Revised ST3 - Service Tax Return

•

0 gostou•412 visualizações

We can now forget about the unified return for Central Excise & Service Tax, as was announced during the last Budget. The format of revised ST3 says it all, effective date not yet announced. Click here to understand the changes.

Recomendados

Mais conteúdo relacionado

Mais de Suzoy Banerjiee

Mais de Suzoy Banerjiee (20)

Revised ST3 - Service Tax Return

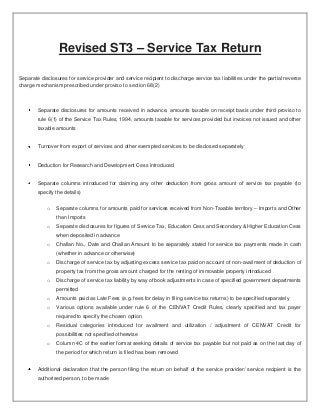

- 1. Revised ST3 – Service Tax Return Separate disclosures for service provider and service recipient to discharge service tax liabilities under the partial reverse charge mechanism prescribed under proviso to section 68(2) Separate disclosures for amounts received in advance, amounts taxable on receipt basis under third proviso to rule 6(1) of the Service Tax Rules, 1994, amounts taxable for services provided but invoices not issued and other taxable amounts Turnover from export of services and other exempted services to be disclosed separately Deduction for Research and Development Cess introduced Separate columns introduced for claiming any other deduction from gross amount of service tax payable (to specify the details) o Separate columns for amounts paid for services received from Non-Taxable territory – Imports and Other than Imports o Separate disclosures for figures of Service Tax, Education Cess and Secondary & Higher Education Cess when deposited in advance o Challan No., Date and Challan Amount to be separately stated for service tax payments made in cash (whether in advance or otherwise) o Discharge of service tax by adjusting excess service tax paid on account of non-availment of deduction of property tax from the gross amount charged for the renting of immovable property introduced o Discharge of service tax liability by way of book adjustments in case of specified government departments permitted o Amounts paid as Late Fees (e.g. fees for delay in filing service tax returns) to be specified separately o Various options available under rule 6 of the CENVAT Credit Rules, clearly specified and tax payer required to specify the chosen option o Residual categories introduced for availment and utilization / adjustment of CENVAT Credit for possibilities not specified otherwise o Column 4C of the earlier format seeking details of service tax payable but not paid as on the last day of the period for which return is filed has been removed Additional declaration that the person filing the return on behalf of the service provider/ service recipient is the authorised person, to be made