Recomendados

Mais conteúdo relacionado

Destaque

Destaque (12)

Semelhante a Tp&l organiser

Mais de BSTAI

Mais de BSTAI (15)

Tp&l organiser

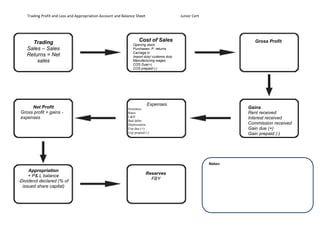

- 1. Trading Profit and Loss and Appropriation Account and Balance Sheet Junior Cert Trading Cost of Sales Gross Profit Opening stock Sales – Sales Purchases- P. returns Carriage in Returns = Net Import duty/ customs duty sales Manufacturing wages COS Due(+) COS prepaid (-) Expenses Net Profit Insurance Gains Gross profit + gains - Rates Rent received expenses L&H Interest received Bad debts Depreciation Commission received Exp due (+) Gain due (+) Exp prepaid (-) Gain prepaid (-) Notes: Appropriation Reserves Insert text here + P& L balance FBY -Dividend declared (% of issued share capital)

- 2. Trading Profit and Loss and Appropriation Account and Balance Sheet Junior Cert Fixed Assets – Current Assets Current Liabilities Depreciation = NBV Closing stock Dividend declared Debtors Machinery Creditors Cash Bank overdraft Equipment Bank Gain Prepaid Land Gain due Expense due Expense prepaid Premises COS due COS Prepaid Fixtures & Fittings Financed By Total Net Assets Working Capital Authorised share capital Working capital CA- CL Issued share capital + &Fixed assets NBV reserves +long term total loan Notes: Capital Employed Reserves Insert text here Issued share capital + reserves +long term loan