Top Rated Pune Call Girls Viman Nagar ⟟ 6297143586 ⟟ Call Me For Genuine Sex...

Base metals price forecast updated

1. Updated Base Metals Price Forecast

Slower start to 2012 before prices regain traction

Commodities Research, 7 December 2011

Bombed out aluminium prices to prevail for a while longer before supply cuts improve balance

Copper prices expected to average above USD 8,000/tonne amid continued supply deficit

Nickel market continues to struggle with oversupply, but supply risks remain to the downside

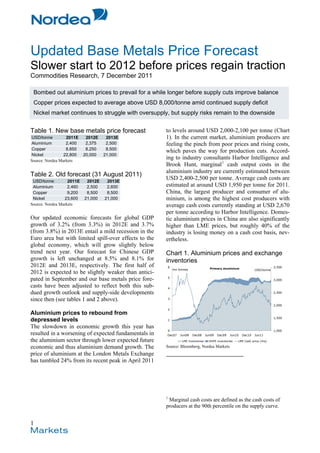

Table 1. New base metals price forecast to levels around USD 2,000-2,100 per tonne (Chart

USD/tonne 2011E 2012E 2013E 1). In the current market, aluminium producers are

Aluminium 2,400 2,375 2,500 feeling the pinch from poor prices and rising costs,

Copper 8,850 8,250 8,500

which paves the way for production cuts. Accord-

Nickel 22,800 20,000 21,000

Source: Nordea Markets

ing to industry consultants Harbor Intelligence and

Brook Hunt, marginal 1 cash output costs in the

aluminium industry are currently estimated between

Table 2. Old forecast (31 August 2011)

USD/tonne 2011E 2012E 2013E

USD 2,400-2,500 per tonne. Average cash costs are

Aluminium 2,460 2,500 2,600 estimated at around USD 1,950 per tonne for 2011.

Copper 9,200 8,500 8,500 China, the largest producer and consumer of alu-

Nickel 23,600 21,000 21,000 minium, is among the highest cost producers with

Source: Nordea Markets average cash costs currently standing at USD 2,670

per tonne according to Harbor Intelligence. Domes-

Our updated economic forecasts for global GDP tic aluminium prices in China are also significantly

growth of 3.2% (from 3.3%) in 2012E and 3.7% higher than LME prices, but roughly 40% of the

(from 3.8%) in 2013E entail a mild recession in the industry is losing money on a cash cost basis, nev-

Euro area but with limited spill-over effects to the ertheless.

global economy, which will grow slightly below

trend next year. Our forecast for Chinese GDP Chart 1. Aluminium prices and exchange

growth is left unchanged at 8.5% and 8.1% for inventories

2012E and 2013E, respectively. The first half of 6 Primary aluminium 3,500

mn tonnes USD/tonne

2012 is expected to be slightly weaker than antici-

5

pated in September and our base metals price fore- 3,000

casts have been adjusted to reflect both this sub- 4

dued growth outlook and supply-side developments 2,500

since then (see tables 1 and 2 above). 3

2,000

2

Aluminium prices to rebound from

1,500

depressed levels 1

The slowdown in economic growth this year has

0 1,000

resulted in a worsening of expected fundamentals in Dec07 Jun08 Dec08 Jun09 Dec09 Jun10 Dec10 Jun11

the aluminium sector through lower expected future LME inventories SHFE inventories LME Cash price (rhs)

economic and thus aluminium demand growth. The Source: Bloomberg, Nordea Markets

price of aluminium at the London Metals Exchange

has tumbled 24% from its recent peak in April 2011

1

Marginal cash costs are defined as the cash costs of

producers at the 90th percentile on the supply curve.

1

2. balanced aluminium market for the next couple of

years, with risks to the outlook largely balanced.

Robust demand growth to be driven by China Current aluminium prices are considered too low

Global end user aluminium demand has stalled, but compared to current operating costs and to our ex-

demand for primary aluminium has remained firm. pectations for the global operating rate, which

The exception is in Europe where physical premi- should remain in the 85-87% range. Prices are

ums have started to come down from elevated lev- therefore expected to average higher than current

els. We have lowered our aluminium demand forward prices over the next two years. We pencil

growth forecast for 2012E to 5.7% (7.7%) but leave in average prices of USD 2,375 (USD 2,500) per

our 2013E growth forecast unchanged at 6.5%. The tonne and USD 2,500 (USD 2,600) per tonne for

decent demand outlook is underpinned by robust 2012E and 2013E, respectively.

demand growth from China of around 10-11%.

Demand is expected to be boosted by aluminium Chart 2. Aluminium forecast versus market

price competitiveness and penetration in the trans- USD/tonne LME Primary Aluminium probability range

Based on implied volatilities in the options market

5,000

portation sector. Growing urbanisation, income and

4,500

market share in automotive, aerospace, electrical,

4,000

electronics and solar energy support robust demand 3,500

growth in the coming years, albeit at a slower pace 3,000

2,500

than previously estimated. 2,500

2,375

2,000

Supply under pressure by poor profitability 1,500

1,000

Global aluminium output has come under intense

500

pressure from poor prices and sticky production

0

costs. However, historically high physical premi- Dec07 Dec08 Dec09 Dec10 Dec11 Dec12 Dec13

ums paid on top of LME prices provide some offset 90% Confidence 95% Confidence LME price

Forward market Nordea Forecast

for producers. Output fell to a 6-month low in Oc- Source: Bloomberg, Nordea Markets

tober according to official figures from the Interna-

tional Aluminium Institute (IAI) as production in Copper prices to reflect continued deficit

China decreased sharply. The pipeline for capacity Copper prices peaked in early February this year at

expansions outside China looks relatively dry and is prices above USD 10,000 per tonne as the funda-

heavily dependent on expansions in India where mental outlook pointed to an increasing supply

output has disappointed already. Chinese planned deficit. However, lack of seasonal restocking by

expansions are decent, but could be hurt by poor Chinese buyers during the spring, who instead

profitability and power-related constraints amid turned to drawing on inventories amid historically

China’s recurring power shortages. According to high prices, tight credit conditions and a closed “ar-

China Electricity Council, the current power short- bitrage window” to import LME based copper, re-

age could last until next spring, but may be allevi- sulted in prices trending lower. Meanwhile, global

ated by the recently announced hike in power prices economic growth slowed, reducing actual and ex-

and cap on coal prices from January. This neverthe- pected copper demand from China and the rest of

less puts upwards pressure on Chinese production the world. LME copper prices tumbled 33% from

costs by an estimated USD 60 per tonne for smelt- the February peak to the recent low in early Octo-

ers without self-generated power. Although current ber (USD 6,785 per tonne), but currently trade

prices incentivise production cuts, especially in around USD 7,800-7,900 per tonne (Chart 3).

China, we expect that prices must remain at current

depressed levels for a while before we see cuts. The industry marginal (90th percentile) cash cost is

Shutting down and restarting production is costly, estimated by consultants Brook Hunt at USD 4,000

high premiums provide offset, costs can come per tonne while the most expensive mine operations

down further and history has shown that prices require almost USD 8,000 per tonne. Prices above

must trade at current levels on the cost curve (50th this “threshold” should therefore only be justified in

percentile) for a sustained period before cuts are a market characterised by deficit, ie refined supply

made. falling short of refined usage resulting in stock

draws. According to the latest data from the Inter-

Bottom line: Capacity is expected to expand at a national Copper Study Group (ICSG), the market

slightly higher pace than demand next year, with was in a production deficit of 161k tonnes (1%) for

the opposite being true for 2013E. We see a largely

2

3. the first eight months of 2011 versus a deficit of per consumption as the power and construction sec-

339k tonnes for the same period of 2010. World tors constitute more than half of total consumption.

demand grew by 1% during this period, while mine We expect Chinese consumption to grow at around

production continued to underperform relative to 7% p.a. the coming two years and expect consump-

capacity with production during the first eight tion per capita to reach levels above those of Eu-

months of 2011 practically unchanged from last rope and North America as early as 2013E. Histori-

year. Production at three of the four largest produc- cally, world real GDP growth of 1% corresponds to

ers (Chile, Peru and the United States) fell by an copper consumption growth of 1.2% (see Nordic

aggregated 4% despite record high copper prices Metals & Mining, 5 October 2011, Nordea Equity

(Chart 4). Research). We expect demand to converge to this

historical relationship after a break-out on the up-

Chart 3. Copper prices and exchange in- side in 2010 and to the downside in 2011E, imply-

ventories ing around 4% y/y global demand growth in both

900

Copper

11,000 2012E and 2013E.

'000 tonnes USD/tonne

800 10,000

700 9,000 Supply expansions look comfortable in theory

600 8,000 Repeated labour strikes, adverse weather condi-

500 7,000

tions, operational problems and lower ore head

400 6,000

grades have become the norm rather than the ex-

300 5,000

ception for copper supply in recent years. 2011 has

200 4,000

been no exception to this “rule” and the ISCG ex-

pects a production deficit of about 200k tonnes for

100 3,000

2011. The project pipeline looks, on paper, rela-

0 2,000

Dec07 Jun08 Dec08 Jun09 Dec09 Jun10 Dec10 Jun11 Dec11 tively comfortable, with expansions at existing

LME inventories SHFE inventories mines (brownfield) and new plants (greenfield)

Comex inventories LME Cash price (rhs)

Source: Bloomberg, Nordea Markets

planned to come on stream the coming few years.

Copper mine production is highly concentrated

Chart 4. Chilean copper ore and concen- given that Americas (mainly Chile, Peru and the

US) and Asia constitute roughly 75% of global out-

trates production continues to disappoint

put. Of the 10 largest copper mines in the world, six

6.5

Chile Copper ore and concentrates production

are Chilean. Judging by production plans for the

6.0

Chilean mines alone, they would manage to meet

mn tonnes, annualised

the expected demand increase by themselves. How-

5.5

ever, copper output tends to fall short of guidance

levels and we expect history to repeat itself.

5.0

Bottom line: ICSG expects an increase in refined

4.5 copper production of 3.4% in 2012E compared to

the producers’ expansion plans of roughly 9%

4.0 growth (1.5m tonnes). We share the view of the

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

ICSG and expect a production deficit to emerge

5y range 2011 2010 5 year avg also in 2012E for a third year in a row. We expect a

Source: Bloomberg, World Bureau of Metals Statistics, Nordea Mar- nearly balanced market in 2013E. Due to a slightly

kets

weaker economic development in the start of 2012,

we have lowered our average price forecast for

Demand to pick up from low 2011-levels

2012E from USD 8,500 per tonne to USD 8,250 per

World copper refined usage is expected to grow by

tonne, but keep our forecast for 2013E at USD

1.5-2% y/y this year after 2010’s strong 7.1% y/y

8,500 per tonne.

growth. China will continue to be the driver of de-

mand growth in the coming years as urbanisation

and industrialisation continue. China will have to

import roughly one-fourth of its copper needs,

meaning that Chinese stocking cycles will remain a

key price driver for the foreseeable future. We also

expect China’s current 5-year plan to support cop-

3

4. Chart 5. Copper forecast versus market Slower demand growth in 2012E, but stronger

USD/tonne LME Copper probability range

Based on implied volatilities in the options market

2013E

20,000

Slower economic growth and industrial production

18,000

in the first half of 2012 than previously forecast

16,000

14,000

will most likely result in lower nickel demand

12,000

growth next year. INSG’s late September forecast

10,000

8,250 8,500

of 6% demand growth for both 2011E and 2012E is

8,000 considered too optimistic, in our view. We factor in

6,000 demand growth of around 5% this year, falling to

4,000

3% next year before climbing to around 9% in

2,000

2013E.

0

Dec07 Dec08 Dec09 Dec10 Dec11 Dec12 Dec13

90% Confidence

Forward market

95% Confidence

Nordea Forecast

LME price Chart 6. Nickel prices and exchange inven-

Source: Bloomberg, Nordea Markets tories

180 Nickel

35,000

'000 tonnes USD/tonne

Nickel prices threatened by supply glut 160

30,000

Nickel has been the underperformer among base 140

25,000

metals this year on expectations of steady supply 120

additions this year and in 2012. Nickel prices 100 20,000

peaked in February above USD 29,000 per tonne, 80 15,000

but currently trades around USD 18,000 per tonne 60

(Chart 6). As stainless steel production accounts for 10,000

40

roughly two-thirds of global nickel consumption, 5,000

20

the slowdown in stainless steel production in the

0 0

second half of the year has put pressure on refined Dec07 Jun08 Dec08 Jun09 Dec09 Jun10 Dec10 Jun11

nickel demand. At the same time, China’s nickel LME inventories LME Cash price (rhs)

pig iron (NPI) industry, an alternative nickel feed- Source: Bloomberg, Nordea Markets

stock for stainless steel production, churned out

record-high amounts. Chinese net imports of re- Supply pipeline impressive on paper

fined nickel have therefore remained low this year, On paper, the expected nickel supply pipeline looks

while imports of nickel ore and concentrates to feed overwhelming, but disruptions and delays have

the NPI production have skyrocketed. Recently, been a constant feature for the industry. Production

however, these producers are getting squeezed out growth is partly dependent on highly complex pro-

of the market as nickel prices have fallen below the jects, which makes delays likely, in our view. The

cost of NPI production, which is estimated by con- International Nickel Study Group (INSG) latest es-

sultants Brook Hunt in the range of USD 19,000- timates point to a supply increase of around 9% in

20,000 per tonne. Moreover, 90% of global nickel 2012E, which is roughly in line with our own esti-

supply operates cash positively at price levels mates. However, this figure does not include any

around USD 15,000 per tonne. general adjustment factor for possible disruptions,

implying that risks to supply are skewed to the

Despite the sluggish price development, record- downside.

high refined nickel production in September and

NPI ramp-up in China, visible exchange inventories Bottom line: Coupled with our demand expecta-

of refined nickel have declined steadily by a total of tion, the strong supply pipeline translates into an

33% since the start of the year (Chart 6). We expect expected supply surplus the coming two years. We

that some of the excess material has been shipped therefore expect prices to continue to be determined

into China and may be stored away in off-market by the costs of the marginal producers. Further-

bonded warehouses. Nevertheless, LME nickel more, we pencil in a slightly lower price assump-

stocks will begin 2012 at the lowest starting level in tion for 2012E of USD 20,000 per tonne (USD

three years. 21,000 per tonne) due to weaker demand expecta-

tions for the start of the year. We nevertheless keep

our previous forecast of USD 21,000 per tonne for

2013E.

4

5. Chart 7. Nickel forecast versus market and business and consumer confidence has eroded,

USD/tonne LME Nickel probability range

Based on implied volatilities in the options market

which could pave the way for an upside surprise to

economic growth. There is also probably pent-up

50,000

metals demand for instance in the United States

40,000 where construction activity remains at depressed

levels. Stronger monetary and fiscal policy easing

30,000

by China would most likely boost metals demand

20,000

20,000 21,000

growth from the world’s largest consumer. How-

ever, implementation of substantial easing meas-

10,000 ures is most likely to be reactive rather than pre-

emptive, in our view, if growth should falter more

0

Dec07 Dec08 Dec09 Dec10 Dec11 Dec12 Dec13 than currently anticipated.

90% Confidence 95% Confidence LME price

Forward market Nordea Forecast

Source: Bloomberg, Nordea Markets

Risks to our outlook Bjørnar Tonhaugen

Forecasting metals prices in the current environ- bjornar.tonhaugen@nordea.com +47 2248 7959

ment is very difficult as the macroeconomic uncer-

tainty is perceived to be heightened. Industrial met-

als demand is highly cyclical and sensitive to

changes in economic growth prospects. The sensi-

tivity of demand to GDP growth is highest for

nickel and aluminium, and lowest for copper. Nev-

ertheless, small changes to the economic outlook

could have relatively large implications for ex-

pected metals demand and thereby the expected

market balance. Our forecast described above must

therefore be viewed as our “best estimate” corre-

sponding to our baseline forecasts for global eco-

nomic growth.

The largest downside risks to our outlook are pre-

dominantly demand-side related. The debt crisis in

the Euro-zone, if not properly contained, may have

large spill-over effects to the global economy

mainly through the financial sector. A so-called

“hard landing” in the Chinese economy, for exam-

ple instigated by a burst of the property and credit

“bubble” is another known risk. Chinese residential

floor space for sale has mushroomed lately as prop-

erty demand has fallen markedly. Anecdotal evi-

dence points to a liquidity crunch among property

developers. If property prices fall sharply, private

construction may be cut back and China’s demand

for raw materials and industrial metals will drop

substantially.

Upside risks to our outlook include stronger eco-

nomic growth than envisaged. Expectations are low

Nordea Markets is the name of the Markets departments of Nordea Bank Norge ASA, Nordea Bank AB (publ), Nordea Bank Finland Plc and Nordea Bank Danmark A/S.

The information provided herein is intended for background information only and for the sole use of the intended recipient. The views and other information provided herein are the

current views of Nordea Markets as of the date of this document and are subject to change without notice. This notice is not an exhaustive description of the described product or the

risks related to it, and it should not be relied on as such, nor is it a substitute for the judgement of the recipient.

The information provided herein is not intended to constitute and does not constitute investment advice nor is the information intended as an offer or solicitation for the purchase or sale

of any financial instrument. The information contained herein has no regard to the specific investment objectives, the financial situation or particular needs of any particular recipient.

Relevant and specific professional advice should always be obtained before making any investment or credit decision. It is important to note that past performance is not indicative of

future results. Nordea Markets is not and does not purport to be an adviser as to legal, taxation, accounting or regulatory matters in any jurisdiction.

This document may not be reproduced, distributed or published for any purpose without the prior written consent from Nordea Markets.

5