From Luxury Escort Service Kamathipura : 9352852248 Make on-demand Arrangemen...

10 September Daily market report

1. Page 1 of 7

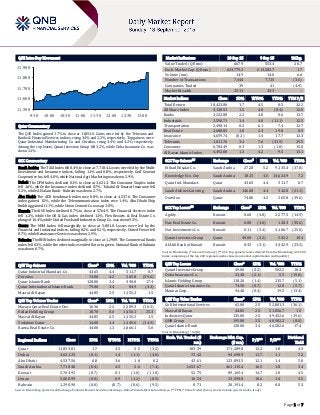

QSE Intra-Day Movement

Qatar Commentary

The QSE Index gained 1.7% to close at 11,853.0. Gains were led by the Telecoms and

Banks & Financial Services indices, rising 3.4% and 2.2%, respectively. Top gainers were

Qatar Industrial Manufacturing Co. and Ooredoo, rising 4.4% and 4.2%, respectively.

Among the top losers, Qatari Investors Group fell 3.2%, while Doha Insurance Co. was

down 2.1%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.4% to close at 7,718.4. Losses were led by the Multi-

Investment and Insurance indices, falling 1.1% and 0.8%, respectively. Gulf General

Cooperative Ins. fell 4.0%, while National Agri. Marketing was down 2.9%.

Dubai: The DFM Index declined 0.1% to close at 3,621.3. The Consumer Staples index

fell 1.6%, while the Insurance index declined 0.7%. Takaful Al-Emarat Insurance fell

5.2%, while Al Salam Bank – Bahrain was down 2.7%.

Abu Dhabi: The ADX benchmark index rose 0.8% to close at 4,537.6. The Consumer

index gained 1.5%, while the Telecommunication index rose 1.4%. Abu Dhabi Ship

Building gained 11.1%, while Union Cement Co. was up 3.8%.

Kuwait: The KSE Index declined 0.7% to close at 5,764.9. The Financial Services index

fell 1.2%, while the Oil & Gas index declined 1.1%. Flex Resorts & Real Estate Co.

plunged 16.4%, while United Foodstuff Industries Group Co. was down 9.5%.

Oman: The MSM Index fell marginally to close at 5,801.0. Losses were led by the

Financial and Industrial indices, falling 0.2% and 0.1%, respectively. United Power fell

8.7%, while Renaissance Services was down 2.9%.

Bahrain: The BHB Index declined marginally to close at 1,290.9. The Commercial Banks

index fell 0.1%, while the other indices ended flat or in green. National Bank of Bahrain

was down 0.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Industrial Manufact. Co. 43.65 4.4 511.7 0.7

Ooredoo 74.80 4.2 265.8 (39.6)

Qatar Islamic Bank 120.00 3.4 390.8 17.4

Qatar International Islamic Bank 79.00 3.4 84.9 (3.3)

Masraf Al Rayan 44.85 2.5 1,155.2 1.5

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 16.36 2.2 2,289.3 (10.3)

Ezdan Holding Group 18.70 0.6 1,456.1 25.3

Masraf Al Rayan 44.85 2.5 1,155.2 1.5

Vodafone Qatar 14.00 1.4 1,149.6 (14.9)

Barwa Real Estate Co. 44.00 1.3 1,066.1 5.0

Market Indicators 10 Sep 15 9 Sep 15 %Chg.

Value Traded (QR mn) 667.9 553.4 20.7

Exch. Market Cap. (QR mn) 623,779.2 613,583.7 1.7

Volume (mn) 14.9 14.0 6.6

Number of Transactions 7,444 7,725 (3.6)

Companies Traded 39 41 (4.9)

Market Breadth 25:11 35:3 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,423.80 1.7 4.5 0.5 12.2

All Share Index 3,138.51 1.5 4.0 (0.4) 12.8

Banks 3,222.88 2.2 4.8 0.6 13.7

Industrials 3,590.71 1.4 4.0 (11.1) 12.5

Transportation 2,490.14 0.2 6.1 7.4 12.7

Real Estate 2,688.85 1.0 2.3 19.8 8.9

Insurance 4,659.74 (0.1) 1.4 17.7 12.3

Telecoms 1,011.76 3.4 7.6 (31.9) 29.5

Consumer 6,784.49 0.3 1.3 (1.8) 15.8

Al Rayan Islamic Index 4,492.00 1.3 4.2 9.5 13.1

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Etihad Etisalat Co. Saudi Arabia 27.28 5.2 9,135.4 (37.8)

Knowledge Eco. City Saudi Arabia 18.15 4.6 14,624.9 7.2

Qatar Ind. Manufact. Qatar 43.65 4.4 511.7 0.7

Saudi Airlines Catering Saudi Arabia 146.68 4.4 342.8 (21.1)

Ooredoo Qatar 74.80 4.2 265.8 (39.6)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Agility Kuwait 0.60 (4.8) 2,277.5 (14.9)

Nat. Real Estate Co. Kuwait 0.08 (3.6) 120.3 (35.6)

Nat. Investments Co. Kuwait 0.11 (3.4) 4,106.7 (25.0)

Qatari Investors Group Qatar 49.00 (3.2) 502.2 18.4

Al Ahli Bank of Kuwait Kuwait 0.32 (3.1) 4,342.9 (23.2)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200

Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Qatari Investors Group 49.00 (3.2) 502.2 18.4

Doha Insurance Co. 23.48 (2.1) 5.5 (19.0)

Islamic Holding Group 118.20 (1.4) 215.7 (5.1)

Qatar Islamic Insurance Co. 74.50 (0.7) 12.0 (5.7)

Mannai Corp. 94.40 (0.4) 19.5 (13.4)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Gulf International Services 62.00 2.5 52,801.3 (36.1)

Masraf Al Rayan 44.85 2.5 51,056.7 1.5

Industries Qatar 135.00 2.5 49,452.6 (19.6)

QNB Group 195.80 2.5 48,902.2 (8.0)

Qatar Islamic Bank 120.00 3.4 46,582.6 17.4

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded ($

mn)

Exchange Mkt. Cap.

($ mn)

P/E** P/B**

Dividend

Yield

Qatar 11,853.01 1.7 4.5 2.5 (3.5) 183.39 171,289.8 12.2 1.8 4.3

Dubai 3,621.25 (0.1) 1.4 (1.1) (4.0) 72.42 94,698.9 11.7 1.1 7.2

Abu Dhabi 4,537.56 0.8 3.6 1.0 0.2 43.61 123,893.5 12.1 1.4 5.0

Saudi Arabia 7,718.40 (0.4) 4.5 2.6 (7.4) 1,653.67 461,115.4 16.5 1.8 3.4

Kuwait 5,764.92 (0.7) 0.1 (1.0) (11.8) 52.75 89,165.4 14.7 1.0 4.5

Oman 5,800.99 (0.0) 0.9 (1.2) (8.5) 10.54 23,590.8 10.6 1.4 4.5

Bahrain 1,290.90 (0.0) (0.7) (0.6) (9.5) 0.71 20,191.4 8.2 0.8 5.3

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,500

11,600

11,700

11,800

11,900

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index gained 1.7% to close at 11,853.0. The Telecoms and Banks &

Financial Services indices led the gains. The index rose on the back of

buying support from non-Qatari and GCC shareholders despite selling

pressure from Qatari shareholders.

Qatar Industrial Manufacturing Co. and Ooredoo were the top gainers,

rising 4.4% and 4.2%, respectively. Among the top losers, Qatari Investors

Group fell 3.2%, while Doha Insurance Co. was down 2.1%.

Volume of shares traded on Thursday rose by 6.6% to 14.9mn from 14.0mn

on Wednesday. Further, as compared to the 30-day moving average of

7.2mn, volume for the day was 106.8% higher. Mazaya Qatar Real Estate

Development and Ezdan Holding Group were the most active stocks,

contributing 15.3% and 9.7% to the total volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

09/10 US Bureau of Labor Statistics Import Price Index YoY August -11.40% -11.10% -10.50%

09/10 US Department of Labor Initial Jobless Claims 5-September 275K 275K 281K

09/10 US Bloomberg Bloomberg Consumer Comfort 6-September 41.4 – 41.4

09/10 US Census Bureau Wholesale Inventories MoM July -0.10% 0.30% 0.70%

09/10 US Census Bureau Wholesale Trade Sales MoM July -0.30% 0.10% 0.40%

09/11 US Bureau of Labor Statistics PPI Ex Food, Energy, Trade MoM August 0.10% 0.10% 0.20%

09/11 US Bureau of Labor Statistics PPI Final Demand YoY August -0.80% -0.90% -0.80%

09/11 US Bureau of Labor Statistics PPI Ex Food, Energy, Trade YoY August 0.70% 0.70% 0.90%

09/11 US US Treasury Monthly Budget Statement August -$64.4B -$73.5B -$128.7B

09/10 France INSEE Industrial Production YoY July -0.80% 0.70% 0.70%

09/10 France INSEE Manufacturing Production YoY July -1.30% 0.70% 0.20%

09/11 France Banque De France Current Account Balance July -0.4B – 0.8B

09/11 Germany Destatis Wholesale Price Index MoM August -0.80% – 0.10%

09/11 Germany Destatis Wholesale Price Index YoY August -1.10% – -0.50%

09/10 UK Royal Institution of Chartered RICS House Price Balance August 53% 46% 44%

09/10 UK Bank of England BOE Asset Purchase Target September 375B 375B 375B

09/10 UK Bank of England Bank of England Bank Rate 10-September 0.50% 0.50% 0.50%

09/11 UK ONS Construction Output SA MoM July -1.00% 0.50% 0.90%

09/11 UK ONS Construction Output SA YoY July -0.70% 0.90% 2.60%

09/11 Spain INE CPI Core MoM August 0.10% – -1.00%

09/11 Spain INE CPI Core YoY August 0.70% – 0.80%

09/11 Italy ISTAT Industrial Production WDA YoY July 2.70% 0.90% -0.30%

09/11 Italy ISTAT Industrial Production NSA YoY July 2.70% – 2.90%

09/10 China National Bureau of Statistics CPI YoY August 2.00% 1.80% 1.60%

09/10 China National Bureau of Statistics PPI YoY August -5.90% -5.60% -5.40%

09/10 China National Bureau of Statistics Foreign Direct Investment YoY CNY August 22.00% – 5.20%

09/11 China The People's Bank of China Money Supply M2 YoY August 13.30% 13.30% 13.30%

09/11 China The People's Bank of China Money Supply M0 YoY August 1.80% 3.00% 2.90%

09/11 China The People's Bank of China Money Supply M1 YoY August 9.30% 6.80% 6.60%

09/11 China National Bureau of Statistics New Yuan Loans CNY August 809.6B 850.0B 1,480.0B

09/11 China National Bureau of Statistics Aggregate Financing CNY August 1,080.0B 1,000.0B 718.8B

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 48.40% 68.63% (135,137,250.99)

GCC 15.91% 6.93% 59,974,199.14

Non-Qatari 35.69% 24.44% 75,163,051.85

3. Page 3 of 7

News

Qatar

FTSE upgrades Qatar’s emerging market status – FTSE Russel, the

global leader in indexing, has upgraded the Qatari market to the

Secondary Emerging Market. Following its September 2015 annual

review, FTSE announced Qatar would be promoted from the

Frontier to the Secondary Emerging Market since it meets the

criteria required for the upgrade. Qatar has already been upgraded

by two other global index compilers MSCI and S&P, in May 2014

and September 2014, respectively. Qatar, along with 10 other

markets, including China and Kuwait, were placed in the FTSE

watch list to be considered for the September 2015 market

classification review for the upgrade at different levels. Of this, just

three markets found their places in the upgraded list. While China

A-Shares remained on Watch List for possible inclusion as the

Secondary Emerging, Kuwait failed to be included in the list this

time. The FTSE Emerging Markets Indices are a part of the FTSE

Global Equity Series (GEIS). The index helps investors analyze the

performance of the most liquid companies in emerging markets.

The index includes several large and mid-cap stocks from

advanced and secondary emerging markets. China had the highest

weight age (26.6%) in this index, followed by Taiwan (14.1%) and

India (12.6%). (Peninsula Qatar)

QSE suspends trading of GWCS shares on September 13 – The Qatar

Stock Exchange (QSE) has suspended trading of Gulf Warehousing

Company’s (GWCS) shares on September 13, 2015 due to the

company’s EGM being held during the day. (QSE)

14 new malls in MERS Qatar expansion strategy – Al Meera

Consumer Goods Co. (MERS) is pursuing an expansion strategy to

construct around 14 new shopping malls across Qatar even as the

retail major opened its 40th state-of-the-art outlet in Al Wajba

recently. The company’s ambitious plan is to open 56 outlets in

different areas of Qatar. MERS deputy CEO Dr. Mohamed Nasser al-

Qahtani said the company is committed to provide a unique and

all-inclusive service to all segments of the Qatari community and

looks forward to the opening of new outlets, which is a way of

supporting Qatar National Vision. He explained that the new

branch would be serving the Al Wajba area, in addition to the New

Rayyan, Muaither, Rawdat Abal Heeran, and Al Sailiya until the

completion of the new branches in those areas. The 4,300-square

meter (sqm) Al Wajba branch constitutes 2,022 sqm of

supermarket area. Al-Qahtani said MERS would launch two more

branches in 2015 at Al Thumama and Rawdat Ekdeem, which will

open its doors weeks apart after obtaining the necessary

approvals and licenses from authorities. (Gulf-Times.com)

Milaha appoints Abdulrahman Essa al-Mannai as president & CEO –

Qatar Navigation (Milaha) has appointed Abdulrahman Essa al-

Mannai as the President and Chief Executive Officer with effect

from September 12, 2015. Al-Mannai previously led the

commercial planning & allocation functions at Qatargas. He will

succeed Khalifa Ali al-Hetmi, who had previously announced his

plan to retire. (Gulf-Times.com)

Low oil prices not to affect Qatar mega mall – Mall of Qatar Deputy

Managing Director Shem Krey said he sees no risk to the $1bn

project from the low oil prices and expects to have signed up

retailers for all the space by 2015-end. The mall, next to the

stadium that is due to host the 2022 FIFA World Cup, is set to open

in August 2016, hosting 500 stores, including a Carrefour

hypermarket. (Reuters)

ORDS: Qatar building ‘smart’ stadiums – Ooredoo (ORDS) Chief

New Business Officer Sheikh Nasser bin Hamad bin Nasser al-

Thani has said that Qatar is building world-class smart stadiums

that will transform the experience of watching and attending

sporting events. Speaking at the Soccerex Global Convention 2015

held in England, Sheikh Nasser said Ooredoo’s vision will support

the creation of next generation of stadiums, which will deploy the

latest network technology to transform the experience of watching

sport. (Gulf-Times.com)

Kahramaa meets high demand for electricity – Qatar General

Electricity & Water Corporation (Kahramaa) has said that it

managed to meet an increased demand for electricity in the

summer, especially during the holy month of Ramadan and Eid al-

Fitr, through the National Control Centre. In a statement,

Kahramaa said the growth in demand was due to the high

temperature witnessed during the period mentioned above.

Besides, the statement noted that the maximum system demand

recorded in June and July was 6,890 megawatt (MW) (June 6) and

6,985 MW (July 29), respectively. (Gulf-Times.com)

D&B: Qatar 3Q2015 business outlook stays strong despite BOI

drops in previous quarters – According to a recent report by Dun &

Bradstreet (D&B), the outlook for the overall business

environment in Qatar remains strong despite the decline in the

composite Business Optimism Index (BOI) over the last two

quarters. The 3Q2015 BOI report, conducted by D&B and

sponsored by the Qatar Financial Centre (QFC), shows that

although planned expansion activities have lost some traction in

both the hydrocarbon and non-hydrocarbon sectors, the overall

business environment outlook still remains strong. The

construction sector forecast declined from a BOI of 46 in 2Q2015

to 34 in 3Q2015 on the back of competition, drying up of new

projects and reduced business activity during the summer season.

This ‘off-season’ also saw the composite BOI for the trade &

hospitality sector reach its second lowest level in six years,

dropping from 28 in 2Q2015 to 6 in 3Q2015. The outlook for the

finance, real estate and business services sector also revealed a

weaker third quarter with a 15-point decrease, from 49 in 2Q2015

to 34 in 3Q2015. Despite the decline in scores for the transport &

communications sector, expectations over securing new projects

and orders in the coming quarter remained firm. (Gulf-Times.com)

Moody’s: Barwa Bank gains foothold in Qatar’s growing Islamic

banking sector – According to a report released by Moody’s

Investors Service, state-owned Barwa Bank has found its niche in

Qatar’s growing Islamic banking sector, benefiting from the

country's strong economy and favorable operating environment.

The bank’s loan book grew 19% in 2014 as compared with 13%

for the system. Moody's expects it to grow by 10-15% in 2015.

Nevertheless, the bank’s asset quality may remain stable over the

next 12 to 18 months, with any weakening in the credit quality of

borrowers to be limited by the supportive operating environment.

Assistant Vice President – Analyst at Moody’s Arif Bekiroglu said

continued high public spending would continue to create further

business opportunities for local banks, particularly those with

well-established government links like Barwa. Furthermore,

Barwa would benefit from regulators’ policies, which prohibit

conventional financial institutions operating Shari’ah-compliant

banking windows and reduce the competition for a fast-growing

customer segment. (Moody’s)

Al Futtaim-Voltas Qatar JV wins QR500mn MEP contract at Doha

Festival City – Al Futtaim Engineering’s Hamad & Mohamad Al

Futtaim and Voltas Qatar have been awarded a QR500mn contract

related to the Doha Festival City project. The joint venture (JV)

bagged the mechanical, electrical and plumbing (MEP) contract for

Doha Festival City Mall, which is expected to be completed by

2016. Doha Festival City Mall, with a gross leasable area of around

250,000 square meters will comprise of 550 outlets, including 85

restaurants and cafes, VOX Cinemas and a snow park. It will

feature around 8,000 parking spaces. (Bloomberg)

4. Page 4 of 7

New projects reaffirm Qatar 2030 plan on course – Qatar News

Agency (QNA) has reported that the Supreme Council for

Economic Affairs & Investment has decided to construct 2,000

villas spread over 2.5 million square meters in south Doha at an

estimated cost of QR10bn in four years. The decision reaffirms that

Qatar National Vision 2030 is on course as per the directives of

Qatar’s Emir HH Sheikh Tamim bin Hamad Al-Thani. ‘Al Sharq’

daily newspaper said that the construction of villas would spur the

real estate sector by attracting developers, investors and benefit

private companies. (Bloomberg)

Early salary payments for Eid al-adha – According to Qatar News

Agency (QNA), the government will pay the salaries of its

employees, retirees and beneficiaries of social security on

September 20, 2015 on account of Eid al-Adha. (Gulf-Times.com)

International

US consumer sentiment drops in September to lowest level in a year

– US consumer sentiment declined in September to the lowest

level in a year as Americans anticipated a weaker economy in the

face of a global slowdown and turbulent financial markets. The

University of Michigan’s preliminary index dropped to 85.7 from

an August reading of 91.9, the largest one-month decline since the

end of 2012. Households were less upbeat than a few months

earlier about future growth in employment and wages, while 73%

of respondents reported hearing of negative economic

developments. The sentiment survey’s current conditions index,

which measures Americans’ assessment of their personal finances,

decreased to an 11-month low of 100.3 from a 105.1 in August.

The measure of expectations six months from now fell to 76.4, the

weakest in a year, from 83.4. With the turmoil in global markets,

consumers will need to see continued strength in employment in

order to stay positive on the economy. (Bloomberg)

BoE keeps rate on hold, unfazed by overseas risks – The Bank of

England (BoE) has said that its rate-setters felt the threat to the

world economy from China’s stock-market slump did not signal a

slowdown for Britain, as they left interest rates at a record-low of

0.5% on September 10. Policy makers voted 8-1 to keep rates

unchanged as expected. They broadly agreed with Governor Mark

Carney, who has said that so far, China’s slowdown is unlikely to

derail the plan to gradually raise British rates. The BoE’s decision

followed a month of declines on global stock markets, driven by

financial turmoil in China and signs of some weakness in Britain’s

economic recovery. However, a minority of policy makers saw a

danger that near-zero inflation could rise faster than forecasted

and exceed its 2% target in a couple of years, suggesting they

would not take much more persuading to back a rate hike. The

central bank staff trimmed their forecast for 3Q2015 growth to

0.6% from 0.7%, roughly in line with Britain’s average rate of

growth. (Reuters)

China central bank enhances reserve requirement flexibility –

China’s central bank is making its reserve requirement rules more

flexible for banks to reduce the risk of an abrupt tightening in

liquidity in the world’s second-largest economy as it cools. The

People’s Bank of China (PBOC) said the amount of deposits that

banks must set aside as reserves at the central bank would soon be

regulated on an average basis as opposed to current daily

assessments. The change, effective from September 15, would help

banks combat sudden funding pressures at a time of heightened

volatility in the yuan that has driven capital from China. Under the

changes, banks can report a daily reserve requirement ratio (RRR)

that is up to 100 basis points lower than the rate set by the PBOC,

but their daily average RRR in the assessed period cannot fall

under the required level. The PBOC said the new rule would allow

banks to set aside less reserves when they are strapped for funds,

but would not be a free pass for lenders to lapse into overdrafts.

(Reuters)

CBR holds rate as economic woes mount – The Central Bank of

Russia (CBR) left its main lending rate on hold as expected on

Friday, for now putting concerns about stubbornly high inflation

before worries about a slumping economy. The bank left its policy

rate unchanged at 11%, following five successive cuts in 2015 that

have reduced the rate by six percentage points after an emergency

hike to 17% in December 2014. The decision to hold rates steady

underscores the harsh policy dilemmas facing Russia as it

simultaneously grapples with rising double-digit inflation and an

economy in the throes of its deepest slump since 2009. The bank

predicted that oil prices would remain around $50 per barrel for at

least the next three years, and saw annual GDP returning to

growth only in 2017. CBR forecasted GDP would decline by 3.9-

4.4% in 2015 and by 0.5-1% in 2016, revising down previous

forecasts. (Reuters)

Regional

ABCC: UAE ranks first among Arab countries in attracting FDI – The

UAE has ranked first among Arab countries in attracting Foreign

Direct Investment (FDI), which amounted to $10.1bn in 2014,

followed by Saudi Arabia and Egypt at $8bn and $4.8bn,

respectively. According to the Arab-Brazilian Chamber of

Commerce (ABCC), the total FDI flowing to the Arab world stood at

$43.9bn during 2014. The GCC region has received almost half of

the resources that were invested in the Arab world in 2014. On the

other hand, the Arab countries made FDIs worth $33.4bn in total.

Kuwait was the biggest investor in the region with an investment

of $13mn during 2014. (GulfBase.com)

ANB Insurance approves SR53.8mn insurance policy for ANB staff –

MetLife AIG ANB Cooperative Insurance Company (ANB

Insurance) has approved the issuance of a health insurance policy

for the Arab National Bank (ANB) staff at an annual premium of

SR53.8mn. The policy, which is set to start on September 17, will

remain active for a 12-month period, while the financial impact of

this will be reflected in the financial results of 3Q2015. (Tadawul)

SAMA to appoint KPMG partner as Deputy Governor for supervision

– According to sources, the Saudi Arabian Monetary Agency

(SAMA) is set to appoint KPMG Saudi Arabia’s Managing Partner

Tareq al-Sadhan as its new Deputy Governor for supervision.

(Reuters)

Saudi Aramco signs contract with Azmeel to build staff homes –

State-owned Saudi Arabian Oil Company (Saudi Aramco) is

planning to build 8,521 homes for its employees, as well as schools

and community facilities, on 10-square kilometers of land in

Dhahran. Saudi Aramco has signed a contract with Saudi-based

Azmeel Contracting to build the first 955 housing units. The

contract for the remaining 1,821 dwellings in Phase I of the South

Dhahran Home Ownership Program (SDHOP) is expected to be

awarded later in 2015. (GulfBase.com)

Saudi ICT sector spending may exceed SR138bn by 2017 – The

Ministry of Interior (MoI) has announced that the Kingdom of

Saudi Arabia will serve as the Official Country Partner for GITEX

Technology Week 2015 – the largest technology event in the

Middle East, Africa, and South Asia. Saudi Arabia’s information &

communications technology (ICT) sector has expanded

significantly over the past 10 years and remains on a strong

growth trajectory. Over the next five years, the ICT market is

expected to expand at a CAGR of 8.1% to exceed SR138bn in 2017.

According to a report by IDC & Mobily, public sector investment in

ICT will play a key role in Saudi Arabia’s nationwide digital

transformation, with the Kingdom’s public sector IT spending set

to grow by 44% from 2014-2017. (GulfBase.com)

5. Page 5 of 7

NCB: Saudi may record largest fiscal deficit in 2015 – According to

the National Commercial Bank (NCB), Saudi Arabia is expected to

reel under its largest fiscal deficit in 2015 because of a sharp

decline in oil prices and higher spending. NCB said the break-even

oil price needed for the Gulf Kingdom to balance its budget

through 2015 is around $91.9 per barrel, however actual crude

prices could be as low as $65 per barrel. The sharp fall in oil prices

is projected to depress Saudi Arabia’s actual revenue by a huge

29% to SR741bn in 2015 from SR1,044bn in 2014. Actual

spending is expected to shrink by only around 7% to SR1,032bn in

2015 from SR1,109bn in 2014. As a result, the actual deficit could

peak at an all-time high of SR290bn in 2015, over quadruple the

2014 gap of SR65.5bn. Experts said the 2015 deficit would be

Saudi Arabia’s highest fiscal gap since the largest Arab economy

began exporting oil in commercial quantities decades ago.

Announcing its budget for 2015, Saudi Arabia projected revenue at

SR715bn and expenditure at SR860bn, leaving a forecast shortfall

of SR145bn. (GulfBase.com)

Rights option still open for Aabar Investments – RHB Capital

Managing Director Datuk Khairussaleh Ramli has said that Aabar

Investments cannot be ruled out from the Malaysian Ringgit 2.5bn

rights issue being called by RHB Capital. Although it has not given

its commitment for the rights, it can still subscribe to its portion at

the entitlement date. RHB Investment Bank, Affin Hwang

Investment Bank, CIMB Investment Bank, Credit Suisse Securities

(Malaysia), Maybank Investment Bank and Public Investment

Bank have committed to underwrite 250.8mn shares representing

around 48.45% of the rights Issue. The remaining 266.9mn rights

shares, representing 51.55% of the total rights shares, are the

entitlements of the Employees Provident Fund Board and OSK

Holdings, the substantial shareholders of RHB Capital, for which

they have provided written undertakings to subscribe in full for

their respective entitlements. Consequently, bankers say that it

would be difficult for Aabar to continue to maintain its stake in the

bank, which currently stands at 21.09%, if it continues to receive

cash as opposed to reinvesting its monies under the RHB Capital

dividend reinvestment plan. (GulfBase.com)

Aramex, Orascom Telecom in talks to build logistics areas in Egypt –

Aramex has confirmed that it is in discussions with Orascom

Telecom Media and Technology Holding to create five logistics

areas in Egypt. However, Aramex has not signed any agreement

related to this matter. (DFM)

DEWA’s AED250mn substation construction on track – Dubai

Electricity & Water Authority (DEWA) has said that it is

progressing according to the plan with the construction of the

400/132kV substation at the Mohammed bin Rashid Al Maktoum

Solar Park. The project includes supplying, installing, testing and

commissioning the 400/132kV substation with four 400kV cables.

Around 30% of the project’s engineering work has been

completed. The substation is being built at a cost of AED250mn

and has a 505 megavolt amperes (MVA) transmission capacity,

and is due to be completed by November 2016. Another substation

with the same capacity will be built to transmit the solar energy of

the Solar Park, which is expected to reach 3,000 megawatt by

2030. (Bloomberg)

Union Properties seeks $123mn loan to fund project – Union

Properties is in talks with a UAE bank to borrow up to around

$123mn to fund a 271-unit project in the Emirate. Union

Properties said that it will also launch a tender for the construction

contract of its Oia residential development in October 2015. Union

Properties General Manager Ahmad al-Marri predicted that this

would be awarded in January or February 2016. He said the loan is

likely to be signed in mid-2016, while the Oia project will be

finished in 2018. (Reuters)

Kuwait to buy 28 Eurofighters jets for $9bn – Kuwait has signed an

MoU to buy 28 Eurofighter jets in a deal worth up to $9bn. The

Eurofighter aircraft are produced by Italy’s Finmeccanica, BAE

Systems and Airbus. According to sources, the 20-year-long deal

with Kuwait would be finalized in a few weeks. Reportedly, Kuwait

is also continuing separate negotiations with the US government

for buying 24 Boeing Co F/A-18E/F Super Hornets, a deal valued

at over $3bn. (Reuters)

Kuwait signs KD116mn solar energy project with Spanish group –

Kuwait has signed a KD116mn contract with Spain-based TSK

Group for a 50 megawatt (MW) solar energy project as part of its

renewable energy drive. Kuwait has a multi-billion-dollar plan to

meet 15% of power demand from renewable sources by 2030. The

country is targeting to produce 4,500 MW from solar and wind

energy by 2030 when demand is expected to rise to 30,000 MW

from the current 12,000 MW. The latest project is due to start

production in December 2017, while two smaller projects of 10-

MW capacity each are expected to come on stream in May 2016

and July 2016. The initial three projects have been funded by the

government but future ones will be awarded to the private sector

on a Build-Operate-Transfer basis. When complete, the project will

meet the electricity demand of 100,000 homes and save about

12.5mn barrels of oil equivalent per year. (Gulf Times) page no. 3

Al Jazeira Services receives offer to sell 36.99% stake in Al Anwar

Ceramics Tiles – Al Jazeira Services has received a preliminary

offer to sell its entire stake, which is 36.99% in Al Anwar Ceramics,

at a price of 370 baizas per share. Following the approval and

acceptance of the offer, the acquirer would commence requisite

legal, financial and commercial due diligence. The company’s

board will meet on September 15, 2015 to discuss the offer. (MSM)

Orpic’s GDP impact to rise to 9% by 2018 – Oman Oil Refineries &

Petroleum Industries Company (Orpic) is expecting to witness its

contribution to the economy boosted to around 8-9% of the GDP

(equivalent to $6.5bn in value terms) in 2018, when a trio of big-

ticket projects is scheduled for completion. This compares with a

current contribution of 6% as of 2014, equivalent to a GDP impact

annualized value of $4.2bn. The company is investing an estimated

$8bn in three ‘strategic growth projects’ that will effectively triple

the value of its asset base. (GulfBase.com)

Zain, Uber announce partnership across Middle East – Zain Group

has entered into a group-wide agreement with Uber to offer Zain

customers discounted and preferential services when using the

Uber platform. The joint agreement is the first of its kind in the

region, and already has been effective and operational in Bahrain,

Jordan and Saudi Arabia. Preferential services will soon be

launched in Kuwait for Zain customers. The agreement will see

Uber choosing Zain as its mobile launch partner and main mobile

service provider for any new future Uber service in any country,

where Zain operates. Uber is an American international

transportation network company. (Bahrain Bourse)

Batelco signs key WiFi agreement – Bahrain Telecommunication

Company (Batelco) has signed an agreement with the Capital

Municipal Council to deploy the latest communications

technologies in Bahrain. Under the agreement, Batelco will install

WiFi hotspots at a number of locations throughout the Capital

Governorate to serve the public. (GulfBase.com)

BFH signs agreement with JLL – The Bahrain Financial Harbour

(BFH) has signed an agreement appointing JLL as its strategic

leasing advisor. The partnership will highlight the property’s many

unique features and advantages to regional and international

organizations looking to relocate, or set up operations in the GCC.

(BNA)

Seera Investment Bank sells Kosan Crisplant for $63.5mn –

Bahrain’s Seera Investment Bank has sold Kosan Crisplant to a

6. Page 6 of 7

regional strategic buyer for $63.5mn. Kosan Crisplant is a

Denmark-based provider of systems and solutions for filling and

reconditioning liquefied petroleum gas (LPG) cylinders.

(Bloomberg)

7. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial

Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or

recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect

losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore

strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS

believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and

completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or

contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the

views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions

included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

QSE Index S&P Pan Arab S&P GCC

(0.4%)

1.7%

(0.7%)

(0.0%) (0.0%)

0.8%

(0.1%)

(1.2%)

(0.6%)

0.0%

0.6%

1.2%

1.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,107.78 (0.3) (1.4) (6.5) MSCI World Index 1,626.99 0.1 2.0 (4.8)

Silver/Ounce 14.61 (0.5) 0.2 (6.9) DJ Industrial 16,433.09 0.6 2.1 (7.8)

Crude Oil (Brent)/Barrel (FM Future) 48.14 (1.5) (3.0) (16.0) S&P 500 1,961.05 0.4 2.1 (4.8)

Crude Oil (WTI)/Barrel (FM Future) 44.63 (2.8) (3.1) (16.2) NASDAQ 100 4,822.34 0.5 3.0 1.8

Natural Gas (Henry Hub)/MMBtu 2.66 (1.6) (0.2) (11.0) STOXX 600 355.72 (0.3) 2.6 (2.6)

LPG Propane (Arab Gulf)/Ton 44.62 (0.3) 3.2 (8.9) DAX 10,123.56 (0.1) 2.7 (3.7)

LPG Butane (Arab Gulf)/Ton 57.00 (0.4) 1.8 (13.0) FTSE 100 6,117.76 (0.7) 2.8 (7.7)

Euro 1.13 0.5 1.7 (6.3) CAC 40 4,548.72 (0.3) 2.4 (0.2)

Yen 120.59 (0.0) 1.3 0.7 Nikkei 18,264.22 (0.3) 1.2 3.6

GBP 1.54 (0.1) 1.7 (1.0) MSCI EM 802.49 (0.2) 1.8 (16.1)

CHF 1.03 0.4 0.2 2.6 SHANGHAI SE Composite 3,200.23 0.1 1.0 (3.7)

AUD 0.71 0.3 2.7 (13.2) HANG SENG 21,504.37 (0.3) 3.2 (8.9)

USD Index 95.19 (0.3) (1.1) 5.5 BSE SENSEX 25,610.21 0.1 2.2 (11.3)

RUB 68.00 0.4 (0.7) 12.0 Bovespa 46,400.50 (1.4) (1.3) (36.7)

BRL 0.26 (0.5) (0.7) (31.5) RTS 799.10 (0.2) 0.7 1.1

141.9

118.3

113.4