3. Three key assumptions 1. The technology is ready (or close), robust and reliable 2. The cost of the system is significantly less than the cost of labor being replaced (i.e., ROI within 6-12 months). 3. There are no legal constraints regarding autonomous mowers

8. Total Market – Mowing Golf Courses About 30,000 golf courses in key markets* Estimated market = $190 million Sport Fields (Soccer, Football, Baseball) Municipal Parks Highways/ Waterways Total Market = $473 million *.: Key markets: USA, Germany, UK, France, Italy, Japan About 55,000 fields in key markets* Estimated market = $110 million About 135k acres of municipal parks in key markets* Estimated market = $135 million About 6.3 million miles of paved roads in key markets* Estimated market = $38 million Preliminary numbers

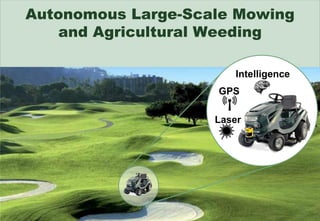

10. This week’s learnings Interviews Unique industry. It will be hard to get large volume of interviews but experts are available and helpful. Industry Partners Determining the method to partner with industry leaders will be a key element for success. Technology For mowing, all technology is available. Business model must be developed. For weeding, technology is close, but still needs work. Risk is higher with weeding, but a large market available.

![Autonomous Mowing and Weeding Systems ,[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object],[object Object]](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)