Social security state taxation map

•

1 like•130 views

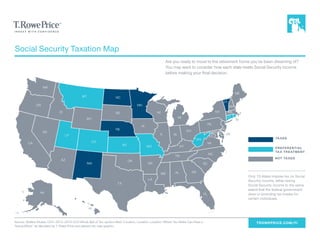

Are you ready to move to the retirement home you've been dreaming of? You may want to consider how each state treats Social Security income before making your final decision.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (18)

Similar to Social security state taxation map

Similar to Social security state taxation map (20)

Recently uploaded

Recently uploaded (20)

Social security state taxation map

- 1. TROWEPRICE.COM/FI CT RI NJ MD DE ME NH VT NY PA WV DC VA NC SC TN KY OH MA IN MI WI IL GAALMS FL LA AR OK TX MOKS IA MN ND SD NE CO UT WY MT ID NM AZ CA NV OR WA AK HI Are you ready to move to the retirement home you’ve been dreaming of? You may want to consider how each state treats Social Security income before making your final decision. Social Security Taxation Map NOT TAXED TAXED PREFERENTIAL TAX TREATMENT Only 13 states impose tax on Social Security income, either taxing Social Security income to the same extent that the federal government does or providing tax breaks for certain individuals. Source: Wolters Kluwer, CCH: 2013–2013 CCH Whole Ball of Tax, section titled “Location, Location, Location: Where You Retire Can Have a Taxing Effect,” as tabulated by T. Rowe Price and placed into map graphic.

- 2. State Tax Treatment of Social Security Income TROWEPRICE.COM/FI The following CCH analysis provides a general overview of how states treat income from Social Security and pensions. Source: Wolters Kluwer, CCH: 2013. STATE SOCIAL SECURITY INCOME Alabama State computation not based on federal. Social Security benefits excluded from taxable income. Alaska No individual income tax. Arizona Social Security benefits subtracted from federal AGI. Arkansas State computation not based on federal. Social Security benefits excluded from taxable income. California Social Security benefits subtracted from federal AGI. Colorado Pension income, including Social Security benefits, up to $24,000 may be subtracted from federal taxable income by those 65 and older, and up to $20,000 by those 55 and older or those who are second-party beneficiaries of someone 55 or older. Connecticut Joint filers and heads of households with AGIs under $60,000 and individuals with AGIs under $50,000 deduct from federal AGI all Social Security income included for federal income tax purposes. Joint filers and heads of house- holds with AGIs over $60,000 and individuals with AGIs over $50,000 deduct the difference between the amount of Social Security benefits included for federal income tax purposes and the lesser of 25% of Social Security benefits received or 25% of the excess of the taxpayer’s provisional income in excess of the specified base amount under IRC Sec. 86(b)(1). Delaware Social Security benefits subtracted from federal AGI. District of Columbia Social Security benefits subtracted from federal AGI. Florida No individual income tax. Georgia Social Security benefits subtracted from federal AGI. Hawaii Social Security benefits subtracted from federal AGI. Idaho Social Security benefits subtracted from federal AGI. Illinois Social Security benefits subtracted from federal AGI. Indiana Social Security benefits subtracted from federal AGI. Iowa For tax years after 2013, Social Security benefits are fully exempt. Kansas For 2012 and thereafter, taxpayers with a federal AGI of $50,000 or less are exempt from any state tax on their Social Security benefits. Kentucky Social Security benefits subtracted from federal AGI. Louisiana Social Security benefits subtracted from federal AGI. Maine Social Security benefits subtracted from federal AGI. Maryland Social Security benefits subtracted from federal AGI. Massachusetts Social Security benefits subtracted from federal AGI. Michigan Social Security benefits subtracted from federal AGI. Minnesota State computation begins with federal taxable income. No subtraction. STATE SOCIAL SECURITY INCOME Mississippi State computation not based on federal. Social Security benefits exempt in total. Missouri Social Security benefits that are included in federal AGI may be subtracted. The maximum amount of benefits that may be deducted is 100% for 2012 and after. Married couples with Missouri AGI greater than $100,000 and single individuals with Missouri AGI greater than $85,000 may qualify for a partial deduction. Montana Separate calculation to determine taxable Social Security benefits. Benefits exempt if income is $25,000 or less for single filers or heads of households or $32,000 for married taxpayers filing jointly and $16,000 for married taxpayers filing separately. Nebraska State computation begins with federal AGI. No subtraction. Nevada No individual income tax. New Hampshire Only dividends and interest are taxable. New Jersey State computation not based on federal. All Social Security benefits are excluded by statute from gross income. New Mexico State computation begins with federal AGI. No subtraction. New York Social Security benefits subtracted from federal AGI. North Carolina Social Security benefits subtracted from federal taxable income. North Dakota State computation begins with federal taxable income. No subtraction. Ohio Social Security benefits subtracted from federal AGI. Oklahoma Social Security benefits subtracted from federal AGI. Oregon Social Security benefits subtracted from federal taxable income. Pennsylvania State computation not based on federal. Social Security benefits not included in state taxable income. Rhode Island Beginning in 2016, Social Security benefits are not taxed if federal AGI is less than $110,000 for a married individual filing jointly or a qualifying widow(er), or less than $80,000 for other filers. South Carolina Social Security benefits subtracted from federal taxable income. South Dakota No individual income tax. Tennessee Only dividends and interest are taxable. Texas No individual income tax. Utah State computation begins with federal taxable income. No subtraction. Vermont State computation begins with federal taxable income. No subtraction. Virginia Social Security benefits subtracted from federal AGI. Washington No individual income tax. West Virginia State computation begins with federal AGI. No subtraction. Wisconsin Full exclusion effective beginning in tax year 2008. Wyoming No individual income tax. T. Rowe Price Investment Services, Inc. C7D6LEPNV E02-329 2016-US-18748 2/16