Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a Charoen pokphand foods pcl[1]

Semelhante a Charoen pokphand foods pcl[1] (20)

Último

Último (20)

Charoen pokphand foods pcl[1]

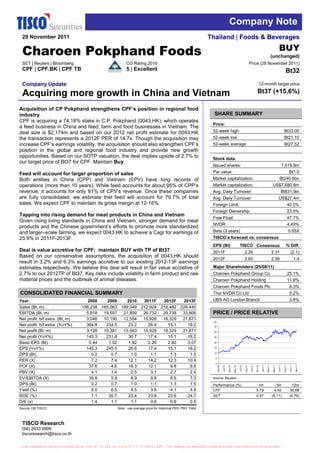

- 1. Company Note 29 November 2011 Thailand | Foods & Beverages BUY Charoen Pokphand Foods (unchanged) SET | Reuters | Bloomberg CG Rating 2010 Price (28 November 2011) CPF | CPF.BK | CPF TB 5 | Excellent Bt32 Company Update 12-month target price Acquiring more growth in China and Vietnam Bt37 (+15.6%) Acquisition of CP Pokphand strengthens CPF’s position in regional food industry SHARE SUMMARY CPF is acquiring a 74.18% stake in C.P. Pokphand (0043.HK), which operates Price: a feed business in China and feed, farm and food businesses in Vietnam. The deal size is $2,174m and based on our 2012 net profit estimate for 0043.HK 52-week high Bt33.00 the transaction represents a 2012F PER of 14.7x. Though the acquisition may 52-week low Bt21.10 increase CPF’s earnings volatility, the acquisition should also strengthen CPF’s 52-week average Bt27.52 position in the global and regional food industry and provide new growth opportunities. Based on our SOTP valuation, the deal implies upside of 2.7% to Stock data: our target price of Bt37 for CPF. Maintain Buy. Issued shares: 7,519.9m Feed will account for larger proportion of sales Par value: Bt1.0 Both entities in China (CPP) and Vietnam (CPV) have long records of Market capitalization: Bt240.6bn operations (more than 10 years). While feed accounts for about 95% of CPP’s Market capitalization: US$7,680.8m revenue, it accounts for only 61% of CPV’s revenue. Once these companies Avg. Daily Turnover: Bt831.9m are fully consolidated, we estimate that feed will account for 79.7% of total Avg. Daily Turnover: US$27.4m sales. We expect CPF to maintain its gross margin at 12-16%. Foreign Limit: 40.0% Foreign Ownership: 23.0% Tapping into rising demand for meat products in China and Vietnam Free Float: 47.7% Given rising living standards in China and Vietnam, stronger demand for meat NVDR: 4.49% products and the Chinese government’s efforts to promote more standardized and larger–scale farming, we expect 0043.HK to achieve a Cagr for earnings of Beta (3 years) 0.65X ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF. TISCO’s forecast vs. consensus 25.9% in 2011F-2013F. EPS (Bt) TISCO Consensus % Diff. Deal is value accretive for CPF; maintain BUY with TP of Bt37 2011F 2.26 2.31 (2.1) Based on our conservative assumptions, the acquisition of 0043.HK should 2012F 2.60 2.56 1.4 result in 3.2% and 6.3% earnings accretive to our existing 2012-13F earnings estimates respectively. We believe this deal will result in fair value accretive of Major Shareholders (25/08/11) 2.7% to our 2012TP of Bt37. Key risks include volatility in farm product and raw Charoen Pokphand Group Co 25.1% material prices and the outbreak of animal diseases. Charoen Pokphand Holding 11.8% Charoen Pokphand Foods Plc 6.3% CONSOLIDATED FINANCIAL SUMMARY Thai NVDR Co Ltd 5.2% Year 2008 2009 2010 2011F 2012F 2013F UBS AG London Branch 3.8% Sales (Bt, m) 156,238 165,063 189,049 212,924 218,482 226,440 EBITDA (Bt, m) 5,818 19,597 21,859 26,732 29,738 33,806 PRICE / PRICE RELATIVE Net profit. b/f extra. (Bt, m) 3,046 10,190 12,554 15,928 18,329 21,671 Bt Net profit. b/f extra. (YoY%) 364.8 234.5 23.2 26.9 15.1 18.2 35 Net profit (Bt, m) 3,128 10,381 13,563 15,928 18,329 21,671 30 Net profit (YoY%) 145.3 231.8 30.7 17.4 15.1 18.2 25 Basic EPS (Bt) 0.44 1.52 1.92 2.26 2.60 3.07 20 EPS (YoY%) 145.3 245.5 26.6 17.4 15.1 18.2 15 10 DPS (Bt) 0.2 0.7 1.0 1.1 1.3 1.5 5 PER (X) 7.2 7.4 12.1 14.2 12.3 10.4 0 PCF (X) 37.6 4.6 16.3 12.1 9.8 8.6 Nov-09 Nov-10 Nov-11 Jan-10 Jun-10 Jan-11 Jun-11 Mar-10 May-10 Aug-10 Oct-10 Mar-11 May-11 Aug-11 Oct-11 PBV (X) 4.1 1.4 2.5 3.1 2.7 2.4 EV/EBITDA (X) 39.9 5.9 8.9 9.8 8.6 7.3 Source: Reuters DPS (Bt) 0.2 0.7 1.0 1.1 1.3 1.5 Performance (%) -1m -3m -12m Yield (%) 6.0 6.5 4.5 3.5 4.1 4.8 CPF 5.79 4.92 30.08 ROE (%) 7.1 20.7 23.4 23.8 23.6 24.7 SET 0.97 (5.11) (0.76) D/E (x) 1.4 1.1 1.1 0.8 0.6 0.5 Source: DB TISCO Note : use average price for historical PER, PBV, Yield TISCO Research (66) 2633 6999 tiscoresearch@tisco.co.th Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 2. Company Note – CPF CPF to acquire 74.18% stake in 43.HK On Friday CPF announced that its board of directors had approved the acquisition of a 74.18% stake in C.P. Pokphand (43.HK), an operator of a feed business in China (CPP) and feed, farm and food businesses in Vietnam (CPV). The deal size is USD2,174m (Bt66,307m). CPF will pay for the acquisition by issuing 694m of its own shares to the CP Group (31.4% of the deal value at Bt30/share with a total value of USD683m or Bt20.8bn). The remainder (USD1,491m or Bt45,475m) will be paid by cash which may come from internal cash flow and debt. After the acquisition, CPF will hold a 74.18% stake in 43.HK (CPF does not have to make a tender offer for the rest of 43.HK shares, according to Hong Kong Stock Exchange rules) and 100% in CPV (CPF already has a 29.18% holding in CPV). Meanwhile the CP Group’s stake in CPF will increase to 49.9% from 42.15% pre- acquisition (see details in Figs. 1-3). Figure 1. Details of the transaction C.P. Pokphand (Hang Seng ticker: 43), an operator of feed businesses in China and Target Vietnam USD2,174m or Bt66,307m: CPF is buying at HKD0.9 per share and will pay by issuing Deal value 694m CPF shares (at Bt30/share or a total of USD683m or Bt20.8bn) and cash of USD1,491m or Bt45.5bn CPF to buy 74.18% of 43.HK shares from CP Group. After the transaction, CPF will hold Deal structure a 74.18% stake in 43.HK while CP Group will hold a 49.9% holding in CPF. Advisor UBS Source: Company data Figure 2. Shareholding structure Pre-acquisition Post-acquisition Public CPG & related parties CPIH Public Public CPG & related parties 70.22% 3.96% 50.10% 49.90% ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF. 42.15% 57.85% CPF CPP 25.82% CPF (CPF TB) (43 HK) (CPF TB) 29.18% 70.82% 74.18% CPV- CPP Vietnam (43 HK) 70.82% 29.18% CPV- Vietnam Source: Company data Figure 3. Indicative timeline BoD's approval November 25, 2011 Book closure December 21, 2011 Record date December 22, 2011 EGM January 18, 2012 Source: Company data 2 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 3. Company Note – CPF Adding to feed business profile 43.HK comprises two main entities: 1) C.P. Pokphand (CPP) which operates a feed business in China. This was acquired by 43.HK in November 2009 and consolidated into the company in February 2010; and 2) C.P. Vietnam (CPV) which operates feed, farm and food businesses in Vietnam. The entity was acquired in early 2011 and has been fully consolidated since July 2011. Both companies have a long track record (more than 10 years) in their respective markets. While feed accounts for about 95% of CPP’s revenue, it accounts for just 61% of CPV’s revenue (farm and food operations account for 34%). Once they are fully consolidated, we estimate that feed will account for 79.7% of CPF’s total sales. We believe it is likely that CPF’s earnings may experience with more volatility as a result of the increased contribution of feed business into its business profiles (revenue contribution from feed may increase from approximately 40% to now a little bit over 50%.) Figure 4. 43.HK’s revenue structure 1H11 Revenue structure by business 2011F Revenue contribution by entity CPV 38% Others 5% Feed Others 95% 4% CPP 58% Source: Company data Expect strong earnings growth by 43.HK ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF.meat Given rising living standards in China and Vietnam, stronger demand for products and the Chinese government’s efforts to promote more standardized and larger–scale farming (partly to avoid the food scares of recent years), we believe that CPP and CPV should achieve moderate to high earnings growth over the next few years (see Fig. 5). The feed business is operated on a cost-plus basis (historical data shows that gross margins range from 12-16%, with lower raw material prices normally resulting in higher margins). There is also room for value-added innovations (with R&D and quality feed, farm yields can be improved). For our earnings estimates, we used the following assumptions: 1) Raw materials: these account for 85% of total production costs of which corn and soybean meal accounts for almost 70%. Therefore, we used corn and soybean meal price movements as the main benchmark in calculating sales prices and gross margin. 2) Sales volume: based on the consumption outlook, historical performance and level of competition, we expect sales volume growth of 10% for CPP and 8-15% for CPV. 3 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 4. Company Note – CPF Figure 5. Assumptions and earnings estimates of 0043.HK 43.HK 2009 2010 2011F 2012F 2013F Main assumptions Corn (US$/ ton) 147 169 237 225 217 Change (%) (15.2) 1.2 27.4 (6.7) (1.6) Soybean meal (US$/ ton) 326 301 349 320 322 Change (%) (2.2) (7.8) 16.2 (8.3) 0.6 Sales volume assumptions Livestock feed (‘000 tons) China 3,584 3,058 3,364 3,700 4,070 Growth (%) (14.7) 10.0 10.0 10.0 Vietnam 892 1,022 1,060 1,210 1,404 Growth (%) 14.7 3.7 14.1 16.1 Aquaculture feed (‘000 tons) China 422 365 402 442 486 Growth (%) (13.5) 10.0 10.0 10.0 Vietnam 271 237 275 302 329 Growth (%) (12.6) 15.8 9.8 9.0 43.HK Revenue (US$, m) 74 1,951 2,780 3,897 4,323 EBIT (US$, m) 10 198 282 373 411 Net profit (US$, m) 9 133 180 242 266 Revenue growth (%) 15.1 50.2 15.0 15.0 15.0 Net profit growth (%) 187.1 1,453.0 35.4 34.7 10.0 Gross margin (%) 12.8 15.9 17.5 16.6 16.5 EBIT margin (%) 14.0 10.1 10.1 9.6 9.5 CPP Revenue (US$, m) 1,948 1,839 2,112 2,279 2,487 EBIT (US$, m) 102 186 223 240 258 Net profit (US$, m) 53 125 145 156 168 Revenue growth (%) 0.2 (5.6) 14.8 ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF.7.9 9.1 Net profit growth (%) 60.0 135.1 16.0 7.8 7.5 Gross margin (%) 13.4 15.9 17.6 17.6 17.4 EBIT margin (%) 5.2 10.1 10.6 10.5 10.4 CPV Revenue (US$, m) 869 1,046 1,297 1,471 1,667 EBIT (US$, m) 61 63 84 100 115 Net profit (US$, m) 17 11 26 32 37 Revenue growth (%) 4.1 20.4 23.9 13.4 13.3 Net profit growth (%) 12.7 (35.7) 135.4 22.6 15.7 Gross margin (%) 14.6 12.6 13.1 13.4 13.5 EBIT margin (%) 7.0 6.1 6.5 6.8 6.9 Source: Company data, Deutsche Bank Figure 6. China’s feed and meat consumption outlook China's Feed volume Pork and poultry consuption per capita in China Tons, m kg CAGR = 7.8% 160 139 70 Pork Poultry 137 140 123 60 120 111 11.7 50 10.7 100 9.7 10.1 10.3 40 80 30 60 47.8 20 38.2 39.3 40.3 42.6 40 20 10 0 0 2006 2007 2008 2009 2011F 2012F 2013F 2015F 2020F Source: Company data 4 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 5. Company Note – CPF Figure 7. Vietnam livestock feed outlook V iet na m 's liv es t oc k f eed pr oduc t ion Tons, m 25 Commercial Feed Home mix 20 4.0 15 6.3 6.5 7.3 10 16.0 5 9.2 10.5 7.5 0 2009 2010 2011F 2015F Source: Company data, Deutsche Bank Slightly positive to CPF’s earnings outlook in 2012-13 due to higher debt burden We expect the acquisition of 0043.HK to result in a sharp rise in interest costs for CPF for the first few years. Although we estimate it will boost CPF’s revenue by 43.8% and 56.3% respectively in 2012-13, the deal will increase its debt burden. We believe CPF may need to issue debentures worth Bt40bn to finance this deal next year. This would result in additional interest expenses of Bt1.8bn and Bt2.8bn in 2012-13F (based on an effective interest rate of 4.5%). We expect CPF’s D/E and D/EBITDA to increase from 0.6x and 1.3x to 1.2x and 2.3x respectively. However, with a projected rise in its EBITDA to Bt38.8bn and Bt48.4bn for these two years, we believe CPF’s cash flow should remain solid. Figure 8. Estimated impact to CPF’s revenue, earnings and debt levels 2011F 2012F 2013F Revenue (Bt, m) ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 212,924 Pre-acquisition 218,482 23:36:03 EST. DownloadPDF. 226,440 Post-acquisition 212,924 314,218 353,878 % change 0.0 43.8 56.3 EBITDA (Bt, m) Pre-acquisition 26,737 29,714 33,772 Post-acquisition 26,737 38,797 48,397 % change 0.0 30.6 43.3 Interest expense (Bt, m) Pre-acquisition 1,463 1,236 895 Post-acquisition 1,463 3,084 3,684 % change 0.0 149.5 311.8 Net profit (Bt, m) Pre-acquisition 15,928 18,329 21,671 Post-acquisition 15,932 20,762 25,263 % change (0.0) (11.7) (14.2) EPS-fully diluted (Bt) Pre-acquisition 2.3 2.6 3.1 Post-acquisition 2.3 2.7 3.3 % change 0.0 3.2 6.3 Interest bearing debt (Bt, m) Pre-acquisition 44,496 37,459 29,974 Post-acquisition 44,496 89,117 89,206 % change 0.0 137.9 197.6 Interest bearing debt/ EBITDA (x) Pre-acquisition 1.7 1.3 0.9 Post-acquisition 1.7 2.3 1.8 Debt to equity (x) Pre-acquisition 0.8 0.6 0.5 Post-acquisition 0.8 1.2 1.1 Source: Deutsche Bank 5 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 6. Company Note – CPF Deal to create another 2.7% accretive value to our current TP We tried to gauge the accretive value of the deal to CPF by using SOTP and applied same multiples that we used with valuation of our current CPF’s 2012TP of Bt37 (we used 12.5x 2012PER for core business, DCF for contribution from CPALL and 10.7x 2012PER for feed business). For the purposes of our valuation we split its business into three parts: 1) domestic and exports sales, with contributions from overseas subsidiaries. We still value this core business as a food company which is striving to increase value-added products (domestic and regional food stocks are trading on an average PER of 12.5x for 2012F), 2) CPALL—as of 9M11, CPF holds a 30% stake in CPALL. We valued CPALL’s contribution to CPF based on our TP of Bt54/share and; 3) 0043.HK—as almost all of 0043.HK’s revenue comes from its feed business, we valued the company based on a conservative 2012F PER of 10.5x (which is in line with the average Thai and regional multiple for such businesses (as shown in Fig. 9). Based on the assumptions listed above, CPF’s fair value post acquisition would increase to Bt38, implying upside of 2.7% to our current TP of Bt37. This would also put the stock on a 2012F PER of 14.6x. Figure 9. CPF’s fair value after acquisition of Bt38 is not expensive even when compared with other feed manufacturers Company Country Mkt Cap PER (x) PBV (x) ROE (%) (US$, m) 2011F 2012F 2011F 2012F 2011F 2012F C.P. Food Thailand 46,936.9 14.4 12.3 3.1 2.7 23.8 23.6 Pre- acquisition C.P. Food Thailand 14.2 11.9 3.1 2.6 23.8 24.8 Post- acquisition Sichuan New Hope China 34,093.1 15.9 16.3 3.4 0.0 24.1 na. C.P. Indonesia Indonesia 26,409.5 15.2 16.9 6.6 6.4 51.8 38.7 Sinofert Holding Hong Kong 12,342.0 17.8 11.5 1.0 0.9 5.5 9.7 Jiangxi Zhengvang China 4,457.1 36.7 31.0 4.3 3.8 11.8 16.3 Tech –A Global Bio-Chem Hong Kong 4,186.7 5.9 4.3 0.6 0.4 10.3 12.8 Technology Xinjiang Tiankang China 3,454.6 31.3 22.1 3.0 3.0 10.1 14.3 Animal-AA ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on Dachan Food Asia Hong Kong 2012-01-15 10.7 1,175.3 23:36:03 EST. DownloadPDF. n.a. 0.7 0.0 7.0 n.a. Lee Feed Mill Thailand 458.2 7.7 n.a. 1.1 0.0 14.0 n.a. Weighted average (pre-acquisition) 15.7 15.2 3.9 2.7 27.3 18.7 Source: Company data, Deutsche Bank, Bloomberg Finance LP; based on closing date price of November 28th, 2011. Figure 10. Based on our post-acquisition assumptions, CPF’’s fair value is Bt38.0/share Base (Bt/share) Value (Bt/share) Target multiple (x) Sum-of-the-part valuation Pre-acq Post-acq Pre-acq Post-acq Pre-acq Post-acq Core Business 2.0 1.7 25.4 20.9 12.5 12.5 CPALL DCF: 9.4 (Based on CPALL's DB TP of Bt54 9.9 9.4 n.a. and CPF's holding in CPALL of 30%) 43.HK 0.16 0.68 1.8 7.3 10.7 10.7 Rounding 0.3 0.3 CPF's 2012 TP (Bt/ share) 37.0 38.0 % change 2.7% Source: Deutsche Bank 6 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 7. Company Note – CPF Risk factors and concerns Volatility in farm commodity prices Volatility in prices of commodities such as pork, chicken, corn and soybean meal can have a major impact on CPF’s gross margin and profitability. CPF’s share price usually comes under downward pressure when prices of raw materials such as corn and soybean meal rise. On the other hand, its share price tends to increase when pork and chicken prices are strong. Although concerns about higher raw material costs may pressure CPF’s share price in the short term, the company has mitigated the risk by buying forward contracts for its major raw material and has also built up corn stockpiles. Outbreak of disease in pigs and poultry Another key risk for CPF is outbreaks of disease in pigs and poultry which can lead to a dramatic decline in the consumption of meat products. During the bird flu outbreak in 2004 many Thais stopped eating chicken while several countries banned the import of poultry from Thailand. As a result, domestic chicken prices collapsed and CPF posted an earnings loss during one quarter. Commerce Ministry price control Government intervention to control food prices can also put pressure on CPF’s margins. During periods when producers plan to raise the price of basic necessities at the same time, the Commerce Ministry may take several months to approve price increases in order to lessen the impact on consumers. Accordingly, this may harm the company’s ability to pass on the increased costs of products and erode its margins. We believe that one product particularly vulnerable to price controls is feed. ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF. 7 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 8. Company Note – CPF CONSOLIDATED INCOME STATEMENT (Bt, m) CONSOLIDATED CASHFLOW STATEMENT (Bt, m) Year Ended December 31, Year Ended December 31, 2009 2010 2011F 2012F 2013F 2009 2010 2011F 2012F 2013F Sales 165,063 189,049 212,924 218,482 226,440 Cash Flows from Operations (CFO) Cost of Goods Sold 135,871 156,351 173,148 176,021 180,015 Net Profit 10,381 13,563 15,928 18,329 21,671 Gross Profit 29,192 32,698 39,776 42,462 46,426 Adjusting Items Not Affecting Cash S&A Expense 18,142 20,632 23,422 24,033 24,908 Depreciation and Amortization 4,719 4,798 5,032 5,216 5,379 Interest Expense 1,949 1,824 1,463 1,236 894 Unrealized FX Loss (Gain) (191) 0 0 0 0 Other Income 2,237 2,484 2,030 2,087 2,163 Others (1,391) 0 325 374 442 Net Profit before Tax 12,929 15,238 20,237 23,287 27,533 + (-) in Working Capital 3,702 (9,999) (2,688) (831) (1,189) Income Tax 2,539 2,388 3,984 4,584 5,420 Net CFO 17,220 9,286 18,597 23,087 26,304 Net Profit before M.I. 10,390 12,850 16,253 18,703 22,113 Cash Flows from Investing Activities (CFI) Net (Profit) Loss of M.I. (200) (296) (325) (374) (442) - (+) in Short-term Investment (37) (3,726) 0 0 0 Net Profit before Extra. Items 10,190 12,554 15,928 18,329 21,671 - (+) in Investment in Affiliates 0 0 0 0 0 FX Gain (Loss) (Net of Tax) 191 1,009 0 0 0 - (+) in Fixed Assets (6,434) (6,285) (7,395) (6,508) (7,229) Other Gain (Loss) 0 0 0 0 0 Net CFI (4,951) (7,995) (7,705) (6,334) (7,285) Net Profit 10,381 13,563 15,928 18,329 21,671 Cash Flows from Financing Activities (CFF) + (-) in Debt Financing (3,856) (927) (5,686) (7,041) (7,491) + (-) in Minority Interest 200 0 325 374 442 + (-) in Share Capital and Premium (1,074) 3,500 0 0 0 + (-) in Warrant 0 0 0 0 0 Revenue Growth (%) 5.6 14.5 12.6 2.6 3.6 + (-) in Equity Adjustment 2,397 (87) 3,514 (325) (374) Gross Margin (%) 17.7 17.3 18.7 19.4 20.5 - Cash Dividend Paid (2,329) (6,884) (7,964) (9,164) (10,836) Net Profit Margin (%) 6.3 7.2 7.5 8.4 9.6 Net CFF (4,862) (4,399) (10,137) (16,531) (18,700) Net Profit Growth (%) 231.8 30.7 17.4 15.1 18.2 Net Cash Increase (Decrease) 7,070 (2,762) 756 222 318 CONSOLIDATED QUARTERLY RESULTS (Bt, m) CONSOLIDATED BALANCE SHEET (Bt, m) 3Q10 4Q10 1Q11 2Q11 3Q11 As of December 31, Sales Revenue 50,296 47,282 45,744 53,230 54,446 2009 2010 2011F 2012F 2013F Cost of Sales 41,056 41,095 38,357 43,578 44,708 Current Assets 53,434 58,971 62,551 63,845 65,692 Gross Profit 9,239 6,186 7,387 9,652 9,739 Current Liabilities 29,637 32,827 30,772 26,388 24,322 S&A Expenses 5,064 5,879 4,581 4,444 4,585 Total Assets 115,698 126,320 132,572 134,985 138,737 Interest Expense 400 477 448 499 400 Total Liabilities 60,719 65,217 59,667 52,866 45,715 ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF. Other Income 514 1,243 311 308 313 Minority Interest 3,095 3,088 4,285 4,334 4,402 Net Profit before Tax 4,926 1,735 3,426 5,981 5,938 Total Equity 51,885 58,015 68,621 77,785 88,621 Income Tax from Operations 778 (180) 623 1,042 1,043 Paid-up Capital 7,520 7,520 7,520 7,520 7,520 Net Profit before M.I. 4,148 1,915 2,803 4,940 4,894 Net (Profit) Loss of M.I. (88) (99) (40) (40) (3) Net Profit before Extra. Items 4,060 1,816 2,763 4,899 4,891 FX Gain (Loss) (Net of Tax) 223 236 23 (30) 21 Gain (Loss) from Asset Write-down 0 0 0 0 0 Other Gain (Loss) 0 0 693 0 168 Net Profit 4,284 2,052 3,479 4,869 5,083 3Q11 Revenue Growth (YoY %) 14.3 3.6 4.9 11.2 8.3 Market Cap (Bt, m) 240,637 Gross Margin (%) 18.4 13.1 16.1 18.1 17.9 Cash&cash equivalent (Bt, m) 8,704 Net Profit Margin (%) 8.5 4.3 7.6 9.1 9.3 Borrowings (Bt, m) 51,922 Net Profit Growth (YoY %) 4.1 (2.8) 7.9 21.7 18.7 Gearing (X) 0.4 KEY FINANCIAL RATIOS FORECAST ASSUMPTIONS 2009 2010 2011F 2012F 2013F 2009 2010 2011F 2012F 2013F Other Incomes to Total Revenue (%) 1.4 1.3 1.0 1.0 1.0 Total Production ('000 Tons/year) S&A Expenses to Sales (%) 11.0 10.9 11.0 11.0 11.0 - Shrimp Feed 519 638 808 808 808 Current (Times) 1.8 1.8 2.0 2.4 2.7 - Animal Feed 2,058 2,040 2,040 2,210 2,295 Quick (Times) 0.9 0.8 0.9 1.1 1.3 - Pork 377 396 404 412 420 A/R Turnover (Days) 31.5 28.7 28.2 29.6 29.5 - Chicken 370 388 404 412 420 Inventory Turnover (Days) 72.8 70.2 71.3 70.6 70.3 - Shrimp 64 80 100 105 111 A/P Turnover (Days) 22.4 22.0 21.0 21.3 21.2 Domestic Price Debt to Equity (Times) 1.1 1.1 0.8 0.6 0.5 - Pork 57.0 58.7 58.2 57.0 57.0 Net Debt to Equity (Times) 0.5 0.6 0.5 0.5 0.4 - Chicken 37.3 40.0 40.8 37.6 37.6 Gearing (Times) 0.4 0.4 0.3 0.3 0.2 - Shrimp 139.0 144.7 152.1 138.9 138.9 Interest Coverage (Times) 10.1 12.0 18.3 24.1 37.8 Avg. Exchange Rate (Bt : US$1) 34.2 31.8 29.5 29.5 29.5 Return on Avg. Assets (%) 9.3 11.2 12.3 13.7 15.8 Ending Exchange Rate (Bt : US$1) 32.8 31.5 31.5 29.5 29.5 Return on Avg. Equity (%) 21.4 24.7 25.2 25.0 26.0 8 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 9. Company Note – CPF Net profit PE Band Bt, m % Bt 25,000 250 60 200 50 20,000 150 40 15,000 100 30 10,000 50 20 0 5,000 10 (50) 0 0 (100) Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 2006 2007 2008 2009 2010 2011F 2012F Profit (Bt, m) Net Profit Growth (%) 2013F 20X 16X 12X 8X 4X Sources : Company data, TISCO Research Sources : Company data, TISCO Research ROAA, ROAE PBV Band % % Bt 18 30 70 15 25 60 50 12 20 40 9 15 30 6 10 20 3 5 10 0 0 0 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 2006 2007 2008 2009 2010 2011F 2012F 2013F ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. 3X ROAA (LHS) ROAE (RHS) 5X 4X 2X DownloadPDF. 1X Sources : Company data, TISCO Research Sources : Company data, TISCO Research Profit margin EV/EBITDA Band % % Bt 25 12 70 60 20 10 50 8 15 40 6 30 10 4 20 5 10 2 0 0 0 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 2006 2007 2008 2009 2010 2011F 2012F 2013F Gross Margin (LHS) Net Profit Margin (RHS) 15X 12X 9X 6X 3X Sources : Company data, TISCO Research Sources : Company data, TISCO Research 9 29 November 2011 Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.

- 10. Company Note – CPF TISCO Securities Company Limited www.tiscosec.com Bangkok 48/8 TISCO Tower 4th Floor, North Sathorn Road, Bangkok 10500, Thailand Tel : (66) 2633 6999 Fax : (66) 2633 6490, (66) 2633 6660 Esplanade Branch 99 Esplanade Shopping Center, Room 202-2, 2nd Floor, Ratchadapisek Road, Din Daeng, Bangkok 10400 Tel : (66) 2641 3251, (66) 2641 3252 Fax : (66) 2641 3253 Chiang Mai 275/4, 2nd Floor, Chang Phuak Road, Chang Phuak, Muang District, Chiang Mai 50300 Tel. 0 5322 4722 Fax. 0 5322 4711 Nakhon Pathom 386, 388 Petchkasem Road, Prapatone, Muang District, Nakhon Pathom 73000 Tel: 0 3421 1812 Fax: 0 3425 1676 Nakhon Ratchasima Tesco Lotus Korat, 719/5 Mittraphap Road, Naimuang, Muang District, Nakhon Ratchasima 30000 Tel: 0 4425 7752 Fax: 0 4425 3752 Udon Thani 227/21 2nd Floor, Udondussadee Road, Muang District, Udon Thani 41000 Tel: 0 4224 6888 Fax: 0 4224 5793 ISIEmergingMarketsPDF us-eyintranet from 123.30.70.126 on 2012-01-15 23:36:03 EST. DownloadPDF. Score Range Level Description 90 - 100 5 Excellent 80 - 89 4 Very Good 70 - 79 3 Good Corporate Governance Report 60 - 69 2 Satisfactory of Thai Listed Companies 2010 50 - 59 1 Pass < 50 or not rated n.a. n.a. Disclaimer The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of lthe Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information. (In order to recognize well performed companies, companies classified into the three highest score groups (Good, Very Good, and Excellent) will be announced to the public). The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. TISCO Securities Company Limited does not confirm nor certify the accuracy of such survey result. The information, statements, forecasts and projections contained herein, including any expression of opinion, are based upon sources believed to be reliable but their accuracy completeness or correctness are not guaranteed. Expressions of opinion herein were arrived at after due and careful consideration and they were based upon the best information then known to us, and in our opinion are fair and reasonable in the circumstances prevailing at the time. Expressions of opinion contained herein are subject to change without notice. This document is not, and should not be construed as, an offer or the solicitation of an offer to buy or sell any securities. TISCO and other companies in the TISCO Group and/or their officers, directors and employees may have positions and may affect transactions in securities of companies mentioned herein and may also perform or seek to perform investment banking services for these companies. No person is authorized to give any information or to make any representation not contained in this document and any information or representation not contained in this document must not be relied upon as having been authorized by or on behalf of TISCO. This document is for private circulation only and is not for publication in the press or elsewhere. TISCO accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or its content. The use of any information, statements forecasts and projections contained herein shall be at the sole discretion and risk of the user. Important Notice : This Document may only be issued or passed on to any person in the United Kingdom if that person is of a kind described in Article 11 of the Financial Services 1986 (Investment advertisements) Exemptions Order 1996 or otherwise pursuant to exemptions to Section 57 of the Financial Services Act 1986. In addition, no person who is an 10 Authorised Person may issue or pass on this Document, or otherwise promote the Company, to any person in the United Kingdom other than under the rules of self-regulatory organisations or the Financial Services Authority applicable to such Authorised Persons. This Document is confidential and is intended solely for the use of its recipient. Any 29 November 2011 duplication or redistribution of this Document is prohibited. Downloaded by us-eyintranet from 123.30.70.126 at 2012-01-15 23:36:03 EST. ISI Emerging Markets. Unauthorized Distribution Prohibited.