QNBFS Daily Market Report October 16, 2018

•

0 likes•37 views

The document provides an intra-day market summary and commentary on the Qatari and broader GCC stock markets. It notes that the QSE Index rose 0.1% led by gains in the industrial and consumer goods indices. Mazaya Qatar Real Estate Development and Alijarah Holding were the top gainers rising 10% and 5.1% respectively. It also provides commentary on price movements and trading volumes in other GCC markets such as Saudi Arabia, Dubai, Abu Dhabi, Kuwait, Oman, and Bahrain.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report October 16, 2018

Similar to QNBFS Daily Market Report October 16, 2018 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report October 16, 2018

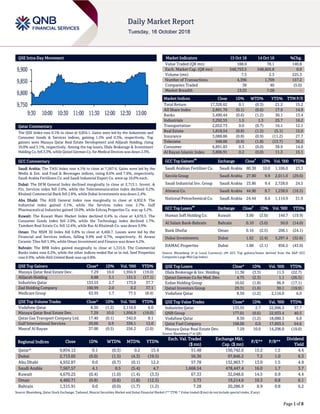

- 1. Page 1 of 8 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.1% to close at 9,834.1. Gains were led by the Industrials and Consumer Goods & Services indices, gaining 1.5% and 0.3%, respectively. Top gainers were Mazaya Qatar Real Estate Development and Alijarah Holding, rising 10.0% and 5.1%, respectively. Among the top losers, Dlala Brokerage & Investment Holding Co. fell 3.3%, while Qatari German Co. for Medical Devices was down 2.3%. GCC Commentary Saudi Arabia: The TASI Index rose 4.1% to close at 7,567.6. Gains were led by the Media & Ent. and Food & Beverages indices, rising 8.6% and 7.6%, respectively. Saudi Arabia Fertilizers Co. and Saudi Industrial Export Co. were up 10.0% each. Dubai: The DFM General Index declined marginally to close at 2,713.1. Invest. & Fin. Services index fell 2.0%, while the Telecommunication index declined 0.2%. Khaleeji Commercial Bank fell 2.8%, while Dubai Investments was down 2.4%. Abu Dhabi: The ADX General Index rose marginally to close at 4,932.9. The Industrial index gained 5.1%, while the Services index rose 2.7%. Gulf Pharmaceutical Industries gained 10.0%, while Eshraq Properties Co. was up 5.2%. Kuwait: The Kuwait Main Market Index declined 0.4% to close at 4,670.3. The Consumer Goods index fell 2.0%, while the Technology index declined 1.7%. Tamdeen Real Estate Co. fell 12.6%, while Ras Al Khaimah Co. was down 9.9%. Oman: The MSM 30 Index fell 0.8% to close at 4,460.7. Losses were led by the Financial and Services indices, falling 0.9% and 0.7%, respectively. Al Anwar Ceramic Tiles fell 5.9%, while Oman Investment and Finance was down 4.2%. Bahrain: The BHB Index gained marginally to close at 1,315.9. The Commercial Banks index rose 0.2%, while the other indices ended flat or in red. Seef Properties rose 0.9%, while Ahli United Bank was up 0.8%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 7.29 10.0 1,956.9 (19.0) Alijarah Holding 8.88 5.1 151.5 (17.1) Industries Qatar 133.55 2.7 173.9 37.7 Zad Holding Company 100.99 2.0 0.2 37.1 Medicare Group 63.95 1.7 77.5 (8.4) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 8.50 (1.2) 2,116.0 6.0 Mazaya Qatar Real Estate Dev. 7.29 10.0 1,956.9 (19.0) Qatar Gas Transport Company Ltd. 17.40 (0.1) 342.0 8.1 Gulf International Services 20.00 0.9 336.1 13.0 Masraf Al Rayan 37.00 (0.5) 256.2 (2.0) Market Indicators 15 Oct 18 14 Oct 18 %Chg. Value Traded (QR mn) 188.0 78.1 140.8 Exch. Market Cap. (QR mn) 548,753.5 548,605.8 0.0 Volume (mn) 7.5 2.3 225.3 Number of Transactions 4,396 1,709 157.2 Companies Traded 38 40 (5.0) Market Breadth 13:23 7:28 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 17,326.62 0.1 (0.3) 21.2 15.2 All Share Index 2,891.70 (0.1) (0.6) 17.9 14.9 Banks 3,490.44 (0.6) (1.2) 30.1 13.4 Industrials 3,292.55 1.5 1.3 25.7 16.2 Transportation 2,052.73 0.0 (0.7) 16.1 12.1 Real Estate 1,818.54 (0.8) (1.5) (5.1) 15.0 Insurance 3,088.86 (0.8) (0.9) (11.2) 27.7 Telecoms 948.06 (0.9) (1.8) (13.7) 36.2 Consumer 6,891.83 0.3 (0.0) 38.9 14.0 Al Rayan Islamic Index 3,806.91 0.2 (0.0) 11.3 15.1 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Saudi Arabian Fertilizer Co. Saudi Arabia 80.30 10.0 1,106.0 23.3 Savola Group Saudi Arabia 27.80 9.9 2,011.0 (29.6) Saudi Industrial Inv. Group Saudi Arabia 23.86 9.4 2,728.0 24.5 Almarai Co. Saudi Arabia 44.90 8.7 1,238.0 (16.5) National Petrochemical Co. Saudi Arabia 24.44 8.6 1,114.9 31.9 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Human Soft Holding Co. Kuwait 3.00 (3.0) 149.7 (19.9) Al Salam Bank-Bahrain Bahrain 0.10 (3.0) 50.0 (14.0) Bank Dhofar Oman 0.16 (2.5) 206.1 (24.1) Dubai Investments Dubai 1.62 (2.4) 5,297.4 (32.8) DAMAC Properties Dubai 1.88 (2.1) 856.5 (43.0) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Dlala Brokerage & Inv. Holding 11.36 (3.3) 11.5 (22.7) Qatari German Co for Med. Dev. 4.75 (2.3) 1.1 (26.5) Ezdan Holding Group 10.02 (1.8) 96.9 (17.1) Qatari Investors Group 29.31 (1.6) 30.1 (19.9) Vodafone Qatar 8.50 (1.2) 2,116.0 6.0 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Industries Qatar 133.55 2.7 22,996.5 37.7 QNB Group 177.01 (0.6) 22,933.4 40.5 Vodafone Qatar 8.50 (1.2) 18,080.3 6.0 Qatar Fuel Company 168.00 0.0 17,603.5 64.6 Mazaya Qatar Real Estate Dev. 7.29 10.0 14,206.0 (19.0) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,834.12 0.1 (0.3) 0.2 15.4 51.48 150,742.6 15.2 1.5 4.4 Dubai 2,713.05 (0.0) (1.5) (4.3) (19.5) 56.36 97,846.2 7.2 1.0 6.3 Abu Dhabi 4,932.87 0.0 (0.7) (0.1) 12.2 57.78 132,963.7 13.0 1.5 4.9 Saudi Arabia 7,567.57 4.1 0.5 (5.4) 4.7 1,668.54 478,447.4 16.0 1.7 3.7 Kuwait 4,670.25 (0.4) (1.0) (1.4) (3.3) 67.33 32,048.0 14.5 0.9 4.4 Oman 4,460.71 (0.8) (0.6) (1.8) (12.5) 5.73 19,214.6 10.3 0.8 6.1 Bahrain 1,315.91 0.0 (0.0) (1.7) (1.2) 7.28 20,286.9 8.9 0.8 6.2 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,750 9,800 9,850 9,900 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QSE Index rose 0.1% to close at 9,834.1. The Industrials and Consumer Goods & Services indices led the gains. The index rose on the back of buying support from Qatari and GCC shareholders despite selling pressure from non-Qatari shareholders. Mazaya Qatar Real Estate Development and Alijarah Holding were the top gainers, rising 10.0% and 5.1%, respectively. Among the top losers, Dlala Brokerage & Investment Holding Company fell 3.3%, while Qatari German Company for Medical Devices was down 2.3%. Volume of shares traded on Monday rose by 225.3% to 7.5mn from 2.3mn on Sunday. Further, as compared to the 30-day moving average of 5.8mn, volume for the day was 29.5% higher. Vodafone Qatar and Mazaya Qatar Real Estate Development were the most active stocks, contributing 28.1% and 26.0% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 3Q2018 % Change YoY Operating Profit (mn) 3Q2018 % Change YoY Net Profit (mn) 3Q2018 % Change YoY Al Batinah Power* Oman OMR 61.0 -0.4% – – 11.4 50.6% Al Suwadi Power* Oman OMR 63.1 3.0% – – 11.5 30.7% Al Hassan Engineering* Oman OMR 18.7 -30.5% – – -3.4 N/A United Power* Oman OMR 4.2 -1.5% – – 0.3 -42.8% Muscat Insurance* Oman OMR 15.6 1.7% – – 879.7 -3.2% Al Ahlia Insurance* Oman OMR 20.0 -1.0% – – 3.0 3.9% United Finance* Oman OMR 7.4 -10.8% – – 0.3 -80.0% Galfar Engineering and Con.* Oman OMR 214.2 -3.3% – – 2.3 N/A SMN Power Holding* Oman OMR 79.2 8.6% – – 6.5 36.2% Al Anwar Holding**6M Oman OMR 0.4 -30.6% – – -0.1 N/A Oman Chlorine* Oman OMR 9.1 77.0% 1.9 136.0% 1.1 34.0% Al Madina Takaful* Oman OMR – – – – 2.2 32.8% Al Fajar Al Alamia* Oman OMR 5.4 18.4% – – 0.5 46.9% Muscat Thread Mills*# Oman OMR 2,210.5 0.8% – – -8.7 N/A Sharqiyah Desalination* Oman OMR 11.3 12.0% – – 0.8 N/A Al Jazeera Steel Products* Oman OMR 91.8 42.5% – – 2.7 2.0% Abrasives Manufacturing*# Oman OMR 45.6 412.7% – – -182.2 N/A Gulf Stone Company* Oman OMR 2.5 -2.0% – – -0.1 #DIV/0! Dhofar Generating Company* Oman OMR 30.2 146.3% – – 0.8 N/A Oman and Emirates Inv. Holding* Oman OMR 4.5 217.8% – – 1.7 N/A Ominvest* Oman OMR 203.0 15.1% – – 19.8 25.3% Oman Investment and Finance* Oman OMR 15.1 -8.2% – – 0.7 -62.0% National Aluminium Products* Oman OMR 36.2 50.8% – – 0.8 N/A National Finance* Oman OMR 31.6 - – – 9.5 #DIV/0! Almaha Petroleum Products Mar.* Oman OMR 364.1 15.0% – – 4.7 15.6% Construction Materials Ind.* Oman OMR 2.7 11.4% – – 0.1 N/A Shell Oman Marketing* Oman OMR 397.7 14.9% – – 9.1 -16.7% Arabia Falcon Insurance* Oman OMR 12.6 -0.1% – – 0.5 238.1% Majan Glass* Oman OMR 6.2 18.0% – – -1.4 N/A Sweets of Oman* Oman OMR 9.8 -5.2% – – -0.2 N/A National Detergent* Oman OMR 17.4 2.7% – – 0.9 22.8% Almaha Ceramics* Oman OMR 6.4 -1.6% – – 1.0 -20.1% Al Omaniya Financial Ser.* Oman OMR 13.3 -10.6% – – 3.0 -14.8% Al Jazeera Services* Oman OMR 5.5 -10.0% – – -1.2 N/A Sohar Power* Oman OMR 50.2 4.5% – – 3.9 353.0% Taageer Finance* Oman OMR 11.8 7.0% – – 1.7 -45.9% Dhofar Insurance* Oman OMR 33.0 -8.4% – – 2.0 N/A Oman Qatar Insurance Co.* Oman OMR 25.0 29.7% – – 1.3 -16.8% Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 30.24% 37.87% (14,360,930.87) Qatari Institutions 20.10% 12.32% 14,614,013.81 Qatari 50.34% 50.19% 253,082.94 GCC Individuals 0.35% 1.22% (1,634,320.55) GCC Institutions 10.21% 5.41% 9,023,761.62 GCC 10.56% 6.63% 7,389,441.07 Non-Qatari Individuals 12.21% 10.20% 3,785,296.78 Non-Qatari Institutions 26.89% 32.97% (11,427,820.79) Non-Qatari 39.10% 43.17% (7,642,524.01)

- 3. Page 3 of 8 National Mineral Water* Oman OMR 6.1 4.1% – – 0.3 N/A Ooredoo Oman* Oman OMR 211.9 3.7% – – 26.8 16.0% Vision Insurance* Oman OMR 20.4 16.6% – – 1.5 4.0% Global Financial Investment* Oman OMR 12.4 2.4% – – 0.8 290.7% Oman National Engine. Invt.* Oman OMR 31.7 -14.4% – – 0.9 -49.3% Source: Company data, DFM, ADX, MSM, TASI, BHB. (*Financials for 9M2018, **Financials for 6M2018-19, # Values in ‘000) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 10/15 Japan Ministry of Economy Trade and Industry Capacity Utilization MoM August 2.2% – -0.6% 10/15 Japan Ministry of Economy Trade and Industry Industrial Production MoM August 0.2% – 0.7% 10/15 Japan Ministry of Economy Trade and Industry Industrial Production YoY August 0.2% – 0.6% 10/15 India Directorate General of Commerce Exports YoY September -2.1% – 19.2% 10/15 India Directorate General of Commerce Imports YoY September 10.5% – 25.4% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 3Q2018 results No. of days remaining Status MCGS Medicare Group 16-Oct-18 0 Due WDAM Widam Food Company 17-Oct-18 1 Due QNCD Qatar National Cement Company 17-Oct-18 1 Due QEWS Qatar Electricity & Water Company 17-Oct-18 1 Due QIBK Qatar Islamic Bank 17-Oct-18 1 Due DHBK Doha Bank 17-Oct-18 1 Due UDCD United Development Company 17-Oct-18 1 Due NLCS Alijarah Holding 18-Oct-18 2 Due QISI The Group Islamic Insurance Company 21-Oct-18 5 Due ABQK Ahli Bank 21-Oct-18 5 Due QIGD Qatari Investors Group 21-Oct-18 5 Due GWCS Gulf Warehousing Company 22-Oct-18 6 Due IHGS Islamic Holding Group 22-Oct-18 6 Due VFQS Vodafone Qatar 22-Oct-18 6 Due QATI Qatar Insurance Company 23-Oct-18 7 Due KCBK Al Khalij Commercial Bank 23-Oct-18 7 Due CBQK The Commercial Bank 23-Oct-18 7 Due IQCD Industries Qatar 24-Oct-18 8 Due MRDS Mazaya Qatar Real Estate Development 24-Oct-18 8 Due QCFS Qatar Cinema & Film Distribution Company 25-Oct-18 9 Due QFLS Qatar Fuel Company 25-Oct-18 9 Due QIMD Qatar Industrial Manufacturing Company 25-Oct-18 9 Due IGRD Investment Holding Group 28-Oct-18 12 Due BRES Barwa Real Estate Company 28-Oct-18 12 Due GISS Gulf International Services 28-Oct-18 12 Due QOIS Qatar Oman Investment Company 28-Oct-18 12 Due MERS Al Meera Consumer Goods Company 28-Oct-18 12 Due QGMD Qatari German Company for Medical Devices 28-Oct-18 12 Due AKHI Al Khaleej Takaful Insurance Company 28-Oct-18 12 Due MPHC Mesaieed Petrochemical Holding Company 29-Oct-18 13 Due AHCS Aamal Company 29-Oct-18 13 Due QFBQ Qatar First Bank 29-Oct-18 13 Due SIIS Salam International Investment Limited 29-Oct-18 13 Due QGRI Qatar General Insurance & Reinsurance Company 29-Oct-18 13 Due DOHI Doha Insurance Group 29-Oct-18 13 Due ERES Ezdan Holding Group 29-Oct-18 13 Due QNNS Qatar Navigation (Milaha) 30-Oct-18 14 Due MCCS Mannai Corporation 30-Oct-18 14 Due Source: QSE

- 4. Page 4 of 8 News Qatar MARK's bottom line driven by net reversals YoY and QoQ in 3Q2018, beating our estimate – Masraf Al Rayan's (MARK) net profit rose 4.4% YoY (+5.8% QoQ) to QR566.0mn in 3Q2018, ahead of our estimate of QR536.1mn (variation of +5.6%). The beat was due to MARK booking net reversals. The bank booked net reversals of QR15.1mn vs. net reversals of QR2.8mn in 3Q2017 (net provisions of QR4.9mn in 2Q2018). Total revenue increased by 3.0% YoY on the back of strong fees & commissions and income from associates, while net interest & investment income was flat. EPS increased to QR0.75 in 3Q2018 from QR0.72 in 3Q2017 and QR0.71 in 2Q2018. Net loans grew by 1.9% QoQ (+2.9% YTD) to QR74.2bn while deposits gained by 2.8% QoQ (3.1% YTD) reaching QR64.5bn. Hence, MARK’s LDR remained at 115% vs. 116% in 2Q2018 (115% at the end of 2017). MARK remains cost efficient with C/I ratio of 22.7%. On the profitability indicators, MARK again continued to maintain its ‘leading position’ with return on average assets at 2.15% and return on average equity at 16.72%, despite depositors’ share of profits increasing by 12.9%, due to higher cost profits on deposits at local and international levels. The bank’s capitalization remained strong with common equity tier 1 (CET 1) at 18.18% and total capital adequacy ratio (CAR) at 19.04%, well above the regulatory requirements including all buffers under Basel III and the Qatar Central Bank standards. MARK’s non-performing loans (NPLs) ratio remained at 0.64%, ‘reflecting a very strong and prudent credit risk management policies and procedures.’ MARK’s Chairman and Managing Director, Hussain Al-Abdulla expressed satisfaction over the results, stating that it was within expectations and in line with the positive indicators of the Qatari economy. (QNBFS Research, QSE, Gulf-Times.com) QIIK's bottom line rises 6.9% YoY and 8.8% QoQ in 3Q2018, beating our estimate – Qatar International Islamic Bank's (QIIK) net profit rose 6.9% YoY (+8.8% QoQ) to QR251.2mn in 3Q2018, beating our estimate of QR235.5mn (variation of +6.7%). EPS amounted to QR4.86 in 9M2018 as compared to QR4.63 in 9M2017. In 9M2018, QIIK earned net profit of QR735mn, up 5% on the same period last year. QIIK’s CEO, Abdulbasit Ahmad Al-Shaibei said, “The bank’s total income for the nine months ended on September 30, amounted to QR1,584mn compared to QR1,385mn for the same period in 2017.” He noted that QIIK’s total assets at the end of the third quarter stood at nearly QR49bn, while the financing portfolio exceeded QR28bn. QIIK’s capital adequacy ratio (under Basel III) reached 16.47 % by the end of the third quarter, which confirms the bank's solid position and its ability to cope with the various market risks. The CEO said, “These results clearly indicate that QIIK continues to achieve growth and success, drawing on the strength and resilience of the Qatari economy, which proved its capabilities to ward off its challengers.” (QNBFS Research, QSE, Gulf-Times.com) DBIS reports net loss of QR17.50mn in 3Q2018 – Dlala Brokerage and Investments Holding Co. (DBIS) reported net loss of QR17.50mn in 3Q2018 as compared to net profit of QR3.29mn in 3Q2017 and net profit of QR0.05mn in 2Q2018. Loss per share amounted to QR0.56 in 9M2018 as compared to EPS of QR0.57 in 9M2017. (QSE) Ooredoo to manage ICT services for Doha Bank – Ooredoo has signed a landmark agreement that will see the company deliver end-to-end managed ICT services to Doha Bank. The agreement was signed by the Head of Administration & Property Department at Doha Bank, Ahmad Ali Al-Hanzab, and Ooredoo’s Chief Operating Officer, Yousuf Abdulla Al-Kubaisi. As part of the five-year contract, Ooredoo will guarantee Doha Bank a seamless managed ICT service, encompassing telecommunications, IT networks, cyber-security, and data center solutions. To ensure Doha Bank’s information is secure, the bank will now move both their main and back-up data center to Ooredoo’s world-class Qatar Data Center. Ooredoo will also refresh Doha Bank’s network infrastructure to support the organization’s mission critical operations. (Gulf-Times.com) Qatar Islamic Insurance Company’s EGM endorses the items listed on its agenda – Qatar Islamic Insurance Company announced the results of the EGM, held on October 14, 2018 and the following decisions were approved: i) Approved the Board of Directors' recommendation to change the name of Qatar Islamic Insurance Company to Qatar Islamic Insurance Group and accordingly modify the Articles of Association. ii) Approved the Board of Directors' recommendation to establish real estate company owned 100% by the group. (QSE) MRDS announces the delivery of Sidra residential compound to the Qatar foundation for Education, Science and Community Development – Mazaya Qatar Real Estate Development Company (MRDS) has handed over the Sidra residential compound to the Qatar Foundation for Education, Science and Community Development, as the complex is ready for housing and use of its vital facilities. Sidra residential compound has 1,165 residential units covering an area of 143,000 square meters, developed by MRDS for the Qatar Foundation for Education and Science under Build-Operate-Transfer scheme (BOT), for a period of twenty years. The contract between the two parties stipulates that the rent payment is payable by a six month advance. The delivery is taking place after the completion of MRDS all construction works and finalizing and issuing of official papers and the latest completion certificate of the project after the completion of all the requirements of the project of furnishing and installation of security systems and the appointment of a specialized company to manage and maintain the complex. (QSE) Qatar’s trade volume with Germany and Italy at QR18.97bn – Qatar’s economic and trade cooperation with Germany and Italy is expected to witness a major boost in the coming years. All the stakeholders, including top government officials and business leaders from all these countries are working aggressively to further deepen and expand area of bilateral cooperation. The combined value of Qatar’s trade exchange with these two major European trade partners (Germany and Italy) reached QR18.97bn (or €4.5bn) in 2017, which is expected to witness significant growth in 2018. According to data provided by embassies of both the countries in Qatar, the trade volume between Qatar and Germany amounted to about €2.5bn in 2017, making Germany one of Qatar’s most important trading

- 5. Page 5 of 8 partners. The total value of Qatar-Italy trade exchange stood at €2bn last year. (Peninsula Qatar) Occidental Petroleum confirms it will no longer pursue Qatar contract extension – Occidental Petroleum confirmed it will no longer pursue the extension of the Idd El-Sharghi North Dome (ISND) offshore field in Qatar, which expires in October 2019, after Qatar Petroleum announced takeover of the oil field. (Bloomberg) Astad to support ‘Made in Qatar’ expo – Astad is supporting the ‘Made in Qatar 2018’ Oman edition as ‘Main Project Management Sponsor’, according to Qatar Chamber, which is organizing the event from November 5 to 9, at the Oman Convention & Exhibition Centre. The expo, which will be held for the second time outside Qatar, aims to exchange experiences with Omani companies in the industrial sectors, as well as to introduce Omanis to Qatari products and open up new foreign markets to small and large Qatari companies. (Gulf- Times.com) International Global FDI falls 41% in 1H2018 after Trump tax reforms – Global foreign direct investment (FDI) fell by 41% to $470bn in 1H2018, the lowest since 2005, preliminary figures from the United Nations Conference on Trade and Development (UNCTAD) showed. President Donald Trump’s US tax reforms were the main cause of the slump, which followed a 23% fall in 2017, as American firms repatriated a net $217bn from foreign affiliates, UNCTAD’s Investment Chief, James Zhan said. FDI, comprising cross-border corporate takeovers, intra-company loans and investments in start-up projects abroad, is a bellwether of globalization and a potential sign of growth of corporate supply chains and future trade ties. But it can also go into reverse as companies pull out of foreign projects or repatriate earnings. Such reversals could erode the importance of international supply chains, which became an increasingly important driver of international trade until 2011, and subsequently stagnated, Zhan said. (Reuters) US retail sales increase modestly; consumer spending strong – US retail sales barely rose in September, as a rebound in motor vehicle purchases was offset by the biggest drop in spending at restaurants and bars in nearly two years. However, other details of the report from the Commerce Department were upbeat and suggested that consumer spending ended the third quarter with strong momentum, which should provide a boost to economic growth, despite anticipated drags from weak exports and a struggling housing market. Retail sales edged up 0.1% last month, after a similar gain in August. Economists polled by Reuters had forecasted retail sales increasing 0.6% in September. Retail sales in September rose 4.7% from a year ago. Excluding automobiles, gasoline, building materials and food services, retail sales jumped 0.5% last month after being unchanged in August. These so-called core retail sales correspond most closely with the consumer spending component of GDP. Consumer spending, which accounts for more than two thirds of US economic activity, is being driven by a robust labor market, with the unemployment rate near a 49-year low of 3.7%. Tight labor market conditions are gradually pushing up wage growth. (Reuters) US government posts widest deficit since 2012 – The US government closed the 2018 fiscal year $779bn in the red, its highest deficit in six years, as Republican-led tax cuts pinched revenues and expenses rose on a growing national debt, according to data released by the Treasury Department. New government spending also expanded the federal deficit for the 12 months through September, the first full annual budget on the watch of US President Donald Trump. It was the largest deficit since 2012. The data also showed $119bn budget surplus in September, which was larger than expected and a record for the month. A senior Treasury official said the monthly surplus was smaller, when adjusted for calendar shifts. Economists generally view the corporate and individual tax cuts passed by the Republican-controlled US Congress late last year, and an increase in government spending agreed in early February as likely to balloon the nation’s deficit. Trump and his fellow Republicans have touted the tax cuts as a boost to growth and jobs. (Reuters) EU says banks have big buffer shortfall as market conditions worsen – Eurozone banks have a large shortfall in their loss- absorbing buffers and now face tougher market conditions for building them up due to higher volatility and widening spreads in sovereign yields, the bloc’s banking watchdogs stated. Under international and EU banking rules, large banks must issue special loss-absorbing debt known as TLAC and MREL that can be converted into capital if a crisis burns through their core capital buffer. The shortfall stands at €125bn ($145bn) for the bloc’s 35 most complex banking groups, said Dominique Laboureix, who is a member of the Single Resolution Board, the EU body that handles failing banks and sets the level of loss- absorbing buffers. These buffers are for use when a bank is in trouble. They are seen as crucial to allow an orderly wind-down of a lender, and should also reduce the cost to taxpayers of any banking rescue. (Reuters) Regional UAE, Saudi Arabian banks to benefit from rising interest rates – Banks in the UAE and Saudi Arabia are expected to benefit from the rising interest rates after the recent interest rate hike by the Federal Reserve, according to rating agency Moody’s and independent analysts. Central banks of both countries track US interest rates, as their currencies are pegged to the Dollar. It is important to maintain interest rates at par or in close range with US rates to prevent capital flight in the event of higher rates offered on Dollar deposits. Analysts said banks in the UAE and Saudi Arabia continue to hold significantly large low cost deposits in current and savings accounts, the pricing of which is not hugely impacted by the Fed rate hike because of the comfortable liquidity situation and relatively modest credit growth. On the lending side, banks have more flexibility on the pricing, leading to better yield and net interest margins. (GulfBase.com) SMEs hold key to regional economic growth – As efforts to stimulate economic growth in the Middle East and North Africa (MENA) territory remain on course, focus is now shifting to small and medium enterprise (SMEs) driven strategies in a bid to accelerate growth. This comes on the back of declining oil reserves and revenues, which served as a wake-up call to the MENA governments on over reliance on their energy reserves

- 6. Page 6 of 8 to fuel their respective economies. However, even as regional political and socio-economic realignment continues to take shape, government driven diversification agendas are steadily mainstreaming SMEs and mid market companies as key economic growth drivers. With an estimated value at $1tn, the MENA SME industry has become important in promoting competitiveness, increasing productivity, and most notably the creation of employment opportunities. (GulfBase.com) Saudi Arabia based ICD halts plan for $1bn fund with IL&FS – The Saudi Arabia based Islamic Corporation for the Development of the Private Sector (ICD) stated that it had halted plans for a $1bn fund with Infrastructure Leasing and Financial Services Group (IL&FS) while the Indian firm undergoes a restructuring. The Indian government took control of IL&FS after it defaulted on some of its debt obligations, sparking fears of wider contagion in the country’s financial sector. In January, the ICD signed a shareholder agreement with the private equity arm of IL&FS to launch an Africa focused infrastructure fund with $105mn in seed capital and a target first close by the middle of this year. (Reuters) Saudi Arabia is clouding Masayoshi Son's $100bn vision – Saudi Arabia’s problems are spilling over into tech. Fallout from the disappearance of prominent Saudi Arabian journalist Jamal Khashoggi has hit Japan’s SoftBank, whose $100bn new economy war chest is backed by the Kingdom. Masayoshi Son’s investors are rattled. Certainly, entrepreneurs like Uber’s Dara Khosrowshahi will be wary of accepting fresh Vision Fund investments. New capital will be harder to come by too. (Reuters) Saudi Arabia’s five-year CDS jump to 11-month high on Khashoggi case – The cost of insuring exposure to Saudi Arabia’s sovereign debt jumped to the highest level in 11 months after the Kingdom faced increasing international pressure over missing journalist Jamal Khashoggi. Further, Saudi Arabia’s currency fell to its lowest level in two years and its international bond prices slipped on October 15, 2018 over fears that foreign investment inflows could shrink as Saudi Arabia faces pressure over the disappearance of journalist Jamal Khashoggi. (Reuters) Saudi Arabia to hold investment conference despite key speakers’ pull outs – Saudi Arabia will go ahead with a major investment conference planned later this month despite key speakers and partners pulling out after the disappearance of journalist Jamal Khashoggi, a statement from the organizers stated. “With more than 150 speakers confirmed from over 140 different organizations, including 17 global partner organizations, the FII (Future Investment Initiative) program will closely examine how investment can be used to drive growth opportunities, fuel innovation and tackle global challenges,” the Public Investment Fund stated. (Reuters) CNN: Saudi Arabia preparing to admit Khashoggi was killed – Saudi Arabia is preparing a report that would admit Saudi Arabian journalist, Jamal Khashoggi was killed as a result of an interrogation that went wrong, as reported by CNN. (Reuters) Saudi Arabia cancels annual diplomatic reception in Washington – The Saudi Arabia’s embassy in Washington canceled its annual National Day reception in an email that gave no explanation for the move, which comes amid a diplomatic crisis over the disappearance of journalist Jamal Khashoggi in Turkey. (Reuters) Trump says US attendance uncertain at Saudi Arabia’s investment meeting – US President, Donald Trump said that he is uncertain whether his administration will participate in Saudi Arabia’s investment conference due to the disappearance of journalist Jamal Khashoggi. Trump told reporters that Treasury Secretary Steven Mnuchin, who was scheduled to attend the Riyadh conference, will decide whether to participate for Saudi Arabia’s investment conference. (Bloomberg) Google and others to boycott Saudi investment conference – Alphabet Inc’s Google became the latest company to drop out of a business conference in Saudi Arabia. Further, US private equity firm Bain Capital’s Co-Chairman, Stephen Pagliuca and private equity firm KKR & Co LP’s (KKR.N) Co-President and Co-COO, Joseph Bae & KKR Global’s Chairman, David Petraeus pulls out of planned Saudi investment conference, according to sources. Mastercard’s CEO, Ajay Banga will not attend the conference, according to the company’s spokesman Seth Eisen. Also, BlackRock’s CEO, Larry Fink and Blackstone Group’s CEO, Stephen Schwarzman will no longer attend the conference, sources said. (Reuters, Bloomberg) Islamic Development Bank hires banks for Sukuk meetings – Islamic Development Bank mandates Credit Agricole CIB, LBBW, NATIXIS and Standard Chartered Bank as joint lead managers & bookrunners to arrange a series of fixed income investor meetings/calls in Europe from October 17. Islamic Development Bank is rated ‘Aaa’ by Moody’s, ‘AAA’ by S&P and ‘AAA’ by Fitch (each with ‘Stable’ outlook). (Bloomberg) UAE calls for IMF, World Bank support in MENA region – Addressing the IMF and World Bank Group annual meetings in Bali, Indonesia, UAE’s Financial Affairs Minister, Obaid Humaid Al Tayer, called on the IMF to support growth plans in the MENA region and provide support in financial integration and utilization of technologies in financial services. Al Tayer said, “We look forward to the fund providing further support to countries in the region affected by political conflicts and those affected by refugee crises, and addressing their implications with regards to the countries’ economies”. (GulfBase.com) UAE’s central bank says new public debt law will make market more resilient, benchmark yield curve – The UAE’s central bank stated that a new public debt law which was approved last week will create a more resilient financial market, benchmark the yield curve and provide more diversified sources of financing. The bank’s watchdog also stated that the law will mobilize additional domestic savings and attract capital inflows. (Reuters) Dana Gas buys back about $99mn of Islamic bonds – Dana Gas bought back about $99mn of Islamic bonds this month as the UAE based energy company restructures its debt. The 4% Nile Delta Sukuk Ltd. certificates will be delivered to principal paying agent Bank of New York Mellon for cancellation, the company stated. After the cancellation, the outstanding of the Nile Delta Sukuk would be about $431mn. (Bloomberg) Dubai property prices sink, market equilibrium not expected soon – Dubai property prices declined at an accelerated pace in 3Q2018, with off-plan sales volumes impacted the most amid general market uncertainty, according to property consultancy

- 7. Page 7 of 8 Chestertons. Average sales prices for apartments and villas have declined 6% from 2Q2018 as reported. Off-plan sales volumes were down 31%, compared with 11% for completed units. “The downward price corrections witnessed in 1Q2018 and 2Q2018 have continued throughout 3Q2018, albeit at an increased pace,” as reported. Chestertons stated that the real estate downturn is expected to continue, given the pace of construction activity witnessed over the last couple of years and the number of units still in the pipeline. (Reuters) Dubai Islamic Bank books credit quality – A firming economy and ambitious lending growth trajectory should help Dubai Islamic Bank (DIB) lower its nonperforming loan ratio further this year, closer to the 2018 target of 3% vs. 3.4% in 4Q2017. DIB expects cost of risk on a gross basis may still rise closer to 70bps in 2018 (57bps year-to-date) given potential pressure on household income and rising interest rates. (Bloomberg) Waha Capital acquires stake in Petronash Holdings in $88mn transaction – Waha Capital, a leading investment company based in Abu Dhabi, UAE, acquired a significant minority stake in Dubai-based Petronash Holdings, a global oilfield services and manufacturing company, for $88mn. The deal includes options to further increase Waha Capital’s stake in Petronash Holdings up to 50%. As part of this transaction, Petronash Holdings will establish research and development centers in Chennai (India) and Dammam (Saudi Arabia) to drive innovation and technology integration, with the objective of expanding the company’s service and product lines and widen the customer base. Petronash Holdings is a leading provider of modular well-site packages, chemical injection systems and wellhead control systems to the oil and gas industry. (ADX) Value of Kuwaiti real estate properties unchanged since beginning of fiscal year – The Ministry of Finance’s official figures revealed that the value of real estate properties of Kuwait has not changed since the beginning of the current fiscal year, KD12.82bn, while the cost of damages to these properties reached KD153.39mn, reported Al-Rai daily. The daily has reported that the country’s real estate assets are under the scrutiny of the ministry which is contemplating on the possibility of adopting the unified standards for assessment. On the other hand, the debts owed to the government reached KD1.391bn by the end of September. This amount is higher than the uncollected debts recorded at the beginning of the current fiscal year, KD1.336bn. Therefore, the uncollected debts increased by KD54.53mn or 4.1% within six months. (GulfBase.com) Kuwait Airways signs agreement to buy eight Airbus A330- 800neo planes – Kuwait Airways stated that it has signed an agreement with European planemaker Airbus to buy eight A330-800neo airliners following five months of negotiations. Kuwait Airways expects the deliveries to take place between March 2019 and the end of 2026, the Gulf carrier reported. (Reuters) ABOB posts 9.6% YoY rise in net profit to OMR21.7mn in 9M2018 – Ahli Bank (ABOB) recorded net profit of OMR21.7mn in 9M2018, an increase of 9.6% YoY. Operating income rose 12.3% YoY to OMR44.9mn in 9M2018. Total assets stood at OMR2.3bn at the end of September 30, 2018 as compared to OMR2.0bn at the end of September 30, 2017. Loans & advances and Financing (net) stood at OMR1.9bn (+13.1% YoY), while customers’ deposits stood at OMR1.6bn (+8.1% YoY) at the end of September 30, 2018. (MSM) NBOB posts 10.4% YoY rise in net profit to OMR38.1mn in 9M2018 – National Bank of Oman (NBOB) recorded net profit of OMR38.1mn in 9M2018, an increase of 10.4% YoY. Operating Profit fell 5.8% YoY to OMR49.9mn. Total assets stood at OMR3.5bn at the end of September 30, 2018 as compared to OMR3.4bn at the end of September 30, 2017. Loans, advances and financing activities for customers (net) stood at OMR2.6bn (-2.0% YoY), while customers’ deposits and unrestricted investment accounts stood at OMR2.5bn (+0.4% YoY) at the end of September 30, 2018. (MSM) BKDB posts 4.9% YoY rise in net profit to OMR36.5mn in 9M2018 – Bank Dhofar (BKDB) recorded net profit of OMR36.5mn in 9M2018, an increase of 4.9% YoY. Profit from operations rose 1.4% YoY to OMR50.8mn in 9M2018. Total assets stood at OMR4.3bn at the end of September 30, 2018 as compared to OMR4.1bn at the end of September 30, 2017. Net loans and advances to customers stood at OMR3.2bn (+0.3% YoY), while deposits from customers stood at OMR3.0bn (-1.9% YoY) at the end of September 30, 2018. (MSM)

- 8. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Aug-14 Aug-15 Aug-16 Aug-17 Aug-18 QSEIndex S&P Pan Arab S&P GCC 4.1% 0.1% (0.4%) 0.0% (0.8%) 0.0% (0.0%) (2.5%) 0.0% 2.5% 5.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,227.25 0.8 0.8 (5.8) MSCI World Index 2,055.11 (0.4) (0.4) (2.3) Silver/Ounce 14.69 0.6 0.6 (13.3) DJ Industrial 25,250.55 (0.4) (0.4) 2.1 Crude Oil (Brent)/Barrel (FM Future) 80.78 0.4 0.4 20.8 S&P 500 2,750.79 (0.6) (0.6) 2.9 Crude Oil (WTI)/Barrel (FM Future) 71.78 0.6 0.6 18.8 NASDAQ 100 7,430.74 (0.9) (0.9) 7.6 Natural Gas (Henry Hub)/MMBtu 3.28 1.9 1.9 6.1 STOXX 600 359.31 0.3 0.3 (11.0) LPG Propane (Arab Gulf)/Ton 97.75 1.3 1.3 (1.3) DAX 11,614.16 1.0 1.0 (13.4) LPG Butane (Arab Gulf)/Ton 109.25 1.6 1.6 0.7 FTSE 100 7,029.22 0.5 0.5 (11.0) Euro 1.16 0.2 0.2 (3.5) CAC 40 5,095.07 0.2 0.2 (7.6) Yen 111.77 (0.4) (0.4) (0.8) Nikkei 22,271.30 (1.7) (1.7) (1.5) GBP 1.32 (0.0) (0.0) (2.7) MSCI EM 971.67 (0.9) (0.9) (16.1) CHF 1.01 0.6 0.6 (1.2) SHANGHAI SE Composite 2,568.10 (1.4) (1.4) (27.0) AUD 0.71 0.2 0.2 (8.7) HANG SENG 25,445.06 (1.4) (1.4) (15.2) USD Index 95.06 (0.2) (0.2) 3.2 BSE SENSEX 34,865.10 0.3 0.3 (11.3) RUB 65.66 (0.7) (0.7) 13.9 Bovespa 83,359.76 1.5 1.5 (3.1) BRL 0.27 1.2 1.2 (11.4) RTS 1,146.72 0.5 0.5 (0.7) 73.7 71.8 71.6