GHP Houston: The Economy at a Glance

•

1 like•771 views

The Greater Houston Partnership has published "The Economy at a Glance" for September 2010.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Similar to GHP Houston: The Economy at a Glance

Similar to GHP Houston: The Economy at a Glance (20)

More from Bob Lowery

More from Bob Lowery (20)

Recently uploaded

Recently uploaded (20)

GHP Houston: The Economy at a Glance

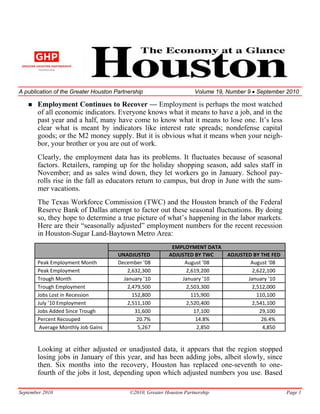

- 1. A publication of the Greater Houston Partnership Volume 19, Number 9 • September 2010 Employment Continues to Recover — Employment is perhaps the most watched of all economic indicators. Everyone knows what it means to have a job, and in the past year and a half, many have come to know what it means to lose one. It’s less clear what is meant by indicators like interest rate spreads; nondefense capital goods; or the M2 money supply. But it is obvious what it means when your neigh- bor, your brother or you are out of work. Clearly, the employment data has its problems. It fluctuates because of seasonal factors. Retailers, ramping up for the holiday shopping season, add sales staff in November; and as sales wind down, they let workers go in January. School pay- rolls rise in the fall as educators return to campus, but drop in June with the sum- mer vacations. The Texas Workforce Commission (TWC) and the Houston branch of the Federal Reserve Bank of Dallas attempt to factor out these seasonal fluctuations. By doing so, they hope to determine a true picture of what’s happening in the labor markets. Here are their “seasonally adjusted” employment numbers for the recent recession in Houston-Sugar Land-Baytown Metro Area: EMPLOYMENT DATA UNADJUSTED ADJUSTED BY TWC ADJUSTED BY THE FED Peak Employment Month December ’08 August ’08 August ’08 Peak Employment 2,632,300 2,619,200 2,622,100 Trough Month January ’10 January ’10 January ’10 Trough Employment 2,479,500 2,503,300 2,512,000 Jobs Lost in Recession 152,800 115,900 110,100 July ’10 Employment 2,511,100 2,520,400 2,541,100 Jobs Added Since Trough 31,600 17,100 29,100 Percent Recouped 20.7% 14.8% 26.4% Average Monthly Job Gains 5,267 2,850 4,850 Looking at either adjusted or unadjusted data, it appears that the region stopped losing jobs in January of this year, and has been adding jobs, albeit slowly, since then. Six months into the recovery, Houston has replaced one-seventh to one- fourth of the jobs it lost, depending upon which adjusted numbers you use. Based September 2010 ©2010, Greater Houston Partnership Page 1

- 2. HOUSTON—THE ECONOMY AT A GLANCE on rate of job creation over the past half year, Houston could recover all the jobs lost in the recession in another 18 to 36 months. Please note, this is a “back of the envelope” calculation, and full recovery could occur sooner or later, depending on such factors as the lifting of the drilling moratorium, the imposition of carbon cap and trade regulations, extension of the Bush era tax cuts, the performance of the stock market, improvements in the commercial real estate market, and budget aus- terity in Austin and Washington. Traditionally, GHP has monitored the number of jobs Houston has gained or lost over a 12-month period. That has been our way of handling the seasonality of the data. The Texas Workforce Commission reports that the 12-month job loss in the Houston metro fell to 9,700 jobs, or 0.4 percent, from July ’09 to July ’10. That is a considerable improvement over the 80,800 job loss (3.1 percent), reported for the 12 months ending July ’09. During the recession, the worst period was for the 12 months ending November ’09, when the region shed 103,800 jobs. Over the past six months, the 12-month job losses have declined consistently; and if the trend continues, Houston’s 12-month job change should turn positive in the next month or two. TWC and the Fed calculate seasonal adjustments only for total employment. Looking back at the unadjusted estimates of employment by industry during the recession, a few trends stand out. • Since August ’08, when private sector employment began to decline, the oil and gas industry has added 3,200 jobs. The oilfield services sector has added jobs every month since April ’10. To date, the offshore drilling moratorium isn’t showing up in the employment numbers. • Employment in health care and social assistance has continued to grow, add- ing 18,200 jobs during the recession. Though recent health care legislation may complicate the delivery and payment for services, it won’t stifle the need for health care. Two demographic trends, an aging population and a rapidly growing population, will continue to fuel the demand for health care workers in Houston. • Houston’s manufacturing sector is slowly recovering. Employment peaked at 245,100 jobs in December ’08, declined for 14 consecutive months, and is trending up, adding 4,000 jobs since the first of the year. The 12-month job loss has declined from 27,000 in January ’10 to 1,100 in July ’10. To summarize, the job market shows some signs of recovery, but it still has quite a way to go before reaching the previous peak. Houston to Lead in Population Growth — The Houston–Sugar Land–Baytown Metro Area will lead the state in population growth, adding 3.53 million residents, September 2010 ©2010, Greater Houston Partnership Page 2

- 3. HOUSTON—THE ECONOMY AT A GLANCE between ’09 and ’35, according to a forecast recently released by The Perryman Group. That reflects a 1.84 percent annual growth rate. Dallas-Plano ranks second in projected population growth, adding 2.61 million residents during the same period, a 1.84 percent compound annual growth rate, and Austin ranks third, add- ing 500,072 residents, a 2.65 percent compound annual growth rate. Perryman also forecasts that Houston will add an additional 1.325 million jobs and account for almost one-fourth of Texas job growth during that time frame. That reflects a 1.57 percent annual growth rate. Real gross product, the final value of all goods and services produced in Houston adjusted for inflation, will grow from $284.5 billion in ’09 to $747.3 billion in 2035. That reflects a 3.78 percent compound annual growth rate. The forecast is in 2000 constant dollars. “The long-term forecast for the state is positive and a return to steady, healthy growth is anticipated,” the report states. International Passenger Travel Increases — The Houston Airport System served 4.74 million passengers in July ’10, bringing its 12-month total to 49.0 mil- lion passengers. This is 6.7 percent less than the record 52.3 million passengers served during the 12 months ending July ’08. Although most passengers are traveling domestically, the majority of growth oc- curred in international travel. The first seven months of the year saw a 4.4 percent increase in international passengers, while domestic travel only rose 0.1 percent. The greatest rise in passenger volume occurred in travel to Canada (22.4 percent), Europe (12.4 percent) and the Middle East (11.6 percent increase). Dubai-based Emirates recently announced plans to add a second daily nonstop flight from Houston Intercontinental to the U.A.E. to handle growing demand for service to the Middle East. “So far this year, each and every month has produced an increase in the number of international passengers,” said Director, Air Service Development, Genaro Peña. “The additional passengers and new nonstop flights have combined to create very positive momentum for HAS in 2010.” Air freight volumes also continue to grow. HAS handled 76.7 million pounds of air freight in July ’10, up 16.7 percent from July ’09. Year-to-date, HAS handled 507.8 million pounds of air freight, up 17.6 percent compared to the same seven months last year. International Trade Posts Gains — Through the first six months of ’10, the Houston-Galveston Customs District handled $100.9 billion in trade, up 31.6 percent from $76.7 billion the first six months of ’09. Exports totaled $44.4 billion, September 2010 ©2010, Greater Houston Partnership Page 3

- 4. HOUSTON—THE ECONOMY AT A GLANCE up 27.7 percent from ’09; and imports totaled $56.5 billion, up 34.8 percent from the same period last year. Five commodities accounted for 73.6 percent of all exports through Houston in the first half of this year: mineral fuel and oil ($12.4 billion), industrial machinery ($8.2 billion) organic chemicals ($6.6 billion), plastics ($3.4 billion) and electric machinery ($2.2 billion). Five commodities accounted for 71.2 percent of all imports handled by the Houston-Galveston customs district: crude oil ($33.0 billion), non-crude oil ($4.1 billion), parts and accessories for ADP machines ($1.4 billion), light oils ($1.0 billion) and casing and tubing ($574.6 million). Houston’s top 20 trade partners accounted for 71.7 percent of the region’s total trade. All but three are showing increases in trade during the first six months of ’10 compared to the same period last year. HOUSTON GALVESTON CUSTOMS DISTRICT TRADE SUMMARY COMBINED IMPORTS + EXPORTS ($ Millions) JUN ’10 YTD JUN ’09 YTD Change ’09 – ’10 Mexico 10,348.2 6,432.7 3,915.4 Venezuela 7,959.8 4,980.3 2,979.4 Nigeria 6,368.4 3,682.5 2,685.9 Brazil 5,062.7 3,654.6 1,408.1 Russia 4,103.9 2,992.7 1,111.2 Saudi Arabia 4,048.4 2,677.0 1,371.4 China 3,865.1 5,141.2 ‐1,27611 Colombia 3,666.0 1,984.5 1,681.5 Germany 3,182.0 3,053.0 129.0 United Kingdom 2,995.7 3,090.5 ‐94.7 Algeria 2,866.1 1,786.6 1,079.5 Netherlands 2,702.9 2,810.4 ‐107.4 Singapore 2,363.3 1,338.5 1,024.7 Korea, Republic Of 2,348.8 1,738.4 610.4 Costa Rica 2,069.9 625.2 1,444.8 Belgium 2,037.7 1,364.5 673.1 Chile 1,770.9 1,245.9 524.9 Japan 1,643.6 1,441.3 202.3 India 1,585.1 1,421.3 163.8 Iraq 1,389.2 1,221.5 167.7 All Other Countries 28,554.7 24,026.0 4,528.7 Houston Total $100,932.4 $76,708.6 $24,223.8 Source: U.S. Census Bureau September 2010 ©2010, Greater Houston Partnership Page 4

- 5. HOUSTON—THE ECONOMY AT A GLANCE New Home Sales Fall — Net sales of new single-family homes fell to 888 transactions in July ’10, a 35 percent decline compared to July ’09, according to Metrostudy’s July Monthly Sales and Traffic Report. Though July sales were down compared to a year ago, they were actually up 11 percent compared to June ’10. Over the first five months of ’10, new home sales grew as consumers accelerated their purchase decisions to take advantage of the new homebuyer tax credit. Once the new homebuyer’s tax credit expired, new home purchases dropped significantly. In the wake of weak demand, builders continue to carefully manage their inventories. The number of spec units under construction saw no growth compared to July ’09 and remained at 1,825. Finished spec inventory rose to 1,371, a 19.4 percent increase from July ’09. Metrostudy estimates that single-family starts in the Houston area will total 18,000 in ’10 and 20,000-21,000 in ’11. Houston’s Cost of Living Remains Below National Average — In Q2/10, the cost of living in Houston was 19 percent below the average for 27 metropolitan areas over 2 million population and 10 percent below the average for all 314 reporting places, according to the ACCRA Cost of Living Index. The index, pro- duced by the Council for Community and Economic Research, measures differences in the relative cost of consumer goods and services appropriate for a professional or managerial household in the top income quintile. Houston’s low cost of living is mostly because of its bargain housing prices. In Q2/10, housing costs in Houston were 39 percent below the major metro average and 22 percent below the average of all reporting places. According to the ACCRA survey, the same new house that cost $211,432 in Houston in July cost $322,968 in Miami, $471,000 in Boston and $609,952 in Washington, D.C. The cost of grocery items in Houston was the lowest among the major metro areas, 16 percent below the major metro average and 12 percent below the national aver- age. Houston did not differ significantly from the nationwide average on the other components: utilities, transportation, health care, and miscellaneous goods and services. ____________________________________ The Greater Houston Partnership is the primary advocate of Houston’s business community and is dedicated to building regional economic prosperity. Visit the Greater Houston Partnership on the World Wide Web at www.houston.org. Contact us by phone at 713-844-3600. September 2010 ©2010, Greater Houston Partnership Page 5

- 6. HOUSTON—THE ECONOMY AT A GLANCE Houston Economic Indicators YEAR-TO-DATE A Service of the Greater Houston Partnership MONTHLY DATA TOTAL OR AVERAGE* Most Year % Most Year % Month Recent Earlier Change Recent Earlier Change ENERGY U.S. Active Rotary Rigs July '10 1,573 931 69.0 1,453 * 1,088 * 33.5 Spot Crude Oil Price ($/bbl, West Texas Intermediate) July '10 76.32 65.29 16.9 77.65 * 54.20 * 43.3 Spot Natural Gas ($/MMBtu, Henry Hub) July '10 4.82 3.72 29.6 4.66 * 3.92 * 18.9 UTILITIES AND PRODUCTION Houston Purchasing Managers Index July '10 52.4 43.8 19.6 55.7 * 43.1 * 29.2 Nonresidential Electric Current Sales (Mwh, CNP Service Area) July '10 4,663,282 4,682,892 -0.4 28,543,283 28,100,130 1.6 CONSTRUCTION Total Building Contracts ($, Houston MSA) July '10 693,601,000 909,986,000 -23.8 5,162,277,000 5,329,382,000 -3.1 Nonresidential July '10 236,703,000 351,361,000 -32.6 1,947,737,000 2,420,516,000 -19.5 Residential July '10 456,898,000 558,625,000 -18.2 3,214,540,000 2,908,866,000 10.5 Building Permits ($, City of Houston) July '10 264,381,291 391,776,848 -32.5 1,915,292,501 2,441,359,244 -21.5 Nonresidential July '10 200,339,600 291,032,204 -31.2 1,276,957,838 1,891,272,020 -32.5 New Nonresidential July '10 80,418,076 206,294,123 -61.0 429,393,202 779,950,337 -44.9 Nonresidential Additions/Alterations/Conversions July '10 119,921,524 84,738,081 41.5 847,564,636 1,111,321,683 -23.7 Residential July '10 64,041,691 100,744,644 -36.4 638,334,663 550,087,224 16.0 New Residential July '10 48,077,428 72,165,892 -33.4 488,185,903 402,091,142 21.4 Residential Additions/Alterations/Conversions July '10 15,964,263 28,578,752 -44.1 150,148,760 147,996,082 1.5 Multiple Listing Service (MLS) Activity Closings July '10 5,056 6,686 -24.4 37,158 35,796 3.8 Median Sales Price - SF Detached July '10 160,880 162,000 -0.7 153,516 * 149,307 * 2.8 Active Listings July '10 55,247 46,598 18.6 50,019 * 45,404 * 10.2 EMPLOYMENT (Houston-Sugar Land-Baytown MSA) Nonfarm Payroll Employment July '10 2,511,100 2,528,100 -0.7 2,511,800 * 2,579,000 * -2.6 Goods Producing (Natural Resources/Mining/Const/Mfg) July '10 478,500 477,100 0.3 477,500 * 522,200 * -8.6 Service Providing July '10 2,032,600 2,051,000 -0.9 2,034,300 * 2,056,800 * -1.1 Unemployment Rate (%) - Not Seasonally Adjusted Houston-Sugar Land-Baytown MSA July '10 8.8 8.3 8.5 * 6.4 * Texas July '10 8.5 8.3 8.2 * 6.5 * U.S. July '10 9.7 9.7 9.8 * 7.9 * Unemployment Insurance Claims (Gulf Coast WDA) Initial Claims July '10 23,437 27,221 -13.9 22,590 * 27,016 * -16.4 Continuing Claims July '10 103,648 148,447 -30.2 108,766 * 129,603 * -16.1 TRANSPORTATION Port of Houston Authority Shipments (Short Tons) July '10 3,448,962 2,886,101 19.5 19,123,164 18,249,204 4.8 Air Passengers (Houston Airport System) July '10 4,738,759 4,723,973 0.3 28,881,175 28,386,331 1.7 Domestic Passengers July '10 3,848,421 3,906,014 -1.5 23,847,415 23,753,489 0.4 International Passengers July '10 890,338 817,959 8.8 5,033,760 4,632,842 8.7 Landings and Takeoffs July '10 74,044 79,986 -7.4 496,032 518,460 -4.3 Air Freight (000 lb) July '10 76,734 65,753 16.7 507,805 431,698 17.6 Enplaned July '10 40,412 35,105 15.1 266,859 231,527 15.3 Deplaned July '10 36,322 30,648 18.5 240,946 200,171 20.4 CONSUMERS New Car and Truck Sales (Units, Houston MSA) July '10 17,810 17,226 3.4 139,819 120,741 15.8 Cars July '10 7,826 7,750 1.0 63,639 54,663 16.4 Trucks, SUVs and Commercials July '10 9,984 9,476 5.4 76,180 66,078 15.3 Total Retail Sales ($000,000, Houston MSA, NAICS Basis) 3Q09 18,738 20,136 -6.9 53,679 59,150 -9.3 Consumer Price Index for All Urban Consumers ('82-'84=100) Houston-Galveston-Brazoria CMSA July '10 194.734 192.325 1.3 192.468 * 190.017 * 1.3 United States July '10 218.011 215.351 1.2 217.603 * 213.455 * 1.9 Hotel Performance (Harris County) Occupancy (%) 1Q10 56.8 62.8 56.8 * 62.8 * Average Room Rate ($) 1Q10 93.91 102.21 -8.1 93.91 * 102.21 * -8.1 Revenue Per Available Room ($) 1Q10 53.31 64.18 -16.9 53.31 * 64.18 * -16.9 POSTINGS AND FORECLOSURES Postings (Harris County) Aug '10 3,372 3,337 1.0 30,346 25,662 18.3 Foreclosures (Harris County) Aug '10 1,059 824 28.5 8,898 7,134 24.7 September 2010 ©2010, Greater Houston Partnership Page 6

- 7. HOUSTON—THE ECONOMY AT A GLANCE Sources Rig Count Baker Hughes Incorporated Port Shipments Port of Houston Authority Spot WTI, Spot Natural Gas U.S. Energy Information Agency Aviation Aviation Department, City of Houston Purchasing Managers National Association of Houston Index Purchasing Management – Car and Truck Sales TexAuto Facts Report, InfoNation, Houston, Inc. Inc., Sugar Land TX Electricity CenterPoint Energy Retail Sales Texas Comptroller’s Office Building Construction Contracts McGraw-Hill Construction Consumer Price Index U.S. Bureau of Labor Statistics City of Houston Building Permits Building Permit Department, City Hotels PKF Consulting/Hospitality Asset of Houston Advisors International MLS Data Houston Association of Realtors® Postings, Foreclosures Foreclosure Information & Listing Employment, Unemployment Texas Workforce Commission Service STAY UP TO DATE! If you would like to receive this electronic publication on the first working day of each month, please e- mail your request for Economy at a Glance to rpate@houston.org. Include your name, title and phone number and your company’s name and address. Archived copies are available to Partnership Members in the Members Only section at www.houston.org. For information about joining the Greater Houston Partnership and gaining access to this powerful resource, call Member Services at 713-844-3683. The foregoing table is updated whenever any data change — typically, 11 or so times per month. If you would like to receive those updates by e-mail, usually accompanied by commentary, please e-mail your request for Key Economic Indicators to rpate@houston.org with the same identifying information. You may request Glance and Indicators in the same e-mail. September 2010 ©2010, Greater Houston Partnership Page 7

- 8. HOUSTON—THE ECONOMY AT A GLANCE HOUSTON MSA NONFARM PAYROLL EMPLOYMENT (000) Change from % Change from July ' 10 Jun ' 10 July '09 Jun '10 July '09 Jun '10 July '09 Total Nonfarm Payroll Jobs 2,511.1 2,528.1 2,520.8 -17.0 -9.7 -0.7 -0.4 Total Private 2,150.2 2,150.6 2,167.4 -0.4 -17.2 0.0 -0.8 Goods Producing 478.5 477.1 492.0 1.4 -13.5 0.3 -2.7 Service Providing 2,032.6 2,051.0 2,028.8 -18.4 3.8 -0.9 0.2 Private Service Providing 1,671.7 1,673.5 1,675.4 -1.8 -3.7 -0.1 -0.2 Mining and Logging 90.0 89.2 87.7 0.8 2.3 0.9 2.6 Oil & Gas Extraction 51.1 50.9 49.2 0.2 1.9 0.4 3.9 Support Activities for Mining 37.7 37.2 37.5 0.5 0.2 1.3 0.5 Construction 167.5 167.8 182.2 -0.3 -14.7 -0.2 -8.1 Manufacturing 221.0 220.1 222.1 0.9 -1.1 0.4 -0.5 Durable Goods Manufacturing 141.3 140.7 141.2 0.6 0.1 0.4 0.1 Nondurable Goods Manufacturing 79.7 79.4 80.9 0.3 -1.2 0.4 -1.5 Wholesale Trade 127.9 128.0 130.5 -0.1 -2.6 -0.1 -2.0 Retail Trade 260.6 260.5 261.6 0.1 -1.0 0.0 -0.4 Transportation, Warehousing and Utilities 120.3 119.9 122.6 0.4 -2.3 0.3 -1.9 Utilities 16.6 16.6 16.7 0.0 -0.1 0.0 -0.6 Air Transportation 23.9 23.9 24.6 0.0 -0.7 0.0 -2.8 Truck Transportation 18.6 18.6 18.7 0.0 -0.1 0.0 -0.5 Pipeline Transportation 9.0 8.9 8.8 0.1 0.2 1.1 2.3 Balance, incl Warehousing, Water & Rail Transport 52.2 51.9 53.8 0.3 -1.6 0.6 -3.0 Information 32.6 32.8 34.5 -0.2 -1.9 -0.6 -5.5 Telecommunications 17.3 17.5 17.9 -0.2 -0.6 -1.1 -3.4 Finance & Insurance 86.4 86.4 88.5 0.0 -2.1 0.0 -2.4 Real Estate & Rental and Leasing 51.1 51.3 51.1 -0.2 0.0 -0.4 0.0 Professional & Business Services 352.2 352.0 356.7 0.2 -4.5 0.1 -1.3 Professional, Scientific & Technical Services 169.9 169.5 173.8 0.4 -3.9 0.2 -2.2 Legal Services 23.2 23.2 23.5 0.0 -0.3 0.0 -1.3 Accounting, Tax Preparation, Bookkeeping 15.6 15.6 16.7 0.0 -1.1 0.0 -6.6 Architectural, Engineering & Related Services 60.8 60.2 60.8 0.6 0.0 1.0 0.0 Computer Systems Design & Related Services 23.4 23.6 24.1 -0.2 -0.7 -0.8 -2.9 Admin & Support/Waste Mgt & Remediation 161.9 162.3 163.7 -0.4 -1.8 -0.2 -1.1 Administrative & Support Services 154.3 154.6 155.3 -0.3 -1.0 -0.2 -0.6 Employment Services 51.2 51.3 52.8 -0.1 -1.6 -0.2 -3.0 Educational Services 41.4 42.4 40.7 -1.0 0.7 -2.4 1.7 Health Care & Social Assistance 264.9 264.2 256.0 0.7 8.9 0.3 3.5 Arts, Entertainment & Recreation 31.0 31.3 31.0 -0.3 0.0 -1.0 0.0 Accommodation & Food Services 210.0 210.9 208.8 -0.9 1.2 -0.4 0.6 Other Services 93.3 93.8 93.4 -0.5 -0.1 -0.5 -0.1 Government 360.9 377.5 353.4 -16.6 7.5 -4.4 2.1 Federal Government 32.0 35.5 29.2 -3.5 2.8 -9.9 9.6 State Government 69.2 69.3 68.6 -0.1 0.6 -0.1 0.9 State Government Educational Services 36.1 36.1 35.1 0.0 1.0 0.0 2.8 Local Government 259.7 272.7 255.6 -13.0 4.1 -4.8 1.6 Local Government Educational Services 171.6 184.6 169.3 -13.0 2.3 -7.0 1.4 SOURCE: Texas Workforce Commission September 2010 ©2010, Greater Houston Partnership Page 8

- 9. HOUSTON—THE ECONOMY AT A GLANCE Population and Employment Houston-Sugar Land-Baytown MSA 2005-2035 10 9 8 7 6 000,000 5 4 3 2 1 0 '05 '10 '15 '20 '25 '30 '35 Population Pop Forecast Employment Empl Forecast Source: The Perryman Group, Spring/Summer 2010 HOUSTON MSA EMPLOYMENT 2001-2011 2.65 160 2.60 140 2.55 120 NONFARM PAYROLL EMPLOYMENT (000,000) 2.50 100 2.45 80 12-MONTH CHANGE (000) 2.40 60 2.35 40 2.30 20 2.25 0 2.20 -20 2.15 -40 2.10 -60 2.05 -80 2.00 -100 1.95 -120 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 12-MONTH CHANGE JOBS Source: Texas Workforce Commission September 2010 ©2010, Greater Houston Partnership Page 9

- 10. HOUSTON—THE ECONOMY AT A GLANCE GOODS-PRODUCING AND SERVICE-PROVIDING EMPLOYMENT HOUSTON MSA 2001-2011 550 2.25 540 2.20 530 2.15 2.10 520 SERVICE-PROVIDING (000,000) 2.05 GOODS-PRODUCING (000) 510 2.00 500 1.95 490 1.90 480 1.85 470 1.80 460 1.75 450 1.70 440 1.65 430 1.60 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 GOODS-PRODUCING JOBS SERVICE-PROVIDING JOBS Source: Texas Workforce Commission UNEMPLOYMENT RATE HOUSTON & U.S. 2001-2011 11 10 9 8 PERCENT OF LABOR FORCE 7 6 5 4 3 2 1 0 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-09 Jan-11 HOUSTON U.S. Source: Texas Workforce Commission September 2010 ©2010, Greater Houston Partnership Page 10

- 11. HOUSTON—THE ECONOMY AT A GLANCE SPOT MARKET ENERGY PRICES 2001 - 2011 140 28 120 24 HENRY HUB NATURAL GAS ($/MMBTU) WEST TEXAS INTERMEDIATE ($/BBL) 100 20 80 16 60 12 40 8 20 4 0 0 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 WTI MONTHLY WTI 12-MO AVG GAS MONTHLY GAS 12-MO AVG Source: U.S. Energy Information Administration INFLATION: 12-MONTH CHANGE 2001-2011 6% 5% 4% 3% 2% 1% 0% -1% -2% -3% Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 HOUSTON CPI-U U.S. CPI-U Source: U.S. Bureau of Labor Statistics September 2010 ©2010, Greater Houston Partnership Page 11