Dynamics of the GTA Condo Market

•

2 gostaram•1,239 visualizações

This document summarizes a presentation by N. Barry Lyon and Jasmine Cracknell to the Toronto Condo Network on March 2nd, 2012 about the dynamics of the Greater Toronto Area condo apartment market. It includes statistics on the number of high-rise buildings and units completed since 2000, yearly new sales and resales from 2002 to 2012, sales by unit type in 2005 and 2012, and average unit sizes from 2004 to 2012. It also discusses new downtown developments in 905 municipalities, planned new office buildings and parks in downtown Toronto, transit solutions, and the future role of investors in the condo market.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (15)

Semelhante a Dynamics of the GTA Condo Market

Semelhante a Dynamics of the GTA Condo Market (20)

Mais de Richard Silver, Certified International REALTOR®

Mais de Richard Silver, Certified International REALTOR® (20)

Último

Último (20)

Dynamics of the GTA Condo Market

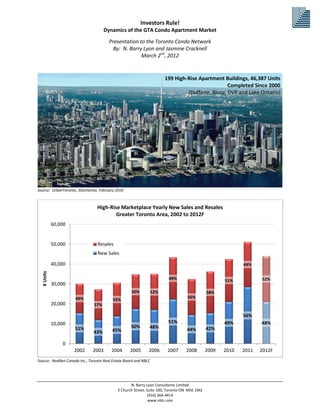

- 1. Investors Rule! Dynamics of the GTA Condo Apartment Market Presentation to the Toronto Condo Network By: N. Barry Lyon and Jasmine Cracknell March 2nd, 2012 199 High-Rise Apartment Buildings, 46,387 Units Completed Since 2000 (Dufferin, Bloor, DVP and Lake Ontario) Source: UrbanToronto, 3Dementia, February 2010 High-Rise Marketplace Yearly New Sales and Resales Greater Toronto Area, 2002 to 2012F 60,000 50,000 Resales New Sales 40,000 44% # Units 49% 51% 52% 30,000 50% 52% 58% 49% 56% 55% 20,000 57% 56% 10,000 51% 49% 48% 51% 50% 48% 42% 43% 45% 44% 0 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012F Source: RealNet Canada Inc., Toronto Real Estate Board and NBLC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 2. New High-Rise Sales 905 vs 416 Greater Toronto Area, 2006 to 2011 25,000 20,000 2005 2006 Total Sales (# Units) 2007 15,000 2008 2009 10,000 2010 2011 5,000 0 905 416 Source: RealNet Canada Inc. and NBLC New High-Rise Sales By Former 416 Municipalities, 2006 to 2011 14000 12000 2005 10000 2006 Total Sales (# Units) 2007 8000 2008 2009 6000 2010 4000 2011 2000 0 Etobicoke North York Scarborough Toronto Source: RealNet Canada Inc. and NBLC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 3. New High-Rise Sales By 905 Municipalities, 2006 to 2011 3,000 2,500 2005 2006 2,000 2007 Total Sales (# Units) 2008 1,500 2009 2010 1,000 2011 500 0 Source: RealNet Canada Inc. and NBLC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 4. N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 5. New High-Rise Sales By Unit Type Greater Toronto Area, 2005 Penthouse Other 3-Bed & Up 3% 2% 2% Studio 4% 1-Bed 2-Bed+Den 20% 20% 2-Bed 1-Bed+Den 21% 28% Source: RealNet Canada Inc. and NBLC New High-Rise Sales By Unit Type Greater Toronto Area, January 2012 Penthouse Other 3-Bed & Up 2% Studio 3% 2% 2% 2-Bed+Den 1-Bed 12% 21% 2-Bed 24% 1-Bed+Den 34% Source: RealNet Canada Inc. and NBLC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 6. Monthly High-Rise New Sales and Resales and Average Pricing Greater Toronto Area, 2006 to 2012 4000 $500,000 New Sales Resales New Price Resale Price $450,000 3500 $400,000 3000 $350,000 Average Sale Price Number of Sales 2500 $300,000 2000 $250,000 $200,000 1500 $150,000 1000 $100,000 500 $50,000 0 $0 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Source: RealNet Canada Inc., Toronto Real Estate Board and NBLC Source: NBLC, RealNet Canada Inc. and RBC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 7. New High-Rise Unsold Inventory and Site Count Greater Toronto Area, 2005 to 2012 25,000 450 High Rise Inventory 400 High Rise Site Count 20,000 350 Unsold Inventory (# of Units) # of Active High-Rise Site 300 15,000 250 200 10,000 150 5,000 100 50 0 0 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Apr-05 Jul-05 Apr-06 Jul-06 Apr-07 Jul-07 Apr-08 Jul-08 Apr-09 Jul-09 Apr-10 Jul-10 Apr-11 Jul-11 Source: RealNet Canada Inc. and NBLC New High-Rise Occupancies Greater Toronto Area, 2000 to 2016F 2016F 2,303 2015F 7,576 2014F 21,608 2013F 25,454 2012F 24,938 2011 14,102 2010 15,788 2009 11,783 2008 12,942 2007 15,407 2006 14,608 2005 15,046 2004 10,066 2003 12,279 2002 9,832 2001 3,906 2000 8,534 0 5,000 10,000 15,000 20,000 25,000 30,000 Total Units Source: RealNet Canada Inc. and NBLC N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 8. New High-Rise Average Unit Size (sq. ft.) Greater Toronto Area, 2004 to 2012 940 920 900 Average Unit Size (sq. ft.) 880 860 840 820 800 780 760 740 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Source: RealNet Canada Inc. and NBLC Opera – 741 square foot Three-Bedroom Unit at Peter Street Condos Source: Site Marketing Materials N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 9. 905’s New Downtowns N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 10. 905’s New Downtowns Mississauga Vaughan N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 11. 905’s New Downtowns Richmond Hill N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 12. Changing Dynamic of Downtown Toronto Planned New Downtown Toronto Office Buildings Source: BMO Capital Markets 10 York Waterfront Parks Coming Along Underpass Park – Waterfront Toronto ] N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 13. Changing Dynamic of Downtown Toronto Underpass Park, Waterfront Toronto Pan Am Athlete’s Village: 2015 View East from Front and Cherry N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 14. Transit Solutions Union Station Redevelopment Doubling Capacity Where Should Transit Go? Downtown Relief Line? N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 15. The Big Unknown – Future Role of Investors N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com

- 16. Investor Driven Condo Launch Format STAGES DESCRIPTION 1 First round of selling, lowest possible pricing. Investors purchase with a “Platinum Agent”. A Platinum Agent is a high-volume broker or sales representative who has the best relationships with condo developers. PLATINUM AGENTS Platinum Agents typically sell 10 or more units in a project (sometimes as much as 50 units). These units are usually ‘allocated’ in advance. Typically 10-15 Platinum Agents in a given project. 2 VIP AGENTS A VIP Agent is a broker or sales representative that has sold a unit or multiple units for the specific developer in the past. A typical project launch will have anywhere from 50-300 VIP agents. These agents will NOT have units allocated to them in advance. 3 Once the VIP stage is over, the developer will open its doors to all brokers and sales representatives. Again, prices are typically raised for this new GENERAL AGENTS phase of selling. Individual investors and buyers, however, are still not permitted to walk in and purchase without the representation of a broker or agent. 4 At the start of sales, the developer will typically launch a website for the project (i.e. ABCcondos.com). The website will provide very limited details, PRE-REGISTRATION and include a ‘registration form’ for individual investors and buyers. It is usually during this phase where individuals are asked to come in and purchase providing them priority over the general public. 5 PUBLIC GRAND OPENING By this phase, the developer will have started their major ad campaign, creating awareness for the project to the general public. This is often accompanied by a ‘Grand Opening’ event, where the public is invited to come in and purchase. N. Barry Lyon Consultants Limited 3 Church Street, Suite 100, Toronto ON M5E 1M2 (416) 364-4414 www.nblc.com