ETV - Bad loans, ECB intervention and competitive advantages

•

0 gostou•157 visualizações

Post published in the Innovation Models Blog following the interview of Hugo Mendes Domingos in ETV's (Portuguese Economic TV) Closing Bell in August 8 2012 about the current increase bad credit loans by households in Portugal.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (14)

Destaque

Destaque (17)

Semelhante a ETV - Bad loans, ECB intervention and competitive advantages

Semelhante a ETV - Bad loans, ECB intervention and competitive advantages (20)

Mais de Hugo Mendes Domingos

Mais de Hugo Mendes Domingos (20)

ETV - Bad loans, ECB intervention and competitive advantages

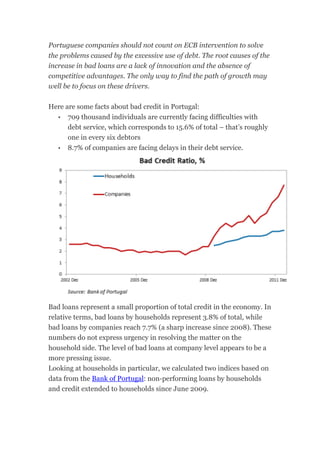

- 1. Portuguese companies should not count on ECB intervention to solve the problems caused by the excessive use of debt. The root causes of the increase in bad loans are a lack of innovation and the absence of competitive advantages. The only way to find the path of growth may well be to focus on these drivers. Here are some facts about bad credit in Portugal: • 709 thousand individuals are currently facing difficulties with debt service, which corresponds to 15.6% of total – that’s roughly one in every six debtors • 8.7% of companies are facing delays in their debt service. Bad loans represent a small proportion of total credit in the economy. In relative terms, bad loans by households represent 3.8% of total, while bad loans by companies reach 7.7% (a sharp increase since 2008). These numbers do not express urgency in resolving the matter on the household side. The level of bad loans at company level appears to be a more pressing issue. Looking at households in particular, we calculated two indices based on data from the Bank of Portugal: non-performing loans by households and credit extended to households since June 2009.

- 2. Bad loans by households are increasing, as expected during an economic crisis. This has not stopped banks to continue to extend credit to households during the same period, as the index shows. Possible solutions No-one should count on the European Central Bank to solve the bad debt problem all by itself. The notion that Portugal’s European partners will solve the country’s economic difficulties by injecting money into the economy could lead to disappointment and is in fact, dangerous. We believe that the answer lies elsewhere: Individuals can be influenced to use less debt but ultimately it comes down to personal responsibility. In the case of companies, the answer lies in good management practices. The turnaround at company level should come from a sense of purpose, to develop new paths and bet on innovative projects. The reality we see, however, is different. Companies rarely show an ability to develop projects that actually result in competitive advantages. Bad loans are one of the consequences of that inability to forge economic growth. Companies should use debt as an instrument to finance growth and focus on innovative projects that are assessed and scrutinized by banks. This is a simple principle that would result in stronger companies and a healthier financial system.

- 3. Hugo Mendes Domingos Comments on ETV's Closing Bell, August 8th 2012 (in Portuguese): Youtube link - http://www.youtube.com/watch?v=4Tb74E2sglE&feature