Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Mcqs on backtesting VaR model with solution

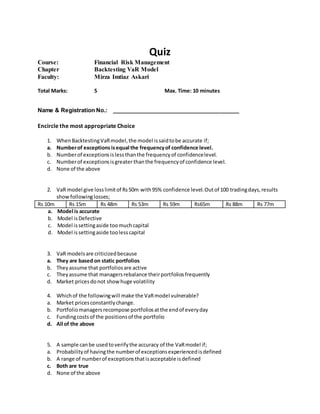

- 1. Quiz Course: Financial Risk Management Chapter Backtesting VaR Model Faculty: Mirza Imtiaz Askari Total Marks: 5 Max. Time: 10 minutes Name & Registration No.: ________________________________________ Encircle the most appropriate Choice 1. WhenBacktestingVaRmodel,the model issaidtobe accurate if; a. Numberof exceptions isequal the frequencyof confidence level. b. Numberof exceptionsislessthanthe frequencyof confidencelevel. c. Numberof exceptionsisgreater thanthe frequencyof confidence level. d. None of the above 2. VaR model give losslimitof Rs50m with95% confidence level.Outof 100 tradingdays,results showfollowinglosses; Rs 10m Rs 15m Rs 48m Rs 53m Rs 59m Rs65m Rs 88m Rs 77m a. Model is accurate b. Model isDefective c. Model issettingaside toomuchcapital d. Model issettingaside toolesscapital 3. VaR modelsare criticizedbecause a. They are based on static portfolios b. Theyassume that portfoliosare active c. Theyassume that managersrebalance theirportfoliosfrequently d. Market pricesdonot showhuge volatility 4. Whichof the followingwill make the VaRmodel vulnerable? a. Market pricesconstantlychange. b. Portfoliomanagersrecompose portfoliosatthe endof everyday c. Fundingcostsof the positionsof the portfolio d. All of the above 5. A sample canbe usedtoverifythe accuracy of the VaRmodel if; a. Probabilityof havingthe numberof exceptionsexperiencedisdefined b. A range of numberof exceptionsthatisacceptable isdefined c. Both are true d. None of the above

- 2. 6. Type 1 error formodel verificationis; a. Acceptingawrong model b. Rejectinga correct model c. Acceptingacorrect model d. None of the above 7. If LR > 3.84, then a. Rejectthe hypothesisthat model is correct b. Acceptthe hypothesisthatmodel iscorrect c. Rejectthe hypothesisthatmodel isincorrect d. None of the above 8. HoldingperiodforVaRpotential lossesshouldcorrespondto a. Time requiredtoliquidatethe portfolio b. Time requiredtohedge the portfolio c. Periodoverwhichportfolioisnotexpectedtochange d. All of the above