Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (13)

Destaque

Destaque (17)

Semelhante a CSH

Semelhante a CSH (20)

CSH

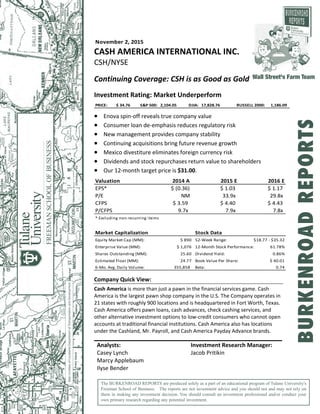

- 1. November 2, 2015 CASH AMERICA INTERNATIONAL INC. CSH/NYSE Continuing Coverage: CSH is as Good as Gold Investment Rating: Market Underperform PRICE: $ 34.76 S&P 500: 2,104.05 DJIA: 17,828.76 RUSSELL 2000: 1,186.09 Enova spin‐off reveals true company value Consumer loan de‐emphasis reduces regulatory risk New management provides company stability Continuing acquisitions bring future revenue growth Mexico divestiture eliminates foreign currency risk Dividends and stock repurchases return value to shareholders Our 12‐month target price is $31.00. Valuation 2014 A 2015 E 2016 E EPS* $ (0.36) $ 1.03 $ 1.17 P/E NM 33.9x 29.8x CFPS $ 3.59 $ 4.40 $ 4.43 P/CFPS 9.7x 7.9x 7.8x * Excluding non‐recurring items Market Capitalization Stock Data Equity Market Cap (MM): $ 890 52‐Week Range: $18.77 ‐ $35.32 Enterprise Value (MM): $ 1,076 12‐Month Stock Performance: 61.78% Shares Outstanding (MM): 25.60 Dividend Yield: 0.86% Estimated Float (MM): 24.77 Book Value Per Share: $ 40.01 6‐Mo. Avg. Daily Volume: 355,858 Beta: 0.74 Company Quick View: Cash America is more than just a pawn in the financial services game. Cash America is the largest pawn shop company in the U.S. The Company operates in 21 states with roughly 900 locations and is headquartered in Fort Worth, Texas. Cash America offers pawn loans, cash advances, check cashing services, and other alternative investment options to low‐credit consumers who cannot open accounts at traditional financial institutions. Cash America also has locations under the Cashland, Mr. Payroll, and Cash America Payday Advance brands. Analysts: Investment Research Manager: Casey Lynch Jacob Pritikin Marcy Applebaum Ilyse Bender The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. Wall Street's Farm Team BURKENROADREPORTS

- 3. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 3 Table 1: Historical Burkenroad Ratings and Prices Report Date Stock Price Rating 12 Month Target Price 11/20/14 $25.00_ Market Outperform $33.00_ 11/07/13 $38.64* Market Outperform $50.00* 10/26/12 $38.91* Market Outperform $52.00* *Price at time of report date and prior to Enova spin‐off INVESTMENT THESIS Enova spin‐off reveals true company value Before November 2014, Cash America had two distinct business segments. The first segment included retail and pawn lending services, which produced steady, low‐risk revenue streams. The second segment included e‐commerce services, which produced rapidly growing, high‐risk revenue streams. The success of each segment depended on different factors. In retail and pawn lending, profitability depended on economic conditions. In e‐commerce and consumer lending, profitability depended heavily on regulatory requirements and analytics. The spin‐off of the Company’s e‐commerce segment, Enova, returned Cash America’s business to a “pure play” pawn lender. With this spin‐off, the Company reduced its regulatory costs and allowed management to focus on its core business of pawn lending. In 2014, total pawn loans written in the U.S. increased by 7.7% compared to a 4.6% increase in 2013, while pawn lending activities accounted for 90.4% of the Company’s total revenues in 2014. Continued pawn loan growth should result in increased Company revenues in the future. Consumer loan de‐emphasis reduces regulatory risk Cash America is reducing its exposure to regulatory risk by decreasing its consumer lending services. Pawn lending has a stable regulatory environment, while regulations in consumer lending are rapidly increasing. In addition to the Enova spin‐off, the Company is de‐ emphasizing its in‐store consumer lending services. Cash America eliminated short‐term consumer lending services in 311 of its stores in 2014. In addition, the Company eliminated 36 locations in Texas providing only consumer loans. In 2014, consumer loan fees accounted for only 8.9% of total revenues compared to 11.0% of total revenues in 2013. The Company’s de‐ emphasis on consumer loans will reduce regulatory compliance costs as well as costs associated with hedging against unknown future regulations. New management provides company stability The Company recently restructured its upper management upon the retirement of the former Chief Executive Officer (CEO), Daniel R. Feehan. T. Brent Stuart took over as Cash America’s new CEO on November 1, 2015. Mr. Stuart has been with Cash America for five years and the Company is not expected to change drastically under his leadership. Daniel R. Feehan, Cash America’s former CEO, will remain active in the Company’s operations with his new position of Chairman of the Board.

- 7. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 7 Customers In the pawn industry, a majority of the customers are individuals, with strong retailers and commercial buyers comprising only 1% of customers. The average customer is 36 years old and has a household average income of $29,000. The industry classifies its customers by generation, with Generation X composing 35% of the market, Baby Boomers composing 30% of the market, and Generation Y composing 22% of the market. In the consumer loan industry, the majority of customers make less than $40,000 annually. Customers in this industry include people without a four‐year college degree, home renters, and people who are separated or divorced. Figure 3 shows the distribution of customer loans based on consumer income level. Figure 3: Consumer Loan Market Segmentation Source: IBIS World Geographic Area The pawn industry and check cashing payday loan services industry are highly concentrated in the Southeast and Southwest regions because the average disposable income level in these regions’ is very low. These two regions compose about 50% of the market. In contrast, New England and the Mid‐Atlantic regions have fewer pawn establishments because these areas have high levels of per capita personal income. Thus, Cash America has the majority of its stores located in the Southeast, Southwest, and Midwest regions. 18.40% 22.50% 16.30% 16.35% 10.20% 8.20% 6.10% 2.00% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% Under $15 $15 ‐ $24.9 $25 ‐ $29.9 $30 ‐ $39.9 $40 ‐ $49.9 $50 ‐ $74.9 $75 ‐ $99.9 Over $100 Percent of Market Household Income (in thousands)

- 10. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 10 Figure 4: Cash America Retail Coverage and Top Ten States Based on Number of Locations Source: Cash America’s Investor Presentation June 30, 2015 Products Cash America offers different products in the two sectors where it operates: financial services and retail. In the financial services sector, the Company’s products include pawn loans, cash advances, auto title loans, gold buying, check cashing, and prepaid debit cards. Pawn lending is the primary form of its financial services. The Company generates revenue in pawn lending through pawn loan fees and service charges as well as through the sale of collateral from forfeited pawn loans. Pawn service charges contribute 56% of Cash America’s net revenue. The Company provides cash to customers by issuing consumer loans through third parties, while check cashing and other financial services are provided only through company‐owned lending locations. Consumer loans contribute to 11% of Cash America’s net revenue. The retail sector includes the customers’ loan collateral, such as jewelry, electronics, tools, and musical instruments that customers forfeit due to the inability to pay off loans, as shown in Figure 5. Cash America determines the prices for collateral items through research and tests, like jewelry authentication and electronic workability, to determine the item’s specific condition and value. About 20% of the time customers forfeit their collateral, which is then sold through retail or commercial sales. The sale of forfeited merchandise contributes to 32% of the Company’s net revenue. Cash America’s target customers are “non‐traditional borrowers.” These borrowers are not willing or able to set up bank accounts to obtain short‐term bank loans. This target customer segment consists of 51 million adults. The customers are served by one of the 826 Cash America locations in the U.S.

- 14. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 14 Table 2: Peer Analysis Company Ticker Symbol Stock Price* Market Cap. (Millions) P/E P/BV EV/ EBITDA EBITDA Margin (%) Debt/E quity (%) Net Revenue (Millions) Cash America International, Inc. CSH (NYSE) $27.97 $738 19.3 0.7 8.4 8.6 17.29 $1,100 EZCORP, Inc. EZPW (NASDAQ) $6.17 $327 (6.2) 0.4 4.3 12.6 35.01 $989 First Cash Financial Services, Inc. FCFS (NASDAQ) $40.06 $1,115 14.9 2.5 9.1 19.8 56.54 $713 eBay, Inc. EBAY (NASDAQ) $24.44 $29,408 12.6 1.5 5.1 29.2 38.49 $17,900 World Acceptance Corp. WRLD (NASDAQ) $26.84 $240 2.2 0.7 3.4 34.9 145.41 $578 Lending Club, Corp. LC (NYSE) $13.23 $4,971 (187.6) 4.98 18.8 58.2 367.54 $213 Source: Thompson One *Price as of Close, September 30, 2015 EZCORP, INC. (EZPW/NASDAQ) EZCORP, Inc. is a specialty consumer financial services company headquartered in Austin, Texas. The company offers retail services for previously‐owned merchandise and short‐term cash solutions including non‐recourse pawn loans, short‐term unsecured loans, and fee‐based credit services. The company operates 1,358 total locations primarily in the U.S., Mexico, and Canada. A total of 497 of these locations are U.S. pawn stores. EZCORP’s revenue growth is steadily declining with 14.3% growth in 2012, 1.61% growth in 2013, and only 0.85% growth in 2014. EZCORP is Cash America’s closest peer based on product and service offerings, but the two companies differ greatly in size. EZCORP’s market capitalization of $327 million is less than half of Cash America’s market capitalization of $738 million. First Cash Financial Services, Inc. (FCFS/NASDAQ) First Cash Financial Services, Inc. operates 912 retail‐based pawn stores and 93 check cashing and financial service stores in the U.S. and Mexico. First Cash Financial Services’ primarily focuses on providing pawn loans with 94.8% of revenues coming from pawn lending activities. First Cash Financial Services is headquartered in Arlington, Texas but does the majority of its business in Mexico. Operations in Mexico contribute to 52.5% of total revenues while operations in the U.S. contribute to 43.9% of total revenues. The company’s revenues have been steadily growing with 11.6% growth in 2013 and 7.9% growth in 2014. However even with this steady growth, Cash America generates almost twice the revenue of First Cash Financial Services.

- 16. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 16 MANAGEMENT PERFORMANCE AND BACKGROUND Cash America’s management team has over 70 years of combined experience leading the Company. The Company’s former President and Chief Executive Officer (CEO), Daniel R. Feehan, begins his retirement on November 1, 2015. Brent Stuart will succeed Mr. Feehan as President and CEO of the Company. Mr. Feehan will remain on the Board of Directors and assume the position of Chairman of the Board. The current Chairman of the Board, Jack Dougherty, will step down at that time but he will continue to serve on the Board of Directors. Mr. Feehan plans to stay active in Cash America’s operations during this transitional period. Return on Invested Capital (ROIC) Return on invested capital (ROIC) is an important measure of management’s ability to turn capital into profits. Table 3 shows Cash America’s ROIC over the past four years compared to the Company’s publicly traded peers. Cash America’s ROIC for years 2011 through 2013 was recently restated due to the Enova Spin‐off. In 2013 and 2014, Cash America’s ROICs of 7.35% and 9.80%, respectively, were higher than its closest competitor EZCORP’s ROICs of (2.48%) and 3.78%. Table 3: ROIC of Cash America and Peers Company 2014 2013 2012 2011 Cash America 7.35% 9.80% 8.39% 11.28% EZCORP (2.48%) 3.78% 16.04% 20.10% First Cash Financial Services 14.73% 18.89% 20.80% 25.31% World Acceptance Corp 15.46% 15.24% 15.76% 16.52% eBay 300.06% 370.02% 1.52% (0.89%) Lending Club 6.99% 11.20% 3.14% (2.58%) Peer Average* 8.41% 11.78% 12.83% 14.13% Source: Thomson One *eBay not included in peer average T. Brent Stuart President and Chief Executive Officer (45) T. Brent Stuart accepted the role of President and Chief Executive Officer (CEO) effective November 1, 2015. He has been with Cash America since 2010 filling the roles of a Regional Vice President, Senior Vice President, and Chief Operating Officer. Before working for Cash America, Mr. Stuart worked with Fremont Investment and Loan, Nationstar Mortgage, Novastar Financial, Inc., CitiFinancial, and Norwest Finance. Mr. Stuart graduated from Southeast Missouri State University with a B.S. in Business Administration.

- 19. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 19 Institutional Investors Table 4 provides the top ten institutional shareholders, which own about 61.01% of the Company’s outstanding shares. Blackrock is Cash America’s biggest investor with 10.85% ownership, while Fiduciary Management is a new investor in the Company with a position of 7.11% ownership. Table 4: Institutional Investors Holder Name Shares Held Ownership (%) Latest Change Investment Style BlackRock Institutional Trust Co. 2,282,659 10.85% (184,006) Index Earnest Partners, LLC 2,087,599 7.85% 92,193 Core Value Dimensional Fund Advisors, LP 1,984,206 7.46% 117,813 Core Growth The Vanguard Group, Inc. 1,943,828 7.31% 17,864 Index Fiduciary Management, Inc. 1,891,734 7.11% 1,891,734 Core Value RidgeWorth Capital Management, LLC 1,476,884 5.55% 1,476,884 Core Growth Brown Advisory, Inc. 1,289,409 4.85% 61,867 GARP Investec Asset Management Ltd. 987,894 3.72% 1,733 Core Growth Denver Investment Advisors, LLC 911,996 3.43% (10,842) Aggressive Growth Brandywine Global Investment Management, LLC 766,501 2.88% (65,936) Deep Value Source: Bloomberg October 4, 2015 Inside Stockholders Cash America’s top five insider stockholders own 2.29% of the Company’s total shares outstanding, while the Company’s executive chairman and former CEO, Daniel, R. Feehan, is the largest insider stockholder with 404,585 shares. Table 5 shows the five individual stockholders with the greatest number of shares. Total insider ownership increased by 8.89% in 2014 compared to 2013 holdings.

- 20. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 20 Table 5: Individual Holders Holder Name Position Shares Held Ownership Feehan, Daniel R. Executive Chairman 404,585 1.52% Stuart, T. Brent CEO 56,170 0.21% Hunter, B. D. Member of Board of Directors 51,881 0.20% Pepe, Victor L. Chief Marketing and Technology Officer 50,441 0.19% Bessant Jr., Thomas A. CFO 45,265 0.17% Source: Bloomberg October 4, 2015 Short Position The short interest ratio provides a significant indicator of market sentiment. After dividing the short interest by the average daily trading volume, investors can make a decision on the number of days they want to short a stock if the price of a stock increases. Bearish sentiment occurs when a short ratio is equal to or greater than five. Cash America has a short ratio of 7.2 days. Therefore, investors are bearish on the Company’s future stock prices. RISK ANALYSIS AND INVESTMENT CAVEATS Cash America’s business strategy exposes the Company to regulatory, operational, and financial risks. Operational risks include reputational risk, the price of gold, unsecured consumer loan credit risk, and acquisition integration. Financial risks include credit risk and liquidity risk. Regulatory Risks The government heavily enforces regulations in the pawn industry. Federal laws require truthful advertising and marketing practices, fair financial practices in lending, loan servicing and debt collection, and protection of sensitive consumer information. At the Federal level, companies have to observe the Patriot Act, Truth‐in‐Lending Act, Bank Secrecy Act and other Internal Revenue Service regulations. If shops handle firearms, they must also follow the Brady Handgun Violence Prevention Act. Inability to abide to regulations causes a store to lose its license. At the state level, pawn establishments must obtain licenses. Failure to adhere to state laws can cause a company to lose its license. States regulate pawn shops’ service charges, interest rates, minimum and maximum terms of a pawn loan, the content and format of the pawn ticket, and the length of time after a loan default that a pawn lending location must hold a pawned item before disposing of it.

- 22. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 22 As shown in Table 6, the debt‐to‐equity ratio, debt to earnings before interest taxes depreciation and amortization ratio, and interest coverage ratio is below the peer average. From 2014 to 2013, the Company’s interest coverage ratio decreased by 2.9% to its current ratio of 2.1% suggesting it may be able to pay interest expenses on its outstanding debt. Table 6: Leverage Ratios Company Debt/Equity Ratio Debt/EBITDA Ratio Interest Coverage Ratio Cash America 17.29% 2.0% 2.1% EZCORP 35.01% 2.5% 2.9% First Cash Financial Services 56.54% 1.8% 7.6% World Acceptance Corp. 145.41% 2.3% 8.7% eBay 38.49% 1.5% 12.8% Lending Club 367.54% 8.5% 0.9% Peer Average 110.05% 3.1% 5.8% Source: Thomson One October 6, 2015 Liquidity Risk Liquidity allows a company to quickly sell its assets and securities to fulfill its short‐term financial demands. The Company uses the current ratio to assess its liquidity by computing the ratio of current assets to current liabilities. Cash America has a current ratio of 6.5, which is a 12% increase from 2013. The Company also uses its quick ratio of 4.8 to assess liquidity. The quick ratio describes the current assets available, excluding inventory, to cover current liabilities. Cash America’s high current and quick ratios show its assets are capable of covering its liabilities. FINANCIAL PERFORMANCE AND PROJECTIONS To project Cash America’s future financial performance, we made assumptions regarding the Company’s operating, investing, and financing activities. Our assumptions used information provided in Cash America’s SEC filings, quarterly conference calls, and other data sources, along with management guidance. Operating Activities To forecast revenues, we used a regression model combined with a terminal growth rate based off of assumptions from the Company’s SEC filings. Our model used six key independent variables and revenues as the dependent variable. Independent variables included seasonality in the second and fourth quarters, gold prices, gas prices, unemployment, and property, plant, and equipment. The Company’s operations are subject to seasonal fluctuations from tax refunds in the first quarter and holiday spending in the fourth quarter. Gold prices greatly impact revenues because 62.9% of collateral held is gold jewelry.

- 27. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 27 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE Edward Altman originally created the Altman Z‐score in 1968 to evaluate the bankruptcy risk for companies over the next two years. Altman calculated the Z‐Score by adding five different financial ratios and assigning weights to adjust for additional financial risk. Within the four different zones, a company is safe when bankruptcy risk is low and the Z‐Score is greater than three. When the Z‐Score is between 2.7 and 2.99, a company should be cautious of bankruptcy, but risk is minor. A Z‐Score between 1.8 and 2.7 implies moderate bankruptcy risk. When the Z‐Score is less than 1.8, the company is headed toward a financial catastrophe Table 7 shows Cash America’s historical Z‐Scores over the last five years. In 2014, Cash America recovered from its financial distress of 2013. Cash America’s most recent Z‐score is in the safe zone due to the Company’s restructuring after the Enova spin‐off. Table 7: Cash America’s Historical Z‐Scores Year 2010 2011 2012 2013 2014 Z‐Scores 3.51 3.61 2.34 1.71 3.23 Source: Cash America 10K filings

- 29. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 29 WWBD? What Would Ben (Graham) Do? Ben Graham is very influential to investors due to his value investing, which focuses on undervalued stocks and eight identifying criteria. The first six criteria decide if a company is underpriced. The last two criteria examine a company’s growth consistency and potential. A company is attractive, according to Graham, if it meets four or more of the criteria. As of November 2, 2015, Graham would label Cash America as relatively attractive because the Company meets four of the eight criteria. Cash America meets the hurdles of having an earnings to price yield two times the yield on a ten‐year treasury note, a stock prices less than 1.5 times the book value per share of the Company, an amount of total debt less than book value, and a current ratio of two or greater. The Company fails the remaining hurdles of a price to earnings ratio (P/E) ratio of half of the stocks highest P/E ratio in the past five previous years, a dividend yield that is half the yield of a ten‐year treasury note, an earnings growth of 7% or higher over the past five years, and a stability in growth of earnings. However, because Cash America only meets half of the criteria, Ben would not have complete confidence in investing in the Company. Cash America does not meet either of Ben Graham’s tests for growth consistency and potential. Figure 9: Ben Graham Dial

- 30. Cash America International (CSH) BURKENROAD REPORTS (www.burkenroad.org) November 2, 2015 30 Earnings per share (ttm) 1.77$ Price: 34.76$ Earnings to Price Yield 5.10% 10 Year Treasury (2X) 4.32% P/E ratio as of 12/30/10 4.5 P/E ratio as of 12/30/11 4.9 P/E ratio as of 12/30/12 5.0 P/E ratio as of 12/30/13 5.8 P/E ratio as of 12/30/14 (10.2) Current P/E Ratio 19.6 Dividends per share (ttm) 0.15$ Price: 34.76$ Dividend Yield 0.43% 1/2 Yield on 10 Year Treasury 1.08% Stock Price 34.76$ Book Value per share as of 9/30/15 38.59$ 150% of book Value per share as of 9/30/15 57.89$ Interest‐bearing debt as of 9/30/15 206,239$ Book value as of 9/30/15 1,024,169$ Current assets as of 9/30/15 687,305$ Current liabilities as of 9/30/15 99,250$ Current ratio as of 9/30/15 6.9 EPS for year ended 12/30/14 (2.22)$ EPS for year ended 12/30/13 2.96$ EPS for year ended 12/30/12 3.42$ EPS for year ended 12/30/11 4.25$ EPS for year ended 12/30/10 3.67$ EPS for year ended 12/30/14 (2.22)$ ‐175% EPS for year ended 12/30/13 2.96$ ‐13% EPS for year ended 12/30/12 3.42$ ‐20% EPS for year ended 12/30/11 4.25$ 16% EPS for year ended 12/30/10 3.67$ Stock price data as of November 2, 2015 No CASH AMERICA INTERNATIONAL INC. (CSH) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury Yes Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs No Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury No Hurdle # 4: A Stock Price less than 1.5 BV Yes Hurdle # 5: Total Debt less than Book Value Yes Hurdle # 6: Current Ratio of Two or More Yes Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years No Hurdle # 8: Stability in Growth of Earnings