaya Qatar Real Estate Dev. 20.24 10.0 106,861.4 81.0 United Development Co. 28.20 (0.7) 52,121.4 31.0 Industries Qatar 172.00 (0.8) 37,860.9 1.8 Masraf Al Rayan 52.80 (0.8) 37,412.4 68.7 Barwa Real Estate Co. 38.95 3.3 28,869.0 30.7 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,865.50 (0.1) (0.1) (0.1) 23.9 135.50 189,535.1 15.8 2.1 3.9 Dubai 4,822.25 (0.2) (0.2) (0.2) 43.1 308.17 94,307.0 22.7 1.9 2.2 Abu Dhabi 4,992.52 (1.2) (1.2) (1.2) 16.4 50.40 137,654.7 13.5 1.8 3.3 Saudi Arabia 10,302.88 0.9 0.9 0.9 20.7 1,784.55 564,042.5 19.8 2.5 2.7 Kuwait 7,123.61 (0.1) (0.1) (0.1) (5.6) 44.63 111,592.5 16.9 1.1 3.9 Oman 7,226.18 0.4 0.4 0.4 5.7 23.64 26,591.7 12.3 1.8 3.8 Bahrain 1,472.44 0.1 0.1 0.1 17.9 0.96 54,220.5 11.7 1.0 4.7 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,860 12,880 12,900 12,920 12,940 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 5 Qatar Market Commentary The QE index declined 0.1% to close at 12,865.5. The Industrials and Banking & Fin. Services indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Salam International Investment Co. and Qatar Oman Investment Co. were the top losers, falling 1.6% and 1.3%, respectively. Among the top gainers, Mazaya Qatar Real Estate Development rose 10.0%, while Qatar Cinema & Film Distri. Co. was up 7.1%. Volume of shares traded on Sunday rose by 21.4% to 13.7mn from 11.3mn on the previous Sunday. However, as compared to the 30-day moving average of 14.3mn, volume for the day was 4.4% lower. Mazaya Qatar Real Estate Dev. and United Development Co. were the most active stocks, contributing 39.7% and 13.6% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings and Earnings Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Al Sagr National Insurance Co. (ASNIC) A.M. Best Dubai FSR/ICR B+/bbb- B++/bbb Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, ICR – Issuer Credit Rating) Earnings Releases Company Market Currency Revenue (mn)2Q2014 % Change YoY Operating Profit (mn) 2Q2014 % Change YoY Net Profit (mn) 2Q2014 % Change YoY Dar Al Takaful Dubai AED 39.5 24.7% 5.1 319.9% 0.5 NA Dubai Investments (DIC) Dubai AED 1,020.8 58.2% – – 540.5 241.0% Aldar Properties Dubai AED 2,194.0 73.9% – – 505.8 -59.6% Kuwait Slaughter House Co. (KSH)* Kuwait KD – – – – 0.4 -16.2% Gulf Cable & Electrical Industries Co.* Kuwait KD – – – – 7.8 -7.2% Injazzat Real Estate Development Co. (IREDC)* Kuwait KD – – – – 0.8 -75.8% National International Holding Co. (NIHC)* Kuwait KD – – – – 0.4 -19.5% Kuwait Reinsurance Co.* Kuwait KD – – – – 0.9 -32.0% Equipment Holding Co. (EHC)* Kuwait KD – – – – 0.5 -84.3% National Petroleum Services Co. – Kuwait (NPSC)* Kuwait KD – – – – 2.1 4.6% Salalah Mills Co. (SMC)* Oman OMR 35.5 20.1% – – 3.8 57.7% Source: Company data, DFM, ADX, MSM (* 1H2014 results) News Qatar QNCD net profit drops QoQ and YoY – Qatar National Cement Company (QNCD) posted a net profit of QR107.9mn in 2Q2014 vs. QR129.9mn in 1Q2014; dropping by 16.9% and 7.7% QoQ and YoY, respectively. EPS stood at QR4.84 as of 1H2014 vs. QR4.80 as of 2H2013. (QE) CBQK appoints new executive general manager – Commercial Bank of Qatar (CBQK) has appointed Mr. Colin Macdonald as Executive General Manager, Business Enablement. Mr. Colin will play a leading role in driving business performance and strategic initiatives, supporting and advising the CEO and the CBQK leadership team. Mr. Colin has wide banking experience, including extensive experience in the Middle East, built over 26 years. (Zawya) ORDS’ Myanmar coverage to reach 68 cities by August 15 – Ooredoo’s (ORDS) coverage in Myanmar will rapidly extend beyond the three main cities of Mandalay, Nay Pyi Taw and Yangon to include some 68 cities and towns by August 15. ORDS has announced the availability of its “crystal clear” voice calls and fast internet services in three of Myanmar’s major cities, Mandalay, Nay Pyi Taw and Yangon, as part of the final preparations for the commercial launch later this month. Initially, ORDS will provide free of charge in a kick-off promotion. In another first, not only for Myanmar but globally, Ooredoo is rolling out a next generation, purely UMTS900 network with some of the most advanced 3G technology in the world. The benefits of this technology include a stronger signal, crystal clear sound and fast Internet. (Gulf-Times.com) ORDS announces MARK as Nojoom partner – Ooredoo (ORDS) has announced Masraf Al Rayan (MARK) as the newest Nojoom partner, further expanding the award-winning reward program’s range of partners. MARK customers can now redeem their Al Rayan Loyalty Points for Nojoom Points and will receive one Nojoom Point for each Al Rayan Loyalty Point redeemed as part of the new partnership. (Gulf-Times.com) Overall Activity Buy %* Sell %* Net (QR) Qatari 63.31% 69.82% (32,108,416.70) Non-Qatari 36.69% 30.18% 32,108,416.70

- 3. Page 3 of 5 Katara Hospitality announces opening of its Paris property – Katara Hospitality has announced the opening of its property in Paris, The Peninsula Paris, following an extensive four-year restoration. It becomes the 18th operational hotel in Katara Hospitality’s portfolio of 28 properties around the world. The Peninsula Paris is jointly owned by Katara Hospitality and The Hongkong and Shanghai Hotels, Limited (HSH). (Gulf- Times.com) ARTIC announces rebranding, launch of Marriott Marquis – Al Rayyan Tourism and Investment (ARTIC), the hospitality subsidiary of Al Faisal Holding Company, has announced a new hotel brand in Doha’s West Bay, where three hotels will be merged to become one property. The company said The Renaissance Doha, Courtyard Doha and Marriott Executive Apartments Doha will be collectively rebranded to become the Marriott Marquis City Center Doha hotel. Marquis is a brand extension of the Marriott hotels and JW Marriott hotels brands. The 5-star Marriott Marquis City Center Doha hotel, located at Omar Al Mukhtar Street, West Bay, is directly connected to the City Center mall. (GulfBase.com) QA to add three extra flights to Madrid, starts second freighter service to Delhi – Qatar Airways (QA) will scale up its operations to Madrid, Spain from November 16 with the addition of three extra flights per week. The increase in frequency will take the total number of flights up from seven to 10 per week, resulting in more options for passengers. Meanwhile, Qatar Airways Cargo has started operating its second freighter service to Delhi, India. The second frequency builds rapidly on the back of the first freighter service from Doha, which arrived at Delhi’s Indira Gandhi International Airport in May 2014. The second freighter service to Delhi started over Ramadan on July 22. (Gulf-Times.com) International Central bank meetings to set stage for parting of ways – After the Federal Reserve maintained its path toward raising US interest rates next year, other major central banks will jostle for space on a crowded stage this week. The European Central Bank, Bank of Japan, Bank of England and the central banks of India and Australia all hold meetings. While imminent action is unlikely, the time when policy settings start pointing in different directions is nearing. US growth rebounded in the second quarter and the Fed upgraded its assessment of the economy last week. It is on course to stop creating money in October but expectations are that there will be no interest rate hike before mid-2015. That puts the Bank of England in pole position to be the first major central bank to push rates up from their record low of 0.5%, perhaps before the year is out. Although the UK economy is expanding at an annualized clip in excess of 3% and unemployment is tumbling, the absence of wage pressure means there is no immediate reason to act. The consensus is that rates will not rise until early 2015 but polling by Reuters last week found economists expect a first voice or two on the nine- strong Monetary Policy Committee to call for a rate rise this week. (Reuters) Portugal announces €4.9bn Banco Espirito Santo rescue – Portugal’s central bank took control of Banco Espirito Santo SA in a €4.9bn bailout that will leave junior bondholders with losses. The Bank of Portugal’s Resolution Fund will move Banco Espirito Santo’s deposit-taking operations and most of its assets to a new company, Novo Banco, which it will own outright. The fund will finance the rescue with a Treasury loan to be repaid by Novo Banco’s eventual sale. According to a central bank, Espirito Santo shareholders and junior bondholders will be left with the most “problematic” assets, including loans to other parts of the Espirito Santo Group and the lender’s stake in its Angolan operation. The Finance Ministry said shareholders, subordinated debt holders as well as board members or former board members directly involved in the more recent events, and not the taxpayers, will be called to shoulder the losses incurred by a banking business they failed to adequately oversee. (Bloomberg) China July official services PMI dips to six-month low – The growth in China's services sector slipped to a six-month low in July as new orders rose at their weakest rate in at least a year, data showed, taking some of the shine off an industry that has been a bright spot in the Chinese economy this year. The National Bureau of Statistics said the official Purchasing Managers' Index (PMI) for the non-manufacturing sector slowed to 54.2 in July from June's 55. That is the weakest reading since January. A reading above 50 in PMI surveys indicates an expansion in activity, while one below the threshold points to a contraction. The slight retreat in the services sector came at a time when China's factories have started to recover, having earlier this year been one of the drags on growth in the world's second largest economy due to faltering demand at home and abroad. In contrast, China's services companies have held up through each slowdown since PMI records began in January 2007, with the index staying above 50 in every month. (Reuters) Regional Saudia seeks permission to operate in Manila – Saudi Arabian Airlines (Saudia) has sought permission from the Philippine commercial air service regulator to operate international scheduled passenger and cargo services in Manila, according to a filing with the Civil Aeronautics Board (CAB). Saudia has applied for a foreign air carrier permit, the first step in a process that will ultimately require Presidential approval. Meanwhile, the CAB said it has scheduled a hearing for Saudia’s application on August 27, 2014. Under Section 16 of Republic Act 776, the carrier is required to publish a notice of hearing at least once for three consecutive weeks in a newspaper of general circulation. (GulfBase.com) Saudi-Egypt air traffic grows 22% in July – According to experts, air traffic between Saudi Arabia and Egypt grew by 22% in July 2014 and is poised to register higher levels over the next few months. Egypt has been reportedly witnessing a growing movement of Saudi investors since the victory of Abdulfattah El- Sisi in the presidential elections and a visit made by custodian of the two holy mosques King Abdullah bin Abdulaziz. In this context, some 20 Saudi firms have lined up plans to invest SR1.57bn in agro projects in areas ranging 100,000—200,000 feddans. According to the CEO of Egypt Air, Hasan Aziz, private aviation companies in the two countries, such as the Nile, Nasma and Flynas began to operate direct flights between Jeddah and Cairo, which were earlier not allowed to operate between major airports. (GulfBase.com) Fire breaks out at Tasnee manufacturing site – National Industrialization Company (Tasnee) announced that a fire broke out at the manufacturing site of one of its subsidiaries, The National Titanium Dioxide Company (Cristal) in Yanbu on July 25, 2014. The fire was at a temporary material warehouse. The company’s manufacturing operations were temporally halted as a safety precaution owing to the fire. However, the plant resumed operations in the next morning. There were neither injuries nor any material impact on 3Q2014 results and the ability to meet customer demand. Tasnee owns 66% of Cristal. (Tadawul) Saudi pension fund's return falls to 8.1% in 2013 – Saudi Arabia based pension fund, Public Pension Agency (PPA) said

- 4. Page 4 of 5 that it made an 8.1% return on its investments in 2013, down from 9.8% in 2012 despite a strong rise in the stock market. PPA, which manages retirement schemes for Saudi nationals, said in its annual report for 2013 that the return on its investments in the Saudi stock market was 25.7% last year. That compared with a 25.5% rise for the market's main equity index. PPA is one of the major investors in the local equity market, with 32% of its total money in 64 listed companies at the end of 2013. (Reuters) Bahri appoints acting CEO – The National Shipping Company of Saudi Arabia (Bahri) has appointed Mr. Mohammad Omair Alotaibi as its acting CEO in addition to his current job effective August 1, 2014 until the board decides a CEO for the company. Alotaibi is currently serving as Vice Chief Executive Officer for finance at Bahri. (Tadawul) SASCO announces date of releasing cash dividends – Saudi Automotive Services Company (SASCO) announced that the distribution of cash dividends for 1H2014 will start from August 14, 2014 through Al Rajhi Bank, where the dividends will be deposited in current accounts related to investors’ portfolio for eligible shareholders. (Tadawul) Accor signs management agreement with Hiranandani Group – Accor Hotel Services Middle East has signed a management agreement with India-based real estate developer, Hiranandani Group, to develop an ibis Styles hotel in Dubai, located alongside the Business Bay Canal. The hotel is envisioned to have 350 modern-designed rooms, an all-day dining restaurant, a specialty restaurant and bar, lobby lounge, swimming pool, fitness center, and up to three meeting rooms. The design of the ibis Styles Business Bay is under process, with completion expected in mid-2016. (Bloomberg) QIL announces special dividend – Qannas Investments Limited (QIL), a closed-ended investment company managed by ADCM, the investment management arm of Abu Dhabi Financial Group (ADFG), announced that it will pay a special dividend of 11.5 cents per share to shareholders after completing four successful exits with a total value of AED116.7mn. In February 2013, QIL sold its holding in Waha Capital yielding a return of 24% in just four months. In 2Q2013, QIL invested in a plot of land on Reem Island (Abu Dhabi) with permission for residential development at one of the best locations in Abu Dhabi. The company sold the land early in 2014, for almost double the acquisition price. QIL exited its position in RAK Petroleum in December 2013, generating a return of 73% in 21 months. QIL announced in May 2014 that Sheffield Holdings Limited had repurchased its holding in the property in accordance with the original sale and repurchase agreement. QIL, along with the co- investor, received a return of 51% on its investment. QIL has now exited the majority of its investments made with the proceeds from its original fund raise, achieving a cumulative internal rate of return of approximately 35%. (GulfBase.com) Etisalat’s Egypt unit to plan $500mn Cairo IPO – According to sources, Emirates Telecommunications Corporation’s (Etisalat) Egyptian unit, Etisalat Misr, is engaged in talks with banks over an initial public offering (IPO). Etisalat Misr, 66% owned by Abu Dhabi- based Etisalat, has sought proposals from banks to manage the share sale. The IPO is planned for Cairo and may raise about $500mn. (Bloomberg) Abu Dhabi’s hotel market records 11.8% profit increase in 1H2014 – According to data from HotStats, Abu Dhabi hotel profits were up 11.8% in 1H2014. Profits grew on the back off strong top-line performance as occupancy levels grew by 4.9% to 78.2%. Revenue per available room (RevPAR) was up 6.8%, while average available room rates (ARR) were stable in the 1H2014. (AmeInfo.com) Kuwait’s Investment Dar loses protection against creditor legal claims – Kuwait-based Investment Dar said that a local court had ruled to lift protection it had against legal action by creditors. Investment Dar was one of several local financial firms which struggled to refinance debt in the aftermath of the global economic crisis, but was the first to reorganize under Kuwait’s Financial Stability Law – introduced in 2009 to assist debt renegotiations in a country with opaque bankruptcy rules. As part of that legislation, Investment Dar secured a halt to all legal cases being brought against the firm in relation to non-payment of debts to allow it to implement its restructuring. However, the company said in a statement that the July 24 court ruling had stated that legal protection from creditors would be lifted in accordance with the financial stability law. Investment Dar remains committed to repaying all three groups of creditors the total amount of KD440mn under its restructuring plan. (GulfBase.com) Mars Hypermarket opens outlet in Salalah – Mars Hypermarket has opened its outlet in Salalah on August 1, 2014. It is the 11th outlet of Mars International in Oman, located at Al Salam street Salalah. (GulfBase.com) Oman MoTC floats tender for Batinah Express – The Oman Ministry of Transport and Communications (MoTC) has floated another tender package (package eighth) for building the ambitious Batinah Expressway project. According to the tender board website, the tender documents will be distributed until August 28, 2014 and it will open on September 22, 2014. Three contracting firms, including Consolidated Contractors and Larsen & Toubro (Oman), have already bought the documents. The first six main packages have already been floated and are under various stages of planning and construction. The Batinah Expressway, a 265km-long dual four-lane expressway, will connect the Muscat Expressway in the wilayat of Barka to Khatmat Milahah in the wilayat of Shinas. The expressway, which is expected to be completed by 2016, will serve as a new all-weather, 8-lane superhighway extending from Muscat to Khatmat Malaha on Oman's border with the UAE. The project, with an estimated cost of OMR1bn, will provide strong new impetus to economic investment along the North and South Batinah governorates and the hinterland, as well as drive Oman's ambitions to emerge as a logistics gateway to the Gulf region. (GulfBase.com) OAPIL reassessing expansion plans to double capacity – Oman Aluminium Processing Industries (OAPIL), a joint venture between Oman Cables Company and Takamul Investment Company, is re-evaluating its plans to expand its present capacity. OAPIL earlier stated that it was planning to double its capacity to over 100,000 tons per annum (tpa), from 48,000tpa now as per its master plan. OAPIL procures its feedstock, liquid aluminium, from Sohar Aluminium to produce rods and overhead conductors. The company has invested OMR15mn for the present plant. OPAIL has plans to add one more production line with the existing plant, which produces aluminium and alloy rods and overhead conductors for the power industry. (Bloomberg) Oman invites bids for 5 new onshore, offshore blocks – The Omani government has invited local and international oil & gas companies to participate in a new bidding round covering a total of five blocks onshore and offshore of Oman. As part of the Oman Bid Round 2014, offshore Blocks 18 and 59 and onshore Blocks 43A, 54 and 58 are available for bidding. (Bloomberg)

- 5. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 5 of 5 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 QE Index S&P Pan Arab S&P GCC 0.9% (0.1%) (0.1%) 0.1% 0.4% (1.2%) (0.2%) (1.6%) (0.8%) 0.0% 0.8% 1.6% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,293.33 0.0 0.0 7.3 DJ Industrial 16,493.37 0.0 0.0 (0.5) Silver/Ounce 20.33 0.0 0.0 4.4 S&P 500 1,925.15 0.0 0.0 4.2 Crude Oil (Brent)/Barrel (FM Future) 104.84 0.0 0.0 (5.4) NASDAQ 100 4,352.64 0.0 0.0 4.2 Natural Gas (Henry Hub)/MMBtu 3.75 0.0 0.0 (13.7) STOXX 600 331.91 0.0 0.0 1.1 LPG Propane (Arab Gulf)/Ton 100.38 0.0 0.0 (20.5) DAX 9,210.08 0.0 0.0 (3.6) LPG Butane (Arab Gulf)/Ton 115.75 0.0 0.0 (15.2) FTSE 100 6,679.18 0.0 0.0 (1.0) Euro 1.34 0.0 0.0 (2.3) CAC 40 4,202.78 0.0 0.0 (2.2) Yen 102.61 0.0 0.0 (2.6) Nikkei 15,523.11 0.0 0.0 (4.7) GBP 1.68 0.0 0.0 1.6 MSCI EM 1,060.13 0.0 0.0 5.7 CHF 1.10 0.0 0.0 (1.4) SHANGHAI SE Composite 2,185.30 0.0 0.0 3.3 AUD 0.93 0.0 0.0 4.4 HANG SENG 24,532.43 0.0 0.0 5.3 USD Index 81.30 0.0 0.0 1.6 BSE SENSEX 25,480.84 0.0 0.0 20.4 RUB 35.79 0.0 0.0 8.9 Bovespa 55,902.87 0.0 0.0 8.5 BRL 0.44 0.0 0.0 4.7 RTS 1,212.74 0.0 0.0 (15.9) 184.9 158.8 143.1