Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a Book building process of ipo

Semelhante a Book building process of ipo (20)

Mais de Dharmik

Mais de Dharmik (20)

Último

Último (20)

Book building process of ipo

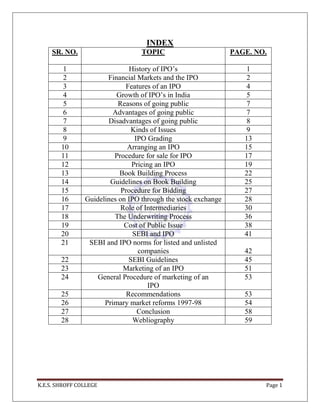

- 1. K.E.S. SHROFF COLLEGE Page 1 INDEX SR. NO. TOPIC PAGE. NO. 1 History of IPO‘s 1 2 Financial Markets and the IPO 2 3 Features of an IPO 4 4 Growth of IPO‘s in India 5 5 Reasons of going public 7 6 Advantages of going public 7 7 Disadvantages of going public 8 8 Kinds of Issues 9 9 IPO Grading 13 10 Arranging an IPO 15 11 Procedure for sale for IPO 17 12 Pricing an IPO 19 13 Book Building Process 22 14 Guidelines on Book Building 25 15 Procedure for Bidding 27 16 Guidelines on IPO through the stock exchange 28 17 Role of Intermediaries 30 18 The Underwriting Process 36 19 Cost of Public Issue 38 20 SEBI and IPO 41 21 SEBI and IPO norms for listed and unlisted companies 42 22 SEBI Guidelines 45 23 Marketing of an IPO 51 24 General Procedure of marketing of an IPO 53 25 Recommendations 53 26 Primary market reforms 1997-98 54 27 Conclusion 58 28 Webliography 59

- 2. K.E.S. SHROFF COLLEGE Page 2 HISTORY The term Initial Public Offering (IPO) slipped into everyday speech during the tech bull market of the late 1990‘s. Back then, it seemed you couldn't go a day without hearing about a dozen new dotcom millionaires in Silicon Valley who were cashing in on their latest IPO. The phenomenon spawned the term silicon ire, which described the dotcom entrepreneurs in their early 20s and 30s who suddenly found themselves living large on the proceeds from their internet companies' IPOs. INVESTORS are still wary of equities in the 1990s, to blame are the excesses in the primary market in the 1990s. Of the thousands of IPOs (Initial Public Offerings) and offers for sale made between 1994 and 1996, less than a hundred were from companies with track record. Even in this shortlist, only a few managed to complete planned projects and deliver value to investors. The rest just frittered the money away. The primary market of the mid-1990s was merely used as a channel to move public funds into private hands. The Securities and Exchange Board of India (SEBI) was late to wake up to the excesses, but when it did, it improved the disclosure framework, tightened the prerequisites for an IPO, and towards the end of the decade, introduced book-building. ( This route brought to market quality, wealth-creating IPOs such as Hughes Software, i-flex solutions, Maruti, Bharti Tele-Ventures, TV Today and Divi's Labs, to name a few. Yet the corporate sector has still not fully lived down the consequences of the excesses of the mid- 1990s.)

- 3. K.E.S. SHROFF COLLEGE Page 3 FINANCIAL MARKETS AND THE IPO The Financial Market is an amorphous set of players who come together to trade in financial assets. Financial Markets in any economic system that acts as a conduit between the organizations who need funds and the investors who wish to invest their money into profitable opportunity. Thus, it helps institutions and organizations that need money to have an access to it and on the other hand, it helps the public in general to earn savings. In modern economic systems Stock Exchanges are the epicenter of the financial activities in any economy as this is the place where actual trading in securities takes place. Modern day Stock Exchanges are most of the centers to trade in the existing financial assets. In this respect, they have come a long way in the sense that these days, they act as a platform to launch new securities as well as act as most authentic and real time indicator of the general economic sentiment. The zone of activities in the capital market is dependent partly on the savings and investments in the economy and partly on the performance of the industry and economy in general. In other words capital market constitutes the channel through which the capital resources generated in the society and made available for economic development of the nation. As such, Financial Markets are functionally classified as having two parts, namely, 1. The Primary Market 2. The Secondary Market Primary Market comprises of the new securities which are offered to the public by new companies. It is the mechanism through which the resources of the community are mobilized and invested in various types of industrial securities. Whenever a new company wants to enter the market it has to first enter the primary market. Secondary Market comprises of further issues which are floated by the existing companies to enhance their liquidity position. Once the new issues are floated and subscribed by the public then these are traded in the secondary market. It provides easy liquidity, transferability and continuous price formation of securities to enable investors to buy and sell them with ease. The volume of activity in the Secondary Market is much higher compared to the Primary Market.

- 4. K.E.S. SHROFF COLLEGE Page 4 IPO FEATURES • An initial public offering (IPO) is the first sale of stock by a company to the public. • An initial public offering (IPO) occurs when a company first sells common shares to investors in the public. Generally, the company offers primary shares this way, although sometimes secondary shares are also sold as IPOs. • Broadly speaking, companies are either private or public. Going public means a Company is switching from private ownership to public ownership. GROWTH OF IPO’s IN INDIA HISTORY OF PRIMARY MARKET Indian capital market was initiated with establishing the Bombay stock exchange in the year 1875. At that time the main function of stock exchange was to provide place for trading in the stocks. Now the exchange has completed more than 125 years. It has undergone several changes. Initially the IPO was called ‗New Issue‘ and the issues in the Primary Market were controlled by CCI (Controller of capital issue). It was working as a department of the MOF (Ministry of Finance). There were very few issues every year. CCI was highly conservative and hardly allowed any premium issues. Also, the regulatory framework was inadequate to control several issues relating to Primary Market. Therefore, in the year 1992 it was abolished. There was no awareness of new issues among the investing public. In fact, during 1950s-1960s, the investment in stock market was considered to be gambling. It was prerogative to highly elite business community to participate in new issues. More than 99% of Indian population never participated in any issue during CCI regime. Around this period, there was tremendous growth in capital market in U.S.A. and Western Europe. In these markets they had established Security Exchange Commission (SEC). It is most powerful autonomous body. The Government of India realized the importance of a similar body in India for healthy and fast growth of Capital Market. Thus Security Exchange Board of India (SEBI) was established with headquarters in Mumbai in 1992. SEBI is the most powerful securities body in India.

- 5. K.E.S. SHROFF COLLEGE Page 5 POPULARISING THE NEW ISSUE Late Shri, Dhirubhai Ambani can be considered as ‗Bhishmapita‘ of new issues, though initially he also had to struggle to get subscribers but he always used innovative ideas for marketing IPOs. It is said that investor never lost money in his pricing methods. There are several incidences of the common man participated in his issues, got allotment, sold shares and created fabulous wealth for themselves. As on 31-12-2003, Reliance Group has more than 3.5 million shareholders. IPO dilutes the ownership stake and diffuses corporate control as it provides ownership to investors in the form of equity shares.

- 6. K.E.S. SHROFF COLLEGE Page 6 REASONS FOR GOING PUBLIC • To raise funds for financing capital expenditure needs like expansion diversification etc. • To finance increased working capital requirement. • As an exit route for existing investors. • For debt financing. ADVANTAGES OF GOING PUBLIC • Stock holder Diversification: As a company grows and becomes more valuable, its founders often have most of its wealth tied up in the company. By selling some of their stock in a public offer, the founders can diversify their holdings and thereby reduce somewhat the risk of their personal portfolios. • Easier to raise new capital: If a privately held company wants to raise capital a sale of a new stock, it must either go to its existing shareholders or shop around for other investors. This can often be a difficult and sometimes impossible process. By going public it becomes easier to find new investors for the business. • Enhances liquidity: The stock of a closely held firm is not liquid. If one of the holders wants to sell some of his shares, it is hard to find potential buyers - especially if the sum involved is large. Even if a buyer is located there is no establishes price at which to complete the transaction. These problems are easily overcome in a publicly owned company. Image: The reputation and visibility of the company increases. It helps to increase company and personal prestige. • Other advantages: Additional incentive for employees in the form of the companies stocks. This also helps to attract potential employees. It commands better valuation of the company better situated for making acquisitions.

- 7. K.E.S. SHROFF COLLEGE Page 7 DISADVANTAGES OF GOING PUBLIC • Cost of Reporting: A publicly owned company must file quarterly reports with the Securities and exchange Board of India. These reports can be costly especially for small firms. • Disclosure: Management may not like the idea or reporting operating data, because such data will then be available to competitors. • Inactive market low price: If a firm is very small and its shares are not traded frequently, then its stock will not really be liquid and the market price may not be truly representative of the stock‘s value. • Control: Owning less than 50% of the shares could lead to a loss of control in the management. • Other disadvantages: The profit earned by the company should be shared with its investors in the form of dividend. An IPO is a costly affair. Around 15-20% of the amount realized is spent on raising the same. A substantial amount of time and effort has to be invested.

- 8. K.E.S. SHROFF COLLEGE Page 8 KINDS OF ISSUES Primarily, issues can be classified as a Public, Rights or preferential issues (also known as private placements). While public and rights issues involve a detailed procedure, private placements or preferential issues are relatively simpler. The classification of issues is illustrated below: (A) Public Issues Public issues can be further classified into Initial Public offerings and Further Public Offerings. In a public offering, the issuer makes an offer for new investors to enter its shareholding family. The issuer company makes detailed disclosures as per the DIP guidelines in its offer document and offers it for subscription. The significant features are illustrated below: • Initial Public Offering (IPO): It is when an unlisted company makes either a fresh issue of securities or an offer for sale of its existing securities or both for the first time to the public. This paves way for listing and trading of the issuer‘s securities. • Further public offering (FPO): It is when an already listed company makes either a fresh issue of securities to the public or an offer for sale to the public, through an offer document. An offer for sale in such scenario is allowed only if it is made to satisfy listing or continuous listing obligations. (B) Rights Issue (RI) It is when a listed company which proposes to issue fresh securities to its existing Shareholders as on a record date. The rights are normally offered in a particular ratio to the number of securities held prior to the issue. This route is best suited for companies who would like to raise capital without diluting stake of its existing shareholders unless they do not intend to subscribe to their entitlements. (C) Private placement It is an issue of shares or of convertible securities by a company to a select group of persons under Section 81 of the Companies Act, 1956 which is neither a rights issue nor a public issue. This is a faster way for a company to raise equity capital. A private placement of shares or of convertible securities by a listed company is generally known by name of preferential allotment. A listed company going for preferential allotment has to comply with the requirements contained in Chapter XIII of SEBI (DIP) Guidelines pertaining to preferential allotment in SEBI (DIP) guidelines include pricing, disclosures in notice etc, in addition to the requirements specified in the Companies Act.

- 9. K.E.S. SHROFF COLLEGE Page 9 (D) Qualified Institutions Placement It is a private placement of equity shares or securities convertible in to equity shares by a listed company to Qualified Institutions Buyers only in terms of provisions of Chapter XIIIA of SEBI (DIP) guidelines. The Chapter contains provisions relating to pricing, disclosures, currency of instruments etc.

- 10. K.E.S. SHROFF COLLEGE Page 10 IPO GRADING IPO grading is the grade assigned by a Credit Rating Agency registered with SEBI, to the initial public offering (IPO) of equity shares or any other security which may be converted into or exchanged with equity shares at a later date. The grade represents a relative assessment of the fundamentals of that issue in relation to the other listed equity securities in India. Such grading is generally assigned on a five-point point scale with a higher score indicating stronger fundamentals and vice versa as below. IPO grade 1: Poor fundamentals IPO grade 2: Below-average fundamentals IPO grade 3: Average fundamentals IPO grade 4: Above-average fundamentals IPO grade 5: Strong fundamentals IPO grading has been introduced as an endeavor to make additional information available for the investors in order to facilitate their assessment of equity issues offered through an IPO. - IPO grading can be done either before filing the draft offer documents with SEBI or thereafter. However, the Prospectus/Red Herring Prospectus, as the case may be, must contain the grade/s given to the IPO by all CRAs approached by the company for grading such IPO. - Further information regarding the grading process may be obtained from the Credit Rating Agencies. - A company which has filed the draft offer document for its IPO with SEBI, on or after 1st May, 2007, is required to obtain a grade for the IPO from at least one CRA. - IPO grade/s cannot be rejected. Irrespective of whether the issuer finds the grade given by the rating agency acceptable or not, the grade has to be disclosed as required under the DIP Guidelines. - However the issuer has the option of opting for another grading by a different agency. In such an event all grades obtained for the IPO will have to be disclosed in the offer documents, advertisements etc. - IPO grading is intended to run parallel to the filing of offer document with SEBI and the consequent issuance of observations. Since issuance of observation by SEBI and the grading process, function independently, IPO grading is not expected to delay the issue process. - The IPO grading process is expected to take into account the prospects of the industry in which the company operates, the competitive strengths of the company that would allow it to address the risks inherent in the business (es) and capitalize on the opportunities available, as well as the company‘s financial position.

- 11. K.E.S. SHROFF COLLEGE Page 11 - While the actual factors considered for grading may not be identical or limited to the following, the areas listed below are generally looked into by the rating agencies, while arriving at an IPO grade : 1. Business Prospects and Competitive Position i. Industry Prospects ii. Company Prospects 2. Financial Position 3. Management Quality 4. Corporate Governance Practices 5. Compliance and Litigation History 6. New Projects—Risks and Prospects It may be noted that the above is only indicative of some of the factors considered in the IPO grading process and may vary on a case to case basis. - IPO grading is done without taking into account the price at which the security is offered in the IPO. Since IPO grading does not consider the issue price, the investor needs to make an independent judgment regarding the price at which to bid for/subscribe to the shares offered through the IPO. - All grades obtained for the IPO along with a description of the grades can be found in the Prospectus. Abridged Prospectus, issue advertisement or any other place where the issuer company is making advertisement for its issue. Further the Grading letter of the Credit Rating Agency which contains the detailed rationale for assigning the particular grade will be included among the Material Documents available for Inspection. - An IPO grade is NOT a suggestion or recommendation as to whether one should subscribe to the IPO or not. IPO grade needs to be read together with the disclosures made in the prospectus including the risk factors as well as the price at which the shares are offered in the issue. - The grades are allocated on a 5-point scale, the lowest being Grade 1 and highest Grade 5. - IPO Grading is intended to provide the investor with an informed and objective opinion expressed by a professional rating agency after analyzing factors like business and financial prospects, management quality and corporate governance practices etc. However, irrespective of the grade obtained by the issuer, the investor needs to make his/her own independent decision regarding investing in any issue after studying the contents of the prospectus including risk factors carefully.

- 12. K.E.S. SHROFF COLLEGE Page 12 - SEBI does not play any role in the assessment made by the grading agency. The grading is intended to be an independent and unbiased opinion of that agency. - The grading is intended to be an independent and unbiased opinion of a rating agency. SEBI does not pass any judgment on the quality of the issuer company. SEBI‘s observations on the IPO document are entirely independent of the IPO grading process or the grades received by the company. IPO

- 13. K.E.S. SHROFF COLLEGE Page 13 ARRANGING AN IPO 1. Select Underwriter - Provides procedural, financial advice - Ultimately buys issue from company (at ―issue price‖) - Ultimately sells it to public (at ―offer price‖) 2. Prepare Registration Statement – for approval of SEC (in accord with Securities Act of 1933). Formal summary that provides information on an issue of securities. 3. Prepare Prospectus – Streamlined version of registration statement, for consideration by potential investors. 4. Set price • Road show – Talks organized to introduce company to potential investors, before the IPO. • Book building – ―Book Building‖ means a process undertaken by which a demand for the securities proposed to be issued by a body corporate is elicited and built up and the price for such securities is assessed for the determination of the quantum of such securities to be issued by means of a notice, circular, advertisement, document or information memoranda or offer document. 5. Selling the shares • Best efforts offering: IPO method in which underwriter promises to sell as much as possible, give best effort, not commit to selling all of issue. • Firm commitment offering: Method in which underwriter buys the whole issue, bears all risk. • Syndicate : Group of underwriters formed to sell a particular issue • Spread: Difference between public ―offer price‖ and price paid by underwriter (―issue price‖). Biggest part of underwriter compensation.

- 14. K.E.S. SHROFF COLLEGE Page 14 PROCEDURE OF SALE OF IPO’S PROCEDURE OF SPALE OF IPO‘S IPOs generally involve one or more investment banks as "underwriters." The company offering its shares, called the "issuer," enters a contract with a lead underwriter to sell its shares to the public. The underwriter then approaches investors with offers to sell these shares. The sale (that is, the allocation and pricing) of shares in an IPO may take several forms. Common methods include: • Dutch auction • Firm commitment • Best efforts • Bought deal • Self Distribution of Stock • A large IPO is usually underwritten by a "syndicate" of investment banks led by one or more major investment banks (lead underwriter). Upon selling the shares, the underwriters keep a commission based on a percentage of the value of the shares sold. Usually, the lead underwriters, i.e. the underwriters selling the largest proportions of the IPO, take the highest commissions—up to 8% in some cases. Multinational IPOs may have as many as three syndicates to deal with differing legal requirements in both the issuer's domestic market and other regions. For example, an issuer based in the E.U. may be represented by the main selling syndicate in its domestic market, Europe, in addition to separate syndicates or selling groups for US/Canada and for Asia. Usually, the lead underwriter in the main selling group is also the lead bank in the other selling groups. Because of the wide array of legal requirements, IPOs typically involve one or more law firms with major practices in securities law, such as the Magic Circle firms of London and the white shoe firms of New York City. Usually, the offering will include the issuance of new shares, intended to raise new capital, as well the secondary sale of existing shares. However, certain regulatory restrictions and restrictions imposed by the lead underwriter are often placed on the sale of existing shares. Public offerings are primarily sold to institutional investors, but some shares are also allocated to the underwriters' retail investors. A broker selling shares of a public offering to his clients is paid through a sales credit instead of a commission. The client pays no commission to purchase the shares of a public offering; the purchase price simply includes the built-in sales credit. The issuer usually allows the underwriters an option to increase the size of the offering by up to 15% under certain circumstance known as the green shoe or overallotment option.

- 15. K.E.S. SHROFF COLLEGE Page 15 PRICING OF IPO Historically, IPOs both globally and in the US have been underpriced. The effect of initial under pricing an IPO is to generate additional interest in the stock when it first becomes publicly traded. This can lead to significant gains for investors who have been allocated shares of the IPO at the offering price. However, under pricing an IPO results in "money left on the table"—lost capital that could have been raised for the company had the stock been offered at a higher price. The danger of overpricing is also an important consideration. If a stock is offered to the public at a higher price than the market will pay, the underwriters may have trouble meeting their commitments to sell shares. Even if they sell all of the issued shares, if the stock falls in value on the first day of trading, it may lose its marketability and hence even more of its value. Investment banks, therefore, take many factors into consideration when pricing an IPO, and attempt to reach an offering price that is low enough to stimulate interest in the stock, but high enough to raise an adequate amount of capital for the company. The process of determining an optimal price usually involves the underwriters ("syndicate") arranging share purchase commitments from lead institutional investors. Issue price A company that is planning an IPO appoints lead managers to help it decide on an appropriate price at which the shares should be issued. There are two ways in which the price of an IPO can be determined: • Either the company, with the help of its lead managers, fixes a price or • The price is arrived at through the process of book building. Note: Not all IPOs are eligible for delivery settlement through the DTC system, which would then either require the physical delivery of the stock certificates to the clearing agent bank's custodian, or a delivery versus payment ("DVP") arrangement with the selling group brokerage firm. This information is not sufficient. Who decides the price of an issue? Indian primary market ushered in an era of free pricing in 1992. Following this, the Guidelines have provided that the issuer in consultation with Merchant Banker shall decide the price. There is no price formula stipulated by SEBI. SEBI does not play any role in price fixation. The company and merchant banker are however required to give full disclosures of the parameters which they had considered while deciding the issue price. There are two types of issues one where company and LM fix a price (called fixed price) and other, where the company and LM stipulate a floor price or a price band and leave it to market forces to determine the final price (price discovery through book building process).

- 16. K.E.S. SHROFF COLLEGE Page 16 a. What are Fixed Price offers? An issuer company is allowed to freely price the issue. The basis of issue price is disclosed in the offer document where the issuer discloses in detail about the qualitative and quantitative factors justifying the issue price. The Issuer company can mention a price band of 20% (cap in the price band should not be more than 20% of the floor price) in the Draft offer documents filed with SEBI and actual price can be determined at a later date before filing of the final offer document with SEBI/ROCs. b. What does “price discovery through book building process” mean? ―Book Building‖ means a process undertaken by which a demand for the securities proposed to be issued by a body corporate is elicited and built up and the price for the securities is assessed on the basis of the bids obtained for the quantum of securities offered for subscription by the issuer. This method provides an opportunity to the market to discover price for securities.

- 17. K.E.S. SHROFF COLLEGE Page 17 BOOK BUILDING IN DETAIL How does Book Building work? Book building is a process of price discovery. Hence, the Red Herring prospectus does not contain a price. Instead, the red herring prospectus contains either the floor price of the securities offered through it or a price band along with the range within which the bids can move. The applicants bid for the shares quoting the price and the quantity that they would like to bid at. Only the retail investors have the option of bidding at ‗cut-off‘. After the bidding process is complete, the ‗cut-off‘ price is arrived at on the lines of Dutch auction. The basis of Allotment (Refer Q. 15.j) is then finalized and letters allotment/refund is undertaken. The final prospectus with all the details including the final issue price and the issue size is filed with ROC, thus completing the issue process. What is a price band? The red herring prospectus may contain either the floor price for the securities or a price band within which the investors can bid. The spread between the floor and the cap of the price band shall not be more than 20%. In other words, it means that the cap should not be more than 120% of the floor price. The price band can have a revision and such a revision in the price band shall be widely disseminated by informing the stock exchanges, by issuing press release and also indicating the change on the relevant website and the terminals of the syndicate members. In case the price band is revised, the bidding period shall be extended for a further period of three days, subject to the total bidding period not exceeding thirteen days. Who decides the price band? It may be understood that the regulatory mechanism does not play a role in setting the price for issues. It is up to the company to decide on the price or the price band, in consultation with Merchant Bankers. The basis of issue price is disclosed in the offer document. The issuer is required to disclose in detail about the qualitative and quantitative factors justifying the issue price. What is firm allotment? A company making an issue to public can reserve some shares on ―allotment on firm basis‖ for some categories as specified in DIP guidelines. Allotment on firm basis indicates that allotment to the investor is on firm basis. DIP guidelines provide for maximum % of shares which can be reserved on firm basis. The shares to be allotted on ―firm allotment category‖ can be issued at a price different from the price at which the net offer to the public is made provided that the price at which the security is being offered to the applicants in firm allotment category is higher than the price at which securities are offered to public.

- 18. K.E.S. SHROFF COLLEGE Page 18 What is reservation on competitive basis? Reservation on Competitive Basis is when allotment of shares is made in proportion to the shares applied for by the concerned reserved categories. Reservation on competitive basis can be made in a public issue to the Employees of the company, Shareholders of the promoting companies in the case of a new company and shareholders of group companies in the case of an existing company, Indian Mutual Funds, Foreign Institutional Investors (including non resident Indians and overseas corporate bodies), Indian and Multilateral development Institutions and Scheduled Banks. Preference while doing the allotment There cannot be any discretion in the allotment process. Prior to the SEBI Circular on DIP Guidelines dated September 19, 2005, the allotment to the Qualified Institutional Buyers (QIBs) was on a discretionary basis. This however has been amended and all allottees are allotted shares on a proportionate basis within their respective categories. Who is eligible for reservation and how much? In a book built issue allocation to Retail Individual Investors (RIIs), Non Institutional Investors (NIIs) and Qualified Institutional Buyers (QIBs) is in the ratio of 35:15: 50 respectively. In case the book built issues are made pursuant to the requirement of mandatory allocation of 60% to QIBs in terms of Rule 19(2)(b) of SCRR, the respective figures are 30% for RIIs and 10% for NIIs. This is a transitory provision pending harmonization of the QIB allocation in terms of the aforesaid Rule with that specified in the guidelines. How is the Retail Investor defined as? ‗Retail individual investor‘ means an investor who applies or bids for securities of or for a value of not more than Rs.1, 00,000.

- 19. K.E.S. SHROFF COLLEGE Page 19 GUIDELINES ON BOOK BUILDING An issuer company proposing to issue capital through book building Shall comply with the following: 75% Book Building Process In an issue of securities to the public through a prospectus the option for 75% book building shall be available to the issuer company subject to the following: The option of book-building shall be available to all body corporate which are eligible to make an issue of capital to the public. The book-building facility shall be available as an alternative the company to the extent of the percentage of the issue which can be reserved for firm allotment. The copy of the draft prospectus filed with the Board may be circulated by the Book Runner to the institutional buyers who are eligible for firm allotment and to the intermediaries eligible to act as underwriters inviting offers for subscribing to the securities. The draft prospectus to be circulated shall indicate the price band within which the securities are being offered for subscription. The Book Runner on receipt of the offers shall maintain a record of the names and number of securities ordered and the price at which the institutional buyer or underwriter is willing to subscribe to securities under the placement portion. The underwriters shall maintain a record of the orders received by him for subscribing to the issue out of the placement portion. Securities as well as the price at which the underwriter shall subscribe to the securities. Provided that the Book Runner shall have an option of requiring the underwriters to the net offer to the public to pay in advance all monies required to be paid in respect of their underwriting commitment. • On determination of the issue price within two day, thereafter the prospectus shall be filed with the Registrar of Company. • The issuer company shall open two different accounts for collection of application moneys, one f or the private placement portion and the other for the public subscription The Book Runner and other intermediaries associated with the book building process shall maintain records of the book building process. The Board shall have the right to inspect such records. Offer to Public through Book Building Process An issuer company may, subject to the requirements make an issue of securities to the public through a prospectus in the following manner a. 100% of the net offer to the public through book building process, ors b. 75% of the net offer to the public through book building process and 25% at the price determined through book building.

- 20. K.E.S. SHROFF COLLEGE Page 20 PROCEDURE FOR BIDDING The method and process of bidding shall be subject to the following: Bid shall be open for at least three working days and not more than seven working days which may be extended to a maximum of ten working days in case the price band is revised. Bidding shall be permitted only if an electronically linked transparent facility is used. Bidding Form: There shall be a standard bidding form to ensure uniformity in bidding and accuracy. The bidding form shall contain information about the investor, the price and the number of securities that the investor wishes to bid. The bidding form before being issued to the bidder shall be serially numbered at the bidding centers and date and time stamped. Allocation / Allotment Procedure: In case an issuer company makes an issue of 100% of the net offer to public through 100% book building process. a) Not less than 35% of the net offer to the public shall be available for allocation to retail individual investors; b) Not less than 15% of the net offer to the public shall be available for allocation to non institutional investors i.e. investors other than retail individual investors and Qualified Institutional Buyers; c) Not more than 50% of the net offer to the public shall be available for allocation to Qualified Institutional Buyers. Provided that 50% of net offer to public shall be mandatorily allotted to the Qualified Institutional Buyers, in case the issuer company is making a public issue. Maintenance of Books and Records: (i) A final book of demand showing the result of the allocation process shall be maintained by the book runner/s. (ii) The Book Runner/s and other intermediaries in the book building process associated shall maintain records of the book building prices. (iii) The Board shall have the right to inspect the records, books and documents relating to the Book building process and such person shall extend full co-operation.

- 21. K.E.S. SHROFF COLLEGE Page 21 GUIDELINES ON INITIAL PUBLIC OFFERS THROUGH THE STOCK EXCHANGE ON-LINE SYSTEM (e-IPO) A company proposing to issue capital to public through the on-line system of the stock exchange for offer of securities shall comply with the requirements as contained in this Chapter in addition to other requirements for public issues as given in these Guidelines, wherever applicable. 1. Agreement with the Stock exchange: The Company shall enter into an agreement with the Stock Exchange(s) which have the requisite system of on-line offer of securities. The agreement mentioned in the above clause shall specify inter-alia, the rights, duties, responsibilities and obligations of the company and stock exchange (s) inter. The agreement may also provide for a dispute resolution mechanism between the company and the stock exchange. 2. Appointment of Brokers: The stock exchange, shall appoint brokers of the exchange, who are registered with SEBI, for the purpose of accepting applications and placing orders with the company. For the purposes of this Chapter, the brokers, so appointed accepting applications and application monies, shall be considered as ‗collection centers‘. The broker/s so appointed, shall collect the money from his/their client for every order placed by him/them and in case the client fails to pay for shares allocated as per the Guidelines, the broker shall pay such amount. 3. Appointment of Registrar to the Issue: The Company shall appoint a Registrar to the Issue having electronic connectivity with the Stock Exchange/s through which the securities are offered under the system. 4. Listing: The Company may apply for listing of its securities on an exchange other than the exchange through which it offers its securities to public through the on-line system. 5. Responsibility of the Lead Manager: The Lead Manger shall be responsible for co- ordination of all the activities amongst various intermediaries connected in the issue / System. The names of brokers appointed for the issue along with the names of the other intermediaries, namely, Lead managers to the issue and Registrars to the Issue shall be disclosed in the prospectus and application form.

- 22. K.E.S. SHROFF COLLEGE Page 22 6. Mode of operation: The company shall, after filing the offer document with ROC and before opening of the issue, make an issue advertisement in one English and one Hindi daily with nationwide circulation, and one regional daily with wide circulation at the place where the registered office of the issuer company is situated. 7. Shelf prospectus: Shelf prospectus shall apply to the issues of securities to be made by public sector banks, scheduled commercial banks and public financial institutions. The provisions of these guidelines relating to public issues shall apply in respect of such issues.

- 23. K.E.S. SHROFF COLLEGE Page 23 ROLE OF INTERMEDIARIES a. Who are the intermediaries in an issue? Merchant Bankers to the issue or Book Running Lead Managers (BRLM), syndicate members, Registrars to the issue, Bankers to the issue, Auditors of the company, Underwriters to the issue, Solicitors, etc. are the intermediaries to an issue. The issuer discloses the addresses, telephone/fax numbers and email addresses of these intermediaries. In addition to this, the issuer also discloses the details of the compliance officer appointed by the company for the purpose of the issue. b. Who is eligible to be a BRLM? A Merchant banker possessing a valid SEBI registration in accordance with the SEBI (Merchant Bankers) Regulations, 1992 is eligible to act as a Book Running Lead Manager to an issue. c. What is the role of a Lead Manager? (Pre and post issue) In the pre-issue process, the Lead Manager (LM) takes up the due diligence of company‘s operations/ management/ business plans/ legal etc. Other activities of the LM include drafting and design of Offer documents, Prospectus, statutory advertisements and memorandum containing salient features of the Prospectus. The BRLMs shall ensure compliance with stipulated requirements and completion of prescribed formalities with the Stock Exchanges, ROC and SEBI including finalization of Prospectus and ROC filing. Appointment of other intermediaries viz., Registrar(s), Printers, Advertising Agency and Bankers to the Offer is also included in the pre-issue processes. The LM also draws up the various marketing strategies for the issue. The post issue activities including management of escrow accounts, coordinate non- institutional allocation, intimation of allocation and dispatch of refunds to bidders etc are performed by the LM. The post Offer activities for the Offer will involve essential follow-up steps, which include the finalization of trading and dealing of instruments and dispatch of certificates and demat of delivery of shares, with the various agencies connected with the work such as the Registrar(s) to the Offer and Bankers to the Offer and the bank handling refund business. The merchant banker shall be responsible for ensuring that these agencies fulfill their functions and enable it to discharge this responsibility through suitable agreements with the Company. A merchant banker is required to do the necessary due diligence in case of QIP mechanism. d. What is the role of a registrar? The Registrar finalizes the list of eligible allottees after deleting the invalid applications and ensures that the corporate action for crediting of shares to the demat accounts of the applicants is done and the dispatch of refund orders to those applicable are sent. The Lead manager coordinates with the Registrar to ensure follow up so that that the flow of applications from collecting bank branches, processing of the applications and other matters till the basis of allotment is finalized, dispatch security certificates and refund orders completed and securities listed.

- 24. K.E.S. SHROFF COLLEGE Page 24 e. What is the role of bankers to the issue? Bankers to the issue, as the name suggests, carries out all the activities of ensuring that the funds are collected and transferred to the Escrow accounts. The Lead Merchant Banker shall ensure that Bankers to the Issue are appointed in all the mandatory collection centers as specified in DIP Guidelines. The LM also ensures follow-up with bankers to the issue to get quick estimates of collection and advising the issuer about closure of the issue, based on the correct figures. f. Question on Due diligence The Lead Managers state that they have examined various documents including those relating to litigation like commercial disputes, patent disputes, disputes with collaborators etc. and other materials in connection with the finalization of the offer document pertaining to the said issue; and on the basis of such examination and the discussions with the Company, its Directors and other officers, other agencies, independent verification of the statements concerning the objects of the issue, projected profitability, price justification, etc., they state that they have sensured that they are in compliance with SEBI, the Government and any other competent authority in this behalf. g. What is the role of merchant banker? Eligibility criteria-SEBI issues an authorization letter to the finance companies, which are eligible to work as merchant bankers. The eligibility criteria depend on network and infrastructure of the company. The company should not be engaged in activities that are banned for merchant bankers by SEBI. SEBI issues authorization letter valid for 3 years and the company has to pay necessary fees. Such merchant banker can be appointed as lead manager for IPO. Functions-Merchant banker can work as lead manager co lead manager investment banker underwriter etc. Responsibility-lead managers are fully responsible for the content and correctness of the prospectus. They must ensure the commencement to the completion of the IPO. Certain guidelines are laid down in section 30 of the SEBI act 1992 on the maximum limits of the intermediaries associated with the issue. Size of the Issue No of Lead Managers 50 cr. 2 50-100 cr. 3 100-200 cr. 4 200-400 cr. 5 Above 400 cr. 1 or more as agreed by the board The number of co managers should not exceed the number of lead managers. There can be only 1 adviser to the issue. There is no limit on the number of underwriters.

- 25. K.E.S. SHROFF COLLEGE Page 25 Informational Asymmetry-in general merchant bankers know the market better than the issuing company. They would exploit the superior knowledge to under price issues. This makes their job easier and helps them earn the goodwill of investors. h. What is the role of broker? All the recognized stock exchange members are called brokers and thus any member of a recognized stock exchange can become a broker to the issue. The brokers can work as broker and underwriter or both. In India usually a broker not only does his normal broking business buying and selling securities for brokerage but also works as an underwriter. They can give underwriting commitment in accordance with their net worth. A broker offer marketing support, underwriting support, disseminates information to investors about the issue and distributes issues stationary at retail investor level. The brokers are governed by rules of SEBI and the respective stock exchange. The brokers are key to the success of the issue. The brokers appoint sub brokers who are in direct contact with the investors.

- 26. K.E.S. SHROFF COLLEGE Page 26 THE UNDERWRITING PROCESS Getting a piece of a hot IPO is very difficult, if not impossible. To understand why, we need to know how an IPO is done, a process known as underwriting. When a company wants to go public, the first thing it does is hire an investment bank. A company could theoretically sell its shares on its own, but realistically, an investment bank is required - it's just the way Wall Street works. Underwriting is the process of raising money by either debt or equity (in this case we are referring to equity). We can think of underwriters as middlemen between companies and the investing public. The biggest underwriters are Goldman Sachs, Merrill Lynch, Credit Suisse First Boston, Lehman Brothers and Morgan Stanley. The company and the investment bank will first meet to negotiate the deal. Items usually discussed include the amount of money a company will raise, the type of securities to be issued and all the details in the underwriting agreement. The deal can be structured in a variety of ways. For example, in a firm commitment, the underwriter guarantees that a certain amount will be raised by buying the entire offer and then reselling to the public. In a best efforts agreement, however, the underwriter sells securities for the company but doesn't guarantee the amount raised. Also, investment banks are hesitant to shoulder all the risk of an offering. Instead, they form a syndicate of underwriters.One underwriter leads the syndicate and the others sell a part of the issue. Once all sides agree to a deal, the investment bank puts together a registration statement to be filed with the SEC. This document contains information about the offering as well as company info such as financial statements, management background, any legal problems, where the money is to be used and insider holdings. The SEC then requires a cooling off period, in which they investigate and make sure all material information has been disclosed. Once the SEC approves the offering, a date (the effective date) is set when the stock will be offered to the public. During the cooling off period the underwriter puts together what is known as the red herring. This is an initial prospectus containing all the information about the company except for the offer price and the effective date, which aren't known at that time. With the red herring in hand, the underwriter and company attempt to hype and build up interest for the issue. They go on a road show - also known as the "dog and pony show" - where the big institutional investors are courted. As the effective date approaches, the underwriter and company sit down and decide on the price. This isn't an easy decision: it depends on the company, the success of the road show and, most importantly, current market conditions. Of course, it's in both parties' interest to get as much as possible. Finally, the securities are sold on the stock market and the money is collected from investors.

- 27. K.E.S. SHROFF COLLEGE Page 27 Is the process followed in India different from abroad? Unlike international markets, India has a large number of retail investors who actively participate in IPO‘s. Internationally, the most active investors are the Mutual Funds and Other Institutional Investors. So the entire issue is book built. But in India, 25 per cent of the issue has to be offered to the general public. Here there are two options to the company. According to the first option, 25 per cent of the issue has to be sold at a fixed price and 75 per cent is through Book Building. The other option is to split the 25 per cent on offer to the public (small investors) into a fixed price portion of 10 per cent and a reservation in the book built portion amounting to 15 per cent of the issue size. The rest of the book built portion is open to any investor.

- 28. K.E.S. SHROFF COLLEGE Page 28 COST OF PUBLIC ISSUE The cost of public issue is normally between 8 and 12 percent depending on the size of the issue and on the level of marketing efforts. The important expenses incurred for a public issue are as follows: • Underwriting expenses: The underwriting commission is fixed at 2.5 % of the nominal value (including premium, if any) of the equity capital being issued to public. • Brokerage: Brokerages applicable to all types of public issues of industrial securities are fixed at 1.5% whether the issue is underwritten or not. The managing brokers (if any) can be paid a maximum remuneration of 0.5% of the nominal value of the capital being issued to public. • Fees to the Managers to the Issues: The aggregate amount payable as fees to the managers to the issue was previously subject to certain limits. Presently, however, there is no restriction on the fee payable to the managers of the issue. • Fees for Regist Rars to the Issue: The compensation to the registrars, typically based on a piece rate system, depends on the number of applications received, number of allotters, and the number of unsuccessful applicants. • Printing Expenses: These relate to the printing of the prospectus, application forms, brouchers, share certificate, allotment/refund letters, envelopes, etc. • Postage Expenses: These pertain to the mailing of application forms, brochures, and prospectus to investors by ordinary post and the mailing of the allotment/refund letters and share certificates by register posts. • Advertising and Publicity Expenses: These are incurred primarily towards statutory announcements, other advertisements, press conferences, and investor‘s conferences. • Listing Fees: This is the concerned fee payable to concerned stock exchange where the securities are listed. It consists of two components: initial listing fees and annual listing fees. • Stamp Duty: This is the duty payable on share certificates issued by the company. As this is the state subject, it tends to vary from state to state.

- 29. K.E.S. SHROFF COLLEGE Page 29 SEBI AND IPO INTRODUCTION ON REGULARITY FRAMEWORK OF IPOS (WITH SPECIAL REFERENCE TO SEBI GUIDELINES ) This chapter presents the regularity framework governing the issuance of IPOs through Public offer , Book building and Online route . The market design for primary market has been provided in the provisions of : (a) The SEBI Act ,1992 , which establishes SEBI to protect investors and develop and regulate securities market ; (b) The Companies Act , 1956 , which sets out the code of conduct for the corporate sector in relation to issue , allotment and transfer of securities , and disclosures to be made in public issue ; (c) The Securities Contracts (Regulation) Act , 1956 , which provides for regulation of transactions in securities through control over stock exchanges ; and (d) The Depositories Act , 1996 , which provides for electronic maintenance and ownership of de-mat securities . SEBI AND IPO ELIGIBILITY NORMS FOR UNLISTED COMPANIES It should have a pre issue network of a minimum amount of Rs1 crore in 3 out of the preceding 5 financial years. In addition the company should compulsorily need the minimum network level during the two immediately preceding years. It should have a track record distributable profits as given in section 205 of companies act 1956 for at least 3 years in the preceding 5 years period. The issue size (i.e. Offer + Form allotment + Promoters contribution through the offer document) should not exceed an amount equal to 5 times its pre issue worth. FOR LISTED COMPANIES It should have a track record distributable profits as given in section 205 of companies act 1956 for at least 3 years in the preceding 5 years period. It should have a pre issue network of a minimum amount of Rs1 crore in 3 out of the preceding 5 financial years with the minimum net worth to be met during the immediately preceding 2 years.

- 30. K.E.S. SHROFF COLLEGE Page 30 SEBI NORMS SEBI has come up with Investor Protection and Disclosure Norms for raising funds through IPO. These rules are amended from time to time to meet with the requirement of changing market conditions. DISCLOSURE NORMS • Risk Factor-The Company/Merchant Banker must specify the major risk factor in the front page of the offer document. • General Risk-Attention of the investor must be drawn on these risk factors. • Issuers Responsibility-It is the absolute responsibility of the issuer company about the true and correct information in the prospectus. Merchant Banker is also responsible for giving true and correct information regarding all the documents such as material contracts, capital structure, appointment of intermediaries and other matters. • Listing Arrangement- It must clearly state that once the issue is subscribed where the shares will be listed for trading. • Disclosure Clause- It is compulsory to mention this clause to distinctly inform the investors that though the prospectus is submitted and approved by SEBI it is not responsible for the financial soundness of the IPO. • Merchant Bankers Responsibility-Disclaimer Clause the Lead Manager has to certify that disclosures made in the prospectus are generally adequate and are in conformity with the SEBI Guidelines. • Capital Structure- the Company must give complete information about the Authorized capital, Subscribed Capital with top ten shareholders holding pattern, Promoters interest and their subscription pattern etc. Also about the reservation in the present issue for Promoters, FII`s, Collaborators, NRI`s etc. Then the net public offer must be stated very clearly. • Auditors Report- The Auditors have to clearly mention about the past performances, Cost of Project, Means of Finance, Receipt of Funds and its usage prior to the IPO. Auditor must also give the tax-benefit note for the company and investors.

- 31. K.E.S. SHROFF COLLEGE Page 31 INVESTOR PROTECTION NORMS. • Pricing of Issue-The pricing of all the allocations for the present issue must follow the bid system. The reservation must be disclosed for different categories of investors and their pricing must be specified clearly. • Minimum Subscription- If the company does not receive minimum subscription of 90% of subscription in each category of offer and if the issue is not underwritten or the underwriters are unable to meet their obligation, then fund so collected must be refunded back to all applicants. Basis of Allotment- In case of full subscription of the issue, the allotment must be made with the full consultation of the concerned stock exchange and the company must be impartial in allotting the shares. • Allotment/Refund- Once the allotment is finalized, the refund of the excess money must be made within the specified time limits otherwise the company must pay interest on delayed refund orders. • Dematerialization of Shares-As per the provisions of the Depositories Act, 1996, And SEBI Rules, now all IPO will be in Demat form only. • Listing of Shares- It is mandatory on the part of the promoters that once the IPO is fully subscribed, and then the underlying shares must be listed on the stock exchange. This provides market and exit routes to the investors.

- 32. K.E.S. SHROFF COLLEGE Page 32 SEBI GUIDELINES IPO of Small Companies Public issue of less than five crores has to be through OTCEI (Over the Counter Exchange of India) and separate guidelines apply for floating and listing of these issues. Public Offer of Small Unlisted Companies (Post-Issue Paid-Up Capital up to Rs.5 crores) Public issues of small ventures which are in operation for not more than two years and whose paid up capital after the issue is greater than 3 crores but less than 5 crores the following guidelines apply. 1. Securities can be listed where listing of securities is screen based. 2. If the paid up capital is less than 3 crores then they can be listed on the Over the Counter Exchange of India (OTCEI) 3. Appointment of market makers mandatory on all the stock exchanges where securities are proposed to be listed. Size of the Public Issue Issue of shares to general public cannot be less than 25%of the total issue. In case of IT, Media and Telecommunication sectors, this stipulation is reduced subject to the conditions that 1. Offer to the public is not less than 10% of the securities issued. 2. A minimum number of 20 lakh securities is offered to the public 3. Size of the net offer to the public is not less than Rs.30 crores. Promoters Contribution 1. Promoters should bring in their contribution including premium fully before the issue 2. Minimum promoter‘s contribution is 20-25% of the public issue. 3. Minimum lock in period for promoter‘s contribution is five years. 4. Minimum lock in period for firm allotment is three years.

- 33. K.E.S. SHROFF COLLEGE Page 33 Collection Centers for Receiving Applications 1. There should be at least 30 mandatory collection centers, which should include invariably the places where stock exchanges have been established. 2. For issues not exceeding Rs.10 crores the collection centers shall be situated at:- • The 4 metropolitan centers viz. Mumbai Delhi Calcutta Chennai • All such centers where stock exchanges are located in the region in which the registered office of the company is situated. Regarding allotments of shares 1. Net Offer the general public has to be at least 25% of the total issue size for listing on a stock exchange 2. It is mandatory for a company to get its shares listed at the regional stock exchange where the registered office of the issuer is located. 3. In an issue of more than 25 crores the issuer is allowed to place the whole issue by book- building. 4. Minimum of 50% of the Net Offer to the public has to be reserved for the investors applying for less than 1000 shares. 5. There should be at least 5 investors for every 1 lakh equity offered. 6. Quoting of PAN or GIR No. in application for the allotment of securities is compulsory where monetary value of investment is Rs.50000/- or above. 7. Indian development financial institutions and Mutual Fund can be allotted securities up to 75% of the issue amount. 8. A venture capital fund shall not be entitled to get its securities listed on any stock exchange till the expiry of 3 years from the date of issuance of securities. 9. Allotment to categories of FIIs and NRIs/OCBs is upto maximum of 24%, which can be further extended to 30% by an application to the RBI-supported by a resolution passed in the General Meeting. Timeframes for Issue and Post-Issue Formalities 1. The minimum period for which the public issue is to be kept open is 3 working days and the maximum for which it can be kept open is 10 working days. The minimum period for right issue is 15 working days and the maximum is 60 working days. 2. A public issue is affected if the issue is able to procure 90% of the total issue size within 60 days from the date of the earliest closure of the public issue.

- 34. K.E.S. SHROFF COLLEGE Page 34 3. In case of oversubscription the company may have he right to retain the excess application money and allot shares more than the proposed issue, which is referred to as ―green-shoe‖ option 4. Allotment has to be made within 30 days of the closure of the Public issue and 42 days in case of Rights issue 5. All the listing formalities of a Public Issue have to be completed within 70 days from the date of closure of the subscription list. Dispatch of Refund Orders. 1. Refund orders have to be dispatched within 30 days of the closure of the issue. 2. Refunds of excess application money i.e. non-allotted shares have to be made within 30 days of the closure of the issue. Other Regulations 1. Underwriting is not mandatory but 90% subscription is mandatory for each issue of capital to public unless it is disinvestment where it is not applicable. 2. If the issue is undersubscribed then the collected amount should be returned back 3. If the issue size is more than Rs500 crores, voluntary disclosures should be made regarding the deployment of funds and an adequate monitoring mechanism put in place to ensure compliance. 4. There should not be any outstanding warrants for financial instruments of any other nature, at the time of the IPO. 5. In the event of the initial public offer being at a premium and if the rights under warrants or other instruments have been exercised within 12 months prior to such offer, the resultant shares will be not taken into account for reckoning the minimum promoters contribution further, the same will also be subject to lock-in. 6. Code of advertisement as specified by SEBI should be adhered to 7. Draft prospectus submitted to SEBI should also be submitted simultaneously to all stock exchanges where it is proposed to be listed. Restrictions on Allotments 1. Firm allotments to mutual funds, FII and employees are not subject to any lock-in period. 2. Within 12 months of the public issue no bonus issue should be made. 3. Maximum percentage of shares, which can be distributes to employees cannot be more than 5% and maximum shares to be allotted to each employee cannot be more than 200.

- 35. K.E.S. SHROFF COLLEGE Page 35 MARKETING OF IPO The role of marketing, and particularly promotion, in the pricing and trading of securities is fairly limited. Preliminary Requirements: The Company has to complete all legal requirements, appoint all intermediaries and once they get SEBI card (approval), the process of marketing of IPO can commence. Timing of IPO: This the most important factor for the success of IPO. If, secondary market is depressed, if there is political unrest, if serious international problems are prevailing then it is considered to be negative factors for timing of IPO‘s. If these factors are favorable then the Company must find out about the timing of other prestigious IPO‘s. Normally in good times many companies are crowding at the same time .This year more than 29 companies are coming with IPO‘s. Around Rs.25, 000-30,000crore of capital is going to be raise this year. Marketing initial public offers (IPO’s) through the secondary market SEBI approved a proposal of marketing IPO‘s through the secondary market. It proposes to use the existing infrastructure of stock exchanges (terminals, brokers and systems), presently being used for secondary market transactions, for marketing IPO‘s with a view to get rid of certain inherent disadvantages faced by issuers and investors like tremendous load on banking and postal system and huge costs in terms of money and time associated with the issue process. This system would confirm to all extant statutory requirements. The investor would approach broker for placing an order for buying shares of primary issues. The registrar in consultation with merchant banker and the regional stock exchange of the issuer will finalize the basis of allotment and intimate the same to the exchanges who in turn shall inform the brokers. The brokers will advise the successful allottees to submit the application form and the amount payable towards the shares. The broker will deposit the amount received in a separate escrow account for the primary market issue. The clearing house of the exchange will debit the primary issue account of the broker and credit the issuer‘s account. Subsequently, the certificates would be delivered to the investors or the depository account of the investor would be credited. The securities can be listed on the stock exchange from the 15th day from the closure of the issue as against 45-60days at present. As investors will have to part with their funds only on successful allotment, their funds are not unnecessarily blocked. This would also ensure that refunds are done away with. The system seeks to reduce the time taken presently for completion of the issue process, as well as the cost of the issue.

- 36. K.E.S. SHROFF COLLEGE Page 36 GENERAL PROCEDURE FOR MARKETING OF IPO (i) PRESS CONFERENCE: Promoters and Lead Managers call for press conference in each major investment center. Reporters are briefed about the issue. They carry it as news-item in their papers. (ii) INVESTORS CONFERENCE: The prospective investors are called by invitation. The Promoters and Lead Managers give presentations. They reply to the questions of the investors to boost their confidence. (iii) ROAD-SHOW: This is like the investors conference but normally is done abroad for marketing ADR/GDR issues. It is an expensive process and requires a lot of legal compliances. The company has to observe the rules of the concerned country. However, road shows are becoming more and more popular in India. (iv) NEWSPAPER ADVERTISEMENT: The Company releases statutory advertisements in leading newspapers. The company has to publish abridges prospectus in leading newspapers. It is the responsibility of the promoters to ensure that the issuing company and their group companies should not release any commercial advertisement, which may influence the investor‘s decision for investment. (v) PRINTING STATIONERY-PROSPECTUS: The company has to print approved prospectus and provide enough copies to all intermediaries. If any investor asks for a copy of prospectus it must be provided to him without any fees. Sufficient quantities should be maintained at the registered office of the company and with the Lead Managers. (vi) PRINTING APPLICATION FORMS: Sufficient number of application forms must be printed much before the opening of the issue. Each form must contain abridged prospectus in SEBI approved format. Sometimes different colored forms are issued to FDI, FII, NRI and general public. It is compulsory to provide stationery to all underwriters and brokers. They will arrange distribution to their sub-brokers and other clients. Sometimes, company makes direct dispatch of forms to prospective investors.

- 37. K.E.S. SHROFF COLLEGE Page 37 RECOMMENDATIONS Since the primary market has continued to remain dormant, SEBI considered on priority basis the recommendations made by the ―Informal Group on Primary Market‖, and accepted most of the recommendations, including the following, which were accepted for immediate implementation:— (i) Primary issues to be compulsorily made through the depository mode after a specified date. (ii) 100 per cent book building in respect of issues of Rs. 25 crore and above. (iii) Reduction in the minimum number of mandatory collection centers in respect of issues above Rs. 10 crore to 4 metropolitan cities plus the place having the regional stock exchange. In order to facilitate flow of funds to the infrastructure sector, the SEBI Board decided to grant specific relaxations to public issues by infrastructure companies. These relaxations would be applicable to infrastructure companies as defined under Section 10 (23G) of the Income Tax Act, 1961 subject to the condition that their projects are appraised by any Development Financial Institution (DFI) or Infrastructure Development Finance Company (IDFC) or Infrastructure Leasing and Financial Services (IL&FS). Further, the projects must also have a participation of at least 5 per cent of the project cost in debt and/or equity by the appraising institution. Subject to these conditions, the infrastructure company can avail of specified relaxations/exemptions from the existing requirements as per SEBI's Disclosure and Investor Protection Guidelines.

- 38. K.E.S. SHROFF COLLEGE Page 38 PRIMARY MARKET REFORMS 1997-98 Entry barrier for unlisted companies modified as dividend payment in immediately preceding 3 years. A listed company required to meet the entry norm only if the post-issue net worth becomes more than five times the pre-issue net worth. Companies required making their partly paid-up shares fully paid up or forfeiting the same, before making a public/rights issue. Unlisted company allowed to freely price its securities provided it has shown net profit in the immediately preceding 3 years subject to its fulfilling the existing disclosure requirements. The Promoters‘ contribution for public issues made uniform at 20% irrespective of the issue size. Written consent from share holders in regard to lock-in made compulsory for securities to be offered for promoter‘s contribution. Appointment of Registrar to an issue for rights issues made mandatory. A provision made regarding disclosure of the share holding of the promoters whose names figure in the paragraph on ―Promoters and their background‖ in the offer document. The SEBI (Registrars to an Issue and Share Transfer Agents) Rules and Regulations 1993 have been amended to provide for an arm‘s length relationship between the Issuer and the Registrar to the Issue. It has now been stipulated that no Registrar to an Issue can act as such for any issue of securities made by anybody corporate, if the Registrar to the issue and the Issuer Company are associates. With a view to facilitating rising of funds by infrastructure projects, SEBI has allowed debt instruments to be listed on the Stock Exchanges without prior listing of equity. Corporates with infrastructure projects and Municipal Corporations to be exempted from the requirements of Rule 19(2b) of Securities (Contract) Regulation Rules to facilitate public offer and listing of its pure debt instruments as well as debt instruments fully or partly convertible into equity without the requirement of prior listing of equity but subject to conditions like investment grade rating. Only body Corporates to be allowed to function as Merchant Bankers.

- 39. K.E.S. SHROFF COLLEGE Page 39 Multiple categories of merchant bankers to be abolished and there shall be only one entity viz., Merchant Banker. Presently, the Merchant Banker allowed to perform underwriting activity but required to seek separate registration to function as a Portfolio Manager under the SEBI (Portfolio Manager) Rules and Regulations, 1993. Merchant Bankers to be prohibited from carrying on fund based activities other than those related exclusively to the capital market; the activities undertaken by NBFCs such as accepting deposits, leasing, bill discounting, etc. not to be allowed to be undertaken by a merchant banker; the existing NBFCs performing merchant banking activities to be given suitable time to restructure their activities.

- 40. K.E.S. SHROFF COLLEGE Page 40 CONCLUSION Nevertheless, there is no denying the enormous interest retail and other investors have shown in the primary market, perhaps even more so than in the secondary one. This interest has been sustained despite the lack of bounce in the secondary market and is not confined to the big issues; even smaller issues have sailed through with large oversubscriptions. If investor are gung-ho about IPO‘s, there are several reasons for it. Unlike earlier IPO booms, this one is being driven by a much better quality of offering. Missing in action so far are the fly-by-night operators of the 1990s who made public offers only to collect the money and vanish. Next, most recent IPO‘s have resulted in gains on listing for the investor. The listing gains have probably initiated a kind of virtuous cycle, tempting investors who have already made money to return to the primary market. Companies have been quick to take advantage of the investor interest in IPO‘s, and banks, broking houses, retail outfits, media houses and government companies are lining up issues. Even mutual funds have got into the act, and are tailoring their offerings to match current market fancies—mid-cap funds, dividend yield funds, and what-have-you. If the government wants to get some money into its kitty through disinvestment programmes, this is the time to make a dash for it.

- 41. K.E.S. SHROFF COLLEGE Page 41 WEBLIOGRAPHY www.nseindia.com www.bseindia.com www.sebi.com