Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (19)

Destaque

Destaque (20)

Semelhante a Financial Armageddon

Semelhante a Financial Armageddon (11)

Último

Último (20)

Financial Armageddon

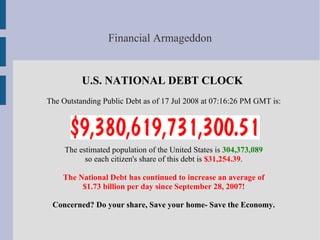

- 1. Financial Armageddon U.S. NATIONAL DEBT CLOCK The Outstanding Public Debt as of 17 Jul 2008 at 07:16:26 PM GMT is: The estimated population of the United States is 304,373,089 so each citizen's share of this debt is $31,254.39. The National Debt has continued to increase an average of $1.73 billion per day since September 28, 2007! Concerned? Do your share, Save your home- Save the Economy.

- 2. The Perfect Crime The biggest investment most Americans have is the target of one of the country's largest Financial Scams. When fully exposed, this will make Enron look like a parking ticket. When the property owner runs out of resources to fight back, their property is then stolen. Investigations verify this scheme is deliberate, and as one attorney put it: 'criminally brilliant'. This illegal business model disregards the law and even gets the legal system to help out.

- 3. Predatory Structured Finance This process, usually referred to as securitization, it can lower the cost of funds for lenders, allowing them to offer better prices. But, it can also capitalize fly-by-night companies that specialize in fraud, deceptive practices, abusive collections, and other predatory behavior. Some of the institutions that sponsor and administer securitization of mortgage backed securities are complicit in predatory lending. By encouraging, facilitating, and profiting from predatory loans, these financiers have themselves slipped into predation. In addition to transferring liability to the secondary market through assignment based rules (such as the Federal Trade Commission’s holder-notice rule or the Home Ownership and Equity Protection Act’s assignee liability provisions), courts and policy makers should explore common law imputed liability theories such as civil conspiracy, aiding and abetting, and joint venture. Unlike assignee liability rules, these older common law theories can reach architects of predatory structured finance that never actually own predatory loans themselves.

- 4. The mortgage transaction as many (most?) of us still understand it: Simple. Straightforward. Ancient history.

- 5. Borrowing Under a Securitization Structure

- 6. The securitization structure diagram shows the components of a typical securitization. It is important to note that not all securitizations are identical. Nevertheless, the diagram generally illustrates the roles of the various participants in a securitization structure. the key elements to a typical securitization include the following: Issuer - A bankruptcy-remote special purpose entity (SPE) formed to facilitate a securitization and to issue securities to investors. Lender - An entity that underwrites and funds loans that are eventually sold to the SPE for inclusion in the securitization. Lenders are compensated by cash for the purchase of the loan and by fees. In some cases, the lender might contract with mortgage brokers. Lenders can be banks or non-banks. Mortgage Broker - Acts as a facilitator between a borrower and the lender. The mortgage broker receives fee income upon the loan's closing. Servicer- The entity responsible for collecting loan payments from borrowers and for remitting these payments to the issuer for distribution to the investors. The servicer is typically compensated with fees based on the volume of loans serviced. The servicer is generally obligated to maximize the payments from the borrowers to the issuer, and is responsible for handling delinquent loans and foreclosures. Investors - The purchasers of the various securities issued by a securitization. Investors provide funding for the loans and assume varying degrees of credit risk, based on the terms of the securities they purchase. Rating Agency - Assigns initial ratings to the various securities issued by the issuer and updates these ratings based on subsequent performance and perceived risk. Rating agency criteria influence the initial structure of the securities. Trustee - A third party appointed to represent the investors' interests in a securitization. The trustee ensures that the securitization operates as set forth in the securitization documents, which may include determinations about the servicer's compliance with established servicing criteria. Underwriter - Administers the issuance of the securities to investors. Credit Enhancement Provider - Securitization transactions may include credit enhancement (designed to decrease the credit risk of the structure) provided by an independent third party in the form of letters of credit or guarantees.

- 7. The Fed, Hedge Fund Managers and Securitization...

- 8. The Deepening Vortex of Our Economy The Analytics of Loss Causation 1- A Material Misrepresentation or Omission- (e.g. Loan application fraud) 2- Scienter- a wrongful state of mind (e.g. Knowing and willful acts of fraud) 3- A connection with a purchase or sale of security (e.g. Mortgage backed security) 4- A reliance to the markets (e.g. Fraud on the Markets- Bear Stearns, Countrywide) 5- Economic Loss- (e.g. Present financial condition of the United States) 6- Loss Causation- ( e.g. Casual connection between the material misrepresentation and the Loss)

- 9. From the transcript of evidentiary hearing - MERS v. Cabrera: quot;It truly concerns me, however, that thousands and thousands of mortgage foreclosure actions have been filed with these allegations. I am not certain what remedy, if any, these people would have were it to be determined that MERS was not ever the proper party notwithstanding that these folks [might] have been in default what their recourse, if any, would be. I'm not certain with the satisfaction of mortgages that have been filed on behalf of MERS how good those are and I am not certain how good title to property is that people bought at these foreclosure sales if it turns or becomes established that MERS was indeed not only not the right party but misrepresented by way of their pleadings and affidavits that they held something they didn't own, so I'm not certain of the consequences but it seems vast.quot; - The Honorable Judge Jon Gordon

- 10. Fight For Fairness This process is not intended to help you get your house for free. The primary goal is to delay the foreclosure and put pressure on the lender to negotiate. Despite all the hype about lenders wanting to help homeowners avoid foreclosure, most borrowers know that’s not the reality. Too many homeowners have experienced lender resistance to their efforts to work out a payment structure to keep them in their homes. Many lenders bear responsibility for these defaults, because they put borrowers into unfair loans using deceptive, hard-sell practices and then made the problem worse with predatory servicing. Most homeowners just want these lenders to give them reasonable terms on their mortgages, many of which were predatory to begin with. With the help of judges who see through these predatory practices, lenders will feel the pressure to work with borrowers to keep them in their homes. Don’t forget lenders made incredible amounts of money by using irresponsible practices to issue and service these loans. That greed led to the foreclosure crisis we’re in today. Allowing lenders to continue foreclosing on home after home, destroying our neighborhoods and our economy hurts us all. So, make it hard for your lender to take your home. Validate your debt, Fight Back!!! Step 1- Make them produce the note. http://youtube.com/watch?v=LqAWCgKuvZ0 http://youtube.com/watch?v=G9GMLVG7mN0&feature=related http://youtube.com/watch?v=0YNyn1XGyWg

- 11. Save your home- Save the Economy The complexities of of mortgage loan securitization cast a shadow of doubt on who has the legal right to foreclose. Under the act, evidence of predatory lending may present a stout defense against foreclosure, as as can any number of mistakes or omissions of a technical nature. If a tiny error made (even innocently) by the lender may be grounds to stop foreclosure, would knowing , willful and malicious acts of material misrepresentation, be also substantiative grounds as well?

- 12. End Part 5 brought to you in part by: Avenue S Mortgage Auditing Change we can believe in