A project report on estimation of working capital reqiurements krishna sugar factory athani

•Transferir como DOC, PDF•

14 gostaram•11,376 visualizações

A project report on estimation of working capital reqiurements krishna sugar factory athani

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a A project report on estimation of working capital reqiurements krishna sugar factory athani

Semelhante a A project report on estimation of working capital reqiurements krishna sugar factory athani (20)

Mais de Babasab Patil

Mais de Babasab Patil (20)

Último

Último (20)

A project report on estimation of working capital reqiurements krishna sugar factory athani

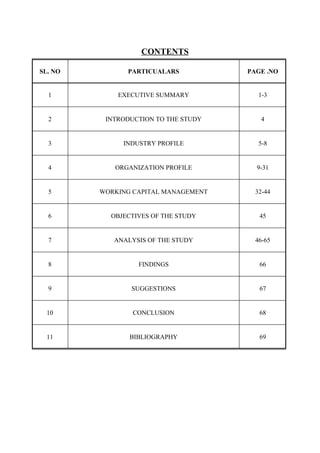

- 1. CONTENTS SL. NO PARTICUALARS PAGE .NO 1 EXECUTIVE SUMMARY 1-3 2 INTRODUCTION TO THE STUDY 4 3 INDUSTRY PROFILE 5-8 4 ORGANIZATION PROFILE 9-31 5 WORKING CAPITAL MANAGEMENT 32-44 6 OBJECTIVES OF THE STUDY 45 7 ANALYSIS OF THE STUDY 46-65 8 FINDINGS 66 9 SUGGESTIONS 67 10 CONCLUSION 68 11 BIBLIOGRAPHY 69

- 2. The Krishna Co-operative Sugar Factory Limited, Athani EXECUTIVE SUMMARY INDUSTRY PROFILE: The advent of modern sugar industry began in 1930 with grant of tariff protection to the Indian sugar industry. The number of sugar mills increased from 30 in the year 1930-31 to 135 in the year 1935 and the production during the same period increased from 1.20 lakh tones to 9.34 lakh tones under dynamic leadership of the private sector. The era of planning for industrial development began in 1950-51 and government laid down targets of sugar production and consumption licensed and installed capacity, sugarcane production during each of the five-year plan periods. Total sugar industries in India are 506 out of which 67 are public sector companies, 157 are private sector companies and 282 are co-operative societies. Total sugar industries in Karnataka are 40 out of which two are public sector companies,18 are private sector companies,19 are co-operative societies and one is joint venture. COMPANY PROFILE: The Krishna Co-Operative Sugar Factory Limited, Athani, is a co-operative society registered under Karnataka co-operative societies Act in 1969. The Plant is located at Sankonattii Village of Athani in Belgaum district. The registration number of the company is DSK/REG/01/80-81 dated 10-03-1981. The industrial license number of the factory is L.I.667 (1988) dated 02/11/1988. The founder of this organization was Late Sri. A.B.Jakanur Ex Min.of Karnataka. At present it has an attractive campus with magnificent buildings over it. There are totally 18,103 shareholders of TKCSFL and it has paid up share capital of Rs.18.39 Crores. During the year 2007-08, it has earned a net profit of Rs.18.34 lakh. During the same year it has produced 7.00 lakh Quintals of sugar and it has crushed 5.60 lakh Tonnes of cane. There are 610 workers in TKCSFL. It is paying salary of Rs. 1500,000 per month to its workers. Total Turnover of sugar is Rs.60.03 crores. Babasabpatilfreepptmba.com Page 2

- 3. The Krishna Co-operative Sugar Factory Limited, Athani NEED FOR THE STUDY: Whether a manufacturing unit or non-manufacturing one, working capital is is the life-line of every concern. Without adequate Working Capital there progress in the industry. Inadequate Working Capital means shortage of raw materials, labour, etc., resulting in partial utilization of available machine capacity. Moreover, research and development in the industry will be at low ebb and essential innovations fail to appear. Inadequate Working Capital frustrates the objectives of the enterprise through lack of funds and contributes towards the failure of a business. On the other hand, more Working Capital may lead to less control over worker’s performance, inefficient store-keeping, excessive stocks of raw material and finished goods, delay in the flow of work-in-progress and lack of coordination in the enterprise. So the amount of Working Capital in every concern should be neither more nor less than what is required. OBJECTIVES OF STUDY: • To study the sources and application of fund of TKCSFL • To examine how the working capital requirements is estimated • A study on the interpretation of working capital on the basis of calculations and estimations • To study the system of inventory management, receivables management and cash management. • To identify weakness and short comings if any as a result of the survey and to offer suggestions METHODOLOGY: DATA COLLECTION METHOD: 1. PRIMARY DATA: The information is collected from the personal interaction With the Accounts officer & workers of the union 2. SECONDARY DATA: This is collected through A) .Annual Reports of the TKCSFL Babasabpatilfreepptmba.com Page 3

- 4. The Krishna Co-operative Sugar Factory Limited, Athani B) Related Information from Internet. FINDINGS: • The current and quick ratios are satisfactory i.e. 2.09 and 0.267 on an average respectively. So the firm’s liquidity position is good. It shows that it is able to meet its current obligations. • The cash reserves maintained by the company are good. But as compared to financial status it is not at remarkable extent. This is serious liquidity crunch to the company. However the company is much safer side because of their outstanding due to farmers, who have also hold shares of company. Another point is farmers are not aggressive to recover their dues. • Proportion of cash to sales maintenance of the cash balance is inadequate. As a rule when sales increase cash also increase, but at a decreasing rate. It shows that inadequate of cash balance. SUGGESTIONS: • The inventory turnover ratio of the company was more than 75%. The firm should search for new customers, and also the firm should focus on it’s foreign exports. • When we analyzed the proportion of cash in sales and current assets, the cash is not sufficient to meet the current expenses. So the firm should maintain sufficient cash balance and bank balance through effective credit policies. The major drawback for the insufficient of cash is that, the inventory has not been selling fast. So the firm should force to think about it. • As it is well known fact that sugarcane grown is not only produces sugar. It can produce many other products also like molasses, cartons, electricity and beverages therefore company need to focus in these areas also. CONCLUSION: When I analyzed the financial performance, the firm’s commitment to meet short obligations is good i.e. liquidity position of the company is good. And in respect cash balance, the firm has not sufficient balance. As a result of that, it may affect the working Babasabpatilfreepptmba.com Page 4

- 5. The Krishna Co-operative Sugar Factory Limited, Athani capital, so totally the firm is struggling to meet its current expenses. And with regard to resources, the firm is not utilizing the assets properly. And similarly the firm has a maintained high inventory. INTRODUCTION TO STUDY The aim of the present study is to examine the Small Scale Industry practices in Working Capital management and to evaluate management performance for the same purpose. “Since the efficiency of the Working Capital management is determined by the efficient administration of its various components- cash, accounts receivable and inventory, the study attempts to determine the management of each component”. “Working Capital in a business enterprise may be compared to the blood in a human body: Blood gives life and strength to the human body. Similarly Working Capital injects life and strength- profits and solvency - to the business organization”. Working Capital refers to short term funds required for the purpose of business operations. The funds used for meeting day to day expenses like, purchase of raw materials, payment of wages and other expenses, stocking of goods, granting of credit to customers and maintenance of the minimum balance. It is not necessary that the funds should be in the form of cash only. It can be in the form of near cash items like, marketable securities, inventories and account receivable Babasabpatilfreepptmba.com Page 5

- 6. The Krishna Co-operative Sugar Factory Limited, Athani INDUSTRY PROFILE INTRODUCTION TO SUGAR INDUSTRY: The Indian sugar industry is a key driver of rural development, supporting India's economic growth. The industry is inherently inclusive supporting over 50 million farmers and their families, along with workers and entrepreneurs of almost 500 mills, apart from a host of wholesalers and distributors spread across the country. The industry is at a cross roads today, where it can leverage opportunities created by global shifts in sugar trade as well as the emergence of sugarcane as a source of renewable energy, through ethanol and cogeneration. While some of these opportunities have been well researched in the past, there was a need to assess the potential for India and to develop a comprehensive and actionable roadmap that could enable the Indian industry to take its rightful place as a food and energy producer for one of the world's leading economies. India is second largest producer of sugarcane next to Brazil. As per last year data, about 4 million hectares of land is under sugarcane with an average yield of 70 tones per hectare. India is largest producer of sugar including traditional sugar sweetener, Khandasari and Gur equivalent to 26 million tones raw value followed by Brazil in the second place at 18.5 million tones. Even in respect of white crystal sugar, India has ranked No position 7 out of last 10 years. Traditional Khandasari and Gur are consumed mostly by the rural population in the early 1930’s nearly 2/3rd of sugarcane production was utilized for production of alternate sweetener, Gur & Khandasari. With better standard of living and high income, the sweetener demand has shifted to white sugar. About 1/3 rd of sugarcane production is utilized by the Gur & Khandasari sectors. Being in the small scale sector, these two sectors are completely free from controls and taxes, which are applicable to the sugar sector. Babasabpatilfreepptmba.com Page 6

- 7. The Krishna Co-operative Sugar Factory Limited, Athani PROFILE OF THE SUGAR INDUSTRY: Sugar mills with cane crushing capacity and sugar production per unit in various countries Country No. of Units Avg. cane crushing Avg. production per per day day Thailand 45 10307 140540 Australia 28 9216 183321 Brazil 213 9168 64018 South Africa 13 6877 137769 Mexico 67 4749 71015 Colombia 10 4590 214900 Cuba 150 4229 45538 Hawaii 9 4111 44111 Mauritius 16 3195 42970 India 506 2527 35000 The advent of modern sugar industry began in 1930 with grant of tariff protection to the Indian sugar industry. The number of sugar mills increased from 30 in the year 1930-31 to 135 in the year 1935 and the production during the same period increased from 1.20 lakh tones to 9.34 lakh tones under dynamic leadership of the private sector. The era of planning for industrial development began in 1950-51 and government laid down targets of sugar production and consumption licensed and installed capacity, sugarcane production during each of the five year plan periods. Total sugar industries in India are 506 out of which 67 are public sector companies, 157 are private sector companies and 282 are co-operative societies. Total sugar industries in Karnataka are 40 out of which two are public sector companies, 18 are private sector companies, 19 are co-operative societies and one is joint venture. Babasabpatilfreepptmba.com Page 7

- 8. The Krishna Co-operative Sugar Factory Limited, Athani Government enacted the Sugar Development Fund Act & Rules, which provides for levy of per quintal of sugar known as Sugar Development Fund (SDF). The SDF is utilized for granting term loans to sugar mills modernization and grants for research projects in the sugar besides creation of buffer stocks as and when required to ensuring price stability. Government de-licensed sugar sector in August 1998. It is now open to entrepreneurs to set up mills without license but at distance of 15 kms away from the existing factory. Sugar units free to expand their capacity and also put up higher capacity new units. This should help to consolidate and expand their capacities wherever cane potential exists. SUGAR INDUSTRY IN INDIA Most of the sugar industries are located in U.P, Bihar, Maharashtra, A.P., Karnataka and T.N. The sugar industry is one of the largest organized industries with total capital investment of more than Rs.500 crores. It employees more than 2.5 lakhs of workers besides creating extensive indirect employment over 25 to 30 million cultivators of sugar cane, dealers in sugar and confectioneries. When sugar industry was granted tariff protection the history of sugar industry started again before 1932, which gave driving force to growth of industry. Again the government in 1951 provided incentives by fixing minimum prices of cane and maximum prices of sugar. This incentive scheme increased the production of sugar but discouraged the cane production. We will see later on how contradictory government. Policies have adversely affected the growth of sugar industry. Unfortunately, government policy has been that of control and re- control from time to time creating an environment inimical (hostility, unfriendly) to the growth of sugar industry. Up to 1957-58 both consumption and production of sugar rose to 20 lakhs tones each. During 1969’s production of sugar rose to 35lakshs tones and during 1970’s it was in between 40 to 50 lakh tones. And during 2000-01 it was in-between 80 to 90 lakhs tones. Babasabpatilfreepptmba.com Page 8

- 9. The Krishna Co-operative Sugar Factory Limited, Athani INDIAN SUGAR INDUSTRY AT GLANCE: No of sugar factories established 574 Total capital employed Rs. 50,000 crores Total annual turnover Rs. 25,000 crores Total payment to cane growers Rs. 18,000 crores Contribution to central & state exchequers Rs. 1700 crores+800 crores Direct employment : rural educated Rs. 5.00 Lakhs Farmers/families involved in sugar cane Rs. 45 million (7.5% of rural population) In global economy, the Indian sugar industry has achieved a number of milestones Largest Sugar Producer in 7 out of 10 years Second Largest Area under Cane/Cane production Amongst the cost effective industries with its field cost (Sugar cane) being the second lowest, despite small land-holding and low productivity Fourth efficient processor of sugar despite low capacity of its sugar plants as compared very large-size plants in other parts of the world GOVERNMENT POLICY: The present policy of decontrol 10% of production by each unit is supplied for public distribution system I as levy sugar at Govt. notified prices admittedly bellow 20% of the actual cost of production. The levy sugar is I to the public irrespective of their economic status. The balance 90% is sold in the free market against monthly/ issued by the Government. This policy has been continuing since 1967-68 except for brief periods of de- control during the years of surplus production and accumulated sugar stocks. Government Babasabpatilfreepptmba.com Page 9

- 10. The Krishna Co-operative Sugar Factory Limited, Athani announces the Statutory Minimum price (SMP) for sugarcane every year based on recommendations of the Commission for Agricultural Cost & Prices (CACP). ORGANISATIONAL PROFILE The Krishna Co-Operative Sugar Factory Limited, Athani (Krishna Sahakari Sakkare Karkhane Niyamit, Athani.) is a co-operative society registered under Karnataka co-operative societies Act in 1969. The industrial license number of the factory is L.I.667 (1988) dated 02/11/1988. The Krishna Co-Operative Sugar Factory Limited, Athani is a co-operative unit. It is situated near Sankonatti village, at a distance of about 6 Km from Athani town. The factory at present has an attractive campus with magnificent buildings over it. Agriculture continues to be an extremely important sector in our country. Cooperative system, as one of its main pillars providing vital support services, is crucial for the transformation of agriculture. It is how inspired the founder Late Sri. A B Jakanur, an agriculturist and a co-operator, to establish this factory during 2000-01 with the financial support from cane growers of this area and the State Government, with an initial crushing capacity 2500 TCD and as a stand-alone sugar industry. This factory had faced a lot of problems all these years in coming out as a viable unit. Though this factory had emerged in this area with a meager beginning, it had not only provided a source of income for forming community but also created a sustainable employment opportunity in this rural area. After a lot of dispute on location of plant, near Sankonatti village, the construction work started in year 1990 and comp elected in the year 2000. The factory was inaugurated by Co- Operative minister of Karnataka State Sri H Vishwanath on 24/03/2002. The regular production was started from 24/03/2002, and the first season lasts from 24/03/2002 to 09/04/2002. The factory started on 24/03/2002 with initial Crushing capacity of 2500 TCD with total expenditure of Rs.46.95 Crore. The area of operation covered 22 villages from Athani Taluka, At present total sugar cane supplied to this sugar industry is from 15,000 acres with average yield per acre of 25 MT. Babasabpatilfreepptmba.com Page 10

- 11. The Krishna Co-operative Sugar Factory Limited, Athani The entire plant and Machinery has been supplied by M/s Triveni Engineering and Industries Limited New Delhi, Rs. 28.17 Crore long-term loan was borrowed from the Co-operative Banks. The factory had created a financial set backs due to the lack of professionalism both in technical and financial managements and not adopted the range of different bi-product activities and had suffered due to a weak governance on efficiency, effectiveness, adaptability and internal and external accountability in the management. However this cooperative and rural based industry must succeed if the poor farmers and the rural unemployed youths have to be prosperous. AREA OF OPERATION: The area of operation of the society shall be confined to the villages of Athani, and Raibag Taluka of Belgaum District and Jamakhandi Taluka of Bagalkot District of Karnataka State. OWNERSHIP PATTERN: A. The authorized share capital of the Society shall be Rs.18.37 crores divided in to total 17971 shares of RS.2, 000/-each as under. i) Rs.3, 00, 29,000/-divided in to 13048 shares of the face value of Rs.2, 000/-each reserved for the grower members called as “A” Class. ii) Rs.5, 98,000/-divided in to 89 shares each reserved for Co-operative Institutions called as “B” Class. iii) Rs.14, 08, 50,000/- from one Government share issued to Government of Karnataka called as “C” Class. iv) Rs.71, 66, 000/- divided in to 4, 309 shares of face value of Rs.2, 000/-each reserved for non-grower members called as “D” Class Babasabpatilfreepptmba.com Page 11

- 12. The Krishna Co-operative Sugar Factory Limited, Athani Babasabpatilfreepptmba.com Page 12

- 13. The Krishna Co-operative Sugar Factory Limited, Athani The Krishna Sahakari Sakkare Karkhane Name of the Company Niyamit Athani Date of Incorporation/Registration No. DSK/REG/01/80-81 Date : 10-03-1981 Nature of Constitution Co-operative Sector Factory code no. 40501 Date of commencement of commercial production of sugar 12/6/2002 Crushing capacity 2500 TCD Project Cost 48.86 crores Production of sugar and its by Products like Activity under taker Molasses ad Bagasse Working period 180-210 days Type unit Large scale Agro based manufacturing unit Main raw material Sugar cane Labour employed 61O Areas of operations 22 villages BOARD OF DIRECTORS: Babasabpatilfreepptmba.com Page 13

- 14. The Krishna Co-operative Sugar Factory Limited, Athani 1) Shri P.C. Savadi : Chairman 2) Shri M.B. Patil : Vice Chairman 3 Shri A.P. Akiwate : Director 4) Shri C.H. Patil : Director 5) Shri B.M. Patil : Director 6) Shri B.M. Kavatakoppa : Director 7) Shri S.A. Mudakannavar : Director 8) Shri G.K. Butali : Director 9) Shri M.K. Kubasad : Director 10) Shri V.G. Telasang : Nominee Director 11) Smt. P.B.Reddy : Nominee Director 12) Shri V.M.Shinge : Nominee Director 13) Shri P.R.Mahajan : Nominee Director 14) Shri I.M. Maniyar : Managing Director STAFF: The employees are responsible for the success or failure of company. There are totally 530 workers in the company. No. of Workers 1) Permanent worker 320 2) Seasonal workers 290 610 Company is paying salary of Rs. 21, 00, 000 per month in season and 15,00,000 per month in off Season to its workers. WORKERS SHIFT SYSTEM: Babasabpatilfreepptmba.com Page 14

- 15. The Krishna Co-operative Sugar Factory Limited, Athani Sugar manufacturing process is continues process it needs employees to take care of the operations 24 hours. So company employs its workers in 3 different shifts and also provide weekly off on routine basis. The shift system of the company is as follows. Shifts Timings Break I 4:00 am to 12:00 pm 30 min II 12:00 pm to 8:00 pm 30 min III 08:00 pm to 4:00 am 30 min GENERAL AND ADMINISTRATION 8:00 am to 12:00 pm 60 min 1:00 pm to 5:00 pm CENTRAL OFFICE 10:00 am to 2:00 pm 30 min 02:30 pm to 5:30 pm JOB SPECIFICATION IN TKCSFL ATHANI Every organization is made not made up only machineries but also consists of people. Hence manpower is very essential and improvement in the production industry .So TKCSFL ATHANI is having manpower sufficiently. Babasabpatilfreepptmba.com Page 15

- 16. The Krishna Co-operative Sugar Factory Limited, Athani Departments Order Daily Wages Enhancement No Change Total Engineering 121 60 57 09 247 Department Production 88 37 31 09 165 Department Cane development 32 0 15 08 55 Department Administration 11 20 16 12 59 Department Civil Department 0 0 0 28 28 Time Office 2 2 0 00 04 Stores 14 29 0 0 43 Department Vehicle 06 03 0 0 09 Department Total 274 151 119 66 610 COMPETITORS: Ugar sugars Hira sugars Renuka sugars Datt sugars (Maharashtra) Panchaganga sugars (Maharashtra) Athani farmer’s sugar factory Dkssk chikkodi INFRASTRUCTURE FACILITIES: Babasabpatilfreepptmba.com Page 16

- 17. The Krishna Co-operative Sugar Factory Limited, Athani Nearer to raw materials Good transportation facilities. Nearer to river place (Krishna River) Good networking. Proper accommodation for its employees ACHIEVEMENTS/AWARDS: STAI, SISSTA & DSTA in their recent 10 th annual convention at Chennai held on 11-08- 2007 have honored this sugar factory with the most prestigious award as the “THE BEST EFFICIENCY & PERFORMANCE SUGAR FACTORY” in the country for the year 2006-07. Hon’ble Union Minister gave the award for agricultural, food & Civil Supplies, in presence of Hon’ble Chief Minister of Tamilnadu. The TKCSFL Athani has also bagged First place for Best Cane Development Award, SISSTA-2007. The companies have the Honor of achieving the Highest Sugar Recovery @ 11.68% in Southern part of India for the year 2008-09. 2.7 VISION & MISSION OF THE ORGANIZATION: “To continue to remain the best performer among sugar manufacturing companies in India & to provide more value to the shareholders by means of efficient capacity utilization of its sugar, power and distillery based facilities.” VISION: The vision statement of The Krishna Co-operative Sugar Factory Limited is “We are dedicated to deliver overall value to our customers by delivering high quality products, exceptional financial performance to our share holders & complete satisfaction to cane growers, employees & stakeholders”. MISSION: Babasabpatilfreepptmba.com Page 17

- 18. The Krishna Co-operative Sugar Factory Limited, Athani At TKCSFL, Athani, they believe in growth through quality, innovation and Research and Development in Agriculture. Their mission is to reduce the overheads and increase the profitability by maximum utility of raw material by way of producing various products. To encourage agro-based co-operative industry To develop co-operative movement in rural sector To encourage the farmers to grow sugarcane for production of sugar and its by-products OBJECTIVES OF TKCSFL, ATHANI To give the good market rate to the farmers who supply the sugar cane to their factory. To keep the good relations with the customers and. farmers and to maximize their satisfaction. Maximum utilization of man power and production capacity and proper utilization of raw material for good recovery. To promote the economic and social betterment among the members through self-help and mutual aid in accordance with the co-operative principles specified in the first schedule of the Act. To encourage self-help, thrift and co-operation amongst member To acquire lands either by way of purchase or otherwise for cultivation of sugar cane and other crops and for erection of buildings, godowns, staff quarters, administrative blocks etc., and for installation of machinery. To manufacture sugar jaggery and their by-products out of sugar-cane grown and supplied by members of the society and other and to sell the same to the best advantage. To undertake such other activities as are identical and conducive to the development of the society. Babasabpatilfreepptmba.com Page 18

- 19. The Krishna Co-operative Sugar Factory Limited, Athani To acquire and install machinery for the utilization of the by-products and buy raw material and sell finished product in the course of utilizing and marketing the by- products. PRODUCT PROFILE: The main and direct product of the sugarcane is sugar. The factory has byproducts like distillery, arrack, co-generation, press mud and ethanol etc. SUGAR: The factory initially started crushing at the rate of 2500 Tonnes crushing per day (TCD). It is needless to emphasis here that this factory has its own credibility and enjoys its own sanctity in the sugar industry. The TKCSFL Athani produces the sugar which can be classified as shown in the table below. The sugar is divided in to three types based on the crystal size; they are large, medium, and small. The production of these is dependent on the crushing capacity of the factory. To produce large sized crystals it takes more time, which in turn affects the crushing. As the size increases the impurity increases and colour of the crystals decreases. TYPE OF SUGAR PRODUCED IN TKCSFL ATHANI: TYPE OF SUGAR SIZE (IN MICRONS) %AGE PRODUCTION IN 2007 LARGE (L30) 1400 NILL MEDIUM (M30) 1120 10-15% SMALL (S30) 600 85-90% DISTILLATION: Babasabpatilfreepptmba.com Page 19

- 20. The Krishna Co-operative Sugar Factory Limited, Athani The unit uses molasses, which is waste in the production of sugar, as raw material for distillation. This molasses has about 40% to 45% of sugar in it. The yeast strain used in fermentation process is Sacchromyces Uvarum. BAGASSES: The fibrous material of sugar cane which after extraction of juice comes out from mill house is called Bagasse and is used as fuel for Boilers. In TKCSFLthey use the Bagasse for high pressure boilers to generate steam. Thus generated steam is used to produce electric power by using Extraction Turbo Generation set. Thus produced power is used to run the factory and excess power is exported through KEB Grid. CO-GENERATION: The factory started producing Power by using Bagasse in the year 2002 with the initial capacity of 6 MW... It installed turbo generator set of capacity 6 MW in the year 2002. As on 2006 the Factory has the total capacity of 6 MW, out of which 4 MW is used for in-house consumption and the remaining power is transported. PRESS MUD: The press mud is obtained in the process of juice purification process. It is used as manure. In K S K N, the press mud is sold to the farmers. PROCUREMENT: The factory obtains the sugarcane, which is required from more than 1000 farmers and by the company farms and others raw materials which are required for the operation is taken from the vendor, here vendors will be evaluated on the basis of price and quality and then the required raw materials will be taken for the efficient vendors. Babasabpatilfreepptmba.com Page 20

- 21. The Krishna Co-operative Sugar Factory Limited, Athani The transport of sugar cane from farmers to the factory will be engaged through Lorries, who will be taken through bidding at the time of harvesting, and also farmers themselves supply by their own bullock carts or by tractors. CANE WEIGHMENT: There are 12 outlaying weigh bridges situated round about Athani for delivering the sugarcane from the farmers. Double check has been provided over the weighment of cane transported from out stations. OPERATIONS: The sugarcane, which is carried by Lorries or other, will be directly fed to the machine where the initial process starts. At the starting point there are knives, which cut sugar cane bunches into individual sugar cane. After this in the next step there are sharp cutter, which cuts the sugarcane bunches into very small pieces. Then it will go to trade marbs (a series of rollers used for crushing purpose) for crushing. Then the juice produced will go for further processing and the Bagasse will be left out there itself. Then they add flocculent [used for mud setting] milk sanitation etc and then after it will go through pans and Masscuite for this Masscuite they will add sodium Hydro Sulphite (to bleach the Masscuite) and it will be separated out and the molasses will be sent to distillery and then white sugar will be bagged. Babasabpatilfreepptmba.com Page 21

- 22. The Krishna Co-operative Sugar Factory Limited, Athani ORGANISATION STRUCTURE: BOARD OF DIRECTORS CHAIRMAN& VICE CHAIRMAN MANAGING DIRECTOR GEN GEN GEN CIVIL STORE MEDICA HEAD CHIEF CHIEF OFFICE LWO WATCH MGR MGR MGR KEEPER L TIME ACCOUNTS SPDT WARD (S) (P) (DS) ENG. OFFICER KEEPER C.D.O OFFICER TOOL ROOM & DIESEL PUMP CHIEF ENG. CHIEF CHEMIST DIST. CHEMIST CO-GEN CANE YARD AGRL DEV GODOWN SECTION GEN ACCOUNT CANE ACCOUNT SALES CASH COMPUTER GAD EST MEETING INWARD & SHARE TYPING GUEST LEGAL PURCHASE SECTION SECTION SECTION OUTWARD SECTION SECTION HOUSE SECTION SECTION Babasabpatilfreepptmba.com SECTION Page 22

- 23. The Krishna Co-operative Sugar Factory Limited, Athani FUNCTIONAL DEPARTMENTS Functional heads 1) Managing Director (M.D) 2) Chief Engineer 3) Chief Chemist 4) Chief Accountant 5) Cane Development Officer (C.D.O) 6) Office Superintendent 7) Accountant (Cane) 8) Labour Welfare Officer (L.W.O) 9) Civil Engineer 10) Accountant (General) 11) Store Keeper 12) Sales Officer 13) Purchase Officer 14) Time Keeper 15) Gudown Keeper 16) Cashier 17) Security Head BRIEF ABOUT FINANCE AND ACCOUNTS DEPARTMENT: Finance plays a vital role in the functioning of all industrial units. Finance is the lifeblood of the organization. In sugar Industry Finance and accounts Department has very vital roles. The financial plan basically deals with raising and proper utilization of funds. The funds can be raised by issue of shares as well as by raising loans through various sources. The finance Babasabpatilfreepptmba.com Page 23

- 24. The Krishna Co-operative Sugar Factory Limited, Athani manager supported with accounts manager and an accounts assistant manages finance department. FUNCTIONS: - They look after the overall financial requirements of the company. They see that a proper inflow and outflow of income and expenditure is maintained. Accounting of sales and sales realization Receipt of cash, cheque and bank drafts etc and issue of official receipts for the same Maintenance of journal, expense ledger and general ledger Costing and accounting is framed and maintained. Yearly budget is framed so that each department can meet their cash requirements. Budget prepared is based on sales forecasting, expenses forecasting, cost forecasting, purchase forecasting etc. Registration and scrutiny of sale orders pertaining to equipment and spare parts FINANCE DEPARTMENT CONSISTS OF FOLLOWING SECTIONS: - • General Accounts Section. • Cane Accounts Section. • Sales Section. • Cash Section. An Accounts Officer is the head of this department. Accountant, sales manager, and head cashier assist him. Babasabpatilfreepptmba.com Page 24

- 25. The Krishna Co-operative Sugar Factory Limited, Athani AS FUNCTIONING OF EACH SECTION IS SUMMARIZED FOLLOWS: GENERAL ACCOUNTS SECTION: General Accounts are looking after the passing of bills and payments. Management is also done by General account section and preparation of financial statements i.e., Balance sheet, profit and loss account is attended by general accounts section. CANE ACCOUNTS SECTION: - The Bills and payment concerned to procurement of sugar cane, is attended by cane accounts section. Payments like cane bills, transport and harvesting bills etc., are prepared and passed in cane accounts section. SALES SECTION: It is looking after sales of sugar and by products molasses, Rectified spirit and other scrap materials. It is keeping records concerned to all sales section. CASH SECTION: It is looking after the payments of all general bills and salary bills apart from cane payment and it is also looking after receipt of cash and cheque payment. All accounts are maintained in usual manner. Various records and books kept are: - General ledger Sub ledger Subsidiary Cash book Bank book Vouchers Babasabpatilfreepptmba.com Page 25

- 26. The Krishna Co-operative Sugar Factory Limited, Athani Each branch prepares trading and profits and loss account and Balance Sheet as on 31 st March every year. And the government Auditor audits the accounts. BANKS (TO PAY BILLS OF THE SUGARCANE SUPPLIERS) SLNO NAME OF THE BANK 1 THE BDCC Bank Ltd, Athani 2 THE BDCC Bank Ltd, Satti 3 THE BDCC Bank Ltd, Halyal 4 THE BDCC Bank Ltd, Konnur 5 THE BDCC Bank Ltd, Kulgod 6 THE BDCC Bank Ltd, Gokak 7 THE BDCC Bank Ltd, Ankali 8 THE BDCC Bank Ltd, Kalloli 9 THE BDCC Bank Ltd, Kabbur 10 THE BDCC Bank Ltd, Gudas 11 THE BDCC Bank Ltd, Harugeri 12 THE BDCC Bank Ltd, Mudalagi 13 THE BDCC Bank Ltd, Ghataprabha 14 THE BDCC Bank Ltd, Shiraguppi 15 THE BDCC Bank Ltd, Yaragatti PURCHASE DEPARTMENT Purchase officer heads Purchase Department. He is responsible for purchasing the spare parts required for the industry. The storekeeper is responsible for stacking; maintaining and issuing required materials to the concerned section. The important functions of this department are: - • Purchasing materials • Calling quotations Babasabpatilfreepptmba.com Page 26

- 27. The Krishna Co-operative Sugar Factory Limited, Athani • Preparing C.S.Q (comparative statement quotation) • Placing before meeting for decision • Placing orders for supply of materials. • Passing bills to Accounts section for payment. Purchase department hierarchy Procedure of purchasing PURCHASE MANAGER GODOWN SUPERVISORS STORE KEEPERS ASSISTANTS 1. Determination of purchase budget In the beginning of the year the purchase manager, with the help of production planning department, prepares a purchase budget. This budget guides him in knowing what and when he has to buy and also quantity. 2. Determination of quantity The stock availability in each location is determined and compared with the actual requirements. After receiving the sales order, raw materials needed are scheduled according to these order level. 3. Purchase order: After satisfy with the quality of materials and reputation of the supplier, purchase order is sent to the supplier. Purchase order includes the date of order, description of materials to be supplied. The copies of this order are sent to the Administrative office, Accounts departments and to the Storekeeper. Babasabpatilfreepptmba.com Page 27

- 28. The Krishna Co-operative Sugar Factory Limited, Athani 4. Receiving and issuing raw materials: - The department heads and the storekeeper check the quality and quantity of raw materials received respectively. The storekeeper enters the details of purchased materials in the store receipt book. Then the general manager passes the amount for payment. PRODUCTION DEPARTMENT Production management refers to the application of management principles to the production function in a factory. In other words production management involves application of planning, organizing, directing and controlling the production process. A well-organized production function can offer competitive advantage to a firm in the following areas. • Higher quality • More inventory turns • Shorter new product lead time • Greater flexibility • Shorter manufacturing lead time • Better customer satisfaction • Reduced wastage Laboratory The factory is having well equipped lab, and the main activity of the lab is to check the content of sugar cane & fixing the correct shape & size of sugar. The lab prepares hourly reports which advice on the addition of the other chemicals in production CHEMICAL SECTION Structure: CHIEF CHEMIST MANUFACTURING CHEMIST DEPUTY CHEMIST Babasabpatilfreepptmba.com Page 28

- 29. The Krishna Co-operative Sugar Factory Limited, Athani LAB IN CHARGE LAB BOY PRODUCTION PROCESS: The main Raw material in the production of sugar is SUGAR CANE The raw materials has to go through following stages before it become finished product. The process in each stage is as under: STAGE:1 SUGAR CANE SUPPLY: The harvested and transported sugar can received is weighed on the weigh Bridge. It is unloaded and kept on the feeder tables. It is fed to the cane carrier as per the requirement. Note: 4500 tons received, 1000 tons stocked and 3500 tons crushing per day. STAGE:-2 MILLING OF CANE/ EXTRACTION OF JUICE: This cane is passed through leveler and fibrizor by making the fine making the fine chips. It is crushed through series of mills. Imbibitions hot water is added prior to the last mill to extract more possible sugar. The Bagasse from the last will is carried through Bagasse conveyor and required quantity of Bagasse is fed to the boilers and excess quality is sent for storage. STAGE:-3 CLARIFICATION AND EVAPORATIONS: The juice from all the mills is pumped to juice weighting scale. It is heated to about 70-77’o c in the juice heaters. It is taken to continuous juice sulphitor in which milk of lime and sulphur di-oxide gas are adjusted to maintain ph 7.0. It is again heated in juice heaters to about 100 to 105’oc and sent to continuous clarifier. Clear juice is taken to multiple effect evaporators to concentrate up to 60oc Brix. Babasabpatilfreepptmba.com Page 29

- 30. The Krishna Co-operative Sugar Factory Limited, Athani The settled mud from the bottom of the clarifier is taken to mud mixer to mix with beguile and taken to continuous vacuum filer. The filtrate is transferred to raw juice receiving tank for treatment. The adhered mud on the screens is scraped and sent out as filter cake, which will be used for composting the manure. STAGE:-4 SUGAR MANUFACTURE AND CRYSTALLIZATION PURING: The concentrated syrup from evaporator is taken to syrup sulpthitor to adjust Ph 4.8 to 5.2. This is stored in the supply tanks and fed to “A” masscult boiling by taking B-seed as a footing. It is concentrated to 92o Brix and dropped to the crystallizer. This masscult is purged in the centrifugal machines. The adhered crystals are scraped to hopper and treated with hot air and cold air blower. It is sent to grader the size for gradation. This graded sugar is stored in SILOS. Weighed and bagged sugar bags are transferred to respective godowns for stacking. STAGE 5:- FURTHER PROCESS: While purging A- massecuite the A-light molasses received is sent to supply tanks and fed to ‘B’- masscult boiling with b-grain as footing. This is purged in the centrifugals. This sugar is used as B- seed and excess is melted and fed to ‘A’- masscult’s. White purging low purity B- Heavy molasses obtained is used for boiling C- massecuite with C- grain as footing. This C- massecuite is taken for purging in Centrifugal machines. The final molasses is separated, weighed and sent to storage tanks. C.F.Magma is sent to melt supply tanks and fed to ‘A’ massecuite boiling. C-light molasses obtained is tired in supply tanks and used for C- massecuite boiling and C- graining also 0. STORES DEPARTMENT This department is headed by storekeeper. To keep the stores and required materials for the factory section wise in a proper way and to maintain their registers and big cards of indents (order goods) Functions: 1) To make the materials requisition for the purpose of knowing the quantity materials. 2) To make purchase order or in simple terms the tenders. Babasabpatilfreepptmba.com Page 30

- 31. The Krishna Co-operative Sugar Factory Limited, Athani 3) To make approval memo for verification of materials. 4) The main function of store department is to prepare a Bin Card. 5) The store Department issues material with reference with store requisitions. 6) To make classification & codification of materials. 7) Receipts of materials. 8) Inspect it with ordered quantity, quality and if any other specifications. 9) Some of the materials like chemicals are to be sent to laboratory for inspection and testing. 10) Getting indents from departmental head and issuing it. 11) To make purchase returns if the materials are rejected. 12) To maintain minimum level of materials. 13) Informing purchase department when materials require. In stores there are two sections 1) Transport Entry table. 2) Store Receipt Table 1) Transport Entry Table They maintain records the receipt of materials at what data, at what time, vehicle number, and quantity in kg. Acknowledgement from vehicles etc 2) Store receipt Table The store keeper maintain the records of receipt of materials, serial no made of transport, purchase order reference, bill no, the name of the supplier etc. the store keeper has given proper conditions to the materials to identify the materials. MARKETING AND SALES DEPARTMENT The American Marketing Association offers the following formal definition: Marketing is an organizational function and a set of processes for creating, communicating, and delivering value to customers and for managing customer relationships in the ways that benefit the organization and its stake holders. It can be viewed Marketing Management as, an art and science of choosing target markets and getting, keeping, and growing customers through creating, delivering, and communicating superior customer value. Babasabpatilfreepptmba.com Page 31

- 32. The Krishna Co-operative Sugar Factory Limited, Athani Channel of distribution Most producers do not sell their goods directly to the final users. Between them stands set of intermediaries performing a variety of function Those intermediaries constitute a marketing channel. Marketing channels are sets of interdependent organizations involved in the process of making a product or service available for use or consumption. Marketing channel decisions are among the most critical decisions facing management. The channel chosen intimately affects all the other marketing decision. The company’s pricing depends on whether it uses mass merchandisers or high quality boutiques. The firm’s sales force and advertising decisions depends upon how much training and motivation dealers need. In addition, the company's channel decisions involve relatively long term commitments to other firms. Role of marketing manager 1) To collect information for sale forecasting. 2) Pricing the products as per the demand. 3) To appoint new dealers and distributors 4) .To have full and perfect knowledge of marketing conditions and policies 5) Marketing department also looks after dispatching goods to the vendors Functions of sales department 1. Sales officer is responsible for selling the products. 2. To look after dispatch of the ordered products. 3. Suggestion, ideas, complaints, feedback from the market to the company. 4. Stocking planning, godown maintenance. Release mechanism of sugar The sale of sugar is controlled by the Chief Director of sugar, New Delhi through release mechanism. Sugar industry is basically a seasonal industry. Hence the sugar will be produced during the season and the sugar thus produced will have to be marketed throughout the year by the sugar mills. Babasabpatilfreepptmba.com Page 32

- 33. The Krishna Co-operative Sugar Factory Limited, Athani The Directorate of sugar will release monthly sugar sale quota for the sugar factories in India and the sugar thus released for the specific month will have to be sold and dispatched before the end of the month. In case any factory not able to sell the entire quantity of the sugar released for the particular month, the remaining quantity will be treated as lapsed. So every factory tries to sell their sugar quote of the month within the validity period. Sales procedure Procedure adopted for sale of sugar and power 1. Sugar Domestic Sale of Sugar The sugar is sold in the domestic market through tender system. Sugar tenders will be called periodically from the various sugar traders. The traders are intimated well in advance about the grade and quality being offered in tender over telephone. The sugar tender is some times conducted at Karnataka Sugar Institute, Belgaum and also at factory site. The officer of KSI will be present at the time of tenders. The rates will be collected over telephone from the various parties along with grade and quantity of sugar required by them. The parties who have offered higher price will be allotted the sugar and they will be instructed to take the sugar delivery within the stipulated period. The sugar will be sold against 100% payment. The rate of domestic price of sugar in the state and the rate of neighboring sugar factories will be compared while selling the sugar in tenders. Export of Sugar When the international price of sugar is remunerative compared to domestic price of sugar, the company exports some of the stock of sugar. The sugar export is mainly undertaken through the mercantile exports or through EXIM Corporation New Delhi. The price for export sugar is negotiated taking into account, the prevailing international sugar price and the price being offered by various sugar factories for export of sugar. Once the rates are finalized, the company will enter into agreement with the party. Then the party will obtain a release orders from chief Director of sugar, New Delhi and necessary excise bond from the concerned authority. After completing all the necessary formalities, sugar will be delivered to the party for export against full payment of the consignment. After the export shipment is completed necessary documents in proof of export of consignment will be collected from the parties. The same will be submitted to the excise department. Babasabpatilfreepptmba.com Page 33

- 34. The Krishna Co-operative Sugar Factory Limited, Athani 2. Export of Power to the KPTCL Grid In addition to the above company is also receiving its revenue from its power plant. Company is having a power plant of 6.0 MW capacities. It is using about 4.0MW for its own/captive consumption; the excess power of about 2.0MW is being exported to the KPTCL. WORKING CAPITAL MANAGEMENT: The aim of the present study is to examine the Small Scale Industry practices in Working Capital management and to evaluate management performance for the same purpose. “Since the efficiency of the Working Capital management is determined by the efficient administration of its various components- cash, accounts receivable and inventory, the study attempts to determine the management of each component”. “Working Capital in a business enterprise may be compared to the blood in a human body: Blood gives life and strength to the human body. Similarly Working Capital injects life and strength- profits and solvency - to the business organization”. Working Capital refers to short term funds required for the purpose of business operations. The funds used for meeting day to day expenses like, purchase of raw materials, payment of wages and other expenses, stocking of goods, granting of credit to customers and maintenance of the minimum balance. It is not necessary that the funds should be in the form of cash only. It can be in the form of near cash items like, marketable securities, inventories and account receivable CONCEPT OF WORKING CAPITAL: Like most other financial concepts, the concept of ‘Working Capital’ is used in different connotations by different writers. Obviously, it is understood either as the total current assets or as the excess of current assets over current liabilities. The former is referred to the gross working Capital and the latter the net Working Capital. So there are two concepts in Working Capital: Gross Working Capital. Net Working Capital Babasabpatilfreepptmba.com Page 34

- 35. The Krishna Co-operative Sugar Factory Limited, Athani Gross Working Capital is the total of all current assets, viz. cash, marketable securities account receivable and inventory Net Working Capita refers to excess of current assets over current liabilities. Both of these concepts have their own importance. “The gross concept is a going concern concept in which management is particularly interested because for the productive utilization of fixed assets all the currents are necessary. The net concept is useful to gauge the financial soundness of a form and is of special interest to sundry creditors and suppliers of short-term loans and advances. It creates confidence among the creditors about the security of their amounts”. No special distinction is made between the terms ‘total current assets’ and ‘Working Capital’ by some authors “ Working Capital is nothing but total of current assets. It is a substitute for Working Capital, though not a perfect one” “Working Capital is the capital circulating into cash over an operating cycle. Working Capital is equated with all the current assets”. “Working Capital and current assets are interchangeable”. The precise meaning of current assets and current liabilities CURRENT ASSETS: Current assets are those assets which are used in the current operation of a business such as inventories, receivables, cash and bank balances and easily convertible securities. These assets generally change their form within an accounting period. “Current assets have a short life span. Cash balance may be held idle for a week or two, accounts receivable may have a life span or 30 to 60 days, and inventories may be held for 30 days 100 days”. CURRENT LIABILITIES: Current liabilities are those claims of outsiders which are expected to mature for payment within an accounting year and include creditors, bill payable, bank-overdraft, outstanding expenses, outstanding tax and income received in advance. “Current liabilities are those liabilities where liquidation is reasonably expected to require the use of existing resources Babasabpatilfreepptmba.com Page 35

- 36. The Krishna Co-operative Sugar Factory Limited, Athani properly classifiable as current assets, or the creation of other current assets, or the creation of other current assets, or the creation of other current liabilities”. FACTORS AFFECTING WORKING CAPITAL NEEDS: The Working Capital requirements of a form depend on many factors. It is a common proposition that the size of Working Capital is a function of sales. Sales alone do not determine the size of Working Capital. But it is constantly affected by the crisis- crossing economic currents flowing in a business. The nature of the firm’s activities, the industrial health of the country, the availability of materials, the ease or tightness of the money market are all parts of these shifting forces. Realizing the complication involved in Working Capital estimates, Gerstenberg observes, “Although no definite rule can be established for determining Working Capital requirements, we can arrive at some general principles. Certain influences, some inherent in the nature of the business and the others arising out of business management policies, affect each of the items of current capital. The following factors affect not only the requirements of Working Capital but also influence to a great extent the composition or structure of Working Capital. It is believed that any attempt at Working Capital management could be improved upon with greater understanding of the underlying factors. THE FOLLOWING FACTORS ARE IMPORTANT: Nature of business Period of manufacture and cost of production, Volume and terms of purchase, Babasabpatilfreepptmba.com Page 36

- 37. The Krishna Co-operative Sugar Factory Limited, Athani Size of business unit, Capacity utilization, Degree of specialization, Seasonal variations, h) Coordination between production and distribution, i) Business cycles, j) Management policy, k) Miscellaneous factors such as government policies, transport and communication system and economic and political environment. FINANCING OF WORKING CAPITAL: In that GFEL, it was financing the working capital from the following five common sources. They are: 1. SHARES: The TKCSFL has issued the equity shares for raising the funds. The Equity Shares do not have any fixed commitment charges and the dividend on these shares is to be paid subject to the availability of sufficient funds. These funds have been injected from the company’s own personal resources, from the members and from the third party investors. 2. TRADE CREDITORS: The trade creditors refer to the credit extended by the suppliers of milk in the normal course of business. The firm has a good relationship with the trade creditors. So that suppliers send the milk to the firm for the payment to be received in future as per the agreement or sales invoice. In this way, the firm generates the short-term finances from the trade creditors. It is an easy and convenient method to finance and it is informal and spontaneous source of finance for the firm. 3. FACTORING OR ACCOUNTS RECIEVABLE CREDIT: Another method of raising short-term finance in The Krishna Co-Operative Sugar Factory Limited, Athani, is through accounts receivables credit offered by the commercial banks. A commercial bank has Babasabpatilfreepptmba.com Page 37

- 38. The Krishna Co-operative Sugar Factory Limited, Athani provided finance by discounting the bills or invoices of its customers. Thus, a firm gets immediate payment for sales made on credit. The factor is also a financial institution, which offers services relating to management and financing of debts arising out of credit sales. Factors render services varying from bill discounting facilities provide commercial banks to the total take over of administration of credit sales including maintenance of sales ledger, collection of accounts receivables, credit control, and protection from bad debts, provision of finance and rendering of advisory services to the firm’s clients. 4. LINE-OF-CREDIT: The business is well capitalized by equity and is has a very good collateral, the business (the firm) might quality fore one. A line-of-credit allows firm to borrow funds for short-term needs when they arise. The funds are rapid once the collections of accounts receivables that result from the short-term sales peak. Lines-of-credit typically are made for one year at a time and expected to be paid it for 30 to 60 consecutive days some times during the year to ensure funds are used for short-term needs only. 5. SHORT-TERM LOAN: The firm has borrowed the funds from the commercial banks to finance for the working capital needs. The short-term loans duration is less than one year. They provide a wide verity of loans to meet the specific requirements of a concern. The different forms in which the banks normally provide loan and advances are Loans Cash credits Overdraft COMPONENTS OF WORKING CAPITAL: The components of working capital are: Cash management Receivables management Inventory management CASH MANAGEMENT: Babasabpatilfreepptmba.com Page 38

- 39. The Krishna Co-operative Sugar Factory Limited, Athani Cash is the liquid form of an asset. It is the ready money available in the firm or with the business, essential for its operations. A firm needs the cash for the following three purposes: Transaction motive: The firm must and should keep the funds for transactions like purchase, sales etc. These activities, which are not known in advance, are not considered while preparing a cash budget. Precautionary motive: The firm also keeps funds for the safeguard against uncertainties, which are an integral part of business operations. Speculative Motive: To tap profits from opportunities arising from fluctuations in commodity prices, security prices, interest rates etc. The company with surplus cash is in a better position to exploit such situations. Cash Flows: The flow of cash into and out of the business over a period refers to cash flow. Cash inflow can be in the form of cash received from customers, lenders and investors. Cash outflow can arise because of payments made to employees (salaries), suppliers and creditors. Positives Cash flow: When cash inflow exceeds outflow it results in positive cash flows. Positive cash flow is beneficial to the business, the only thing to be cautious about is the opportunity cost, incurred as a result of idle money. Negative Cash flows: Negative cash flows arise when cash outflow exceeds inflows. This can be due to various reasons. A good cash management has a major impact on the overall working capital management. It is required to meet the business obligations in the firm. The benefits of good cash Management are: Control of financial risk Opportunity for profit Increased customer, supplier, and shareholder confidence The cash management is commonly deals with the following aspects. Babasabpatilfreepptmba.com Page 39

- 40. The Krishna Co-operative Sugar Factory Limited, Athani Cash planning or identifying sources of cash flows Managing the cash flows Optimum cash level Identifying various avenues to invest surplus cash TYPES OF WORKING CAPITAL: While planning for the Working Capital one has to keep in mind different classification of Working Capital. They are: Permanent of fixed Working Capital: Permanent Working Capital is the minimum amount of current assets, which is needed to conduct a business even during the dullest season of the year. This amount varies from year to year, depending upon the growth of a company and the stage of the business cycle in which it operates. It is the amount of funds required to produce the goods and services, which are necessary to satisfy demand at a particular point. It represents the current assets, which are required on a continuing basis over the entire year. It is maintained as the medium to carry on operations at any time. Temporary or variable Working Capital: Temporary or variable or fluctuating Working Capital is the amount of Working Capital which is required to meet seasonal in nature, it means the blocking of Working Capital in stock and it will take time to convert it into cash. In order to meet special exigencies like, launching of extensive marketing campaign, for conducting research etc., special Working Capital is required. OPERATING CYCLE: The operating cycle can be said to be at the heart of the need for Working Capital. “The continuing flow from cash as advances to suppliers, to inventory, to accounts receivable and back into cash is what is called the operating cycle”. In other words, the terms cash cycle refers to the length of time necessary to complete the following cycle of events. Fuel, power and office expenses to meet selling costs, such as packing, advertising etc Babasabpatilfreepptmba.com Page 40

- 41. The Krishna Co-operative Sugar Factory Limited, Athani The aim of such an approach is not only directed towards management of Working Capital fund inflows and outflows, but also directed to refine the balancing judgment between liquidity and profitability. ADEQUACY OF WORKING CAPITAL: A business enterprise should have enough Working Capital. Without adequate Working Capital it cannot be run effectively a manufacturing concern is sure to collapse if it is run for longer period without or with meager amount of Working Capital. Therefore, the enterprise has to maintain adequate Working Capital can avail following advantages: It enables the enterprise to enjoy uninterrupted flow of production by obtaining the raw material well in time. It enables an enterprise to avail cash discounts on the purchase and hence, it reduces costs, It enables to make regular payments of salaries, wages and other day to day commitments which raise the morale of its employees, increases their efficiency, reduce-wastage and costs, It enables to extend favorable credit terms to customers, It will help to maintain the good will and credit worthiness which is essential for raising the loans from banks and others on easy and favorable terms, It helps to exploit favorable market conditions such as, purchasing its requirements in bulk when the prices are lower and by holding its inventories for higher prices, This gains the confidence of its investors and creates a favorable market to raise additional funds in the future and It creates an environment of security, confidence, high morale and overall efficiency in a business, etc. Babasabpatilfreepptmba.com Page 41

- 42. The Krishna Co-operative Sugar Factory Limited, Athani INADEQUACY OF WORKING CAPITAL: At the same time inadequacy of Working Capital will affect business prospects adversely. Goodwill of the firm will be at stake if the Working Capital gap is not bridged. Shortage of Working Capital or inadequacy of Working Capital will affect profitability. Liquidity and soundness of a business enterprise, it can cause following damages: It stagnates growth. It becomes difficult for the enterprise to undertake profitable projects for non-availability of the Working Capital funds, It becomes difficult to implement operating plans and achieve an enterprise’s profit target, An enterprise may not be able to take advantage of cash discount facilities, An enterprise will not be able to pay its dividends because of the non availability of funds, An enterprise may have to borrow funds at exorbitant rates of interest, Operating inefficiencies creep in when it becomes difficult even to meet day-to-day commitments, An enterprise loses its reputation when it is not in a position to honor its short term obligations. As a result, an enterprise faces tight credit terms. SHORT-TERM BANK CREDIT - A SOURCE OF FINANCE: There are four categories of sources of Working Capital namely; Trade credit Bank credit Current provisions and non-bank short term borrowing, and Long term source comprising equity capital and long-term borrowings Babasabpatilfreepptmba.com Page 42

- 43. The Krishna Co-operative Sugar Factory Limited, Athani Trade credit and short-term credit are the primary sources for financing Working Capital, in our country. According to an estimate, both these sources together finance about three fourth of the Working Capital requirements of an industry”. FORMS OF CREDIT: After getting the overall credit limit sanctioned by the banker, the borrower draws funds periodically. The following forms of credit are available to him. Loan arrangement: Under this arrangement, the amount of the loan is credited by the bank to the borrower’s account and the interest is payable on the balances outstanding. Overdraft arrangement: The borrower is allowed to overdraw in his current account with the bank up to a stipulated limit and the interest is payable on the actual loan utilized. Cash credit arrangement: The borrower can draw to a stipulated limit based on the security margin. Usually, such credit is allowed against Pledge or hypothecation of goods but the borrower can provide alternative securities also in conformity with the terms of advance. Bills purchased and bills discounted: This arrangement is of relatively recent origin in India. With the introduction of the New Bill Market Scheme in 1970 by the Reserve Bank of India, a bank credit is made available through discounting of bills by banks. This scheme intends to link credit with the sale and purchase of goods. To popularize this scheme, the discount rates are fixed lower than those of cash credit. Term loans: Bank advance loans for 3 to 7 years payable in yearly or half yearly installments. PRINCIPLES OF WORKING CAPITAL MANAGEMENT E. L. Walker’s Capital Propositions and James C. Van Home’s elucidation of the same. These propositions are also known as the principles dealing with risk factors and serve as the basis of Working Capital theory. Principle-1 Babasabpatilfreepptmba.com Page 43

- 44. The Krishna Co-operative Sugar Factory Limited, Athani The first principle is concerned with the relationship between the levels of Working Capital and sales. Briefly, it may be stated as follows: if Working Capital is varied relative to sales, the amount of risk that a form assumes is also varied and the chances of gain or loss are increased This principle implies that a definite relation wrists between the degree of risk and the rate of return. That is the more the risk that a firm assumes, the greater is the possibility of gain or loss. The opportunity for gain is enhanced by choosing an appropriate asset and liability structure. The firm’s return on investment will be comparatively large when there are a low proportion of current assets to total assets and a high proportion of current liabilities to total liabilities. This strategy, no doubt, will result in a low level of Working Capital and relatively great profitability but the firm assumes a risk of technical insolvency, i.e., the inability to meet its cash obligations. Therefore, the risk involved with various levels of current assets and current liabilities must be evaluated in relation to the profitability associated with those levels. Principle -2 As already stated above, the main purpose of management is determining the ideal level of Working Capital. This principle serves as a basis for determination and is applicable to investments made not only in various components of Working Capital but also in fixed assets. Stated precisely, it is as follows: capital should be invested in each component of Working Capital as long as the equity position of the firm improves. Principle - 3 The third principle is concerned with the risk resulting from the type of capital used to finance Working Capital directly affects the amount of risk that a firm assumes as well as the possibility of gain or loss, and cost of capital Babasabpatilfreepptmba.com Page 44

- 45. The Krishna Co-operative Sugar Factory Limited, Athani Principle - 4 As stated above, the extent of the of debt depends upon the level of risk a management wishes to undertake. It should be noted that the risk is not only associated with the amount of debt used relative to equity but also related to the nature of the contacts negotiated by the borrower. The dates of maturity and restrictive clauses of the contracts are the most important characteristics of debt contracts that directly affect the firm’s operations. The greater the disparity between the maturities of a firm’s short -term debt instruments and its flow of internally generated funds, the greater the risk and vice versa. Incidentally, management is not compensated for assuming the risk referred to in this concept; therefore, under no circumstances should the risk be assumed. On the whole, a management has to determine the liquidity of the firm on the basis of information about risk and opportunity. Costs of holding liquidity. The degree of liquidity, desirable is a function of profitability of insolvency of various levels of liquidity, the opportunity cost of maintaining those levels and the cost of bankruptcy. Therefore, the behavior of the management should be influenced not only by the risk and the opportunity costs associated with the various levels of liquidity, but also by the cost of bankruptcy. Thus the management must behave in a manner consistent with the maximization of shareholder’s wealth. FACTORS INFLUENCING WORKING CAPITAL REQUIREMENTS Nature of business – This is one of the primary factors influencing the working capital requirements of a firm. The Krishna Co-Operative Sugar Factory Limited, Athani, is a manufacturing firm, has a longer operating cycle for manufacturing the products, and investing more funds in its current assets. Therefore, it requires much more working capital. Babasabpatilfreepptmba.com Page 45

- 46. The Krishna Co-operative Sugar Factory Limited, Athani Market conditions – The level of competition existing in the market also influences working capital requirement. When competition is high, the company should have enough inventories of finished goods to meet a certain level of demand. Otherwise, customers are highly likely to switch over to competitor’s products. It thus has greater working capital needs. When competition is low, but demand for the product is high, the firm can afford to have a smaller inventory and would consequently require lesser working capital. But this factor has not applied in these technological and competitive days. ESTIMATION OF WORKING CAPITAL REQIUREMENTS Managing the working capital is a matter of balance. The firms must have sufficient funds on hand to meet its immediate needs. The Krishna Co-Operative Sugar Factory Limited, Athani, is manufacturing oriented organization; the following aspects have to be taken into consideration while estimating the working capital requirements. They are: • Total costs incurred on material, wages and overheads. • The length of time for which raw material are to remain in stores before They are issued for production. • The length of the production cycle or work-in-process, i.e., the time taken for conversion of raw material into finished goods. • The length of sales cycle during which finished goods to be kept waiting for sales. • The average period of credit allowed to customers. • The amount of cash required paying day-today expenses of the business. • The average amount of cash required to make advance payments • The average credit period expected to be allowed by suppliers. • Time lag in the payment of wages and other expenses. Babasabpatilfreepptmba.com Page 46

- 47. The Krishna Co-operative Sugar Factory Limited, Athani OBJECTIVES OF STUDY To study the sources and application of fund of TKCSFL To examine how the working capital requirements is estimated A study on the interpretation of working capital on the basis of calculations and estimations To study the system of inventory management, receivables management and cash Ma nagement. To identify weakness and short comings if any as a result of the survey and to offer suggestions Babasabpatilfreepptmba.com Page 47

- 48. The Krishna Co-operative Sugar Factory Limited, Athani ANALYSIS AND INTERPRETATION OF DATA: TABLE 1: CALCULATION OF WORKING CAPITAL Particulars 2005-06 2006-07 2007 – 08 Current Assets Inventories 193771415 624968314 717284971.5 Sundry debtors 11081938.99 25182025.76 5727392 Cash 72521 325153.45 28456.45 Bank 27143285.9 26566127.5 14554932.44 Other assets 939201052 12356005.85 16419308.96 Loans & advances 37226454.5 4315300.17 4315300.17 Receivables from govt. 1859709 1859709 1859709 1210356376.39 693712926.73 76019007 Current Liabilities Sundry creditors 1893901.5 18503328 11822912 Babasabpatilfreepptmba.com Page 48

- 49. The Krishna Co-operative Sugar Factory Limited, Athani Term loans DCC bank 51010105.66 61987719 68212128 Others Statutory payable 2640680 5336185 8322361 Excise duty 551827 551827 551827 Net Working Capital 1154259862.23 607333867.73 48500689 The Net Working Capital has been increased in 2006 – 2007, when compared to other years. This is due to huge rise in inventories …………. TABLE 2: STATEMENT SHOWING INCREASE & DECREASE IN WORKING CAPITAL: Babasabpatilfreepptmba.com Page 49

- 50. The Krishna Co-operative Sugar Factory Limited, Athani Particulars Particulars Increase in Current Assets Decrease in Current Assets Inventories 431196899 92316657.5 Inventories - Sundry debtors 14100086.77 - Sundry debtors - 19424634 Cash 252632.45 - Cash - 296697 Bank - - Bank 577158.4 12011195.06 Other assets - 4063303.11 Other assets 926845046.15 - Loans & advances - Loans & advances 32911154.33 - Receivables from govt. - - Receivables from govt. - - Decrease in Current Liabilities Increase in Current Liabilities Sundry creditors Sundry creditors 16609426.5 - - 66804156 Term loans 10977613.34 - 6224409 - DCC bank 2695505 2986176 Others Statutory payable - - - - Excise duty Excise duty - -- - Increase in working capital Decrease in working capital - 62534882.96 546925994.5 - Total 990615903.72 103477994 Total 992475612.72 163184116.61 Babasabpatilfreepptmba.com Page 50

- 51. The Krishna Co-operative Sugar Factory Limited, Athani TABLE 3: COMPUTATION OF WORKING CAPITAL: Year Current Assets Current Liabilities Working Capital 2005-06 25,88,44,064 12,83,39,937 13,05,04,127 2006-07 72,30,11,048 32,37,78,891 39,92,32,157 2007-08 81,24,64,742 39,73,58,597 41,51,06,145 Working Capital 450000000 399232157 415106145 400000000 Working Capital 350000000 300000000 250000000 200000000 Working 130504127 150000000 Capital 100000000 50000000 0 2005-06 2006-07 2007-08 Year Interpretation: It was in positive in the following 3years i.e., from 2005-06 to 2006-07 and in 2007-08 it has been in comparatively high positive terms i.e., amount of Rs. 41,51,06,145. It indicates that, in the 2007-08, the working capital has met its current obligations... Babasabpatilfreepptmba.com Page 51

- 52. The Krishna Co-operative Sugar Factory Limited, Athani CURRENT RATIO: Current ratio is also known as ‘working capital ratio’ which compares the total current assets of the business unit to its current liabilities. This ratio measures its short-term solvency, which only reflects its ability to meet short-term obligation. The higher the ratio the greater the business unit’s ability to meet current obligation and more the safety of funds of the short-term creditors Thus, a current ratio of 2:1 is considered satisfactory. Current Assets Current ratio = ——————— Current liabilities TABLE 4 : COMPUTATION OF CURRENT RATIO Year Current Assets Current Liabilities Ratio 2005-06 25,88,44,064 12,83,39,937 2.01 2006-07 72,30,11,048 32,37,78,891 2.23 2007-08 81,24,64,742 39,73,58,597 2.04 Ratio 2.25 2.2 2.15 2.1 Ratio Ratio 2.05 2 1.95 1.9 2005-06 2006-07 2007-08 Year Interpretation: The Current Ratio for the year 2005-06 is below standard ratio. It is increased to 2.01 to 2.23 for 2006-07, which is above standard ratio. For the year 2007-08 it Babasabpatilfreepptmba.com Page 52

- 53. The Krishna Co-operative Sugar Factory Limited, Athani is decreased to 2.23 to 2.04, which below standard ratio. It indicates that, the firm is able to meet its current obligations. QUICK RATIO: It establishes a relationship between quick, or liquid assets and current liabilities. An asset is liquid if it can be converted into cash immediately or reasonably soon without a loss of value. Cash is the most liquid asset. Inventories are considered to be less liquid. Quick assets (current assets - Inventory) Quick ratio = ———————————————— Current liabilities TABLE 5 : COMPUTATION OF QUICK RATIO: Year Current Assets Current Liabilities Ratio 2005-06 4,95,54,229 12,83,39,937 0.380 2006-07 7,64,04,609 32,37,78,891 0.235 2007-08 7,04,60,447 39,73,58,597 0.177 Ratio 0.4 0.35 0.3 0.25 Ratio 0.2 Ratio 0.15 0.1 0.05 0 2005-06 2006-07 2007-08 Year Babasabpatilfreepptmba.com Page 53

- 54. The Krishna Co-operative Sugar Factory Limited, Athani Interpretation: The ideal ratio is 1:1. The Quick ratio of current assets & liabilities are below the standard ratio. It indicates that the firm’s liquidity position is good. CURRENT ASSET TURNOVER RATIO: Assets are used to generate sales. Therefore, a firm should manage its assets efficiently to maximize sales. The relationship between sales & assets is called assets turnover. Sales Current asset turnover ratio= ______________ Current assets TABLE 6 : COMPUTATION OF CURRENT ASSET TURNOVER RATIO: Year Sales Current Assets Ratio 2005-06 94,06,20,046 25,88,44,064 3.63 2006-07 79,13,32,804 72,30,11,048 1.09 2007-08 40,96,02,092 81,24,64,742 0.50 Babasabpatilfreepptmba.com Page 54

- 55. The Krishna Co-operative Sugar Factory Limited, Athani Ratio 4 3.5 3 Ratio 2.5 2 Ratio 1.5 1 0.5 0 2005-06 2006-07 2007-08 Year Interpretation: The above table exhibits how the current assets were efficiently utilized in generating sales. In the above table the ratio shows that, the firm has utilized the currents assets properly. WORKING CAPITAL TURNOVER RATIO: Net sales Working capital turnover ratio = ———————— Net working capital TABLE 7: COMPUTATION OF WORKING CAPITAL TURNOVER RATIO: Year Net Sales Net working Capital Ratio 2005-06 94,06,20,046 1,15,42,59,862 0.81 2006-07 79,13,32,804 60,73,33,868 1.30 2007-08 40,96,02,092 73,12,59,661 0.56 Babasabpatilfreepptmba.com Page 55

- 56. The Krishna Co-operative Sugar Factory Limited, Athani Ratio 1.4 1.2 1 0.8 Ratio Ratio 0.6 0.4 0.2 0 2005-06 2006-07 2007-08 Year Interpretation: The ratio is fluctuating. That was high in 2006-07, 1.30.and it was negative in 2005-06 i.e. 0.81 and 2007-08 i.e.0.56 it indicates that the working capital has been utilized effectively in 2006-07. INVENTORY MANAGEMENTS: Inventory management is one of the components of working capital. This management is concerned with the effective management of stock or inventory. Inventory consisting of raw material, work-in-progress and finished goods, represent a significant proportion of total current assets. In the case of TKCSFL, the inventory consisting only finished goods these finished goods consist of sugar, molasses& bagasse these inventories are not sold then and there but disposed of as per the company act guidelines for sugar and it’s by products. The effectiveness of working capital is depends on this inventory managements effective. So, effective management of particular in working capital in general can also be evaluated by the computing inventory related ratios. Inventory turnover ratio reflects the relationship Babasabpatilfreepptmba.com Page 56

- 57. The Krishna Co-operative Sugar Factory Limited, Athani between costs of goods old during or given period and the average inventory. This ratio helps the average inventory. This ratio helps in determining the liquidity of a business concern in as a much as it indicates the rate at which the inventories are converted into sales and then into cash ultimately This ratio is calculated by the following ratio. Cost of goods sold Inventory turnover ratio = ———————— Average inventory Where, Cost of goods sold = Sales - Gross profit Opening stock + Closing stock And average inventory = ------------------------------ 2 365 Inventory holding period = ——————————— Inventory turnover ratio TABLE 8: COMPUTATION OF INVENTORY TURNOVER RATIO: Year Sales Average Inventory Ratio 2005-06 26,40,87,564 10,11,41,647 2.61 2006-07 69,74,45,272 67,11,26,643 1.03 2007-08 84,53,40,822 73,42,01,254 1.15 Babasabpatilfreepptmba.com Page 57