Indian Hotels Co.Balance sheetBalance sheet for Indian Hotels Co. LimitedBalance Sheet for1-MarMar-20Mar-19AssetsCurrent AssetsCash39.98148.296Accounts Receivable196.96250.94249.99Inventory52.7259.151.21Capital work in progress51.72137.833.94Loans and advances1036.62847.68850.36Investments4409.674151.54112.7Total current assets1325.811305.921247.56Fixed assetsGross Block422.74.664036.473025.51(-) Acc. Depreciation915.07725.11539.17Net Block3359.593311.362486.34Current liabilities2786.442405.511953.41Provisions198.18208.9188.79Total current liabilities2984.622614.412142.2Net current assets-1658.81-1308.49-894.64Misc Expenses000Total assets6162.1762922.175738.34Liabilities and equityCurrent liabilitiesShare capital118.93118.93118.93Reserves & surplus4089.454464.634364.81Net worth4208.384583.564483.74Secured loan1953.791708.611254.6Unsecured loan000Total current liabilities6162.176292.175738.34Please make sure that total assets equals total liabilities and equity in your balance sheet.If the difference. The two size of the balance sheet is greater than zero, please review the values entered.

Indian Hotels Co,CashflowCash FlowRs (in Crores)ParticularsMar'21Mar'20Mar'19Mar'18Mar'17Profit Before Tax-640.28437.74417.54284.23262.04Net Cash Flow from Operating Activity-53.21610.85546.81481.12458.32Net Cash Used in Investing Activity-383.6-332.96-372.44-1387.63-95.83Net Cash Used in Financing Activity338.66-235.35-206.721012.79-368.92Net Inc/Dec In Cash and Cash Equivalent-98.1542.54-32.35106.28-6.12Cash and Cash Equivalent - Beginning of the Year131.4788.93121.281521.12Cash and Cash Equivalent - End of the Year33.32131.4788.93121.2815

Indian Hotels P&L Acc.Profit & Loss - Indian Hotels Company Ltd.Rs (in Crores)Mar'21Mar'20Mar'19Mar'18Mar'1712Months12Months12Months12Months12MonthsINCOME:Sales Turnover1133.152743.472780.412583.952401.56Excise Duty00000NET SALES1133.152743.472780.412583.952401.56Other Income110.52134.4190.555.3958.02TOTAL INCOME1243.672877.882870.912639.342459.58EXPENDITURE:Manufacturing Expenses405.28768.3790.25745.89723.49Material Consumed00000Personal Expenses538.64725.07703.85649.61633.24Selling Expenses27.6373.1677.2593.0980.95Administrative Expenses258.5415.88479.62466.56444.2Expenses Capitalised00000Provisions Made00000TOTAL EXPENDITURE1230.051982.412050.971955.151881.88Operating Profit-96.9761.06729.44628.8519.68EBITDA13.62895.47819.94684.19577.7Depreciation203.81203.78169.1151.34151.31Other Write-offs00000EBIT-190.19691.69650.84532.85426.39Interest294.79237.55158.64193.43197.86EBT-484.98454.14492.2339.42228.53Taxes-115.536.33153.84136.46118.86Profit and Loss for the Year-369.48417.81338.36202.96109.67Non Recurring Items-128.94-32.44-81.19-60.9938.16Other Non Cash Adjustments00000Other Adjustments-26.3616.046.535.8-4.65REPORTED PAT-524.78401.41263.7147.77143.18KEY ITEMSPreference Dividend00000Equity Dividend59.4647.7441.8327.57-1.66Equity Dividend (%)5040.1435.1723.18-1.68Shares in Issue (Lakhs)11892.5811892.5811892.5811892.5898 ...

Measures of Dispersion and Variability: Range, QD, AD and SD

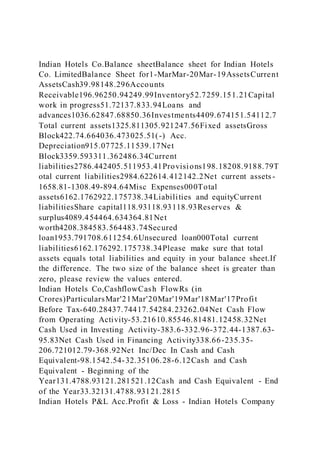

Indian Hotels Co.Balance sheetBalance sheet for Indian Hotels Co.

1. Indian Hotels Co.Balance sheetBalance sheet for Indian Hotels

Co. LimitedBalance Sheet for1-MarMar-20Mar-19AssetsCurrent

AssetsCash39.98148.296Accounts

Receivable196.96250.94249.99Inventory52.7259.151.21Capital

work in progress51.72137.833.94Loans and

advances1036.62847.68850.36Investments4409.674151.54112.7

Total current assets1325.811305.921247.56Fixed assetsGross

Block422.74.664036.473025.51(-) Acc.

Depreciation915.07725.11539.17Net

Block3359.593311.362486.34Current

liabilities2786.442405.511953.41Provisions198.18208.9188.79T

otal current liabilities2984.622614.412142.2Net current assets -

1658.81-1308.49-894.64Misc Expenses000Total

assets6162.1762922.175738.34Liabilities and equityCurrent

liabilitiesShare capital118.93118.93118.93Reserves &

surplus4089.454464.634364.81Net

worth4208.384583.564483.74Secured

loan1953.791708.611254.6Unsecured loan000Total current

liabilities6162.176292.175738.34Please make sure that total

assets equals total liabilities and equity in your balance sheet.If

the difference. The two size of the balance sheet is greater than

zero, please review the values entered.

Indian Hotels Co,CashflowCash FlowRs (in

Crores)ParticularsMar'21Mar'20Mar'19Mar'18Mar'17Profit

Before Tax-640.28437.74417.54284.23262.04Net Cash Flow

from Operating Activity-53.21610.85546.81481.12458.32Net

Cash Used in Investing Activity-383.6-332.96-372.44-1387.63-

95.83Net Cash Used in Financing Activity338.66-235.35-

206.721012.79-368.92Net Inc/Dec In Cash and Cash

Equivalent-98.1542.54-32.35106.28-6.12Cash and Cash

Equivalent - Beginning of the

Year131.4788.93121.281521.12Cash and Cash Equivalent - End

of the Year33.32131.4788.93121.2815

Indian Hotels P&L Acc.Profit & Loss - Indian Hotels Company

3. Income110.52134.4190.555.3953.86Total

Income1243.672877.882870.912639.34244 5.11EXPENSESStock

Adjustments00000Raw Material

Consumed107.93235.74246.76232.64219.99Power and

Fuel00000Employee

Expenses538.64725.07703.85649.61633.22Administration and

Selling Expenses00000Research and Development

Expenses00000Expenses Capitalised00000Other

Expenses583.481021.61100.361072.91017.41Provisions

Made00000TOTAL

EXPENSES1230.051982.412050.971955.151870.62Operating

Profit-

96.9761.06729.44628.8520.63EBITDA13.62895.47819.94684.1

9574.49Depreciation203.81203.78169.1151.34151.29EBIT-

190.19691.69650.84532.85423.2Interest294.79237.55158.64193

.43197.86EBT-484.98454.14492.2339.42225.34Taxes-

115.536.33153.84136.46116.91Profit and Loss for the Year-

369.48417.81338.36202.96108.43Extraordinary Items-155.3-

16.4-74.66-55.1933.51Prior Year Adjustment00000Other

Adjustment00000Reported PAT-

524.78401.41263.7147.77141.94KEY ITEMSReserves Written

Back00000Equity

Capital118.93118.93118.93118.9398.93Reserves and

Surplus4089.454464.634364.814275.032668.27Equity Dividend

Rate4050504035Agg. Non-Promoter Share(Lakhs)00000Agg.

Non-Promoter Holding(%)00000Government Share00000Capital

Adequacy Ratio00000EPS(Rs.)NaNNaNNaNNaNNaNRs (in

Crores)

Sheet6

Sheet7

Sheet8

Foundations of Finance

Tenth Edition

Chapter 4

21. current assets59,664

Current ratio===.74

current liabilities80,203

M

M

cash+accounts receivable12,370

Acid-test ratio===0.15

current liabilities80,203

M

M

accounts receivableaccounts receivable

Days in receivables==

annual credit sales

daily credit sales

365

æö

ç÷

èø

5,6145,614

===10.24 days

500,343×.40

548

360

MM

M

M

annual credit sales

Accounts receivable turnover=

accounts receivable

$500,343*.40

==35.65

$5,614

M

X

M

22. inventory

Days in inventory=

annual cost of goods sold

365

$43,783$43,783

42.80days

$373,396

$1,023

365

M

M

M

===

cost of goods sold

Inventory turnover

inven

=

tory

373,396

Inventory turnover==8.53X

43,783

M

M

operating profits

Operating return on assets=

total assets

20,437

0.1010%

204,522

M

M

===

Operating return on assetsoperating prof

it margin total asset turnover

=´

operating profitssales

23. Operating return on assets=×

salestotal assets

operating profits$20,437

Operating profit margin==0.04=4.1%

sales$500,343

M

M

=

sales$500,343

Total asset turnover==2.45X

total assets$204,522

M

M

=

sales$500,343

Fixed assets turnover==4.36X

net fixed assets$114,818

M

M

=

total debt$125,382

Debt ratio==0.61=61%

total assets$204,522

M

M

=

operating profits20,437

Times interest earned==9.38X

interest expense2,178

M

M

=

net income

Return on equity=

total common equity

net income$9,862

24. Return on equity = ==0.125=12.5%

total common equity$79,140

M

M

market price per share$86.00

Price/earnings ratio==26.22X

earnings per share$3.28

=

market price per share86

Price/book ratio==3.27X

equity book value per share26.3

=

.MsftOfcThm_Text1_Fill {

fill:#000000;

}

.MsftOfcThm_MainDark1_Stroke {

stroke:#000000;

}

XYZ Balance sheethttps://formswift.com/sem/static-non-

state/balance-

sheet?utm_source=google&utm_medium=cpc&utm_campaign=st

atic__balance_sheet__search&u_adgroup=balance_sheet__b&u_

device=c&u_country=us&u_producttype=formswiftdotcom&u_p

roduct=balance_sheet&u_landingpage=2019aa9&headline=Creat

e%20A%20Free%20Balance%20Sheet%20Online&u_sitelinkid=

53908&gclid=CjwKCAiA6seQBhAfEiwAvPqu1_O0V5Bqq1LaS

diEDNly0A1-

TCu5KAGyXcThOUkccE2vSJrdXu46fhoCCJUQAvD_BwEForm

SwiftBalance Sheet forAssetsCurrent AssetsCashAccounts

ReceivableInventoryPrepaid expensesNotes receivableOther

current assetsTotal current assetsFixed assetsLong-term

investmentsLandBuildingMachinery and fixturesOther fixed

25. assetsNet fixed assetsOther assetsGoodwillTotal

assetsLiabilities and equityCurrent liabilitiesAccounts

payableAccrued wagesAccrued payroll taxesAccrued employee

benefitsInterest payableShort-term notesCurrent portion of

long-term debtTotal current liabilitiesLong term

liabilityMortgageOther long-term liabilitiesTotal long-term

liabilitiesOwners equityPaid in capitalNet incomeTotal

equityTotal liabilities and equityPlease make sure that total

assets equals total liabilities and equity in your balance sheet.If

the difference. The two size of the balance sheet is greater than

zero, please review the values

entered.https://formswift.com/sem/static-non-state/balance-

sheet?utm_source=google&utm_medium=cpc&utm_campaign=st

atic__balance_sheet__search&u_adgroup=balance_sheet__b&u_

device=c&u_country=us&u_producttype=formswiftdotcom&u_p

roduct=balance_sheet&u_landingpage=2019aa9&headline=Creat

e%20A%20Free%20Balance%20Sheet%20Online&u_sitelinkid=

53908&gclid=CjwKCAiA6seQBhAfEiwAvPqu1_O0V5Bqq1LaS

diEDNly0A1-

TCu5KAGyXcThOUkccE2vSJrdXu46fhoCCJUQAvD_BwE

XYZ Income

https://formswift.com/builder.php?documentType=income-

statement&ses=02e40e6f0896d5eee72a23f4035164fb&key=2679

98070&utm_source=google&utm_medium=cp c&utm_campaign=

static__income_statement__b&u_adgroup=income_statement&u

_device=c&u_country=us&u_producttype=formfindrdotcom&u_

product=income_statement&u_landingpage=2018aa2&headline=

Create+A+Free+Income+Statement+Online&u_sitelinkid=88292

&gclid=CjwKCAiA6seQBhAfEiwAvPqu12OkzuJGHgFIr0e0p1k

4QSP7P48IxMk7ZbGKkIoxS78FimeAIbqC6xoCyvYQAvD_Bw

E#0FormSwiftIncome statementFor the

periodEndedRevenuesProductsLess returns and

allowancesServicesOtherTotal

revenueCostsProductsServicesOtherTotal costGross

profitOperating expensesGen. and administrativeInsuranceNon-

recurringPayroll taxesRentResearch and developmentSalaries

26. and wagesSales and marketingUtilitiesOtherTotal operating

expensesOperating incomeNot operating, or otherInterest

revenueInterest expensesGain on sale of assetsLoss on sales of

assetsGain from legal actionLoss from legal actionDepreciation

and amortizationOther gameOther lossTotal not operating

otherPretax incomeTaxesIncome tax expenseNet income

Sheet3

Sheet4

Sheet5

Sheet6

Sheet7

Sheet8

Sheet1TABLE 21-1 Financial Ratio AnalysisRatioValue Less

Than 1Value = 1Value More Than 1Current ratio = current

assets/current liabilitiesDebts greater than assets; potentially

major problemsDebts and assets are equalAssets greater than

debts; current ratio of 2 is desirableAcid-test ratio = quick

current assets / current liabilitiesCash flow could be a

problemBusiness is in satisfactory conditionBusiness is in good

financial conditionOperating ratio = (COGS+OPERATING

EXPENSES)/NET SALESDesirableMarginalUndesirableGross

profit margin ratio = (Gross profit from sales)/net sales0.25 to

0.40 is industry averageUncommon except for businesses with

low turnover and high investmentUndesirableAsset turnover

ratio = net sales / average total assets0.40 to 1.0 is industry

averageUncommonUncommonTotal debt to total assets ratio =

total liabilities / total assets0.05 to 0.75 is industry averageDebt

ratio is too highDebt ratio is dangerously high

Operations Management Paper Assignment:

Using the LIRN resource, please search for an article/ a business

case study which discusses / involves lean operations.

In 4-5 written pages (not including cover page and

bibliography) please do the following:

(a) Summarize the key points from the article you found.

27. (b) Highlight 3 key lessons you have learned from reading this

article.

(c) Discuss how this article connects with the material in

Lesson 4. (Lesson 4 material “New approaches in Lean

management” also attached.)

*Lesson 4 topic: Lean operations supply the customer with

exactly what the customer wants when the customer wants it,

without waste, through continuous improvement. In this lesson,

we discuss the usefulness of lean operations and just-in-time

operations, and cover what is means to be a lean organization,

and ways to build lean sustainability.

Note: Please make sure to use APA format. Include at least one

direct quote from the article as well as its accompanying

reference (citation).

General Guidelines:

· The cover page and reference page/s are not included in the

above-stated page requirement. These should be in addition to

page requirements.

· Papers need to be formatted in proper APA 7th Edition

style.

· Each paper requires a minimum of at least three outside

peer-reviewed sources for your references (unless stated

otherwise in the guidance above).

o Acceptable/credible sources include: Academic journals and

books, industry journals, and the class textbook.