5. 7

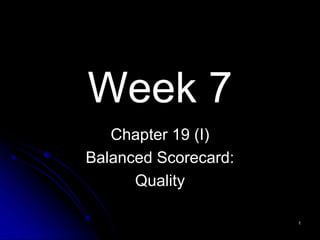

NON-FINANCIAL MEASURES

BIG DECISIONS

—ALLOCATE RESOURCES

FEEDBACK

CEO

CFO

CIO

CUSTOMER INTERNAL

PROCESS

LEARNING + GROWTH

FINANCIAL MEASURES

TRAINING

GET

ATTENTION

Big Picture

Decision Relevance of Financial and Non-Financial

Measures inside the Firm

INVEST

MENT

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

6. 8

Week 7-8 Learning Outcome Summary

Introduction

Quality-Definition

Quality-Measurement

Learning objective 1: Explain the four cost categories in a costs-of-

quality program

Learning objective 2: Develop Nonfinancial measures and methods to

improve quality

Learning objective 3: Use cost of quality measures to make decisions

Learning objective 4: Use financial and nonfinancial measures to

evaluate quality

Time-related Measurement

Learning objective 5: Describe customer-response time and on-time

performance

Learning objective 6: Describe why delay occurs and their costs

Learning objective 7: Use financial and nonfinancial measures of time

Learning objective 8: Theory of Constraints

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

7. 9

Why quality and time?

Quality and time-based competition are often critical parts of any

competitive strategy

Quality based competition

Attributes of quality

1. Design and Conformance quality

who is our customer?

2. Drivers of quality (Casual influences)

How to execute?

Prevention Appraisal Internal failure External failure

SCA

Competitors

Customer

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

8. How important is Quality?

• Needle in Teddy Bear

• Quality and Cost are not Tradeoffs

10

12. Simple Factory Audit in

Asia

Extensive factory audit

(ISO 9001) in China and

Asia

Corporate Social Audits

(SA 8000) in China and

Asia

Pre Production

Inspection

First Article Inspection

Production Monitoring

in China & Asia

During Production

Inspection

Defect Sorting Service

Pre Shipment Inspection

Container Loading

Supervision

Lab Testing & Certification

China Sourcing Academy | 45

2. Three Circle Control Framework

3. Measurement and Verification (e.g. Asia Quality Focus)

14. ALWAYS BE WATCHFUL

Product arrives on time

Product is as ordered

Product works

CAN THEY REPLICATE THE

EXPERIENCE?

Summary

China Sourcing Academy | 35

16. 21

Define it

Product quality dimensions

Design

Conformance

Service quality

Measure it

Financial

Customer

Internal

Learning and Growth

Use it

Competing on Quality

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

17. 22

Quality – the total features and characteristics of a product or a

service made or performed according to specifications to satisfy

customers at the time of purchase and during use

A quality focus reduces costs and increases customer satisfaction

Quality as a Competitive Tool

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

18. 23

Actual

Performance

Design

Specifications

Customer

Satisfaction

Conformance

Quality

Failure

Design

Quality

Failure

1. Design Quality – refers to how closely the characteristics of a product or service

meet the needs and wants of customers

2. Conformance Quality – refers to the performance of a product or service relative to

its design and product specifications

Two Basic Aspects of Quality (Define it!)

Quality and Failure (Define it!)

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

19. 25

Performance

Refers to the efficiency with which a product achieves its intended purpose.

Features

Attributes of a product that supplement a product’s basic performance.

Reliability

The propensity for a product to perform consistently over its useful design life.

Conformance

Numerical dimensions for a product’s performance, such as capacity, speed, size,

durability, color, or the like.

Product Quality Dimensions (Define it!)

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

20. 26

Durability

The degree to which a product tolerates stress or trauma without failing.

Serviceability

Ease of repair.

Aesthetics

Subjective sensory characteristics such as taste, feel, sound, look, and smell.

Perceived Quality

Based on customer opinion. Customers imbue products and services with their

understanding of their goodness.

Product Quality Dimensions (Define it!)

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

21. 28

Service Quality Dimensions (Define it!)

• Tangibles

•Include the physical appearance of the service facility, the equipment,

the personnel, and the communication material.

• Service Reliability

•Differs from product reliability in that it relates to the ability of the service

provider to perform the promised service dependably and accurately.

• Responsiveness

•The willingness of the service provider to be helpful and prompt in providing

service.

• Assurance

•The knowledge and courtesy of employees and their ability to inspire trust

and confidence.

• Empathy

•Caring, individual attention paid to customers by the service firm.

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

22. 29

1. Financial

2. Customer

3. Internal Business Process

4. Learning and Growth

Four Perspectives of the Balanced Scorecard

(Measure it!)

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

23. 30

The Financial Perspective: Cost of Quality (COQ)

(Measure it!)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Four Categories of Quality Costs:

1. Prevention Costs – incurred to preclude the production of products that do

not conform to specifications

2. Appraisal Costs – incurred to detect which of the individual units of

products do not conform to specifications

3. Internal Failure Costs – incurred on defective products before they are

shipped to customers

4. External Failure Costs – incurred on defective products after they are

shipped to customers Learning Outcome 1:

Explain the four cost

categories in a costs-of-

quality program

…prevention, appraisal,

internal failure, and external

failure costs

(P. 757)

1

24. What is the reality of the

Cost of Quality Report?

• Nose Job

• Where do the quality costs come from?

31

25. Elements of Costs of Quality Reports (Measure it!)

32

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

The items in Exhibit 19-1 come from all business functions of the value chain, and they

are broader than the internal failure costs of spoilage, rework, and scrap described in

Chapter 18.

26.

27.

28. 36

Example - Photon:

Determining COQ Using Activity-Based Costing (Measure it!)

1. Identify the Chosen Cost Object (Photocopying machines)

2. Identify the Direct Costs of Quality of the Product (Employees such as inspectors and workers

in repair areas who are dedicated to a product line)

3. Select the Activities and Cost-Allocation Bases to Use for Allocating Indirect Costs of Quality to

the Product (Photon indentifies the number of inspection-hours as the cost-allocation base for

the inspection activity)

4. Identify the Indirect Costs of Quality Associated with Each Cost-Allocation Base (e.g.

photocopying machines use 240,000 inspection-hours)

5. Compute the Rate per Unit of Each Cost-Allocation Base (Column 2 of Exhibit 19-2, Panel A,

shows these rates)

6. Compute the Indirect Costs of Quality Allocated to the Product (Quality – related inspection

costs for the photocopying machines are $9,600,000 ($40 per hr * 240,000 inspection-hours))

7. Compute the Total Costs of Quality by Adding All Direct and Indirect Costs of Quality Assigned

to the Product (Photon’s total costs of quality in the COQ report for photocopying machines is

$40.02 million (bottom of column 4, panel A), or 13.3% of current revenues (bottom of column 5)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

We illustrate the issues in managing quality – computing the cost of quality, identifying quality problem,

and taking actions to improve quality, - using Photon Corporation. Photon makes many products;

however, we’ll focus on Photon’s photocopying machines, which earned an operating income of $24

million on revenues of $300 million in 2013.

29. Example - Photon:

Activity-Based COG Analysis

37

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Photon makes many products; however, we’ll focus on Photon’s photocopying machines, which

earned an operating income of $24 million on revenues of $300 million in 2013.

44

30. 38

Opportunity Costs as a result from poor quality:

Contribution Margin and Income forgone from lost sales

Lost Production

Lower Prices

Excluded due to estimation difficulties and being unrecorded as to

the financial accounting records

Cost of Quality Exclusions (Measure it!)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

31. 39

NON-FINANCIAL MEASURES

BIG DECISIONS

—ALLOCATE RESOURCES

FEEDBACK

CEO

CFO

CIO

CUSTOMER INTERNAL

PROCESS

LEARNING + GROWTH

FINANCIAL MEASURES

TRAINING

GET

ATTENTION

Evaluating Strategy

Decision Relevance of Financial and Non-Financial

Measures inside the Firm

INVEST

MENT

32. 40

Example - Osborn, Inc.

Exercise 19-16 – Cost of Quality Analysis (rep old ex)

Osborn, Inc., produces cell phone equipment. Amanda Westerly,

Osborn’s president, decided to devote more resources to the

improvement of product quality after learning that her company

had been ranked fourth in product quality in a 2011 survey of cell

phone users. Osborn’s quality-improvement program has now

been in operation for 2 years, and the cost report shown here has

recently been issued.

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

33. 41

Example - Osborn, Inc.

Exercise 19-16 – Cost of Quality Analysis (rep old ex)

1. For each period, calculate the ratio of each COQ category to

revenues and to total quality costs

2. Based on the results of requirement 1, would you conclude that

Osborn’s quality program has been successful? Prepare a short

report to present your case.

3. Based on the 2011 survey, Amanda Westerly believed that Osborn

had to improve product quality. In making her case to Osborn

management, how might Westerly have estimated the opportunity

cost of not implementing the quality improvement program?

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

34. Example - Osborn, Inc.

19-16. The ratios of each COQ category to revenues and to total quality costs for each period are

as follows: Osborn, Inc. : Semi-annual Costs of Quality Report (in thousands)

6/30/2012 12/31/2012 6/30/2013 12/31/2013

Actual

% of

Revenues

% of Total

Quality

Costs Actual

% of

Revenues

% of Total

Quality Costs Actual

% of

Revenues

% of Total

Quality

Costs Actual

% of

Revenues

% of Total

Quality Costs

(1) (2) = (3) = (4) (5) = (6) = (7) (8) = (9) = (10) (11) = (12) =

(1) ÷

$8,240

(1) ÷

$2,040

(4) ÷

$9,080 (4) ÷ $2,159 (7) ÷ $9,300(7) ÷ $1,605

(10) ÷

$9,020

(10) ÷

$1,271

Prevention costs

Machine maintenance $ 440 $ 440 $ 390 $ 330

Supplier training 20 100 50 40

Design reviews 50 214 210 200

Total prevention costs 510 6.2% 25.0% 754 8.3% 34.9% 650 7.0% 40.5% 570 6.3% 44.9%

Appraisal costs

Incoming inspection 108 123 90 63

Final testing 332 332 293 203

Total appraisal costs 440 5.3% 21.6% 455 5.0% 21.1% 383 4.1% 23.9% 266 3.0% 20.9%

Internal failure costs

Rework 231 202 165 112

Scrap 124 116 71 67

Total internal failure

costs 355 4.3% 17.4% 318 3.5% 14.7% 236 2.5% 14.7% 179 2.0% 14.1%

External failure costs

Warranty repairs 165 85 72 68

Customer returns 570 547 264 188

Total external failure

costs 735 8.9% 36.0% 632 7.0% 29.3% 336 3.6% 20.9% 256 2.8% 20.1%

Total quality costs $2,040 24.7% 100.0% $2,159 23.8% 100.0% $1,605 17.2% 100.0% $1,271 14.1% 100.0%

42

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

35. 43

Example - Osborn, Inc.

Exercise 19-16 – Cost of Quality Analysis

2. Has Osborn’s quality program been successful?

• Total quality costs as a percentage of total revenues have declined

from 24.7% to 14.1%.

• External failure costs, those costs signaling customer dissatisfaction,

have declined from 8.9% of total revenues to 2.8% of total revenues and

from 36% of all quality costs to 20.1% of all quality costs. These declines

in warranty repairs and customer returns should translate into increased

revenues in the future.

• Internal failure costs as a percentage of revenues have been halved

from 4.3% to 2%.

• Appraisal costs have decreased from 5.3% to 3% of revenues.

Preventing defects from occurring in the first place is reducing the

demand for final testing.

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

36. 44

Example - Osborn, Inc.

Exercise 19-16 – Cost of Quality Analysis

2. Has Osborn’s quality program been successful?

• Quality costs have shifted to the area of prevention where problems

are solved before production starts: total prevention costs (maintenance,

supplier training, and design reviews) have risen from 25% to 44.9% of

total quality costs. The $60,000 increase in these costs is more than offset

by decreases in other quality costs.

• Because of improved designs, quality training, and additional pre-

production inspections, scrap and rework costs have almost been halved

while increasing sales by 9.5%.

• Production does not have to spend an inordinate amount of time with

customer service since they are now making the product right the first

time and warranty repairs and customer returns have decreased.

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

37. 45

Example - Osborn, Inc.

Exercise 19-16 – Cost of Quality Analysis

3. How might you estimate the opportunity cost of not

implementing the quality improvement program?

• Sales and market share would continue to decline if the quality

program was not implemented and then calculated the loss in

revenue and contribution margin.

• The company would have to compete on price rather than

quality and calculated the impact of having to lower product prices.

• Opportunity costs are not recorded in accounting systems

because they represent the results of what might have happened if

the company had not improved quality. Nevertheless, opportunity

costs of poor quality can be significant. It is important for Osborn to

take these costs into account when making decisions about quality.

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

38. 46

The Customer Perspective (Measure it!)

Nonfinancial Measures of Customer Satisfaction include:

• Surveys on satisfaction

• Market share

• Number of defective units shipped to customers

• Number of customer complaints

• Product fail rates

• Delivery delays / On-time deliveries

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Learning Outcome 2:

Develop nonfinancial

measures and methods to

improve quality

…customer satisfaction

measures, internal-business

process measures and

learning-and-growth

measures.(P. 761)

2

39. 47

Three techniques for identifying and analyzing quality

problems:

Control Charts

Pareto Diagrams

Cause-and-Effect Diagrams

Internal Business Perspective (Measure it!)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

40. Internal Business Perspective -Control Charts

(Measure it!)

Example - Photon’s copier problem

48

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

41. This Pareto diagram shows quality problem with respect to Photon’s photocopying

machines and also indicates how frequently each type of defect occurs.

49

Internal Business Perspective Pareto Diagrams

(Measure it!)

Example - Photon’s copier problem

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

42. Multiple suppliers

Incorrect specification

Variation in purchased

components

Flawed part design

Incorrect

manufacturing

sequence

Inadequate tools

Incorrect speed

Poor

maintenance

Inadequate

supervision

Poor training

New operator

Internal Business Perspective Cause-and-Effect

Diagrams (Measure it!)

Example - Photon’s copier problem

50

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Human Factors Methods and

Design Factors

Machine-related

Factors

Materials and

Components Factors

43. 51

Percentage of defective products

Average repair time at customer site

Percentage of reworked products

Number of different types of defects found

Number of design and process changes made

Internal Business Perspective Non-financial

Measures (Measure it!)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

44. 53

Employee turnover ratio

Employee empowerment – number of processes in which

employees have the right to make decisions without consulting

supervisors

Employee satisfaction

Employee training

The Learning and Growth Perspective

Non-financial Measures (Measure it!)

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

45. Application of relevant cost concept in Chapter 11

Example - Photon’s copier problem

Two solutions proposed (p.765)

Electronically inspect and test the frames before production starts.

Redesign and strengthen the frames and their shipping containers to

withstand mishandling during transportation.

See Exhibit 19-6

Estimated incremental costs

Cost savings from less rework, customer support and repairs

Increased contribution margin from higher sales as a result of building

a reputation for quality and performance (Exhibit 19-6, line 14).

54

Relevant costs and Benefits of Evaluating Quality

Improvement

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Learning Outcome 3:

Use costs of quality measures to

make decisions…identify relevant

incremental costs and benefits

and opportunity costs to evaluate

tradeoffs. (P765)

3

46. Relevant costs and Benefits of Evaluating

Quality Improvement

Exhibit 19-6 Estimated Effects of Quality-Improvement Actions on Costs of Quality for Photocopying Machines at Photon Corporation

Relevant Costs and Benefits of

Further Inspecting Incoming

Frames

Redesigning Frames

Relevant cost Relevant Benefit per

Unit

Quantity Total

Benefits

Quantity Total Benefits

(1) (2) (3) (4) (5) (6)

Additional inspection and testing costs $(400,000)

Additional process engineering costs $(300,000)

Additional design engineering costs $(160,000)

(2)X(3) (2)X(5)

Savings in rework costs $40 per hr 24,000 hrs $960,000 32,000 hrs $1,280,000

Savings in customer-support costs $20 per hr 2,000 hrs 40,000 2,800 hrs 56,000

Savings in transportation costs for repair parts $180 per load 500 loads 90,000 700 loads 126,000

Savings in warranty repair costs $45 per hr 20,000 hrs 900,000 28,000 hrs 1,260,000

Total contribution margin from additional sales $6,000 per copier 250 copiers 1,500,000 300 copiers 1,800,000

Net cost savings and additional contribution margin $3,090,000 $3,862,000

Difference in favor of redesigning frames $772,000

55

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

1. Estimated

incremental costs

3. Increased contribution

margin from higher sales

as a result of building a

reputation for quality and

performance

2. Cost savings from

less rework, customer

support and repairs

47. 56

Advantages of Financial Measures of Quality

(Measure it!)

COQ focuses managers’ attention on the costs of poor quality

COQ measures assist in problem solving by comparing costs and

benefits of different quality-improvement programs and setting

priorities for cost reduction

COQ provides a single, summary measure of quality performance for

evaluating tradeoffs among the costs of prevention, appraisal,

internal failure, and external failure

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

Learning Outcome 4:

Use financial and nonfinancial

measures to evaluate quality

…nonfinancial measures are

leading indicators of future costs of

quality. (P766)

4

48. 57

Advantages of non-financial Measures of Quality

(Measure it!)

Nonfinancial measures of quality are often easy to quantify and

understand

Nonfinancial measures direct attention to physical processes and to

areas that need improvement

Nonfinancial measures provide immediate short-run feedback on

whether quality-improvement efforts have succeeded

Nonfinancial measures are useful indicators of future long-run

performance

Introduction Quality-Definition

Quality-

Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures

49. 58

NON-FINANCIAL MEASURES

BIG DECISIONS

—ALLOCATE RESOURCES

FEEDBACK

CEO

CFO

CIO

CUSTOMER INTERNAL

PROCESS

LEARNING + GROWTH

FINANCIAL MEASURES

TRAINING

GET

ATTENTION

Evaluating Strategy

Decision Relevance of Financial and Non-Financial

Measures inside the Firm

INVEST

MENT

50. 59

Summary

Introduction

Quality-Definition

Quality-Measurement

Learning objective 1: Explain the four cost categories in a costs-of-

quality program

Learning objective 2: Develop Nonfinancial measures and methods to

improve quality

Learning objective 3: Use cost of quality measures to make decisions

Learning objective 4: Use financial and nonfinancial measures to

evaluate quality

Time-related Measurement

Learning objective 5: Describe customer-response time and on-time

performance

Learning objective 6: Describe why delay occurs and their costs

Learning objective 7: Use financial and nonfinancial measures of time

Learning objective 8: Theory of Constraints

Introduction Quality-Definition Quality-Measurement

BSC Time-Related

Measures

Theory of ConstraintsTime-related Measures