Event-Driven Architecture Masterclass: Challenges in Stream Processing

Currency arbitrage

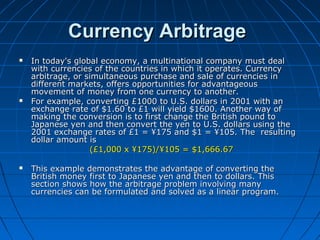

1. Currency ArbitrageCurrency Arbitrage

In today's global economy, a multinational company must dealIn today's global economy, a multinational company must deal

with currencies of the countries in which it operates. Currencywith currencies of the countries in which it operates. Currency

arbitrage, or simultaneous purchase and sale of currencies inarbitrage, or simultaneous purchase and sale of currencies in

different markets, offers opportunities for advantageousdifferent markets, offers opportunities for advantageous

movement of money from one currency to another.movement of money from one currency to another.

For example, converting £1000 to U.S. dollars in 2001 with anFor example, converting £1000 to U.S. dollars in 2001 with an

exchange rate of $1.60 to £1 will yield $1600. Another way ofexchange rate of $1.60 to £1 will yield $1600. Another way of

making the conversion is to first change the British pound tomaking the conversion is to first change the British pound to

Japanese yen and then convert the yen to U.S. dollars using theJapanese yen and then convert the yen to U.S. dollars using the

2001 exchange rates of £1 = ¥175 and $1 = ¥105. The resulting2001 exchange rates of £1 = ¥175 and $1 = ¥105. The resulting

dollar amount isdollar amount is

(£1,000 x ¥175)/¥105 = $1,666.67(£1,000 x ¥175)/¥105 = $1,666.67

This example demonstrates the advantage of converting theThis example demonstrates the advantage of converting the

British money first to Japanese yen and then to dollars. ThisBritish money first to Japanese yen and then to dollars. This

section shows how the arbitrage problem involving manysection shows how the arbitrage problem involving many

currencies can be formulated and solved as a linear program.currencies can be formulated and solved as a linear program.

2. Currency Arbitrage ModelCurrency Arbitrage Model

Suppose that a company has a total of 5 million dollars that canSuppose that a company has a total of 5 million dollars that can

be exchanged for euros (€), British pounds (£), yen (¥), andbe exchanged for euros (€), British pounds (£), yen (¥), and

Kuwaiti dinars (KD). Currency dealers set the following limitsKuwaiti dinars (KD). Currency dealers set the following limits

on the amount of any single transaction: 5 million dollars, 3on the amount of any single transaction: 5 million dollars, 3

million euros, 3.5 million pounds, 100 million yen, and 2.8million euros, 3.5 million pounds, 100 million yen, and 2.8

million Kds. The table below provides typical spot exchangemillion Kds. The table below provides typical spot exchange

rates. The bottom diagonal rates are the reciprocal of the toprates. The bottom diagonal rates are the reciprocal of the top

diagonal rates. For example,diagonal rates. For example,

rate(€ -> $) = 1/rate( $ -> €) = 1/0.769 = 1.30rate(€ -> $) = 1/rate( $ -> €) = 1/0.769 = 1.30

$ € £ ¥ KD

$ 1 0.769 0.625 105 0.342

€ 1/0.769 1 0.813 137 0.445

£ 1/0.625 1/0.813 1 169 0.543

¥ 1/105 1/137 1/169 1 0.0032

KD 1/0.342 1/445 1/543 1/0.0032 1

Is it possible to increase the dollar holdings (above the initial $5 million)

by circulating currencies through the currency market?

3. Mathematical Model:Mathematical Model:

The situation starts with $5 million. This amount goes through a numberThe situation starts with $5 million. This amount goes through a number

of conversions to other currencies before ultimately being reconverted toof conversions to other currencies before ultimately being reconverted to

dollars. The problem thus seeks determining the amount of eachdollars. The problem thus seeks determining the amount of each

conversion that will maximize the total dollar holdings.conversion that will maximize the total dollar holdings.

For the purpose of developing the model and simplifying the notation, theFor the purpose of developing the model and simplifying the notation, the

following numeric code is used to represent the currencies.following numeric code is used to represent the currencies.

Currency $ € £ ¥ KD

Code 1 2 3 4 5

Define:Define:

xxijij = Amount in currency i converted to currency j, i and j = 1,2, ... ,5= Amount in currency i converted to currency j, i and j = 1,2, ... ,5

For example,For example, xx1212 is the dollar amount converted to euros andis the dollar amount converted to euros and xx5151 is the KDis the KD

amount converted to dollars. We further define two additional variablesamount converted to dollars. We further define two additional variables

representing the input and the output of the arbitrage problem:representing the input and the output of the arbitrage problem:

II = Initial dollar amount (= $5 million)= Initial dollar amount (= $5 million)

yy = Final dollar holdings (to be determined from the solution)= Final dollar holdings (to be determined from the solution)

4. Mathematical Model:Mathematical Model:

Our goal is to determine the maximum final dollar holdings, y,Our goal is to determine the maximum final dollar holdings, y,

subject to the currency flow restrictions and the maximum limitssubject to the currency flow restrictions and the maximum limits

allowed for the different transactions.allowed for the different transactions.

1

($)

3

(£)

x13

0.625 x13

X13 ≤ 5

Definition of the input/output variable, x13, between $ and £

We start by developing the constraints of the model. FigureWe start by developing the constraints of the model. Figure

demonstrates the idea of converting dollars to pounds. The dollardemonstrates the idea of converting dollars to pounds. The dollar

amountamount xx1313 at originating currency 1 is converted toat originating currency 1 is converted to 0.625 x0.625 x1313

pounds at end currency 3. At the same time, the transacted dollarpounds at end currency 3. At the same time, the transacted dollar

amount cannot exceed the limit set by the dealer,amount cannot exceed the limit set by the dealer, xx1313 ≤ 5≤ 5..

To conserve the flow of money from one currency to another, eachTo conserve the flow of money from one currency to another, each

currency must satisfy the following input-output equationcurrency must satisfy the following input-output equation

Total sum available of

currency (input)

== Total sum converted of

other currencies (output)

5. Mathematical Model:Mathematical Model:

Dollar (i=1)Dollar (i=1)

Total available dollars = Initial dollar amount + dollar amount from otherTotal available dollars = Initial dollar amount + dollar amount from other

currenciescurrencies

= I= I + (€ $) + (£ $) + (¥ $) + (KD $)→ → → →+ (€ $) + (£ $) + (¥ $) + (KD $)→ → → →

= I + 1/0.769 x= I + 1/0.769 x2121 + 1/0.625 x+ 1/0.625 x3131 + 1/105 x+ 1/105 x4141 + 1/0.342 x+ 1/0.342 x5151

Total distributed dollars = Final dollar holdings + dollar amount to otherTotal distributed dollars = Final dollar holdings + dollar amount to other

currenciescurrencies

= y= y + ($ €) + ($ £) + ($ ¥) + ($ KD)→ → → →+ ($ €) + ($ £) + ($ ¥) + ($ KD)→ → → →

= y + x= y + x1212 + x+ x1414 + x+ x1414 + x+ x1515

GivenGiven II = 5, the dollar constraint thus becomes= 5, the dollar constraint thus becomes

y + xy + x1212 + x+ x1313 + x+ x1414 + x+ x1515 – (1/0.769 x– (1/0.769 x2121 + 1/0.625 x+ 1/0.625 x3131 + 1/105 x+ 1/105 x4141 + 1/0.342+ 1/0.342

xx5151) = 5) = 5

12. Mathematical Model:Mathematical Model:

SolutionSolution

The optimum solution (using file amplEx2.3-2.txt or solverEx2.3-2.xls) is:The optimum solution (using file amplEx2.3-2.txt or solverEx2.3-2.xls) is:

SolutionSolution InterpretationInterpretation

y = 5.09032y = 5.09032 Final holdings = $5,090,320.Final holdings = $5,090,320.

Net dollar gain = $90,320, which representsNet dollar gain = $90,320, which represents

a 1.8064% rate of returna 1.8064% rate of return

xx1212 = 1.46206= 1.46206 Buy $1,462,060 worth of eurosBuy $1,462,060 worth of euros

xx1515 = 5= 5 Buy $5,000,000 worth of KDBuy $5,000,000 worth of KD

xx2525 = 3= 3 Buy €3,000,000 worth of KDBuy €3,000,000 worth of KD

xx3131 = 3.5= 3.5 Buy £3,500,000 worth of dollarsBuy £3,500,000 worth of dollars

xx3232 = 0.931495= 0.931495 Buy £931,495 worth of eurosBuy £931,495 worth of euros

xx4141 = 100= 100 Buy ¥100,000,000 worth of dollarsBuy ¥100,000,000 worth of dollars

xx4242 = 100= 100 Buy ¥100,OOO,000 worth of eurosBuy ¥100,OOO,000 worth of euros

xx4343 = 100= 100 Buy ¥100,000,000 worth of poundsBuy ¥100,000,000 worth of pounds

xx5353 = 2.085= 2.085 Buy KD2,085,000 worth of poundsBuy KD2,085,000 worth of pounds

xx5454 = .96= .96 Buy KD960,OOO worth of yenBuy KD960,OOO worth of yen

13. Mathematical Model:Mathematical Model:

Remacks. At first it may appear that the solution is nonsensical because itRemacks. At first it may appear that the solution is nonsensical because it

calls for usingcalls for using

xx1212 + x+ x1515 = 1.46206 + 5 = 6.46206= 1.46206 + 5 = 6.46206

or $6,462,060 to buy euros and KDs when the initial dollar amount is onlyor $6,462,060 to buy euros and KDs when the initial dollar amount is only

$5,000,000. Where do the extra dollars come from? What happens in$5,000,000. Where do the extra dollars come from? What happens in

practice is that the given solution is submitted to the currency dealer aspractice is that the given solution is submitted to the currency dealer as

one order, meaning we do not wait until we accumulate enough currencyone order, meaning we do not wait until we accumulate enough currency

of a certain type before making a buy. In the end, the net result of allof a certain type before making a buy. In the end, the net result of all

these transactions is a net cost of $5,000,000 to the investor. This can bethese transactions is a net cost of $5,000,000 to the investor. This can be

seen by summing up all the dollar transactions in the solution:seen by summing up all the dollar transactions in the solution:

I = y + xI = y + x1212 + x+ x1313 + x+ x1414 + x+ x1515 – (1/0.769 x– (1/0.769 x2121 + 1/0.625 x+ 1/0.625 x3131 + 1/105 x+ 1/105 x4141 + 1/0.342+ 1/0.342

xx5151) = 5.09032 + 1.46206 + 5 – (3.5/0.625 + 100/105) = 5) = 5.09032 + 1.46206 + 5 – (3.5/0.625 + 100/105) = 5

Notice thatNotice that xx2121, x, x3131, x, x4141 and xand x5151 are in euro, pound, yen, and KD, respectively,are in euro, pound, yen, and KD, respectively,

and hence must be converted to dollars.and hence must be converted to dollars.