Energy & Commodities, No. 10 - December 14, 2011

•

0 likes•259 views

Energy & Commodities, No. 10 - December 14, 2011

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (7)

Similar to Energy & Commodities, No. 10 - December 14, 2011

Similar to Energy & Commodities, No. 10 - December 14, 2011 (18)

More from Swedbank

More from Swedbank (20)

Recently uploaded

Recently uploaded (20)

Energy & Commodities, No. 10 - December 14, 2011

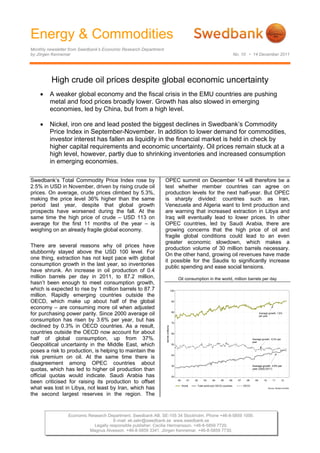

- 1. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department by Jörgen Kennemar No. 10 • 14 December 2011 High crude oil prices despite global economic uncertainty A weaker global economy and the fiscal crisis in the EMU countries are pushing metal and food prices broadly lower. Growth has also slowed in emerging economies, led by China, but from a high level. Nickel, iron ore and lead posted the biggest declines in Swedbank’s Commodity Price Index in September-November. In addition to lower demand for commodities, investor interest has fallen as liquidity in the financial market is held in check by higher capital requirements and economic uncertainty. Oil prices remain stuck at a high level, however, partly due to shrinking inventories and increased consumption in emerging economies. Swedbank’s Total Commodity Price Index rose by OPEC summit on December 14 will therefore be a 2.5% in USD in November, driven by rising crude oil test whether member countries can agree on prices. On average, crude prices climbed by 5.3%, production levels for the next half-year. But OPEC making the price level 36% higher than the same is sharply divided: countries such as Iran, period last year, despite that global growth Venezuela and Algeria want to limit production and prospects have worsened during the fall. At the are warning that increased extraction in Libya and same time the high price of crude – USD 113 on Iraq will eventually lead to lower prices. In other average for the first 11 months of the year – is OPEC countries, led by Saudi Arabia, there are weighing on an already fragile global economy. growing concerns that the high price of oil and fragile global conditions could lead to an even greater economic slowdown, which makes a There are several reasons why oil prices have production volume of 30 million barrels necessary. stubbornly stayed above the USD 100 level. For On the other hand, growing oil revenues have made one thing, extraction has not kept pace with global it possible for the Saudis to significantly increase consumption growth in the last year, so inventories public spending and ease social tensions. have shrunk. An increase in oil production of 0.4 million barrels per day in 2011, to 87.2 million, Oil consumption in the world, million barrels per day hasn’t been enough to meet consumption growth, which is expected to rise by 1 million barrels to 87.7 million. Rapidly emerging countries outside the OECD, which make up about half of the global economy – are consuming more oil when adjusted for purchasing power parity. Since 2000 average oil consumption has risen by 3.6% per year, but has declined by 0.3% in OECD countries. As a result, countries outside the OECD now account for about half of global consumption, up from 37%. Geopolitical uncertainty in the Middle East, which poses a risk to production, is helping to maintain the risk premium on oil. At the same time there is disagreement among OPEC countries about quotas, which has led to higher oil production than official quotas would indicate. Saudi Arabia has been criticised for raising its production to offset what was lost in Libya, not least by Iran, which has the second largest reserves in the region. The Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000. E-mail: ek.sekr@swedbank.se www.swedbank.se Legally responsible publisher: Cecilia Hermansson. +46-8-5859 7720. Magnus Alvesson. +46-8-5859 3341. Jörgen Kennemar. +46-8-5859 7730.

- 2. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department, continued No. 10 • 14 December 2011 Substantially lower capacity utilisation at Japan’s conditions are not as tight as for crude, especially nuclear power plants after the tremendous damage now that the impact of last year's major flooding in caused by last spring’s earthquake has led to higher Australia, one of the world's largest coal producers, oil consumption. Before the earthquake nuclear has faded. Still, higher long-term energy power accounted for 30% of the country's total consumption in emerging economies, where coal energy production, and was expected to rise to 40% still represents a significant share of energy by 2017. Lower nuclear power production should production, points to strong underlying demand for also have an effect on the price of oil, especially coal and upward pressure on prices. since Japan is the world's second largest consumer after the US. In the wake of the nuclear disaster in Fukushima, safety requirements have been Excluding energy commodities, Swedbank’s tightened around the world at the same time that Commodity Price Index fell by 4.6%, marking the seventh consecutive month the index has fallen and several older nuclear power plants have been shut down. Despite that global nuclear power production the first time it is lower than the same month last fell in 2011 to 366 gigawatts (GW), it is still year. The price drop for non-ferrous metals continued in November (1.9% in USD), but at a expected to account for a growing share of electricity production in coming decades. slower rate than the last two months. Prices rose for zinc, copper and lead after declining since last summer. The price of nickel fell during last month, Trading in oil contracts for delivery in late 2012 and however, to just under USD 18 000 per ton, the 2013 indicates that crude prices will remain high lowest level in two years. The price of nickel is despite the possibility of a slight decline on the trending lower at the same time that iron ore and market. At the time of writing the price of crude for steel prices are also falling in pace with weaker delivery at the end of next year was USD 106 per industrial activity. The latter noted the largest price barrel, but it is expected to fall to just over USD 100 drop between October November, by 7.2% in USD. by the end of 2013. Prices could quickly move, This means that iron ore and scrap prices have lost however, if real economic conditions change nearly 20% in the last three months. This is a bigger significantly, as they did during the second half of drop than for industrial metals that are priced daily 2008. The slowdown in the Brazilian economy on the global financial markets, which is probably during the third quarter and in several Asian due more to speculative flows than in the case of countries shows that emerging economies are iron ore and steel. being affected by weaker demand from mature industrial countries. Swedbank’s Commodity Price Index, USD World crude oil stocks Declining indicators for global industrial activity suggest that metal prices will continue lower in coming quarters, especially as the growth rate weakens in the EU with a risk of spreading to The price of coal has dropped in 2011, but from a emerging economies in 2012. Several Asian high level, and since January has given back countries saw their growth rates decline this fall. In 12.6%. From a fundamental perspective, supply China, industrial production rose by 12.4% on an 2 (5)

- 3. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department, continued No. 10 • 14 December 2011 annual basis in November, the lowest increase The price index for food commodities fell by 2.3% in since 2009. At the same time Chinese housing USD in November, which means prices have fallen prices have eased off significantly. cumulatively by nearly 12% in the last three-month period (September-November). Lower imbalances thanks to higher food production, which is expected Since last summer global pulp prices have trended to exceed global demand, are contributing to till lower, falling in November by an average of 4.6% in lower food prices. The UN’s Food and Agriculture USD or 3.3% in SEK. A weaker global economy, Organization (FAO) estimates that grain production falling prices and profit pressures have led to will grow in volume by 3.7% in 2011, compared with production cutbacks in the forestry industry. Pulp a consumption increase of just under 2%. As a futures point to a further price decline in coming result, inventories have improved after having quarters. Among agricultural commodities, cotton shrunk in 2010. Volatility in food prices suggests has seen the biggest price change in the last year, considerable price sensitivity, however, in the event driven by both fundamental factors and speculation. of production disruptions or changes in the global The price of cotton has been nearly cut in half since economy. The financial crisis in the EMU, which last spring, when it reached record-high levels and carries the risk of spreading to the global financial a shortage was apparent. Conditions changed markets and hurting growth, is also driving food during the summer and fall. In addition to increased prices downward. Lower food prices this past fall supplies, prices have been hurt by lower investor are expected to ease inflation pressures, especially interest due to growing concerns about the fiscal in countries where food commodities weigh heavily crisis in the EMU and its effect on the global in the consumer price index. financial market. Pulp and cotton prices in USD, monthly averages Jörgen Kennemar 3 (5)

- 4. Energy & Commodities Monthly newsletter from Swedbank’s Economic Research Department by Jörgen Kennemar No. 10 • 14 December 2011 Swedbank Commodity Index - US$ - Swedbank Commodity Index - SKr - Basis 2000 = 1oo 14-12-11 Basis 2000 = 1oo 14-12-11 9.2011 10.2011 11.2011 9.2011 10.2011 11.2011 T otal index 368,0 356,1 365,0 T otal index 265,6 257,4 267,4 Per cent change month ago 6,1 -3,2 2,5 Per cent change month ago 10,1 -3,1 3,9 Per cent change year ago 34,7 23,5 22,8 Per cent change year ago 26,9 23,2 21,4 T otal index exclusive energy 308,4 282,5 269,5 T otal index exclusive energy 222,6 204,2 197,4 Per cent change month ago -2,6 -8,4 -4,6 Per cent change month ago 1,0 -8,3 -3,3 Per cent change year ago 12,6 1,1 -5,0 Per cent change year ago 6,1 0,8 -6,2 Food, tropical beverages 298,3 275,0 268,6 Food, tropical beverages 215,3 198,8 196,8 Per cent change month ago -1,6 -7,8 -2,3 Per cent change month ago 2,1 -7,7 -1,0 Per cent change year ago 21,3 7,1 -0,6 Per cent change year ago 14,3 6,8 -1,7 Cereals 306,1 281,8 277,2 Cereals 220,9 203,7 203,1 Per cent change month ago -1,0 -7,9 -1,6 Per cent change month ago 2,7 -7,8 -0,3 Per cent change year ago 27,5 11,6 7,8 Per cent change year ago 20,1 11,3 6,6 T ropical beverages and tobacco 317,4 293,8 286,5 T ropical beverages and tobacco 229,1 212,4 209,9 Per cent change month ago -1,5 -7,4 -2,5 Per cent change month ago 2,2 -7,3 -1,2 Per cent change year ago 20,0 8,5 0,5 Per cent change year ago 13,1 8,1 -0,7 Coffee 212,2 193,3 192,9 Coffee 153,2 139,7 141,3 Per cent change month ago 0,4 -8,9 -0,2 Per cent change month ago 4,1 -8,8 1,1 Per cent change year ago 29,7 19,6 10,9 Per cent change year ago 22,2 19,3 9,6 Oilseeds and oil 251,9 229,8 224,2 Oilseeds and oil 181,8 166,1 164,3 Per cent change month ago -2,3 -8,8 -2,4 Per cent change month ago 1,4 -8,6 -1,1 Per cent change year ago 20,1 0,5 -8,9 Per cent change year ago 13,1 0,2 -10,0 Industrial raw materials 311,3 284,6 269,8 Industrial raw materials 224,7 205,7 197,6 Per cent change month ago -2,9 -8,6 -5,2 Per cent change month ago 0,8 -8,4 -3,9 Per cent change year ago 10,5 -0,5 -6,3 Per cent change year ago 4,0 -0,8 -7,4 Agricultural raw materials 195,6 186,9 173,7 Agricultural raw materials 141,2 135,1 127,3 Per cent change month ago -3,1 -4,4 -7,1 Per cent change month ago 0,6 -4,3 -5,8 Per cent change year ago 11,8 0,6 -8,9 Per cent change year ago 5,3 0,3 -10,0 Cotton 105,3 101,2 96,2 Cotton 76,0 73,2 70,5 Per cent change month ago 1,6 -3,9 -4,9 Per cent change month ago 5,5 -3,7 -3,7 Per cent change year ago 8,8 -10,0 -27,1 Per cent change year ago 2,5 -10,3 -28,0 Softwood 148,6 144,7 138,3 Softwood 107,3 104,6 101,3 Per cent change month ago -3,4 -2,6 -4,4 Per cent change month ago 0,2 -2,5 -3,1 Per cent change year ago -0,4 -5,7 -7,4 Per cent change year ago -6,2 -6,0 -8,5 W oodpulp 967,2 930,3 887,3 W oodpulp 698,1 672,4 650,0 Per cent change month ago -2,7 -3,8 -4,6 Per cent change month ago 0,9 -3,7 -3,3 Per cent change year ago -0,5 -3,7 -7,3 Per cent change year ago -6,3 -4,0 -8,4 Non-ferrous metals 257,2 236,7 232,3 Non-ferrous metals 185,6 171,1 170,2 Per cent change month ago -6,0 -8,0 -1,9 Per cent change month ago -2,4 -7,8 -0,5 Per cent change year ago 5,5 -10,2 -12,0 Per cent change year ago -0,7 -10,5 -13,0 Copper 8314,3 7370,9 7551,4 Copper 6000,8 5327,9 5532,2 Per cent change month ago -8,1 -11,3 2,4 Per cent change month ago -4,6 -11,2 3,8 Per cent change year ago 7,9 -11,1 -10,8 Per cent change year ago 1,6 -11,4 -11,9 Aluminium 2296,3 2174,5 2073,2 Aluminium 1657,3 1571,8 1518,8 Per cent change month ago -3,9 -5,3 -4,7 Per cent change month ago -0,3 -5,2 -3,4 Per cent change year ago 6,2 -7,3 -11,1 Per cent change year ago 0,0 -7,6 -12,2 Lead 2297,9 1946,4 1981,6 Lead 1658,5 1406,9 1451,7 Per cent change month ago -4,5 -15,3 1,8 Per cent change month ago -1,0 -15,2 3,2 Per cent change year ago 5,2 -18,2 -16,6 Per cent change year ago -0,9 -18,4 -17,6 Z inc 2076,4 1859,6 1915,7 Z inc 1498,6 1344,2 1403,5 Per cent change month ago -6,1 -10,4 3,0 Per cent change month ago -2,6 -10,3 4,4 Per cent change year ago -3,5 -21,6 -16,4 Per cent change year ago -9,1 -21,8 -17,4 Nickel 20388,5 18919,9 17879,4 Nickel 14715,2 13675,8 13098,6 Per cent change month ago -7,5 -7,2 -5,5 Per cent change month ago -4,0 -7,1 -4,2 Per cent change year ago -9,9 -20,5 -21,9 Per cent change year ago -15,2 -20,7 -22,9 Iron ore, steel scrap 759,8 669,4 620,9 Iron ore, steel scrap 548,4 483,9 454,9 Per cent change month ago 0,4 -11,9 -7,2 Per cent change month ago 4,1 -11,8 -6,0 Per cent change year ago 14,8 10,6 3,0 Per cent change year ago 8,1 10,3 1,8 Energy raw materials 394,5 388,7 407,4 Energy raw materials 284,7 281,0 298,4 Per cent change month ago 9,5 -1,4 4,8 Per cent change month ago 13,6 -1,3 6,2 Per cent change year ago 44,6 33,1 34,4 Per cent change year ago 36,2 32,7 32,8 Coking coal 465,7 448,9 428,4 Coking coal 336,1 324,5 313,8 Per cent change month ago 1,0 -3,6 -4,6 Per cent change month ago 4,8 -3,5 -3,3 Per cent change year ago 31,3 21,6 5,3 Per cent change year ago 23,6 21,2 4,1 Crude oil 391,2 386,0 406,4 Crude oil 282,3 279,0 297,7 Per cent change month ago 10,0 -1,3 5,3 Per cent change month ago 14,1 -1,2 6,7 Per cent change year ago 45,4 33,7 36,2 Per cent change year ago 36,9 33,3 34,6 Source : SW EDBANK and HW W A-Institute for Economic Research Hamburg Source : SW EDBANK and HW W A-Institute for Economic Research Hamburg Swedbank Economic Research Department Swedbank’s monthly Energy & Commodities newsletter is published as a service to our customers. We believe that we have used reliable sources and methods in the preparation SE-105 34 Stockholm, Sweden of the analyses reported in this publication. However, we cannot guarantee the accuracy or Phone +46-8-5859 7740 completeness of the report and cannot be held responsible for any error or omission in the ek.sekr@swedbank.se underlying material or its use. Readers are encouraged to base any (investment) decisions www.swedbank.se on other material as well. Neither Swedbank nor its employees may be held responsible for Legally responsible publisher losses or damages, direct or indirect, owing to any errors or omissions in Swedbank’s Cecilia Hermansson, +46-88-5859 7720 monthly Energy & Commodities newsletter. Magnus Alvesson, +46-8-5859 3341 Jörgen Kennemar, +46-8-5859 7730 Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000. E-mail: ek.sekr@swedbank.se www.swedbank.se Legally responsible publisher: Cecilia Hermansson. +46-8-5859 7720. Magnus Alvesson. +46-8-5859 3341. Jörgen Kennemar. +46-8-5859 7730.