Siemens PLM e a liderança na Indústria automobilística

•

1 like•715 views

Veja aqui o Infográfico apresentando a liderança da Siemens PLM no mercado Automotivo

Recommended

More Related Content

Viewers also liked

Viewers also liked (11)

More from PLMX -Soluções para Negocios

More from PLMX -Soluções para Negocios (20)

Recently uploaded

Recently uploaded (20)

Siemens PLM e a liderança na Indústria automobilística

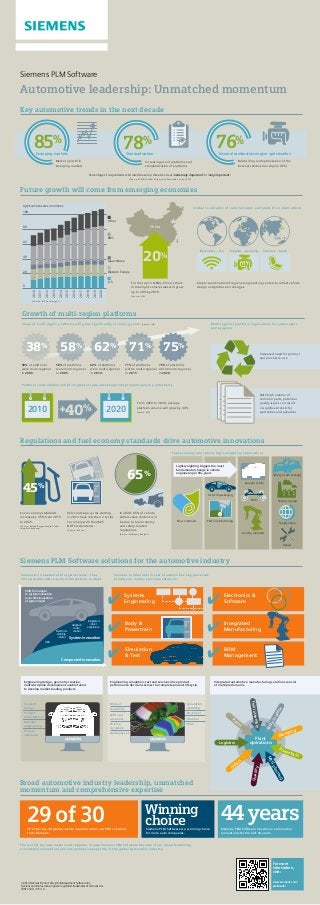

- 1. Automotive leadership: Unmatched momentum Siemens PLM Software © 2014 Siemens Product Lifecycle Management Software Inc. Siemens and the Siemens logo are registered trademarks of Siemens AG. 43811-X20 12/14 A For more information, visit: www.siemens.com/ plm/leader Downsizing and optimization of the internal combustion engine (ICE) Increasing use of platforms and standardization of platforms Market growth in emerging markets Broad automotive industry leadership, unmatched momentum and comprehensive expertise Winning choiceSiemens PLM Software is a winning choice for more auto companies. 29 of the top 30 global vehicle manufacturers use PLM solutions from Siemens. 29 of 30 44 yearsSiemens PLM Software has driven automotive innovations for the last 44 years. The world’s top automakers and suppliers choose Siemens PLM Software because of our broad leadership, unmatched momentum and comprehensive expertise in the global automotive industry. Siemens PLM Software solutions for the automotive industry Innovation is needed at the system level – thus more people need to work in the systems context. Shift from single to system innovation (over 50% innovation at system level) Component innovation System innovation ABS Electronic stability control Adaptive cruise control Integrated driver experience Bodyinwhite Stamping Powertrain MFGplanning Paint Logistics Plant operations Orders Qualilty Finalassembly Engineering simulation, test and services drive product performance decisions across the complete product lifecycle. Engineering design, geometry creation, multi-discipline development enable teams to develop market-leading products. Simulation modeling Structural Thermal Flow Motion Durability NVH and acoustics Driving dynamics Multi-physics Concept design Product development Detailed engineering Process validation Integrated automotive manufacturing solutions consist of multiple domains. Siemens continues to invest in automotive key processes to help you realize your innovation in: Systems Engineering Body & Powertrain Simulation & Test Electronics & Software Integrated Manufacturing BOM Management Repair Supply chain Factory design Safety (crash testing) Fuel-economy and vehicle light-weighting implications New materials Part manufacturing Vehicle packaging Analysis (CAE) NVH Joining methods Light-weighting triggers the most fundamental change in vehicle engineering in 50+ years 45% Vehicle design cycles starting in 2013 have less than 2 cycles to comply with the 2025 NHTSA standards. (Source: IHS Inc.) Regulations and fuel economy standards drive automotive innovations Fuel economy standards increase by 45% from 2015 to 2025. (Source: Roland Berger/Lazard Global Supplier Database) 65% In 2020, 65% of vehicle added-value content will be due to fuel economy and safety-related regulations. (Source: McKinsey Analysis) Growth of multi-region platforms 38% of platforms were multi-regional in 2000. 58% of platforms were multi-regional in 2005. 62% of platforms were multi-regional in 2010. 71% of platforms will be multi-regional in 2015. 75% of platforms will be multi-regional in 2020. 38% 58% 62% 71% 75% Share of multi-region platforms will grow significantly in coming years (Source: IHS) Multi-regional platform implications for automakers and suppliers Platform consolidation will drive greater scale advantage and program launch productivity From 2010 to 2020, average platform volume will grow by 40% (Source: IHS) Increased need for product and process re-use With high volume of common parts, potential quality issues can result in significant costs for warranties and penalties2010 2020+40% For the top 12 OEMs, China’s share in total light-vehicle sales will grow up to 20% by 2019. (Source: IHS) China 20% Electronics – U.S. Engines – Germany Interiors – Japan Global localization of vehicle design and production implications Global coordination of regional engineering centers to reflect vehicle design and production changes. Future growth will come from emerging economies (Source: IHS Auto Insight ) 100 Light-vehicle sales in millions 80 60 40 20 U.S. 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 0 Western Europe Japan/Korea BRIC Other Key automotive trends in the next decade 76% Standardization Internal combustion engine optimization 78%85% Percentage of respondents who rated these top three trends as ‘extremely important‘ or ‘very important‘. (Source: KPMG‘s Global Automotive Executive Survey 2014) Emerging markets