Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a 14 April Daily market report

Semelhante a 14 April Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

14 April Daily market report

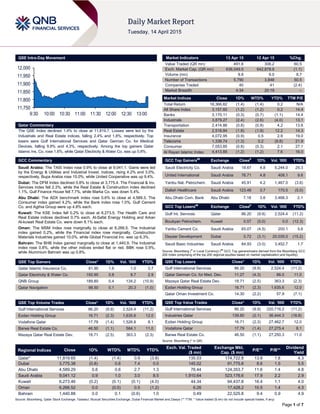

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 1.4% to close at 11,819.7. Losses were led by the Industrials and Real Estate indices, falling 2.4% and 1.8%, respectively. Top losers were Gulf International Services and Qatar German Co. for Medical Devices, falling 9.9% and 4.3%, respectively. Among the top gainers Qatar Islamic Ins. Co. rose 1.6%, while Qatar Electricity & Water Co. was up 0.8%. GCC Commentary Saudi Arabia: The TASI Index rose 0.9% to close at 9,041.1. Gains were led by the Energy & Utilities and Industrial Invest. indices, rising 4.2% and 3.0%, respectively. Bupa Arabia rose 10.0%, while United Cooperative was up 9.4%. Dubai: The DFM Index declined 0.8% to close at 3,775.4. The Financial & Inv. Services index fell 2.3%, while the Real Estate & Construction index declined 1.1%. Gulf Finance House fell 7.7%, while Marka Co. was down 5.4%. Abu Dhabi: The ADX benchmark index rose 0.6% to close at 4,589.3. The Consumer index gained 4.2%, while the Bank index rose 1.0%. Gulf Cement Co. and Agthia Group were up 4.8% each. Kuwait: The KSE Index fell 0.2% to close at 6,273.5. The Health Care and Real Estate indices declined 0.7% each. Al-Safat Energy Holding and Arkan Al-kuwait Real Estate Co. were down 8.1% each. Oman: The MSM Index rose marginally to close at 6,266.5. The Industrial index gained 0.2%, while the Financial index rose marginally. Construction Materials Industries gained 10.0%, while Global Financial Inv. was up 6.3%. Bahrain: The BHB Index gained marginally to close at 1,440.9. The Industrial index rose 0.8%, while the other indices ended flat or red. BBK rose 0.9%, while Aluminium Bahrain was up 0.8%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar Islamic Insurance Co. 81.90 1.6 1.0 3.7 Qatar Electricity & Water Co. 192.90 0.8 8.7 2.9 QNB Group 189.80 0.4 134.2 (10.9) Qatar Navigation 98.50 0.1 20.3 (1.0) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Gulf International Services 86.20 (9.9) 2,524.4 (11.2) Ezdan Holding Group 16.71 (2.3) 1,635.6 12.0 Vodafone Qatar 17.79 (1.4) 1,526.8 8.1 Barwa Real Estate Co. 46.50 (1.1) 584.1 11.0 Mazaya Qatar Real Estate Dev. 18.71 (2.5) 363.3 (2.3) Market Indicators 13 Apr 15 12 Apr 15 %Chg. Value Traded (QR mn) 491.6 306.2 60.5 Exch. Market Cap. (QR mn) 636,049.5 642,878.9 (1.1) Volume (mn) 9.8 9.0 8.7 Number of Transactions 5,790 3,848 50.5 Companies Traded 40 41 (2.4) Market Breadth 4:34 20:19 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,366.82 (1.4) (1.4) 0.2 N/A All Share Index 3,157.60 (1.2) (1.2) 0.2 14.4 Banks 3,170.11 (0.3) (0.7) (1.1) 14.4 Industrials 3,879.27 (2.4) (2.6) (4.0) 13.1 Transportation 2,414.86 (0.8) (0.9) 4.2 13.6 Real Estate 2,518.84 (1.8) (1.9) 12.2 14.3 Insurance 4,072.95 (0.9) 0.5 2.9 19.0 Telecoms 1,339.74 (1.3) 0.2 (9.8) 21.9 Consumer 7,053.85 (0.8) (0.3) 2.1 27.1 Al Rayan Islamic Index 4,413.85 (1.2) (1.2) 7.6 16.0 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Electricity Co. Saudi Arabia 18.67 4.8 5,244.0 25.3 United International Saudi Arabia 76.71 4.8 408.1 9.6 Yanbu Nat. Petrochem. Saudi Arabia 45.91 4.2 1,467.0 (3.6) Dallah Healthcare Saudi Arabia 123.46 3.7 170.5 (5.0) Abu Dhabi Com. Bank Abu Dhabi 7.18 3.6 3,468.3 2.1 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Gulf Int. Services Qatar 86.20 (9.9) 2,524.4 (11.2) Boubyan Petrochem. Kuwait 0.57 (5.0) 0.0 (12.3) Yanbu Cement Co. Saudi Arabia 65.07 (4.5) 200.1 5.6 Deyaar Development Dubai 0.72 (3.1) 20,035.0 (15.2) Saudi Basic Industries Saudi Arabia 84.93 (3.0) 3,452.7 1.7 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Gulf International Services 86.20 (9.9) 2,524.4 (11.2) Qatar German Co. for Med. Dev. 11.27 (4.3) 86.0 11.0 Mazaya Qatar Real Estate Dev. 18.71 (2.5) 363.3 (2.3) Ezdan Holding Group 16.71 (2.3) 1,635.6 12.0 Qatar Oman Investment Co. 14.30 (2.2) 57.9 (7.1) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Gulf International Services 86.20 (9.9) 220,716.2 (11.2) Industries Qatar 139.80 (2.1) 36,444.3 (16.8) Ezdan Holding Group 16.71 (2.3) 27,462.7 12.0 Vodafone Qatar 17.79 (1.4) 27,275.4 8.1 Barwa Real Estate Co. 46.50 (1.1) 27,250.3 11.0 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 11,819.65 (1.4) (1.4) 0.9 (3.8) 135.03 174,722.8 13.8 1.8 4.3 Dubai 3,775.38 (0.8) 0.6 7.4 0.0 145.02 91,775.8 8.6 1.5 5.5 Abu Dhabi 4,589.29 0.6 0.6 2.7 1.3 76.44 124,353.7 11.6 1.4 4.8 Saudi Arabia 9,041.12 0.9 1.0 3.0 8.5 1,910.64 523,176.6 17.9 2.2 2.9 Kuwait 6,273.46 (0.2) (0.1) (0.1) (4.0) 44.34 94,437.8 16.4 1.1 4.0 Oman 6,266.52 0.0 (0.0) 0.5 (1.2) 6.26 17,428.2 10.5 1.4 4.3 Bahrain 1,440.88 0.0 0.1 (0.6) 1.0 0.49 22,525.8 9.4 0.9 4.9 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 11,750 11,800 11,850 11,900 11,950 12,000 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index declined 1.4% to close at 11,819.7. The Industrials and Real Estate indices led the losses. The index fell on the back of selling pressure from GCC shareholders despite buying support from Qatari and non-Qatari shareholders. Gulf International Services and Qatar German Co. for Medical Devices were the top losers, falling 9.9% and 4.3%, respectively. Among the top gainers Qatar Islamic Insurance Co. rose 1.6%, while Qatar Electricity & Water Co. was up 0.8%. Volume of shares traded on Monday rose by 8.7% to 9.8mn from 9.0mn on Sunday. Further, as compared to the 30-day moving average of 7.9mn, volume for the day was 23.2% higher. Gulf International Services and Ezdan Holding Group were the most active stocks, contributing 25.8% and 16.7% to the total volume respectively. Source: Qatar Stock Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Islamic Corporation for the Development of the Private Sector (ICD) Moody’s Saudi Arabia LT IR/ST IR – Aa3/P-1 – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR– Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, IR – Issuer Rating) Earnings Releases Company Market Currency Revenue (mn) 1Q2015 % Change YoY Operating Profit (mn) 1Q2015 % Change YoY Net Profit (mn) 1Q2015 % Change YoY Yanbu National Petrochemical Co. (YANSAB) Saudi Arabia SR – – 364.0 -43.6% 285.1 -48.7% National Company for Glass Industries (ZOUJAJ) Saudi Arabia SR – – 7.6 -1.3% 18.6 25.7% Tourism Enterprise Co. (Shams) Saudi Arabia SR – – 0.8 6.0% 0.6 5.8% Taiba Holding Co. Saudi Arabia SR – – 62.2 5.6% 202.3 240.0% Samba Financial Group (SFG) Saudi Arabia SR – – – – 1,278.0 3.1% Halwani Brothers Co. (HB) Saudi Arabia SR – – 39.1 18.5% 25.9 9.7% United Finance Co. (UFC) Oman OMR 3.0 -1.4% – – 1.1 1.2% Port Services Corporation (PSC) Oman OMR 1.1 -82.8% – – -0.5 NA Oman International Development & Investment Co. (OMINVEST) Oman OMR 22.8 17.2% – – 5.7 26.8% Areej Vegetable Oils & Derivatives (AVOD) Oman OMR 21.5 -13.9% – – 1.0 17.7% Packaging Co Ltd. Oman OMR 2.0 51.7% – – 0.1 NA Al Batnah Hotels Co. Oman OMR 0.4 33.1% – – 0.1 116.6% Shurooq Investment Services Holding Co. (SISCO) Oman OMR 0.0 -67.3% – – -0.1 NA Oman Packaging Co. (OPC) Oman OMR 3.4 13.9% – – 0.1 2,879.6% Computer Stationery Industry (CSI) Oman OMR 0.8 -2.0% – – 0.2 50.9% National Aluminium Products Co. (NAPCO) Oman OMR 6.2 51.9% – – 0.2 3.8% Source: Company data, DFM, ADX, MSM Overall Activity Buy %* Sell %* Net (QR) Qatari 59.48% 50.58% 43,680,169.19 GCC 4.41% 14.72% (50,698,066.55) Non-Qatari 36.12% 34.69% 7,017,897.36

- 3. Page 3 of 7 Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/13 France Banque De France Current Account Balance February -1.8B – -0.2B 04/13 Italy ISTAT Industrial Production MoM February 0.60% 0.50% -0.70% 04/13 Italy ISTAT Industrial Production WDA YoY February -0.20% -1.30% -2.20% 04/13 Italy ISTAT Industrial Production NSA YoY February -0.20% – -5.10% 04/13 China Customs Gen. Admin. Trade Balance CNY March 18.16B 250.00B 370.50B 04/13 China Customs Gen. Admin. Exports YoY CNY March -14.60% 8.20% 48.90% 04/13 China Customs Gen. Admin. Imports YoY CNY March -12.30% -11.30% -20.10% 04/13 China National Bureau of Stat. Trade Balance March $3.08B $40.10B $60.62B 04/13 China National Bureau of Stat. Exports YoY March -15.00% 9.00% 48.30% 04/13 China National Bureau of Stat. Imports YoY March -12.70% -10.00% -20.50% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar Reuters: Qatar ‘most acquisitive’ in Mideast in 1Q2015 – According to a report by Thomson Reuters, Qatar was found to be the most acquisitive nation in the Middle East (Mideast) region accounting for 48% of the Middle Eastern outbound merger and acquisition (M&A) activity during 1Q2015. The largest deal with Middle Eastern M&A involvement during 1Q2015 was the $1.9bn offer for the remaining stake in Canary Wharf Group by Stork Holdings, jointly owned by the Qatar Investment Authority and Brookfield Property Partners. The report stated that M&A were active during 1Q2015 in the Mideast region, while outbound M&A drove activity, up 161% from 1Q2014 to reach $4bn, the highest first quarter total since 2011. Reuters said the acquisitions by the UAE and Saudi Arabian companies accounted for 27% and 14% respectively of the Middle Eastern outbound M&A, adding industrials was the most active sector, representing 33% of the M&A involving Middle East. (Gulf-Times.com) IDC: Qatar IT market set for fast growth – According to the International Data Corporation (IDC), Qatar’s IT services market is changing at a rapid pace. Qatar is expected to lead IT services spending in the region through 2018. According to IDC’s latest forecast, the combined IT services market of some of the countries in the region, including Qatar, Oman, Bahrain, and Kuwait, is expected to expand at a compound annual growth rate (CAGR) of 12.5% over the coming years to total $1.82bn in 2018. The global advisory services firm expects this growth to be driven by government–led infrastructure development projects, e-government initiatives, transformations in the transportation and banking & financial services sectors, and private sector developments as governments in the region pursue diversification strategies into non-oil sectors. IDC is the premier global provider of market intelligence and advisory services. (Peninsula Qatar) Doha Metro could reduce annual CO2 emissions – Qatar Rail Managing Director Abdulla Abdulaziz Al-Subaie said Doha Metro could potentially reduce annual CO2 emissions by 258,000 tons. He said the project will also facilitate a saving of 2mn km of travel (by vehicles) a day. Al-Subaie reiterated the transport firm’s plans to hold regular stakeholder engagement summits as it is aims to transform Qatar into a “smart city” using integrated transportation solutions. He underscored Qatar Rail’s role in the economic, social, human, and development of Qatar, as well as its role in employment generation. (Gulf-Times.com) MRDS to disclose 1Q2015 results on April 27 – Mazaya Qatar Real Estate Development Company (MRDS) will announce its financial results for 1Q2015 on April 27, 2015. (QSE) International Fitch affirms US AAA rating on financial flexibility – Fitch Ratings has affirmed the AAA credit rating for the US, citing the strength of the nation’s economy, capital markets and status as the issuer of the world’s reserve currency. Fitch said the outlook for the rating is stable. The rating agency said that the economic growth in the US has been faster than that in most of the developed economies, and the nation benefits from its diversity and technological advancements, bolstered by strong institutions and a favorable business climate. Fitch added that the budget deficit, which has narrowed from a peak of $1.4tn in 2009 to $483.3bn in 2014, is expected to continue to shrink in 2015 and 2016, though reforms for mandatory spending and taxation measures will be needed to prevent increases after 2018. (Bloomberg) ECB bond-buying slows as QE enters second month – The European Central Bank (ECB) bought €9.159bn worth of government bonds in the fifth week of its quantitative easing (QE) program, a slower pace than a week earlier and below the average amount needed to keep the program on track. Having made a smooth start to its QE program, the lackluster amount purchased this week is unlikely to set alarm bells ringing. Under the QE program, which started in early March 2015, the ECB aims to purchase €60bn of securities a month (bonds, ABS and covered bonds) until September 2016 or beyond, that if needed to see a sustained adjustment in the inflation path back toward the ECB's target of just under 2%. (Reuters) EC VP: EU working with Italy to solve bad loan issue – The European Commission (EC) Vice President (VP), Valdis Dombrovskis said that the commission is helping Italy find solutions to its bad bank loans, raising hopes that Rome's efforts to solve one of its biggest economic problems is not being ignored in Brussels. He said the EU's executive body was also working with other capitals over how to help the region's banks offload piles of non-performing loans. Italy has around €186bn of bad loans. Meanwhile, he said Greece is not moving fast enough to draw up and implement structural reforms and there is limited time to prevent it running out of cash. An April 9 meeting of deputy finance ministers, called the Euro Working Group, gave Athens a deadline of six working days to present a revised economic reform plan, before eurozone finance ministers meet on April 24 to decide whether to unlock emergency funding to keep Greece afloat. (Reuters) BoJ sees economy improving region by region, keeps upbeat view – The Bank of Japan (BoJ), in a quarterly report, raised its economic assessment for three of Japan's nine regions, signaling that the benefits of its stimulus program was broadening. The central bank kept its optimistic assessment for

- 4. Page 4 of 7 the remaining six regions intact, stressing that solid demand at home and overseas are underpinning the output and job market. The BoJ Governor Haruhiko Kuroda said that Japan's economy is likely to continue recover moderately as a trend. The central bank will issue fresh long-term economic and inflation forecasts at the next rate review on April 30, 2015. (Reuters) S&P: India's fiscal improvements vulnerable to shocks – International rating agency Standard and Poor's (S&P) warned that India's hard-won fiscal improvements could fail to withstand an external shock, given ‘less than rock solid’ public finances that pose a concern for its sovereign rating profile. The rating agency lauded India's efforts to increase capital expenditure by more than 25% in 2015-16, versus an average rise of 5.4% since 2011-12. However, it expressed concerns that the spending plans could also be hit if India failed to raise the amount targeted from the sale of stakes in state-run firms. India, constrained by a modest average income level and the government's weak fiscal position, has a BBB- rating from S&P, with a "stable" outlook. Meanwhile, India’s consumer price inflation unexpectedly slowed to a three-month low in March, rising 5.17% YoY, which could encourage the central bank to deliver another off-cycle interest rate cut to boost economic recovery. (Reuters) Regional Abraaj closes $990mn sub-Saharan Africa fund – Emerging- market focused private equity firm Abraaj Group has closed a $990mn sub-Saharan Africa fund, which is its third in the region. European and North American investors committed 64% of the capital in the Abraaj Africa Fund III, with funding from global institutional investors, pension funds and sovereign wealth funds adding up to 76%. (Reuters) Thomson Reuters: Mideast M&A deals reaches $9.5bn in 1Q2015 – According to the Thomson Reuters’ quarterly investment analysis on the region, mergers & acquisitions (M&A) deals in the Middle East (Mideast) have registered $9.5bn in 1Q2015. Although this is less than half the value registered during 4Q2014, it marks a 152% increase over 1Q2014 and the best annual start since 2012. Thomson Reuters’ MENA Managing Director, Nadim Najjar said Mideast equity and equity-related issuance totaled $2.5bn during 1Q2015, 59% less than the value recorded during 4Q2014. (Bloomberg) Bloomberg: Saudi Aramco mega deals boost EMEA Islamic loans to $7.1bn – The slump in oil prices since June 2014 has not dampened the appetite for Shari’ah-compliant credit in the Gulf region. According to data compiled by Bloomberg, loan deals worth around $4bn from Saudi Arabian Oil Company and its joint venture Rabigh Refining & Petrochemical Co. have fueled the busiest ever start to the year for Islamic borrowing in Europe, the Middle East and Africa. Loans worth $7.1bn have been raised so far in 2015 as compared to around $3bn for the same period in 2014. The increase in borrowing highlights how companies in the oil producing GCC region are maintaining investments even after oil prices dropped about 50% since June 2014. Shari’ah-compliant lenders are taking a bigger role in regional deals as the global Islamic finance industry’s assets are expected to almost double by 2018. (Bloomberg) Petro Rabigh BoD recommends capital rise through right issue – Rabigh Refining & Petrochemical Company’s (Petro Rabigh) board of directors has recommended a capital increase of SR7.04bn through rights issue shares. Through this capital increase, the company aims to finance the Rabigh Phase II project. The ownership of the Phase II Project was transferred from the founding shareholders Saudi Aramco and Sumitomo Chemical to Petro Rabigh. The rights issue is subject to necessary approvals. Shareholders registered at the close of trading on the day of the extraordinary general meeting will be eligible. (Tadawul) CDSI: Saudi non-oil exports dropped 19.9% in February 2015 – According to the Central Department of Statistics & Information (CDSI), Saudi Arabia’s imports rose 1.6% YoY in February 2015, while non-oil exports dropped 19.9%. Non-oil exports traditionally account for around 12% of the country’s overall exports. As per the latest report by Jadwa Investment, the value of non-oil exports declined in January 2015, reflecting an impact of lower prices, since volumes exported recorded a monthly increase to 3.9mn tons in January 2015 from 3.7mn tons in December 2014. Similarly, imports in January fell by 9.4% MoM and 9.1% YoY. During February 2015, government deposits and reserves fell by SR30bn and SR100bn, respectively. (GulfBase.com) Cayan Group reveals AED3.1bn property projects in Dubai, Riyadh – Saudi-based property developer Cayan Group has unveiled property projects worth AED3.1bn in Dubai and Riyadh. The company’s latest portfolio of projects includes residential properties in Dubai and a commercial tower in Riyadh. Earlier in 2015, the company launched a branded residential tower and hotel apartment named ‘Cayan Cantara’ in Dubai, which will be completed by 2018. The project, which is located on Umm Suqeim Road, will have a 38-storey hotel apartment complex and a 42-storey residential tower. Cayan Cantara will have retail shops, restaurants, a spa, an outdoor screen and a conference hall. (Bloomberg) ARB net profit declines 10.96% YoY in 1Q2015 – Al Rajhi Bank (ARB) reported SR1.52bn net profit in 1Q2015, reflecting a decline of 10.96% YoY. The bank’s total assets grew 11.25% YoY to SR320.43bn in 1Q2015. Loans & advances reached SR205.16bn, showing an increase of 6.25% YoY, while customer deposits amounted to SR265.60bn. EPS stood at SR0.93 in 1Q2015 as against SR1.05 in 1Q2014. (Tadawul) SABB reports SR1.12bn net profit in 1Q2015 – The Saudi British Bank (SABB) reported SR1.12bn net profit in 1Q2015 as compared to SR1.1bn in 1Q2014. The bank’s total assets grew 8.41% YoY to SR190.16bn in 1Q2015. Loans & advances reached SR120.43bn, showing an increase of 9.58% YoY, while customer deposits stood at SR149bn. EPS amounted to SR0.74 in 1Q2015 as against SR0.72 in 1Q2014. (Tadawul) DSE awarded AED334mn MEP contract – Drake & Scull Engineering (DSE), the engineering subsidiary of Drake & Scull International (DSI), has been awarded a contract worth AED334mn for MEP works (mechanical, electrical, and plumbing) for an upcoming hotel and residences building to be constructed on the Palm Jumeirah in Dubai. Under the agreement’s terms, DSE will complete the supply, installation, and handover of detailed MEP works for the hotel by 2016. The upscale project located on the man-made island consists of three separate buildings of G+7 floors and will include a 360- room five star hotel and two residential buildings. (DFM) DPR partners with Picsolve for AED100mn image capture deal – Dubai Parks & Resorts (DPR) and Picsolve International have entered into an image capture agreement. This partnership will create one of the world’s largest photography integrations, with Picsolve managing a full-range of image requirements for the multibillion-dollar leisure destination taking shape in Dubai. The agreement, which is expected to bring AED100mn in revenues over a five-year period, sees Picsolve managing a full- range of digital, video and image capture solutions that will allow guests to enjoy a seamless photo record of their visit. (DFM)

- 5. Page 5 of 7 Dubai launches Mohammed bin Rashid Fund for SMEs – Dubai SME has launched the new Mohammad Bin Rashid Fund for SMEs, a government initiative established by a law issued by HH Shaikh Mohammad Bin Rashid Al Maktoum, the Ruler of Dubai. The fund aims at maximizing financing solutions for innovative businesses while developing Emirati entrepreneurs. The fund’s assets surpass AED600mn and offer Emirati nationals between 21 and 65 years old two types of loans: The seed capital loan, offered directly to start-ups that require funding of more than AED50,000 but not exceeding AED500,000, and the credit scheme loan, offered through banking partners to both start-ups and existing businesses requiring funds in excess of AED500,000, but not exceeding AED5mn. (GulfBase.com) DEWA to invest AED30bn to rise solar capacity, seeks involvement in Egypt – The Dubai Electricity & Water Authority’s (DEWA) Managing Director & CEO, Saeed Al Tayer said that the company will invest AED30bn to increase the power capacity of Shaikh Mohammad Bin Rashid Al Maktoum Solar Park. Currently, the park is generating 13 megawatts (MW) of electricity. He said the solar park is one of the largest renewable energy projects in the region with a planned capacity of 1,000 MW by 2019 produced at a cost of AED12bn and by the completion phase in 2030, its capacity will be increased up to 3,000 MW at a cost of AED30bn. Meanwhile, DEWA is also is looking to participate in energy projects in Egypt and keen to lend its expertise. (GulfBase.com) JLL: Dubai housing prices fall slightly in 1Q2015 – According to a report by Jones Lang LaSalle (JLL), housing prices in Dubai fell slightly and rents were flat in 1Q2015 as compared to 4Q2014. As per the report, Dubai’s real estate sector has been among the most volatile globally over the past decade, swinging from boom to bust to boom again. Prices recovered to near peak values after falling by about half from their 2008 highs, but are now weakening again. JLL said, apartment sale prices fell 2% in 1Q2015 versus 4Q2014. Villa sale prices dropped 1%, while rental values for both villas and apartments were flat. JLL estimated that around 730 residential units were delivered in Dubai in 1Q2014, with an additional 22,000 to be handed over by 2015-end. Dubai had 379,000 residential units as of March 31, 2015. In the hotel sector, average daily room rates fell 5% YoY to $273 in the 12 months to February 2015, while occupancy rates edged down to 86% from 88%. Combined, this led to a 7% drop in revenue per available room to $235. (Reuters) Marka completes Retailcorp acquisition – Marka Company has completed its acquisition of Retailcorp UAE, a subsidiary of Istithmar, a Dubai World company. The acquisition has been funded by a blend of Marka’s own collateral and bank facilities. Earlier in December 2014, Marka entered into an agreement to acquire the company in a deal valued at around AED220mn. Marka will invest in Retailcorp’s existing business with a goal to achieve double digit growth over the next 12-18 months. (GulfBase.com) DCCI members’ 1Q2015 exports reaches AED76.1b – Exports of Dubai Chamber of Commerce & Industry’s (DCCI) members in March 2015 reached an all-time high of AED28.1bn, pushing the total export value for the 1Q2015 to AED76.1bn for the first time. The exports increased 8% from AED70.3bn recorded in 4Q2014 and rose 7% from the AED71.1bn in 1Q2014. The number of Certificates of Origin issued by Dubai Chamber also increased to a total of 228,000, up 8% YoY. Dubai Chamber’s active exporters in 1Q2015 reached 8,231, represented a 3% increase over both 4Q2014 and 1Q2014. (Gulf-Base.com) AFNIC’s OGM approves 10% dividend – Al Fujairah National Insurance Company’s (AFNIC) ordinary general meeting (OGM) has approved the distribution of 10% dividend for the financial year ended December 31, 2014. (ADX) Mubadala GE Capital: No plans to change shareholdings – Mubadala GE Capital, a venture between Abu Dhabi state fund Mubadala and GE Capital, said that its ownership would remain unchanged despite General Electric's (GE) decision to divest from its finance unit. Earlier on April 10, 2015, GE said that it would shed most of GE Capital and return as much as $90bn to shareholders as it became a simpler industrial business instead of an unwieldy hybrid conglomerate of banking and manufacturing. (Reuters) IFA joins Morgans in $545mn Dubai Palm apartment project – Kuwait’s IFA Hotels & Resorts Co. plans to build luxury hotel apartments on the Palm Jumeirah man-made island in Dubai that will be managed by Morgans Hotel Group of New York. According to IFA’s CEO for the Middle East Khaled Saeed Esbaitah, the mixed-use development, set to cost $545mn will include 110 hotel apartments that will be managed under Morgans’ Delano brand. An additional 190 apartments will be sold. (Bloomberg) DIDI’s AGM approves 18% cash dividend – Dhofar International Development & Investment Holding Company’s (DIDI) annual general meeting (AGM) has approved the distribution of 18% cash dividend (18 baizas per share) for the financial year ended December 31, 2014. (MSM) Oman Tribune: 11 firms in race for Musandam IPP contract – Oman Tribune reported that a total of 11 companies are in the race to secure a key consultancy contract for the 120 megawatts (MW) Musandam Independent Power Project (IPP) in Oman. Earlier in February 2015, Oman Power & Water Procurement Company (OPWP) floated a tender to select the consultant who will have to provide the project management & technical consultancy services for the IPP. A joint venture between Oman Oil Company and LG International, Musandam Power Company, aims to set up a dual-fuel fired power plant at Tibat in Musandam, which is expected to be operational by 2016-end. (GulfBase.com) Sur steel plant considering Duqm for relocating project – Sun Metals’ Operations Director P T Sivarajan said that the plant may be shifted to Duqm, if the promoters do not receive permission from the government for mid-sea unloading of imported scrap. Sun Metals is the developer of 2.5mn ton per annum steel plant in Sur. (GulfBase.com) PDO to lift oil output by 5% in four years – Petroleum Development Oman’s (PDO) Managing Director, Raoul Restucci said that the company is aiming to lift its crude oil output by about 5% over the next four years. He said the company seeks to reach 600,000 barrels per day (bpd) by 2019 and would then maintain that production level for 10 years. PDO's planned average output for 2015 is 570,000 bpd. (Reuters) GFH gets shareholders’ nod for capital reduction, name change – Gulf Finance House’s (GFH) extraordinary general meeting (EGM) has approved the proposed elimination of accumulated losses through a reduction in the GFH’s issued and paid-up capital. The capital reduction will be effected at a ratio of 6 shares per each 10 shares held at a nominal value of $0.265 per share; thus eliminating $897mn of accumulated losses. As a result, the share capital will be reduced from $1.49bn divided into 5.64bn shares to $598mn divided into 2.256bn shares. Shareholders decided to continue with listing the bank’s GDRs on the London Stock Exchange (LSE) and the

- 6. Page 6 of 7 Kuwait Stock Exchange (KSE) and authorized the board of directors to adopt the necessary resolutions. The EGM also approved the BoD’s proposal to change the commercial name of the company from ‘Gulf Finance House’ to ‘GFH Financial Group B.S.C.’. (Bahrain Bourse) Jawad Business raises $235mn refinancing loan – Bahrain- based Jawad Business Group has raised a $235mn loan to refinance existing debt. The firm has borrowed $215mn through a term loan in an amortizing structure, which will last for between five and six years, and the rest through a revolving facility. (GulfBase.com)

- 7. Contacts Saugata Sarkar Ahmed Al-Khoudary Sahbi Kasraoui Head of Research Head of Sales Trading – Institutional Head of HNI Tel: (+974) 4476 6534 Tel: (+974) 4476 6548 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 200.0 220.0 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 QSE Index S&P Pan Arab S&P GCC 0.9% (1.4%) (0.2%) 0.0% 0.0% 0.6% (0.8%) (1.8%) (1.2%) (0.6%) 0.0% 0.6% 1.2% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,198.89 (0.7) (0.7) 1.2 MSCI World Index 1,772.08 (0.4) (0.4) 3.7 Silver/Ounce 16.28 (1.1) (1.1) 3.7 DJ Industrial 17,977.04 (0.4) (0.4) 0.9 Crude Oil (Brent)/Barrel (FM Future) 57.93 0.1 0.1 1.0 S&P 500 2,092.43 (0.5) (0.5) 1.6 Crude Oil (WTI)/Barrel (FM Future) 51.91 0.5 0.5 (2.6) NASDAQ 100 4,988.25 (0.2) (0.2) 5.3 Natural Gas (Henry Hub)/MMBtu 2.56 0.5 0.5 (14.6) STOXX 600 413.63 0.1 0.1 5.6 LPG Propane (Arab Gulf)/Ton 54.00 0.9 0.9 10.2 DAX 12,338.73 (0.4) (0.4) 9.5 LPG Butane (Arab Gulf)/Ton 59.75 1.3 1.3 (4.8) FTSE 100 7,064.30 (0.3) (0.3) 1.3 Euro 1.06 (0.3) (0.3) (12.7) CAC 40 5,254.12 0.2 0.2 7.5 Yen 120.13 (0.1) (0.1) 0.3 Nikkei 19,905.46 (0.0) (0.0) 13.3 GBP 1.47 0.3 0.3 (5.8) MSCI EM 1,041.46 0.7 0.7 8.9 CHF 1.02 0.1 0.1 1.7 SHANGHAI SE Composite 4,121.71 2.1 2.1 27.2 AUD 0.76 (1.2) (1.2) (7.2) HANG SENG 28,016.34 2.7 2.7 18.7 USD Index 99.49 0.2 0.2 10.2 BSE SENSEX 29,044.44 0.3 0.3 7.0 RUB 52.28 (2.4) (2.4) (13.9) Bovespa 54,239.77 (0.9) (0.9) (7.7) BRL 0.32 (1.5) (1.5) (15.1) RTS 1,004.62 0.5 0.5 27.1 169.8 134.9 122.8