EY Global Consumer Insurance Survey 2014

•

1 gostou•1,196 visualizações

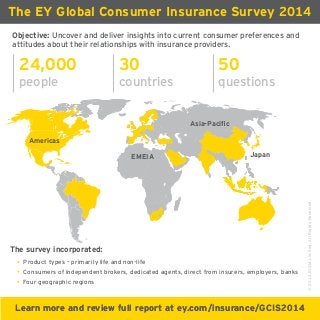

Objective: Uncover and deliver insights into current consumer preferences and attitudes about their relationships with insurance providers.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais de EY

Mais de EY (20)

EY Global Consumer Insurance Survey 2014

- 1. ©2014EYGMLimited.AllRightsReserved.Learn more and review full report at ey.com/insurance/GCIS2014 The EY Global Consumer Insurance Survey 2014 Objective: Uncover and deliver insights into current consumer preferences and attitudes about their relationships with insurance providers. 24,000 people 30 countries 50 questions Product types – primarily life and non-life Consumers of independent brokers, dedicated agents, direct from insurers, employers, banks Four geographic regions Learn more and review full report at ey.com/insurance/GCIS2014 The survey incorporated: Americas Asia-Pacific EMEIA Japan

- 2. ©2014EYGMLimited.AllRightsReserved. The EY Global Consumer Insurance Survey 2014 Key Finding 1 High turnover and low trust signal serious relationship issues. Supermarkets Banks Car manufacturers Online shopping sites Insurance companies Pharmaceutical companies 84% 82% 80% 78% 68%70% Insurers are not as trusted as other types of businesses Learn more and review full report at ey.com/insurance/GCIS2014

- 3. ©2014EYGMLimited.AllRightsReserved. The EY Global Consumer Insurance Survey 2014 Key Finding 2 Just because they leave you doesn’t mean they don’t love you. Good news: insurers have many advocates 66% Customers likely or very likely to recommend their insurance provider to friends or relatives. Bad news: advocates often leave Customers willing to recommend their insurance provider who have closed policies in last 18 months. 38% The relationship can go on even if policies are lost “Alumni” customers who leave may have future value$ Learn more and review full report at ey.com/insurance/GCIS2014

- 4. ©2014EYGMLimited.AllRightsReserved. The EY Global Consumer Insurance Survey 2014 Key Finding 3 Insurers have so few interactions with their customers that each one becomes a critical moment of truth. 44% Customers who have had no interactions with their insurers in the last 18 months 70%Customers experiencing moments of truth who report a positive outcome Engagement = Opportunity Learn more and review full report at ey.com/insurance/GCIS2014

- 5. ©2014EYGMLimited.AllRightsReserved. The EY Global Consumer Insurance Survey 2014 Key Finding 4 Consumers want more frequent, meaningful and personalized communications. Customers who want to hear from their insurers at least semi-annually 57% Customers who currently hear from their insurers at least semi-annually 47% Ready to hear from you Only 14% of customers are very satisfied with current communications Learn more and review full report at ey.com/insurance/GCIS2014

- 6. ©2014EYGMLimited.AllRightsReserved. The EY Global Consumer Insurance Survey 2014 Key Finding 5 As consumers embrace digital, insurers must rethink their distribution strategies and partner relationships. 80% Consumers willing to use digital and remote channel options for different tasks and transactions. Phone Video Online ChatEmail Learn more and review full report at ey.com/insurance/GCIS2014