EY Customer Segments Banking Offerings

•Download as PPTX, PDF•

1 like•180 views

A compiled detail version of EY Customer Segment Offerings to these group of people - Migrant Workers, SMEs, Entrepreneurs, The Future Silver Economy, Rural Agri-Laborers, Students Studying Abroad, Non-Profit Organizations (NPOs), Gig Economy Workers, SINKs & DINKs and NSF

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to EY Customer Segments Banking Offerings

Similar to EY Customer Segments Banking Offerings (20)

More from Varun Mittal

More from Varun Mittal (20)

Recently uploaded

Recently uploaded (20)

EY Customer Segments Banking Offerings

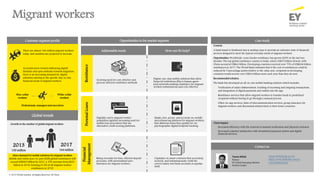

- 1. Migrant workers Global trends Context: A bank based in Southeast Asia is seeking ways to provide an extensive suite of financial services designed to meet the typical everyday needs of migrant workers. Opportunities: Worldwide, cross-border remittance has grown 600% in the last two decades. The top global remittance country is India, where US$70 billion flowed, with China second at US$64 billion. Developing countries received over 75% of US$636 billion remittances in 2017. The World Bank estimates that if the cost of remittances could be reduced by 5 percentage points relative to the value sent, recipients in developing countries would receive over US$16 billion more each year than they do now. Recommended solution: The bank has developed an all-in-one mobile banking solution which includes: • Verification of salary disbursement, tracking of incoming and outgoing transactions, and integration of digital payments and wallets into the app. • Remittance services that allow migrant workers to transfer funds to predefined recipients without having to go through a manual process. • Other on-app services: Sales of telecommunication services, group insurance for migrant workers, and discounted airfares back to their home countries. More demand for mobile solutions for migrant workers Mobile and online peer-to-peer (P2P) global remittances will exceed US$300 billion by 2021, a 33% increase from $225 billion in 2018, forming 61.8% of all migrant worker remittances in 2018. Client impact: • Increased efficiency with the removal of manual verification and physical contracts. • Increased customer satisfaction with streamlined payment system and digital financial services. There are almost 164 million migrant workers today, and numbers are projected to increase. As trends move toward embracing digital lifestyles and open attitudes towards migration, there is an increasing demand for digital solutions catering to the specific day-to-day financial needs of migrant workers. Professionals, managers and executives White-collar workers Blue-collar workers Personal Loans Digitally-savvy migrant worker population signifies increasing need for mobile loan procedures that use alternative credit scoring platforms. Hassle-free, secure, and accurate on-mobile microfinancing platform for migrant workers that disburses loans they qualify for via psychographic digital footprint tracking. Financial Management Rising necessity for time-efficient deposit processes, with personalized user- interfaces for migrant workers. Capitalize on smart contracts that accurately, securely, and instantaneously credit the correct salary into bank accounts on payday itself. Growth in the number of global migrant workers 2013 150 million 2017 164 million Remittance Growing need for cost-effective and process-efficient remittance methods. Digital, one-stop mobile solutions that allow financial institutions (FIs) to bypass agent- send networks making remittance for migrant workers instantaneous and cost-effective. Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Contact us:

- 2. Small and Medium Enterprises (SMEs) Global trends Context: A bank is looking into issuing loans to online retailers. However, it is difficult to assess the credit risk of SMEs without data points. Opportunities: Over 67.8% of SMEs prefer non-traditional financing options. Banks are moving towards offering peer-to-company (P2C) loans by coming up with specialized loans for SMEs. Recommended solution: • Partner with online retailers and offer loans to sellers on those platforms. • Lenders must have conducted some transactions before they are eligible for the loans. • Loan payment will be collected by deducting money monthly form the seller’s account. • In the event where the lender is unable to repay loans, their inventory will be liquidated and sold off to recoup the money. Money can also be recouped directly from the lender’s bank account or credit card. Increasingly, SMEs act as engines of economic growth and laboratories for innovation - helping to build modern economies that improve people’s lives. This is especially true in Emerging Markets (EMs) where SMEs account for 80% of jobs and 33.3% of GDP. However, SMEs face high barriers in accessing finance to scale their businesses. Formal Micro (<5 FTE) 18% Formal SME (>5 FTE) 7% Estimated no. of SMEs in EMs (365 million -445 million) SME Informal 70% Accounting Rising demand for automated accounting processes such as reconciliation and expense reporting. One-stop platform for all SMEs needs including invoicing, submitting expenses and bank reconciliation using an app. Loans There is a growing need for SME loans that do not require collateral. Assess credit risk via alternative credit scoring using aggregators such as information collected from retailers. Client impact: • Total loan amount being disbursed in a year: US$1 Billion. • Eliminated risk of default by liquidating assets of lenders. Insurance Growing need for cost-effective insurance management solutions catered to SMEs. Provide customizable modular insurance based on the size, budget and needs of the company, while automating claims for a seamless user experience. 70% of all SMEs in EMs lack access to credit 82% of SMEs in ASEAN prefer to invest in technology as a means to raise productivity Of which, 78% would prefer business-oriented tools 82% 70% 78% Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 3. Entrepreneurs Global trends From young to old, there is a rise in the number of people interested to start their own business. Currently, there are 400 million entrepreneurs in the world. Context: A bank was looking for a solution to offer funding to entrepreneurs with inconsistent revenue stream and a small amount of information on credit worthiness. It is difficult to assess the risk of providing loans to budding entrepreneurs with no past track records. It is also time consuming and slow to utilize paper business loan application. Opportunities: Median year-on-year decrease in bankruptcy rates stood at an average of 7.5% since 2012, reflecting improved economic climates for entrepreneurs. Recommended solution: We recommend utilizing a digitalized loan application process which allows loans to be applied online, providing convenience to busy entrepreneurs. • Every loan application will automatically run through a bank’s risk model. • Detailed reports are generated for lenders to monitor borrowers loan activity and credit spread. 67% of entrepreneurs cited the lack of capital and cash flow management as their the top concern. Entrepreneurs may not be able to enjoy benefits full-time employees have, such as insurance plans which is often at the back of their mind. Loan Approvals 41% of business owners do not have life insurance. Big Banks Small Banks Institution lenders 24.3% 26.1% 48.7% 49.6% 63.8% 64.8% June’17 June’18 66% of the people worldwide think entrepreneurship is a good career choice. 77% of small business rely on personal savings for their initial funds. 77% 41% 66% Insurance Growing need for cost-effective insurance management solutions catered to entrepreneurs. Provide customizable modular insurance based on the size, budget and needs of the company, while automating claims for a seamless user experience. Raising Capital Increase demand for alternative forms of credit scoring for new entrepreneurs who may experience income volatility, and have insufficient collateral. Automatic and accurate evaluation of entrepreneurs’ risk by analyzing their digital footprint. Increased profitability for banks to provide loans to entrepreneurs by converting their illiquid assets to digital assets. Automate payments to ensure timely cash inflow from customers using ledger technology. One-stop digital solution that manages company finances including forecast adjustment based on intrinsic and extrinsic factors. Financial Management Increasing need for a convenient and hassle-free cash flow management solution that improves entrepreneurs’ bargaining power. Client impact: • Improved customer satisfaction with efficient and simple loan application process. • Reduced time taken for loan applications and approvals from hours to minutes. • The automated decline function freed up loan officers’ time. • Removed the need for bank’s customers to physically visit a branch office to apply for loan. Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 4. The Future Silver Economy Global trends Context: A bank is looking to make banking services more reliable and secure for the elderly through guarding them against identity theft, as well as help them manage their finances in a personable yet efficient fashion. Opportunities: The global silver economy is estimated to be valued at US$15 trillion by 2020. Recommended solution: • Integrating a machine-learning solution that understands the specific customer’s financial profile, and identifies any suspicious behavior which differs considerably from his usual financial activity. • In the event where there may be suspicious behavior, alerts are automatically sent to trusted family members, lawyers, or advisors. • The machine-learning solution is able to understand financial behavior, such as whether an individual is a net saver or net spender, and provides financial planning and investment advice following the analysis. The 'Silver Economy’ traditionally refers to older people between 65 and 75 who retired. In 30 years time, the number of people aged 60 years or over would have doubled. Over half of the those aged below 30 years are worried about growing older. Globally, population aged 60 or over is growing faster than all other age groups. Growth They are often concerned about saving up for their retirement fund and health implications that may arise from ageing. Additionally, the number of people with dementia worldwide is expected to increase to 82 million in 2030. This creates concern for their financial management as they age. Investments Increased demand for customized portfolio management for elderly as they age and develop health complications. Provide a convenient and reliable investment tracking tool that can automatically rebalance their portfolio with minimal monitoring. Insurance Burgeoning elderly population requires convenient insurance solution with user- friendly interface catered to their needs. Simplified, voice-activated, one-stop claims solution which can share receipts with insurance company and provide customer service support. Financial Management Real-time, 24/7 interface to explore financial planning in a cost-effective way, built on a secure platform that monitors clients’ financial activities, identifying signs of exploitation or anomalies. Rising importance of secure, easy-to-use and reliable banking services provider for the elderly as they are susceptible to identity theft. Client impact: • Earned the trust of the elderly clientele as a bank that is able to make transactions secure and efficient. • Streamlined and value-added digital customer service for a new growth market, enabling the bank to have a stronger market hold compared to future competitors. Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 5. Rural Agri-Laborers Debt profile – Thai farmers Farming and Agricultural operations employ 40% of Thailand’s 33 Million person workforce, with an estimated contribution of 10% to the national GDP. Majority of the farms are family-run and smaller in scale, making it difficult for them to secure financing for their operations. Context: A financial institution was looking to implement a payment solution for one of its major clients, a farming corporation with over 100,000 independent farmers and 154 buying centers. Farmers would come to these buying centers to sell their produce, and in return given cash. However this proved to be problematic as on occasion, over €120,000 was being transferred daily, leading to the potential of robbery, staff misappropriation of money, and the added logistics of depositing large amounts of cash into bank accounts daily. Opportunities: Thailand’s agricultural export accounts for 8.4% of her GDP which amounts to USD 38.2 billion. Applicable solution: • Implement a web based system that allows produce to be weighed, and then processing payments to vendor accounts upon completion. • Automate most of the sale process, by only requiring personnel to spot check products for quality control before automatically weighing. These farms rely on outdated methods of recording transactions and contracts. Payments One-stop mobile solution that records terms of contract and automates payments. Digital ledger that records transactions and contracts to build trust between buyers and sellers. Insurance A financial product that allows agri- laborers to insure the most valuable portions of their crops, hedging the risk of a potential poor harvest and minimize losses. Rising need for crop insurance given the wider variability in crop yield. Financing A growing segment of agri-laborers need flexible loan arrangements for seasonal fluctuations in crop produce. Implement a solution that allows agri- laborers to instantly withdraw funds as needed as opposed to a lump sum loan. B$338 Billion Average amount borrowed by loan sharks in a year to finance farm operations and higher entry costs. Accumulated debt for a rural-agri farmers, due to high interest rate. Estimated increase in average annual income by 2037, stipulated in the government’s “Thailand 4.0” economic model. B$21.59 Billion 700% Client impact: • Generated credit scores using historical earnings of farmers, which can be utilized should they wish to apply for a bank loan. • Increased bank efficiency by reducing the amount of cash the bank counts and handles each day. Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 6. Students Studying Abroad Global trends With the world continuing to become connected, more students have begun to recognize the value of studying outside of their home country to gain a global education, in addition to international exposure. Context: A large bank was looking to provide a simplified banking solution for students abroad, who often face difficulties managing their personal finances. The implementation of a digital system would provide a seamless banking experience at an affordable cost for them. Opportunities: Asian students account for 53% of all students studying abroad worldwide with the cost of higher education abroad averaging around US$157,782. 45% of parents would consider buying a property in their child's country of study and this growing market requires financial services. Recommended solution: The bank is offering a mobile application tailored to the needs of travelers which includes: • 24/7 foreign currency conversion on the app at competitive foreign exchange rates by tracking the rates and converting them in real-time. • Ability to top up the card wallet easily through the app or online. • Enhanced security feature by allowing the card to be locked remotely via the app when it is lost. • Hold multiple currencies to avoid hidden charges by transacting in local currency. • Withdrawals can be done overseas at selected ATMs. • Travel insurance available for purchase. Study Abroad Destinations • There are currently almost 5 million international students globally today • By 2025, it is projected that that number will rise to over 8 million • 53% of current global international students originate from Asian countries As a result of moving to a foreign country, there are inconveniences and hurdles that these international students face. Payments Multi-currency card which allows storing of different currencies and offers competitive exchange rate. Increasing number of students studying abroad imply a greater need for cashless solution such as debit cards. Insurance Growing need for insurance policies tailored to students studying abroad such as insurance covering lost or stolen items. Bite-size travel insurance policy options available for students to purchase their desired level of coverage. Savings Rising demand for international bank accounts in country of education. Cross border accounts, with the ability to utilize a singular bank account in several countries and hold several currencies. Client impact: • Increased suite of services available for students studying abroad, providing them a convenient and affordable banking option. USA U.K. australia france germany All other countries Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 7. Non-Profit Organizations (NPOs) Global trends Context: A bank is looking for a solution to provide increased transparency in the donation process made by the donors to the NPOs’. Opportunities: From 2012-2018, online donations worldwide increased year-on-year at an average of 10.7%, cumulatively adding up to US$149.1 billion. Recommended solution: It is recommended that the FI utilize digital technology to prevent international aid payments fraud. • A cloud-based, end-to-end digital payments solution can be created to provide a secure, private and fully-traceable service. • Currency exchange can be done by the banks to eliminate the high foreign exchange and bank fees. • All transactions are traceable and permanently recorded on the platform. • Fraud detection and protection programs are also included in the system. Client impact: • Decreased the cost of cross-currency payments through optimization of bank and foreign exchange fees. • Increased transparency of donations through payment tracking system. Non-profit Companies Charities Religious Organizations Transparency NPO’s heavy reliance on public funding demands greater transparency in donations. Time Due to the nature of the non-profit industry, raising funds is a recurring struggle for them. Traceability 30% of money donated as foreign aid is lost to corruption and fraud, according to the United Nations. 40% of Millennial donors are enrolled in a monthly giving program. 25% of donors complete their donations on mobile devices. 31% of donors worldwide donate to NPOs outside their country of residence. 25% Insurance There is a growing need for group insurance policies by NPOs without P&L statements. Insurance policy tailored to the needs of NPOs. Loans Rising necessity of NPO-tailored loans for acquisition, construction and equipment. Assess creditworthiness of NPOs by analyzing their payments footprint, such as rent and utility bill payment. Collections Provide a affordable and transparent and traceable solution to transfer money overseas allowing customization of payments frequency. Increased desire by the public and NPOs for cost-effective collection solutions that offer a greater level of auditability and traceability of donations. 40% 31% Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 8. Gig Economy Workers Global trends Context: A bank wanted to target gig workers who didn’t qualify for loans under traditional credit scoring systems used to assess the risk of lending to individuals. Acknowledging that these were potentially healthy clients, the bank was losing >90% of them to unconventional competitor such as P2P lenders because of the lack of customer information. Opportunities: 49% of gig workers are interested doing digital-enabled work. While 47% of gig workers sell goods and services on platforms such as Carousell, 43% drive cars, 24% share online content or videos and 11% have set up a start-up. Recommended solution: To increase the number of loans disbursed for these underserved individuals, it is recommended that the bank develop an alternative credit scoring rubric for gig workers: • Integrate a FinTech solution into the client’s mobile devices to collect their digital footprint. • The solution tailors a set of smart credit criteria rules based on bank’s preference and gig worker’s usage pattern on their phones. Client impact: • Significant increase of loans disbursed with a delinquency increase of only 2.3%. • User adoption reached 78% by the end of the trial. • Reduced need for manual check as processing time is shortened by hours. • Maintained FTE count for loan processing even when loan application increased. Ride-Hailing Drivers Digital “Influencers” Entrepreneurs From ride-hailing app drivers to tech entrepreneurs, there is a rise in the number of people working in the gig economy. 33% of global workforce is opting for gig-economy work. While the gig economy offers flexibility and independence, income is volatile and “gig” workers do not enjoy the same benefits as employees in large companies do. Global motivations for gig economy Primary Income Interim Income (between jobs) 55% 22% 19% Supplementary Income 50% of organizations report significant increase in the use of gig workers over the last five years 36% of employees in APAC may lose access to health protections 97% of the gig economy workers are likely to stay for more than 2 years Insurance Increased preference for easy- to-use, digital insurance platforms that offer flexibility and breadth specific to their on- the-job risks. Optimize premium pricing for each individual by providing telematics insurance. Digitally deliver usage-based insurance tailored to gig workers’ lifestyle. Personal Loans Offer short-term, flexible loans by analyzing their digital footprint. Simplifying loan application process across all channels by leveraging on mobile applications. Burgeoning demand for alternative forms of credit scoring for gig workers as they experience income volatility. Financial Management Require an on-the-go, portfolio management solution that suits their dynamic schedule and risk appetite. Digital nomads require low-cost and convenient cross-border transactions solutions. Mobile-first and wealth saving platform using auto portfolio rebalancing based on investors’ risk appetite. Utilize remittance platform to make cross-border transactions simple and affordable. 50% 36% 97% Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 9. 58464 70939 99378 132161 USA Singapore UAE Hong Kong SINKs & DINKs (18-49 years old, no kids) Global trends Average spending on child‘s education (in USD) Housing Wedding loans Childcare expenses Newly Weds often find it a struggle to manage their finances. After paying off their wedding and honeymoon, they have to consider housing and education costs, should they have children. Couples are not planning their outlay properly before they have children. Context: A banking financial company is looking to provide personal loans for consumers online without heavy documentation, which is often needed for large ticket loans. Couples who wish to obtain recurring loans online instantly would be attracted to use this platform. Opportunities: Globally, the percentage of women having a two-child family had fallen by 7% in 20 years. In Thailand, childless couples form 16% of all Thai families due to the rising cost of living and desire to improve discretionary income. Recommended solution: It is recommended that the bank utilize an online loan platform allowing customers to obtain recurring loans while improving their credit worthiness. • Self-learning chatbot allows application, document submission and loan approvals to be on the website, messenger and on the application. • Customers empowered to repay loans swiftly and timely by creating a seamless payment solution, allowing loans to be repaid online or on the application. 75% of parents rely on their day-to-day income to fund their children’s education rather than on longer- term investments and savings. 61% of engaged couples plan to charge their expenses to their credit card. Personal Loans Customize loans for young couples’ lifestyle and housing needs. Tailor loans for young couples by analysing their digital footprint to understand their needs. Automatic and accurate evaluation of young couples’ risk by analyzing their digital footprint and transaction history. Client impact: • Reduced operating cost of bank due to faster turn-around time using cloud based technology. • Increased loans available for customers who are borrowing short-term for everyday uses due to faster turn-around time. Increase demand for alternative forms of credit scoring for young couples who need to take on multiple, customized loans. Financial Management Increasing focus on growing their retirement funds especially for couples not planning to have children. Growing need for a convenient investment portfolio and financial management solution, including saving up for an emergency fund. One-stop solution that includes budgeting and expense control, providing 24/7, real-time monitoring. Provide a convenient investment tracking tool with the ability to automatically rebalance the portfolio. 75% 61% Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 10. Singapore National Service Full-time (NSF) Insurance Opportunities As per 8th December 2018 estimates, there are 45,800 NSFs serving in the military. These NSFs receive equitable monthly allowances, and are covered under an existing MINDEF/MHA group insurance scheme. Context: A global financial services group was looking to expand it’s customer base by offering a mobile, on-the-go insurance scheme for military personnel. However, they recognized that these military personnel were regularly on the move, and many soldiers, sea men and air men go for tours and deployments in far-away regions for months at a stretch. Furthermore, some of these military personnel already had disabilities that were a direct result of war, and the group wanted to create a seamless banking/insurance experience for them. Recommended solution: • It is recommended for the group to set up a separate mobile channel for military men and women who only have access low-bandwidth internet, one that keeps the essentials of a mobile-banking/insurance solution. • Furthermore, injured veterans i.e. visually impaired soldiers can deposit checks using voice-guided Natural Language Processes (NLPs) features on their mobile devices. Client impact: For clients who installed the white-labelled application and agreed to the data collection • Served military personnel who previously did not have access to conventional business solutions while they were on military tours. • Increased customer satisfaction with streamlined digital financial services for their military clients. • Removed high-bandwidth internet requirements, improving accessibility to financial services for soldiers on the go. However, the lack of accessibility and flexibility with current financial solutions limit the value provided to the NSF and the FIs. Republic of Singapore Air Force Republic of Singapore Navy Republic of Singapore Army $27,400 $22,100 $17,060 Estimated earnings for an NSF (22 months) Cumulatively, the estimated earnings of all military NSFs over the period of their 2 years would total to SGD $895,506,800 Estimated earnings for a combat specialist Estimated earnings for a combat naval Diver/Commando/Officer Estimated earnings for a combat enlistee Leveraging on data-centric solutions to gather non-confidential data that optimizes premium prices based on the NSF’s digital footprint and their pre-assessed vocational risk. Increased preference for easy-to-use, digital insurance platforms that offer flexibility and breadth in terms of coverage, beyond just life, disability, and accident. Growing insurance needs for NSFs who require follow-up insurance solutions after their tenure of service (for health conditions that arise in their line of service) Burgeoning demand for insurance schemes that offer tailored plans, covering vocation-specific risks and responsibilities. Seamless and customized insurance plans for servicemen that follows through beyond their Operationally-Ready-Date (ORD). Digitally assisted, one-stop solution for servicemen to share reports with the insurer, from wherever they are in the world. Opportunities in the market segment Customer segment profile Case study How can FIs help? Addressable needs © 2019 EYGM Limited. All Rights Reserved. ED None Varun Mittal Partner EY Global Emerging Markets FinTech Leader varun.mittal@sg.ey.com https://www.linkedin.com/in/ varunmittalonline Contact us:

- 11. EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. © 2019 EYGM Limited. All Rights Reserved. EYG no. 000980-19Gbl This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice. ey.com

Editor's Notes

- Onboard existing fintechs. Transferwise Personal loans – psychography default tracker

- Accounting: Opportunity for .. As SME spend min of 20 hrs…. OCBC bizsolution/ UOB bizsmart One stop platform for all SME needs through the use of open APIs. (Xero) Rephrase high complexity. Retailers have info of SMEs. Have data points to do credit scoring. Amazon and BoA Merrill Lynch case study. Case study: (MSMEs) Context: A bank in Philippines was looking for a solution to offer lending solutions to SMEs that do not have a financial track record nor parent company support. Furthermore, the bank targeted SMEs that required quick funding to pay their employees, and have limited options for affordable financing. The bank aimed to loan an amount of USD 50-150 for a period of 10 to 30 days, at 1% interest per day. Recommended solution: This platform should offer merchant and e-commerce financing, invoice financing and online trade financing specifically tailored for these SMEs. Partner a non-bank digital SME provider, and integrate their white-labelled Software Development Kit (SDK) into the client’s mobile app. Tailor a set of smart credit criteria rules based on bank’s preference and customer’s application data, and non-anonymous data collected from the customer‘s smartphone. By finding non-traditional ways to serve SMEs, EY offers unconventional solutions to help banks develop methods to accommodate the growing needs of this increasing bracket of the global economy. Client impact: Total loan amount being disbursed: USD $200,000 Number of borrowers who defaulted on their first loan payment: Decreased by 63%, from 75% to 28% Percentage of clients who are repeat clients: ~40% Time to “Yes”: Less than 1 hour for 90% of customers who applied for a loan

- dementia. Growing. Financial management -> trust bank to manage their assets. Auto rebalancing. Since they getting old. Autoportfolio rebalancing --> is this the right solution? - Humanize the information Simplify interactions and changing capabilities Simplify paper-less, one-stop claim solution, digitally assisted one-stop claim solution to share receipts and reports with the insurer Real-time, 24/7 accessible, cost-effective

- https://www.sciencedirect.com/science/article/pii/S0305750X15002703 https://krishijagran.com/blog/top-7-banks-providing-easy-loans-to-agri-laborers/ https://www.globalagriculture.org/report-topics/industrial-agriculture-and-small-scale-farming.html http://spore.cta.int/en/article/mobile-based-payment-solution-for-smallholder-farmers.html

- Search: propensity of students to be high flyers. High salary. They become high networth customers who needs banks. http://monitor.icef.com/2017/09/oecd-charts-slowing-international-mobility-growth/ http://www.oecd.org/education/imhe/46130419.pdf https://www.citibank.com.sg/gcb/deposits/global-foreign-currency-account.htm?icid=SGDPAFCENSTSGCALM https://migrationdataportal.org/themes/international-students https://stats.oecd.org/Index.aspx?DataSetCode=EDU_ENRL_MOBILE https://www.oecd-ilibrary.org/education/data/education-at-a-glance/share-of-international-students-enrolled-by-country-of-origin_0223bce2-en https://www.oecd.org/education/skills-beyond-school/EDIF%202013--N%C2%B014%20(eng)-Final.pdf https://rhbgroup.com.sg/personal/travelfx

- Usage-based insurance. Telematics Auto portfolio rebalancing based on investors’ risk appetite using robo-advisors Data source for credit scoring.

- https://www.weforum.org/agenda/2017/08/parents-in-these-countries-spend-the-most-on-their-childrens-education/ https://www.cnbc.com/2018/03/13/wedding-debt-can-hurt-a-couples-financial-future.html Insurance http://www.digitalinsuranceagenda.com/118/bima-brings-micro-insurance-to-underserved-families-in-emerging-markets/ http://www.digitalinsuranceagenda.com/94/policypal-your-digital-insurance-manager/ Case study: https://www.thehindubusinessline.com/money-and-banking/icici-bank-paytm-team-up-to-offer-small-digital-loans/article9963942.ece https://www.icicibank.com/aboutus/article.page?identifier=news-paytm-and-icici-bank-tieup-to-offer-short-term-instant-digital-credit-20171611114321842 https://economictimes.indiatimes.com/wealth/personal-finance-news/etmoney-partners-with-fullerton-india-to-offer-personal-loans-up-to-rs-20-lakh/articleshow/67176044.cms https://www.expresscomputer.in/news/fullerton-indias-digital-business-has-grown-10x-in-the-last-one-year/25133/ https://www.fullertonindia.com/pdf/pr/PR-Paytm-26June2018.pdf