2. Definition

• "Cheque is an instrument in writing containing an unconditional

order, addressed to a banker, sign by the person who has deposited

money with the banker, requiring him to pay on demand a certain

sum of money only to or to the order of certain person or to the

bearer of instrument."

• Section 5 of the Indian Negotiable Instrument Act of 1881

defines the Cheque as “A Bill of Exchange drawn specially

on a specified Banker and not on expressed to be

payable otherwise than on demand”...

5. Essentials of Cheque

• It is an Instrument in writing, i.e., it must be written in Ink

and not by pencil.

• It must be Drawn on Particular Bank. It is drawn by a

customer who has deposited money with the Bank.

• It must not contains any conditions.

• It must be signed by the Account holder.

• It is always payable on demand.

• It must contain an order to pay certain sum of money

• A Cheque is payable to a Specified Person Only

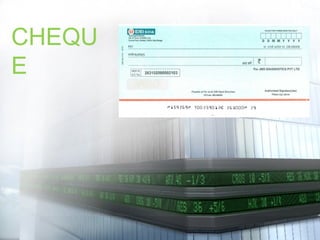

6. 400 026 016

Crossing of Cheque

Payee Name

Date

Amount In Words

Bank

Signature of

Drawer

Account No.

Amount

7. Types of Cheque

• Bearer Cheque

• Order Cheque

• Open Cheque

• Crossed Cheque

• Anti-Dated Cheque

• Post-Dated Cheque

• Stale Cheque

• Mutilated Cheque

8. 1) Open cheques

A) Bearer cheques:

• If a drawer orders the bank to pay a stated sum of money to the

bearer, it is called a bearer cheque.

• Any person who lawfully possesses a bearer cheque is entitled to

receive payment of that cheque.

B) Order cheques:

• If a cheque is to the order of a person in whose favor the cheque is

drawn it is called order cheque.

• The order cheque is paid by the bank only when the bank is

satisfied about the identity of the payee.

8

9. Open Cheque

• When a cheque is not crossed, it is known as an “Open Cheque”

or an “Uncrossed Cheque”.

• These cheques may be cashed at any bank and the payment of

these cheques can be obtained at the counter of the bank or

transferred to the bank account of the bearer.

• An open cheque may be a bearer cheque or an order cheque.

10. Bearer Cheque

• The words “or bearer” printed on the cheque, & it is not cancelled,

then the cheque is called a bearer cheque.

• A bearer cheque is made payable to the bearer i.e. it is payable to

the person who presents it to the bank for encashment.

• In simple words a cheque which is payable to any person

who presents it for payment at the bank counter is called

‘Bearer cheque’

11.

12. Order Cheque

• The word "or order" is written on the face of the cheque, the

cheque is called an order cheque.

• Such a cheque is payable to the person specified therein as the

payee, or to any one else to whom it is endorsed (transferred).

13.

14. Crossed Cheque

• Crossed cheque means drawing two parallel lines on the left

corner of the cheque with or without additional words like

“Account Payee Only” or “Not Negotiable”.

• A crossed cheque cannot be en-cashed at the cash counter of a

bank but it can only be credited to the payee’s account. This is a

safer way of transferring money then an Uncrossed or open

cheque.

15.

16. 2)CROSSED CHEQUES

• If a cheque is crossed by drawing two parallel lines

across the face of the cheque, with or without the words

and Co or A/c payee only, it is called a crossed cheque.

• The crossed cheque cannot be paid on the counter of the

drawee bank.

• It will be deposited in the account of a person in whose

order or favor it is drawn.

16

18. 1) General crossing

• The drawing up of two simple parallel lines on the face of the cheque at

the top left hand corner with or without the words & Co. Not negotiable

or Account Payee only is known as general crossing.

• The effect of general crossing is that the crossed cheque cannot be paid at

the counter of the bank. Its payment can only be deposited into the

payee’s account only.

18

19. 1) General crossing

• Generally, cheques are crossed when

• There are two transverse parallel lines, marked across its face or

• The cheque bears an abbreviation "& Co. "between the two

parallel lines or

• The cheque bears the words "Not Negotiable" between the two

parallel lines or

• The cheque bears the words "A/c. Payee" between the two

parallel lines.

• A crossed cheque can be made bearer cheque by cancelling the

crossing and writing that the crossing is cancelled and affixing the

full signature of drawer.

• 19

20. 2)Special crossing

• A cheque is deemed to be crossed especially when it

bears across its face the name of the banker either with

or without the words ‘Not Negotiable’.

• In case of special crossing the payment can only be

made to the bank named therein the cheque.

20

21. • NOT NEGOTIABLE

• Transferee can’tget better title than transferor –

Normal principle is that a person cannot transfer better title

to property that he himself has.

• For example, if a person steals a car and sells the same,

the buyer does not get any legal title to the car as the

transferor himself had no title to the car. The real owner of

car can anytime obtain possession from the buyer, even if

the buyer had purchased the car in good faith and even if

he had no idea that the seller had no title to the car.

22. Objectives of crossing

• It prevents the payment of the cheque to a wrongful

holder.

• It ensures safe payment..

• It facilitates in tracing the recipient of the payment..

• Further it is a guard against any cheating or theft.

22

23. Anti-Dated Cheque

• Cheque in which the drawer mentions the date earlier than the date

on which it is presented to the bank, it is called as “anti-dated

cheque”.

• Such a cheque is valid upto six months from the date of the

cheque drawn.

24. Post-Dated Cheque

• Cheque on which drawer mentions a date which is yet to come

(future date) to the date on which it is presented, is called post-

dated cheque.

• For example

– If a cheque presented on 10th Jan 2012 bears a date of 25th Jan 2012, it

is a post-dated cheque. The bank will make payment only on or after

25th Jan 2012.

25. Stale Cheque

• If a cheque is presented for payment after six months from the

date of the cheque, it is called stale cheque. After expiry of that

period, no payment will be made by banks against that cheque.

• A stale cheque is not honored by the bank.

26. Mutilated Cheque

• When a cheque is torn into two or more pieces and presented for

payment, such a cheque is called a mutilated cheque. The bank

will not make payment against such a cheque without getting

confirmation of the drawer.

27. Crossing of Cheque

• Crossing of a cheque means "Drawing Two Parallel Lines" across

the face of the cheque. Thus, crossing is necessary in order to have

safety.

• Crossed cheques must be presented through the bank only because

they are not paid at the counter.

• Crossing is a popular device for protecting the drawer and payee

of a cheque.

• Types of Crossing :-

1. General Crossing

2. Special or Restrictive Crossing

28. General Crossing

• There are two transverse parallel lines, marked across its face, or

– The cheque bears an abbreviation "& Co. "between the two parallel

lines, or

– The cheque bears the words "Not Negotiable" between the two parallel

lines, or

– The cheque bears the words "A/c. Payee" between the two parallel lines.

29. Special or Restrictive Crossing

• Crossing is that the bank makes payment only to the banker

whose name is written in the crossing. Specially crossed

cheques are more safe than a generally crossed cheques.

30. Material Alteration

• Any alteration made in the cheque is Material Alteration.

• These cheque are not honored by Banks, for making This as a

valid cheque then the drawer has to sign at every correction made.

• Alterations' Like:

– Date,

– Amount,

– Payee Name,

– Converting order into bearer cheque, etc.

32. Endorsement

• Signature included on the front or back of a check acknowledging

that both parties have agreed to exchange the specified amount on

the document.

• The signature or account information included on the back of a

check acknowledges that the intended recipient received the

document and deposited it.

• To cash a cheque, the issuer and the recipient must endorse the

document.

• Negotiation of an instrument is the process by which the

ownership is transferred from 1 person to another person.

33. Contd…

• There are 2 parties in Endorsement

– Endorser

– Endorsee

• Endorser

– The Person who signs the instrument with an instrument of

transferring his ownership.

• Endorsee

– The person in who’s favor the instrument is transferred.